Sporadic fighting continued in the Middle East, including in Lebanon, killing hundreds of people, Reuters reported on Thursday. Iranian officials said this breached the terms of a ceasefire that was less than a day old.

Iran’s lead negotiator and parliament speaker, Mohammed Bager Qalibaf, said it would be “unreasonable” to continue talks with the United States on a permanent peace deal under these conditions. Iran’s Islamic Revolutionary Guard Corps said shipping through the Strait of Hormuz stopped after Israel expanded strikes in Lebanon.

Ceasefire Negotiations Breakdown

The White House said the United States would still hold direct talks with Iran despite the ongoing clashes. US Vice President JD Vance is due to lead a US delegation to Islamabad, with the first round of talks set for Saturday morning local time.

CNN reported that Israel struck more than 100 sites across Lebanon on Wednesday. The Israel Defense Forces said it was the largest coordinated set of strikes on Lebanon since the war began.

West Texas Intermediate rose 0.53% to $91.40 at the time of writing.

We recall the significant tensions in late 2025 when sporadic fighting drew threats from Iran and intensified Israeli strikes on Lebanon. WTI crude oil was trading at $91.40, and markets were on edge over a potential shutdown of the Strait of Hormuz. The planned US-Iran talks in Islamabad, led by Vice President Vance, created a highly uncertain environment for energy prices.

Oil Market Volatility Outlook

Following those events, oil prices experienced extreme volatility, with WTI briefly spiking to over $115 per barrel in early 2026 before settling back down. The CBOE Crude Oil Volatility Index (OVX) hit multi-year highs, reflecting the market’s fear, which shows how quickly risk premiums can be priced in. Those weeks taught us that even the threat of disruption is enough to cause significant price swings.

The IRGC’s claim to have stopped shipping never materialized into a full-scale, prolonged closure of the Strait of Hormuz. However, the threats alone were enough to cause war risk insurance premiums for oil tankers to surge, adding a tangible cost to every barrel transiting the critical waterway. About 21% of the world’s daily oil consumption, or roughly 21 million barrels, passes through the strait, making its security non-negotiable for stable prices.

The talks in Islamabad eventually led to a fragile de-escalation, which is why we see prices today hovering in the mid-$80s instead of triple digits. That calm appears to be fraying, with compliance to the temporary agreement now being questioned. This brings the memory of late 2025’s volatility back into sharp focus for traders.

Given the potential for another flare-up, traders should consider buying long-dated call options to hedge against a sudden price spike in the coming weeks. Bull call spreads could be used to lower the upfront cost of positioning for this upside risk. The market demonstrated last year how quickly it can react, and being unprepared for a repeat could be a costly mistake.

The key takeaway from the 2025 events is that the geopolitical risk premium is now more sensitive than it has been in years. Small escalations in the Middle East can now have an outsized impact on oil prices. We should therefore expect volatility to remain elevated and plan our strategies accordingly.

Gold (XAU/USD) traded around $4,705 in early Asian trading on Thursday, after posting modest gains near $4,720 earlier in the session. Prices edged lower as markets reacted to a temporary two-week ceasefire between the US and Iran.

US President Donald Trump said on Tuesday he agreed to suspend bombing and attacks on Iran for two weeks, if Iran re-opens the Strait of Hormuz. Fighting continued in the region, including Israel-Hezbollah clashes in Lebanon, and Iranian officials said this breached the ceasefire terms.

Geopolitical Risk And Gold Pricing

Gold had faced selling pressure in recent weeks on concerns that higher oil prices from the conflict could lift inflation and limit interest-rate cuts. Gold is often sought during geopolitical uncertainty, but it offers no yield, which can weigh on demand when rates are high.

Federal Reserve minutes released on Wednesday said officials at the March meeting still expected to cut rates this year, despite uncertainty from the Iran war and tariffs. Policymakers said they must stay “nimble” as inflation remained above the Fed’s target, while hiring had been mostly flat over the past year.

Central banks added 1,136 tonnes of gold worth about $70 billion in 2022, the highest annual purchase since records began. The World Gold Council reported emerging economies including China, India and Turkey increased reserves.

We remember how the fragile ceasefire between the US and Iran in 2025 caused gold to dip below $4,750, creating a period of market uncertainty. That temporary calm provided a false sense of security, as underlying conflicts continued to simmer. The market dynamics have shifted significantly since then, and we must adapt our strategies accordingly.

Rate Cuts Back On The Table

The breakdown of that ceasefire last year led to sustained inflationary pressures that prevented the Federal Reserve from cutting rates as we had hoped. This kept a lid on gold prices throughout the second half of 2025, even as geopolitical risk remained high. Looking back, the Fed’s need to remain “nimble,” as stated in their March 2025 minutes, translated into a prolonged period of high interest rates.

Now, in April 2026, the picture is changing, as recent data shows inflation is finally beginning to cool. The latest Consumer Price Index (CPI) report for March 2026 showed a decline to 3.1%, the lowest reading in over a year. This has firmly put Fed rate cuts back on the table for later this year.

This shift in monetary policy outlook is a primary catalyst for gold. The CME FedWatch Tool is currently indicating a 65% probability of a rate cut by the September 2026 FOMC meeting. As a non-yielding asset, gold becomes significantly more attractive as interest rates are poised to fall.

For derivative traders, this environment suggests that positioning for upside in gold is prudent. Buying long-dated call options, such as those expiring in December 2026 with strike prices around $5,000, offers a way to capitalize on a potential rally driven by Fed easing. This strategy provides exposure to significant gains while capping the initial risk to the premium paid.

