The US Dollar Index (DXY) traded near 99.65 in Asian hours on Monday, rising above 99.50. It reached its highest level since late November 2025 as tensions grew in the Middle East.

US President Donald Trump said he does not want to negotiate an end to the war with Iran and demanded that Tehran capitulate, while US and Israeli airstrikes continued. Israel’s Defence Minister Israel Katz warned Lebanon on Saturday to disarm Hezbollah or “pay a very heavy price”.

Middle East Tensions Lift Safe Haven Demand

The US Dollar strengthened against other currencies as demand rose for safer assets amid the conflict. The move was also linked to higher oil prices.

US labour data presented a counterweight to the Dollar’s rise. The US Bureau of Labor Statistics reported that Nonfarm Payrolls fell by 92,000 in February.

This followed a January increase of 126,000, revised from 130,000. The February result also missed the forecast for a 59,000 rise.

We are seeing the US Dollar Index push above 99.50, a level not seen in over three months, driven by escalating conflicts in the Middle East. This safe-haven rush is the dominant force in the market right now. However, the market is also trying to digest a shockingly weak US jobs report from last Friday.

Trading Strategy Under Higher Volatility

The sharp conflict between a risk-off geopolitical event and poor domestic economic data creates significant uncertainty, which is a recipe for higher volatility. The Cboe Volatility Index (VIX) has already jumped to over 24, climbing from the mid-teens just a few weeks ago. This environment suggests that buying options to play on large price swings, rather than just direction, could be a primary strategy in the coming weeks.

The geopolitical tensions have also sent crude oil prices surging, with WTI crude recently breaking past $95 a barrel for the first time since late 2024. This supports the dollar against currencies of energy-importing nations like the Euro and the Japanese Yen. Derivative traders might look at call options on the USD against these currencies to ride the current safe-haven trend.

At the same time, we cannot ignore that the US economy lost 92,000 jobs, which is a major reversal from expectations of a 59,000 gain. While we saw volatile jobs data throughout 2025, a miss of this magnitude is a serious red flag for the health of the US economy. This weakness suggests the dollar’s current strength is built on a shaky foundation.

This weak employment figure immediately impacts expectations for Federal Reserve policy. Fed funds futures are already shifting to price in a higher probability of an interest rate cut at the next FOMC meeting. A rate cut would be bearish for the dollar, creating a direct conflict with the current rally.

Given these opposing forces, traders should consider strategies that hedge against a sudden reversal. For instance, while holding a long dollar position via futures, one could buy out-of-the-money put options on a currency pair like USD/JPY. This provides protection if the negative economic data begins to outweigh the safe-haven demand, causing the dollar’s rally to quickly unwind.

Create your live VT Markets account and start trading now.

Start trading now – Click here to create your real VT Markets account

WTI crude rose for a fifth straight session, opening with a gap up and trading near $110.60 a barrel in Asian hours on Monday. It reached $110.73, its highest level since June 2022, amid concerns that a prolonged Middle East conflict could disrupt energy supplies.

Middle Eastern producers reduced output as the Strait of Hormuz remained closed due to the Iran war. Kuwait announced precautionary cuts, and Iraq’s southern output fell to 1.3 million barrels per day from 4.3 million.

Supply Shock In The Gulf

Qatar’s energy minister Saad Sherida Al‑Kaabi told the Financial Times that Gulf producers may halt exports within weeks. The report said oil could rise to $150 per barrel.

The Telegraph reported that US President Donald Trump described higher oil prices as a “very small price to pay” in the context of defeating Iran. Trump also posted that Iran’s option was unconditional surrender and that he would help choose Iran’s next leader afterwards.

The Iran war entered its second week with no stated end point. Mojtaba Khamenei was appointed supreme leader just over a week after Ali Khamenei was killed in US-Israeli strikes.

A correction on March 9 at 2:30 GMT revised the headline to “over three-year highs”, not “54-month highs”.