This bullish outlook is further supported by relentless demand from central banks, which has continued unabated. Recent World Gold Council data for the first quarter of 2026 shows global central banks added another 290 tonnes to their reserves. This consistent buying creates a strong floor for the gold price and signals confidence from major institutional players.

While the primary trend appears bullish, implied volatility remains elevated due to lingering geopolitical tensions. Therefore, using strategies like a bull call spread can be effective. This involves buying a call option at a lower strike price and selling one at a higher strike, which lowers the initial cost and defines the risk.

GBP/USD rose by more than 1% on Wednesday after the US and Iran agreed to a Pakistan-brokered two-week ceasefire, reaching about 1.3485. It later fell back towards 1.3400 as questions emerged about how long the deal would last, while JD Vance called it a “fragile truce” and Israel launched its largest assault on Lebanon since the war began, excluding the Hezbollah front from the terms.

UK data released on Wednesday were weak. Halifax house prices fell 0.5% month on month in March versus a forecast 0.1% rise, the S&P Global Construction PMI printed 45.6 versus 44.5 previously, and the RICS housing price balance dropped to -23%, its lowest since early 2024.

Fed Signals And Market Reaction

The Fed’s March minutes showed an 11–1 vote to keep the federal funds rate at 3.50% to 3.75%. Officials noted higher near-term inflation expectations linked to oil prices and tariffs, the median outlook still indicates one 25 basis point cut this year, and some members said a hike could be needed if inflation stays above target.

Thursday includes the BoE Q1 Credit Conditions Survey, plus US core PCE for February, Q4 GDP, and weekly jobless claims, followed by Friday’s March CPI and the University of Michigan’s preliminary April sentiment and inflation expectations. On a 15-minute chart, GBP/USD was 1.3399, above the 200-period EMA at 1.3354, with Stochastic RSI near 81.

We remember well how this time last year, in early 2025, GBP/USD saw a temporary surge on a fragile ceasefire deal. The rally was fleeting, as doubts about the deal and underlying economic weakness in the UK quickly took over. This serves as a critical reminder that geopolitical headlines can create false momentum.

That weak UK housing data from March 2025, with prices falling and surveys plunging, was an early signal of the slowdown that prompted the Bank of England to cut rates twice in the second half of that year. Today, the situation has only marginally improved, with the latest Nationwide House Price Index for March 2026 showing a meager 0.2% annual rise. UK economic growth remains stagnant, with Q4 2025 GDP confirmed at just 0.1%, justifying the market pricing in at least one more BoE rate cut by this autumn.

Strategy Implications For Gbp Usd

Conversely, the Federal Reserve’s hawkish tone from those March 2025 minutes proved prescient, as they only delivered one rate cut late in the year. US inflation has remained stubbornly persistent, with the most recent core PCE reading for February 2026 coming in at 2.9%, still well above the Fed’s target. This wide and persistent policy divergence between a dovish BoE and a patient Fed continues to put fundamental pressure on the pound.

Given this backdrop, we should view any strength in GBP/USD as an opportunity to establish bearish positions. Buying put options with expiry in the next 4-6 weeks provides a clear, risk-defined way to trade an expected decline. This strategy allows us to profit from the fundamental weakness without being overexposed to the kind of sharp, headline-driven reversals we saw last year.

The sharp spike to 1.3485 in 2025 reminds us that volatility can be unpredictable. Therefore, selling out-of-the-money call spreads could be an effective strategy to generate income and capitalize on the view that the pair’s upside is limited. This is particularly attractive if the pair rallies towards the 1.2700 resistance level, a key technical barrier throughout early 2026.

UK housing survey data from RICS showed a house price balance of -23% in March. This was below the forecast of -18%.

The negative balance indicates that more survey respondents reported price falls than rises. The result points to weaker price momentum than expected for March.

Uk Housing Data Signals Faster Slowdown

The March housing price data came in significantly weaker than anyone expected, falling to -23 against a forecast of -18. This is the clearest sign yet that the UK economy is slowing faster than anticipated. We believe this puts immediate pressure on the Bank of England to pivot towards a rate cut sooner than the market has been pricing.

We should anticipate a weakening of the British Pound against the dollar and the euro over the coming weeks. The latest data from the Office for National Statistics shows UK inflation has been stubborn at 2.9%, but this housing report will likely outweigh that, making rate cuts the primary market driver. Therefore, buying put options on GBP/USD with a June expiry looks like a prudent way to position for this expected slide.

This negative housing sentiment directly impacts UK equities, especially domestically-focused companies on the FTSE 250. We expect stocks in the construction and banking sectors to underperform significantly. Looking at options on major housebuilders, we see implied volatility has already jumped 15% this morning, suggesting the market is scrambling to price in this new risk.

From a historical standpoint, this downturn feels more severe than the brief cooling-off period we saw in the third quarter of 2025. Back then, the market bounced back on hopes of a soft landing, but this data suggests the full impact of the rate hikes from 2024 and 2025 is still filtering through the economy. This increases the likelihood that broad market volatility will remain elevated for the next month.

USD/JPY fell 0.66% on Wednesday, dropping from near 160.00 to around 158.50. The 160.00 area has been tested once since Tokyo’s intervention campaign in July 2024, and the move formed lower highs with price holding just below the 15-minute 200-period EMA into the Asian open.

The drop followed news of a two-week US–Iran ceasefire and Tehran’s agreement to reopen the Strait of Hormuz. This reduced demand for safe-haven assets after supporting the US Dollar and crude oil through March, which helped the Yen regain ground.

Ceasefire Risks And Market Framing

The ceasefire remains uncertain, as neither side has signed the underlying 10-point framework. Markets are treating the two-week period as a limited window rather than a full settlement.

Japan’s calendar is light through Friday, while the Bank of Japan is expected to hike on 28 April, with about a 70% probability priced in. US data due includes core PCE and Q4 GDP on Thursday, then March CPI plus University of Michigan sentiment and inflation expectations on Friday.

On the 15-minute chart, USD/JPY was 158.57, below the 200-period EMA at 158.92, with Stochastic RSI near 14. Resistance is near 158.92.

The recent dip in USD/JPY, caused by the temporary US-Iran ceasefire, should be seen as an opportunity to position for high volatility, not a new trend. The two-week agreement is fragile, creating a countdown that could snap safe-haven demand right back into the US Dollar. This pullback below 159.00 gives us a better entry point for strategies that benefit from sharp market swings.

Upcoming US inflation data is the most immediate catalyst and presents a clear trading opportunity. We should consider buying short-dated options straddles to profit from a large price move following the CPI and PCE releases, regardless of the direction. Looking at similar situations, we can recall how the March 2024 CPI report came in hotter than expected at 3.5%, causing a significant repricing in currency markets and showing how a surprise can drive the dollar higher.

BoJ Meeting And Event Risk

On the Japanese side, we should be cautious of the upcoming Bank of Japan meeting on April 28, even with a rate hike heavily priced in. When the BoJ hiked for the first time in 17 years back in 2024, the yen actually weakened as the bank’s forward guidance remained very cautious. A similar “sell the news” reaction is a distinct possibility, making it risky to be outright long the yen into the event.

The fragile geopolitical situation means the risk of the ceasefire failing is high, which would cause the pair to spike back toward 160.00. We can cheaply hedge for this outcome by purchasing out-of-the-money call options. This provides a limited-risk way to profit from a sudden return of the safe-haven bid for the US dollar.

Finally, the 160.00 level remains a critical line in the sand due to the risk of official intervention, which we saw in July 2024. Just as Japan intervened to defend the yen back in 2022, any strong push above 160.00 will likely be met with resistance, making it a key level to sell against. This creates a ceiling on the pair for now, unless a major new catalyst emerges.

USDJPY trades at 159.141, up 0.148 (+0.09%), after a high of 159.242 and a low of 158.896.

The yen is still down about 2% since the conflict began, even after the ceasefire cooled oil and eased some stagflation pressure.

Markets remain focused on Kazuo Ueda and the April 28 BOJ decision, with traders still trying to judge whether the next move is a hike or another cautious hold.

The yen has stabilised rather than strengthened decisively. USDJPY is trading at 159.141, which shows that lower oil has helped, but only to a point.

The two-week ceasefire between the US and Iran cooled crude and reduced some of the pressure on Japan’s import bill, which gave the yen a bit of room to recover from the most stressed part of the move.

That relief has not turned into a clean reversal. The pair is still sitting close to the upper end of the recent range, and the market is still carrying the memory of the move toward 160.461. Traders are treating the ceasefire as temporary and conditional, not as a durable end to the energy shock.

A cautious near-term view still favours choppy trade in the upper 150s while the truce remains fragile.

Lower Oil Helps Japan, but the Damage Has Not Disappeared

The yen’s earlier weakness was tied directly to the energy shock. Japan imports most of its energy, so higher crude lifted import costs and worsened the growth-inflation mix. That is why the yen stayed weak even when safe-haven logic might normally have helped it.

The ceasefire has softened that problem, but it has not removed it. Shipping through Hormuz is still not fully normal, Israeli strikes on Lebanon continue to cloud regional sentiment, and the market still doubts how durable the current arrangement really is.

The drop in oil prices has reduced immediate stagflation fear, yet it has not fully repaired confidence in Japan’s external outlook.

That leaves the yen with partial support rather than a full macro tailwind.

BOJ Expectations Are Now the Main Domestic Driver

With the oil panic easing slightly, attention has shifted back to the Bank of Japan. Governor Kazuo Ueda has kept the tightening bias alive, but markets still do not know how forceful the next signal will be.

The Bank of Japan will probably increase its benchmark rate this month to avoid falling behind on controlling inflation, according to a former executive director at the central bank https://t.co/NHIRhR21ce

The BOJ left rates at 0.75% in March and said rising oil costs could feed underlying inflation, while officials have also stressed that financial conditions remain accommodative and real rates are still negative.

That creates a narrow and unstable balance. If the BOJ leans clearly toward another hike, the yen can find more support.

Japanese workers’ wages adjusted for inflation rose at the fastest pace since 2021, backing the case for the Bank of Japan to consider a rate hike as soon as this month https://t.co/CZFuzjiE8d

If Ueda stays cautious and emphasises the economic risks from the Middle East conflict, traders may conclude the BOJ wants more time, which would leave USDJPY vulnerable to another push higher.

Markets have already been pricing a meaningful chance of a move around the April 27–28 meeting window, so the risk is no longer just about direction. It is about whether the BOJ delivers the confidence traders expect.

USDJPY Technical Outlook

USDJPY is trading near 159.14, holding steady after pulling back from its recent high around the 160.46 level. Price action shows a pause in momentum following the prior rally, with the pair now consolidating in a tighter range just below key resistance.

The structure suggests buyers are still present, but upside momentum has cooled as the market digests gains near the upper boundary.

From a technical standpoint, the trend remains constructively bullish but softening in the near term. Price is hovering around the 5-day (159.19) and 10-day (159.23) moving averages, which are now flattening and offering immediate support.

The 20-day (159.18) sits just beneath, reinforcing a clustered support zone, while the broader structure continues to hold above the rising 30-day (157.18), keeping the underlying uptrend intact.

Key levels to watch:

Support: 159.00 → 158.40 → 157.20

Resistance: 159.90 → 160.50 → 161.10

The pair is currently consolidating just below the 159.90–160.00 resistance area. A clean break above this region would likely reopen the path toward 160.50, with scope for further upside if momentum builds.

On the downside, 159.00 is acting as immediate support. A break below this level could trigger a deeper pullback toward 158.40, though such a move would likely remain corrective unless the broader trend structure weakens.

Overall, USDJPY is in a controlled consolidation within an uptrend, with price holding above key moving averages. The next directional move will likely hinge on whether buyers can reclaim the 160.00 level or if sellers push the pair into a deeper retracement.

What Traders Should Watch Next

The next move depends on three linked drivers: whether the ceasefire holds, whether oil stays off the highs, and whether Ueda sharpens or softens the BOJ’s pre-meeting message. If crude stays lower and BOJ language firms up, the yen can extend its recovery.

If the truce weakens or the BOJ hesitates, USDJPY may stay pinned near the highs and start leaning back toward 160.

Why Is USDJPY Holding Near 159 Instead Of Falling More Sharply?

Lower oil prices have taken some pressure off Japan’s import bill, but the yen is still dealing with Bank of Japan uncertainty and a ceasefire that markets view as fragile rather than permanent. That has kept USDJPY close to 159.14 instead of driving a deeper drop.

How Did The US-Iran Ceasefire Help The Yen?

The ceasefire triggered a sharp fall in oil and reduced near-term stagflation fears. Japan is highly exposed to imported energy costs, so any cooling in crude usually gives the yen some relief.

Why Has The Yen Still Fallen About 2% Since The Conflict Began?

The broader move still reflects the damage from the earlier oil shock. Higher fuel costs worsened Japan’s growth-inflation mix and weakened the yen even when risk aversion was high. The current pullback in USDJPY has only recovered part of that move.

What Are Markets Expecting From The BOJ Now?

The BOJ kept rates at 0.75% in March, but markets have continued to price a meaningful chance of another move around the late-April meeting. The uncertainty is no longer just about whether the BOJ can hike, but whether Kazuo Ueda will signal that clearly enough before the decision.

Why Does BOJ Guidance Matter So Much For USDJPY?

USDJPY is sitting close to a crowded level, so even small shifts in BOJ language can move expectations quickly. A clearer tightening message would support the yen, while another cautious hold-or-wait tone could leave the pair leaning back toward 160.

Start trading now – Click here to create your real VT Markets account

USDX trades at 98.679, up 0.043 (+0.04%), but it remains on track for a weekly drop of more than 1%.

A two-week US-Iran ceasefire and lower oil prices have eased the inflation shock that supported the dollar through March.

One-year US inflation expectations rose to 3.4% in March from 3.0% in February, while expected gasoline-price inflation jumped to 9.4%.

The dollar is no longer trading with the same urgency that drove it higher through the worst of the Iran shock. USDX is holding near 98.679, a modest rebound on the day, but still well below the recent peak at 100.481. The main reason is straightforward.

A two-week ceasefire has reduced the immediate need for safe-haven positioning, and the drop in oil has pulled out part of the inflation premium that had been supporting the greenback.

The dollar and oil are trading in lockstep in the wake of the US-Iran ceasefire this week, tightening the relationship between them to near-record levels https://t.co/raserekvOB

That has changed the tone, but not the full structure. The ceasefire is temporary, Hormuz traffic is still not fully normal, and markets are still treating the current calm as conditional rather than durable. That keeps the dollar softer than it was, but not yet in a clean bearish trend.

Lower Oil Has Softened the Dollar’s Main Support

The dollar’s March strength came from two linked forces: war risk and higher-for-longer rate pricing. Oil fed both. Once crude fell sharply after the ceasefire announcement, the market had less reason to keep chasing the dollar higher.

The dollar fell against all its major peers after the US and Iran agreed to a two-week ceasefire, sapping demand for the currency as a haven https://t.co/4voiHcsucM

That matters because the US still benefits when energy shocks hurt importers more than exporters, but that advantage narrows when crude retreats. The market is now pricing in a less severe inflation spillover than it was one week ago, which has made defensive dollar longs less attractive.

The problem for dollar bears is that oil has eased, not normalised. Shipping disruption, political uncertainty, and the risk of renewed escalation still leave a residual premium in rates and currencies.

Inflation Still Limits the Downside

The dollar has weakened, but inflation risk remains high enough to prevent the market from rebuilding an easy Fed-cut story. March survey data showed one-year inflation expectations rising to 3.4% from 3.0%, while expected gasoline-price inflation jumped to 9.4%, the highest since the 2022 energy shock.

That keeps the rates backdrop sticky. A lower dollar usually needs either cleaner disinflation or visibly weaker growth data. Right now, the market has neither.

The ceasefire has cut one part of the problem, but households are still expecting higher fuel costs, and businesses are still facing elevated logistics prices.

That is why the dollar is slipping in an orderly way instead of breaking lower.

CPI is the Next Real Test

The next move in USDX depends on whether the upcoming CPI data confirms that the conflict has already filtered into broader price pressure. Service data has already pointed in that direction. Input prices rose at the fastest pace in more than 13 years, while growth slowed, which is exactly the kind of mix that makes central banks cautious.

Investors in the $31 trillion Treasury market are going into a closely-watched report on consumer prices hedging against more losses in government bonds, as a fragile truce between the US and Iran takes hold. https://t.co/7gFvFLEekL

If CPI comes in firm, the dollar can stabilise quickly because traders will go back to higher-for-longer thinking. If CPI lands softer than feared, the latest pullback can extend because the market will have room to remove more of the inflation premium that built through March.

That leaves the dollar trading off two clocks at once: the truce clock and the inflation clock.

USDX Technical Outlook

The US Dollar Index (USDX) is trading near 98.68, continuing its pullback after failing to sustain gains above the 100.48 high. Price action shows a clear shift in momentum, with a series of lower highs forming and recent candles reflecting sustained selling pressure.

The move lower has now pushed the index beneath key short-term support, suggesting the bullish phase has paused and a corrective structure is developing.

From a technical standpoint, the trend is tilting bearish in the short term. Price is trading below the 5-day (99.09) and 10-day (99.46) moving averages, both of which are turning lower and acting as immediate resistance.

The 20-day (99.42) is also flattening and beginning to roll over, reinforcing the loss of upside momentum. This alignment indicates that rallies are likely to face selling pressure unless the index can reclaim higher ground.

Key levels to watch:

Support: 98.70 → 97.90 → 96.40

Resistance: 99.40 → 100.00 → 100.50

The immediate focus is on the 98.70 zone, which price is currently hovering around. A sustained break below this level could open the path toward 97.90, where stronger support may emerge.

On the upside, 99.40 now acts as near-term resistance. A move back above this level would suggest stabilisation and could lead to a recovery toward the 100.00 handle.

Overall, USDX is showing signs of short-term weakness after rejecting the 100 level. The structure now favours consolidation or further downside unless buyers can regain control above the 99.40–100.00 region.

What Traders Should Watch Next

The market is now weighing three variables together: whether the ceasefire holds, whether shipping through Hormuz improves enough to keep oil lower, and whether CPI confirms or challenges the inflation story.

A stable truce and softer inflation would likely keep pressure on the dollar. A renewed threat to Hormuz or a hotter inflation print would likely pull buyers back quickly.

Why is the Dollar Index Holding Near 99 Instead of Falling More Sharply?

The dollar has lost part of its war-driven safe-haven premium, but traders have not fully abandoned it because the ceasefire is temporary, Hormuz disruptions have not fully cleared, and inflation risk is still high. Recent market coverage also showed the dollar stabilising after touching a one-month low near 98.525.

What Caused the Weekly Drop in USDX?

The biggest driver was the two-week US-Iran ceasefire, which helped push oil lower and reduced fears of a more immediate inflation shock. That made defensive dollar positioning less urgent than it was during the worst of the March energy spike.

Why Does Oil Still Matter for the Dollar Even After the Ceasefire?

Oil still shapes inflation expectations and Fed pricing. Even after the truce, Brent and WTI remained elevated because the market still doubts how quickly flows through Hormuz can normalise. As long as energy stays expensive, the dollar keeps some support from higher-for-longer rate expectations.

Why Hasn’t the Ceasefire Fully Reversed Safe-Haven Demand?

Because the pause looks fragile. Market reports still describe the truce as uncertain, with continued attacks in the region and ongoing limits on ship crossings through Hormuz. That keeps traders from treating the current calm as a full resolution.

What Are Markets Waiting for Next on the Macro Side?

The next major test is US March CPI. Inflation expectations have already moved higher, and the market wants to see whether the oil shock has started feeding into official price data strongly enough to keep the Fed cautious.

Start trading now – Click here to create your real VT Markets account

ExxonMobil sits at the centre of one of the biggest market debates: whether traditional oil majors can adapt to a lower-carbon future without sacrificing profitability.

Exxon is maintaining an oil-first strategy, backed by strong global demand and cash flow

The company is investing selectively in carbon capture, hydrogen, and low-emission fuels

For traders, XOM remains closely tied to oil prices, geopolitics, and energy demand cycles

Recent headlines have highlighted a shift in sentiment across the energy sector, with oil majors moving from a period of strong gains into renewed volatility. A key trigger has been the disruption to Exxon’s operations linked to geopolitical tensions in the Middle East.

According to recent reporting, Exxon has seen around 6% of its global output affected due to conflict-related disruptions in the region. At the same time, broader energy markets have started to soften after a strong run, with oil prices pulling back as supply concerns fluctuate and demand expectations adjust.

This combination has created pressure on XOM stock in the short term:

Production disruptions raise uncertainty around near-term output.

Shifting market sentiment moves energy stocks from momentum to reassessment.

What makes this particularly important is how quickly the narrative can change. Energy stocks often move in cycles, and the same factors that drove record gains, such as tight supply and geopolitical risk, can also lead to sharp pullbacks when conditions stabilise or expectations shift.

This is where Exxon’s strategy becomes relevant again.

When the market moves from strong gains into uncertainty, investors tend to reassess:

How resilient are earnings across cycles?

Whether production growth can offset disruptions.

How well-positioned are companies for longer-term structural shifts?

In other words, the recent decline is not just about short-term headlines. It is a reminder that Exxon’s performance still sits at the intersection of oil markets, geopolitics, and long-term energy transition dynamics.

The energy transition is often described as a simple shift away from oil. Markets, however, rarely move in simple lines. The real story is more complicated, and ExxonMobil sits right in the middle of it.

XOM still generates the bulk of its earnings from oil and gas. That alone makes it highly sensitive to crude prices, geopolitical risk, and the broader supply-demand balance in global energy markets.

Exxon Mobil says 6% of its global first-quarter production was knocked out as the US-Israel war on Iran paralyzed much of the Persian Gulf energy industry https://t.co/XYGLeLdxMn

At the same time, the company is also trying to position itself for a lower-carbon future, though on its own terms and in its own chosen areas.

That creates the central tension behind XOM stock. Exxon is not trying to reinvent itself as a renewable energy company. It is trying to remain an oil giant while selectively building businesses that fit the next phase of energy demand.

Exxon’s Strategy: Oil First, Transition Second

Exxon’s strategy stands out because it is more cautious and more selective than that of some of its peers. Rather than making an aggressive public pivot into wind and solar, the company has chosen to keep its core oil and gas engine firmly in place.

That decision reflects the company’s view that the world will continue to need large volumes of hydrocarbons for decades, even as lower-emission technologies gain ground.

In practice, that means Exxon is still allocating substantial capital toward upstream production, particularly in areas where it believes returns are strongest and project economics remain attractive.

Its expansion in places such as Guyana and the Permian Basin reflects that approach. These are not side projects. They are central to Exxon’s current earnings power and long-term production strategy.

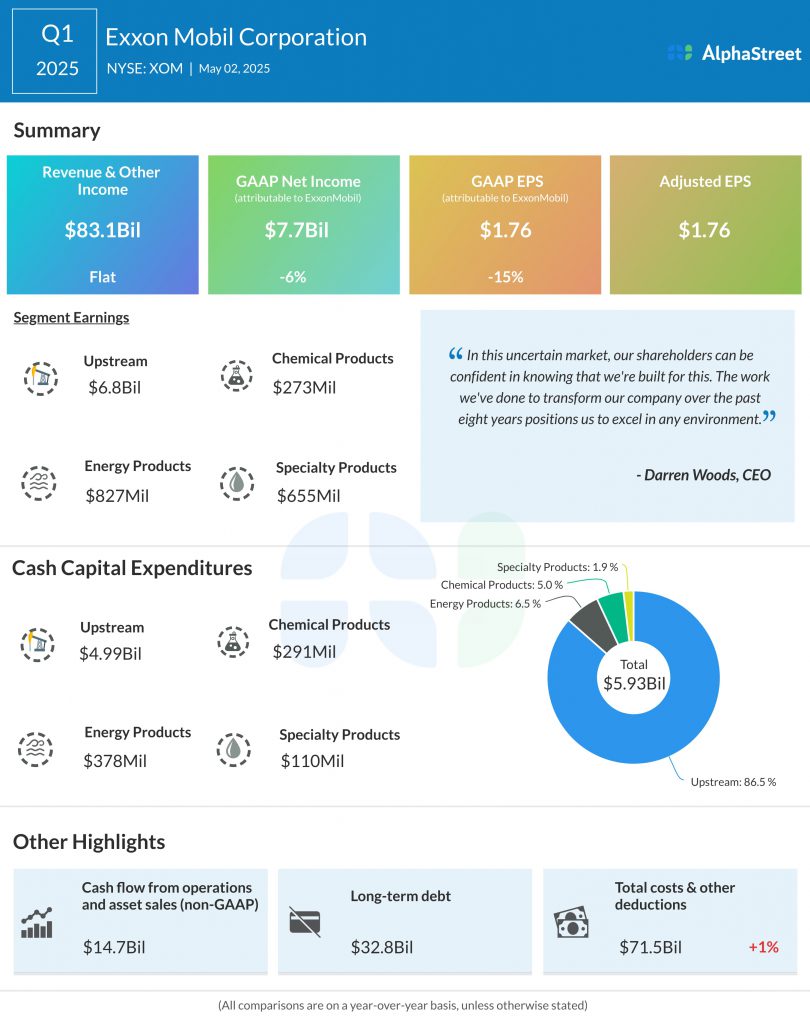

Source: AlphaStreet

This oil-first model gives the company a few important advantages:

High cash flow during strong energy cycles: When crude prices rise, Exxon’s traditional operations generate the cash needed to support dividends, buybacks, and long-term investment.

Operational familiarity and scale: The company understands large-scale hydrocarbon production better than almost anyone in the industry.

Capital discipline: Management can continue investing in areas where returns are visible, rather than chasing growth in unfamiliar markets.

The trade-off, of course, is perception. Exxon can look slower to transition than its peers that market themselves more aggressively around renewables. But the company appears comfortable with that distinction. Its message is clear: remain strong in oil first, then build transition exposure in areas where it believes the returns are commercially durable.

A Different Take on the Energy Transition

That does not mean Exxon is ignoring the energy transition. It means it is approaching it in a different way.

Rather than spreading itself across a broad range of renewable technologies, Exxon has concentrated its lower-emission strategy around a narrower set of industrial opportunities. These are areas where it believes its engineering capability, industrial scale, and energy infrastructure experience can provide a competitive edge.

The company’s transition focus is concentrated in several key areas:

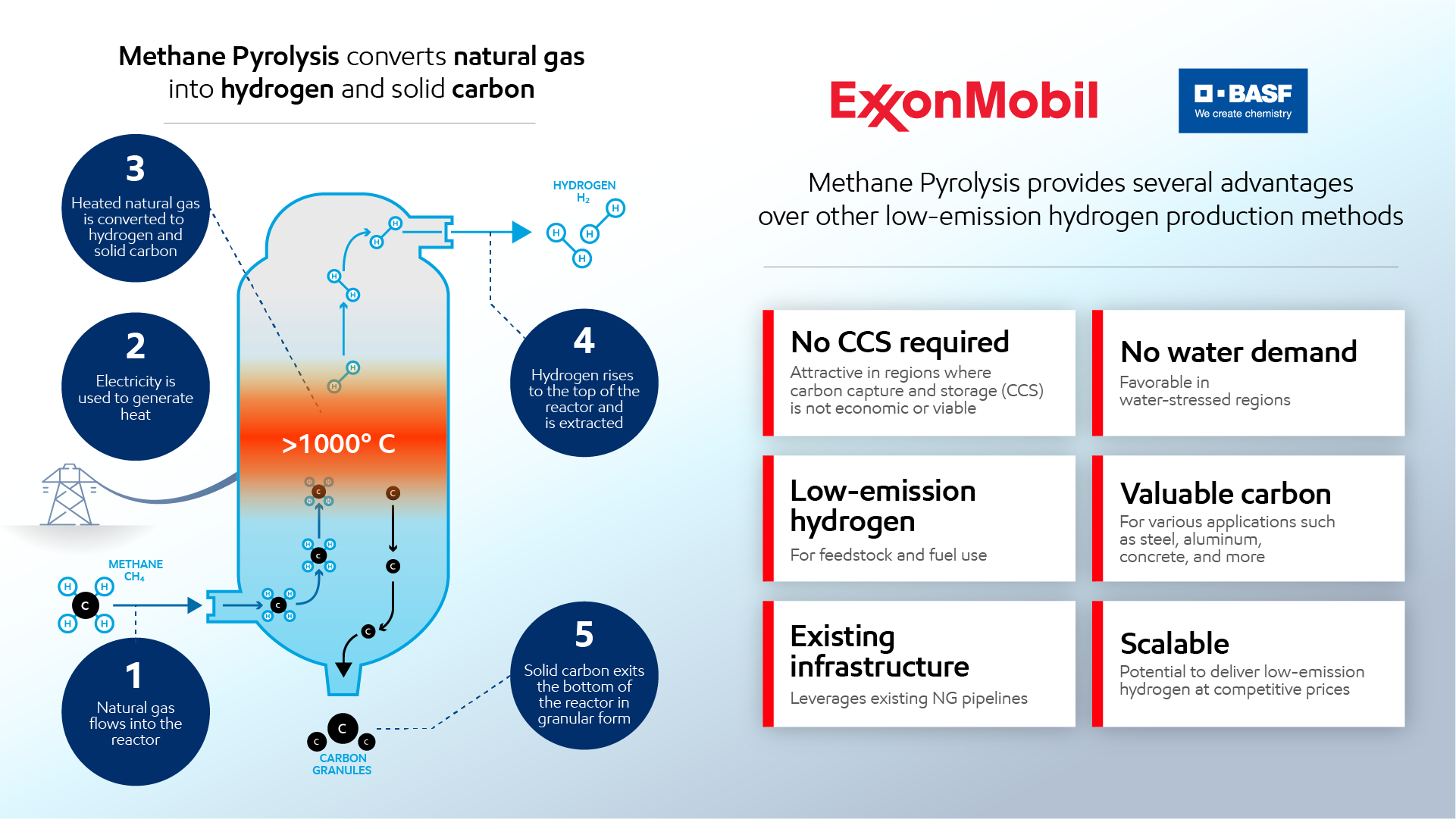

Carbon capture and storage (CCS): Exxon sees carbon capture as one of the most commercially viable pathways for reducing industrial emissions at scale.

Hydrogen: The company is building exposure to hydrogen as a fuel source for sectors that are difficult to electrify.

Low-emission fuels: This includes fuels aimed at industrial and heavy transport use cases where conventional electrification may be less practical.

Source: ExxonMobil

This is an important distinction. Exxon is not trying to win the consumer-facing renewable race. It is targeting industrial decarbonisation, where projects tend to be larger, longer-duration, and more aligned with the company’s existing capabilities.

That selective approach also helps explain why the market remains divided on Exxon’s transition story. Some investors see discipline and realism. Others see hesitation. In truth, the company is making a deliberate bet that the most profitable parts of the transition will not necessarily be the loudest ones.

As Darren Woods, CEO of ExxonMobil, has repeatedly argued, the world still needs a secure energy supply at scale, and reducing emissions must happen in a way that fits industrial reality rather than political slogans alone.

Oil Demand Is Still the Foundation

One of the reasons Exxon can maintain this strategy is that oil demand remains more resilient than many early transition narratives assumed.

Even as cleaner technologies gain market share, large parts of the global economy still depend on hydrocarbons. Aviation, shipping, freight, petrochemicals, and heavy industry continue to rely heavily on oil and gas. Emerging economies also remain major engines of incremental energy demand, particularly where infrastructure for alternatives is still developing.

This means Exxon’s core business still rests on a powerful foundation:

Global oil demand remains above 100 million barrels per day: That level of consumption continues to support large-scale upstream investment.

Demand is proving sticky in hard-to-electrify sectors: Industrial transport and heavy manufacturing still rely on traditional fuels.

Energy security remains politically important: Governments continue to prioritise stable access to oil and gas, especially during periods of geopolitical tension.

This matters for XOM stock because it reinforces the relevance of Exxon’s core earnings engine. The transition may be real, but so is the continued need for hydrocarbons. For now, Exxon is operating in the overlap between those two realities.

Cash Flow Is the Real Advantage

Exxon’s transition strategy only works because its traditional business continues to generate the cash to support it.

That cash flow is arguably the company’s biggest strategic advantage. In stronger oil environments, Exxon has the ability to fund shareholder returns and future-facing projects at the same time. That is a powerful position, particularly when compared with transition strategies that rely more heavily on external capital or lower-margin growth areas.

The company’s financial strength supports several priorities at once:

Dividend support: XOM remains attractive to income-focused investors because of its long-standing dividend profile.

Shareholder returns: Buybacks and balance-sheet flexibility are easier to sustain when operating cash flow is strong.

Transition investment: New spending on carbon capture, hydrogen, and low-emission technologies can be funded internally.

However, this also creates a subtle tension. Strong oil profits give Exxon more flexibility, but they can also reduce the market urgency to diversify. In other words, the better the oil cycle is for Exxon, the easier it becomes to keep the transition on a selective rather than transformative path.

That is why traders need to look beyond the headline cash flow number. The real question is how effectively Exxon uses the strength of its traditional business to prepare for a changing energy mix.

Geopolitics Still Favours Oil

The energy transition is also shaped by geopolitics, and in the short to medium term, geopolitics still tends to favour oil.

Tensions in the Middle East, OPEC production decisions, sanctions, shipping disruptions, and supply shocks all have a direct effect on crude prices. Because Exxon’s earnings remain closely linked to hydrocarbon markets, the company often benefits when supply risks push energy prices higher.

This is one of the reasons EXXON continues to hold macro relevance. It is not just a stock tied to company-specific execution. It is also a market proxy for broader energy security concerns.

Several geopolitical drivers continue to matter:

Middle East tensions: These can quickly raise supply-risk premiums in oil markets.

OPEC and producer coordination: Production cuts or discipline can support oil prices and improve earnings visibility for Exxon.

Sanctions and trade routes: Disruptions to global flows can reinforce the value of established producers with global scale.

From a trading perspective, this means XOM often becomes more attractive when oil volatility rises. Even if the long-term transition story remains a live debate, short-term market conditions can still swing strongly in favour of Exxon’s legacy strengths.

Exxon’s performance remains closely tied to crude oil movements. Traders often monitor XOM alongside broader energy markets and USOil to track shifts in supply and demand.

What Traders Should Watch

For traders, XOM is best understood as a stock where corporate fundamentals and macro conditions are tightly linked.

The first and most obvious variable is oil itself. Exxon’s earnings power still responds directly to crude prices, so any sustained move in WTI or Brent is likely to shape sentiment around the stock.

But the stock is not driven by oil alone. Traders should also watch whether Exxon’s capital allocation supports the case that the company is preparing intelligently for the next phase of the energy market.

A few signals matter most:

Oil price trends: These remain the strongest short-term driver of earnings expectations.

Capital expenditure discipline: The market wants to see spending support growth without eroding returns.

Transition project progress: Carbon capture and hydrogen investments matter more when they start to show commercial traction.

Dividend durability: Exxon’s appeal for many investors still depends on reliable shareholder returns.

Geopolitical developments: These can reprice the stock quickly through the oil channel, even before company-specific news arrives.

This is where interpretation matters. A trader looking at XOM is not just analysing an oil major. They are also analysing the shape of the global energy cycle, the durability of oil demand, and whether the market is rewarding traditional profitability over transition ambition.

As energy markets evolve, traders can also explore opportunities across oil, commodities, and global energy stocks through CFD Shares on the VT Markets app.

How XOM Fits Into a Broader Trading Strategy

XOM works well in a broader trading strategy because it can express multiple market views at once.

For some traders, it is primarily a crude oil proxy with equity characteristics.

For others, it is a dividend-backed energy exposure with lower volatility than pure commodity instruments. It can also serve as a way to gain exposure to inflationary or geopolitically driven market environments.

Within portfolio construction, XOM can play several roles:

Energy exposure with company-specific cash flow support

A real-asset hedge during inflationary periods

A more stable complement to commodity-linked trades

A way to monitor how the market is pricing the tension between oil demand and energy transition policy

It also creates natural links to other tradable assets. Traders following XOM often keep one eye on crude, one eye on broader energy indices, and another on transition-sensitive names across industrials and clean energy. That wider context is what makes the stock useful. It is not just a single-company story. It is a window into how markets are balancing old energy and new energy at the same time.

Bottom Line

For traders and investors, that makes XOM stock a useful name to watch. It remains deeply tied to oil markets, but it also offers insight into how one of the world’s largest energy companies is navigating the shift toward a lower-carbon future without giving up the earnings power of its traditional business.

Create a live VT Markets account today to access our platform features, including market insights and educational content.

FAQs

What is XOM stock?

XOM stock represents shares of Exxon Mobil Corporation, one of the world’s largest oil and gas companies.

Is ExxonMobil investing in clean energy?

Yes. Exxon is investing in carbon capture, hydrogen, and low-emission fuels, although it remains heavily focused on oil and gas.

Why is XOM stock tied to oil prices?

Exxon’s revenue and profits are largely driven by oil and gas production, making its stock highly sensitive to energy prices.

Is XOM a good dividend stock?

XOM is known for its strong dividend, typically offering yields in the 3% to 4% range, supported by cash flow from operations.

Can ExxonMobil adapt to the energy transition?

Exxon is pursuing a selective strategy, focusing on industrial decarbonisation while maintaining its core oil business.

Start trading now – Click here to create your real VT Markets account

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

As part of our commitment to provide the most reliable service to our clients, there will be maintenance this weekend.

Maintenance Details:

Please note that the following aspects might be affected during the maintenance:

1. The price quote and trading management will be temporarily disabled during the maintenance. You will not be able to open new positions, close open positions, or make any adjustments to the trades.

2. There might be a gap between the original price and the price after maintenance. The gaps between Pending Orders, Stop Loss, and Take Profit will be filled at the market price once the maintenance is completed. It is suggested that you manage the account properly.

3. During the maintenance period, VT Markets APP will not be available. It is recommended that you avoid using it during the maintenance.

4. During the maintenance hours, the Client portal will be unavailable, including managing trades, Deposit/Withdrawal and all the other functions will be limited.

The above data is for reference only. Please refer to the MT4/MT5 software for the specific maintenance completion and marketing opening time.

Thank you for your patience and understanding about this important initiative.

If you’d like more information, please don’t hesitate to contact [email protected]