Derivatives Positioning And Risk

With WTI crude breaking $110, the immediate focus should be on bullish strategies using derivatives. We are seeing a massive surge in call option buying, particularly for contracts with strike prices of $120 and $130 expiring in the next two months. The CBOE Crude Oil Volatility Index (OVX), a key measure of oil price volatility, has already surged past 60, reflecting extreme market uncertainty and making options premiums very expensive.

We should remember the price action following the conflict in Ukraine back in early 2022, when crude briefly touched similar levels before peaking near $130. Given the direct closure of the Strait of Hormuz, a chokepoint for roughly 20% of global supply, the $150 per barrel target mentioned seems increasingly plausible. This historical precedent from last decade suggests the current rally has significant room to run as long as the conflict continues to escalate.

In the futures market, we are observing an extreme state of backwardation, signaling a severe immediate supply shortage. The premium for the front-month April contract over the May contract has blown out to over $5, a level not seen since the supply shocks we experienced in 2025. This structure strongly incentivizes holding long positions and signals that the physical market is exceptionally tight right now.

Despite the bullish momentum, the risk of a sharp reversal on any news of de-escalation means hedging is critical. We are seeing some traders buy far out-of-the-money put options as a low-cost way to protect against a sudden peace agreement or a coordinated release from strategic petroleum reserves. The high implied volatility makes these hedges expensive, but they could be essential if the political situation changes unexpectedly.

Create your live VT Markets account and start trading now.

Start trading now – Click here to create your real VT Markets account

USD/CAD rose from the mid-1.3500s after reaching a nearly one-month low in Asia on Monday. The move lacked follow-through and the pair struggled to hold gains above 1.3600.

Rising tensions in the Middle East supported a global move towards safer assets and lifted the US dollar to its highest level since November 2025. This offset the weak US Nonfarm Payrolls report released on Friday.

Oil Shock And Safe Haven Demand

Crude Oil jumped more than 25% intraday, moved above $110, and hit a nine-month high on Monday. The rise was linked to supply risk concerns around the Strait of Hormuz.

Higher oil prices supported the Canadian dollar and limited USD/CAD upside. The earlier break below a multi-week trading range support suggests the pair may need stronger buying to confirm a near-term base and any sustained rebound.

We are seeing a classic tug-of-war in USD/CAD, with the pair struggling around the 1.3600 level. The safe-haven appeal of the US dollar is strong, with the DXY index pushing 106.50, a level not seen since November 2025. This is happening while WTI crude oil prices remain elevated near $108 a barrel after the massive recent spike, directly supporting the Canadian dollar.

The demand for US dollars is fueled by the escalating conflict in the Middle East, which is overshadowing poor domestic data. For instance, last Friday’s Nonfarm Payrolls report on March 6th showed a disappointing addition of only 95,000 jobs, yet the market is more focused on geopolitical risk. Consequently, we’ve seen the probability of a Federal Reserve rate cut by June plummet from over 70% last month to below 30% today, as inflation fears from high energy prices take hold.

Positioning And Volatility Strategies

On the other side of the trade, the surge in oil is a massive boost for the loonie. This is not just a speculative spike; it is fundamentally altering Canada’s terms of trade and providing a strong headwind against any significant USD/CAD advance. Adding to this, the latest inflation data from Statistics Canada came in hotter than expected at 3.1%, making it difficult for the Bank of Canada to consider rate cuts, which further supports the CAD.

For derivative traders, this environment of high uncertainty and opposing powerful forces screams for volatility plays. Buying options, such as straddles or strangles, on USD/CAD could be a prudent way to position for a large move in either direction over the coming weeks, as a resolution to either the oil shock or the geopolitical tension will likely cause a sharp breakout. Implied volatility is high, but the potential for a multi-cent move makes it a calculated risk.

Given that the pair broke below its multi-week trading range last week, we must be cautious about taking on new bullish positions. A more tactical approach might involve using options to define risk, such as buying puts to speculate on a move lower towards the 1.3400s. Alternatively, for those who believe the USD will prevail, selling put spreads could be a way to collect premium while betting that the mid-1.3500s will hold as a floor.

Create your live VT Markets account and start trading now.

Start trading now – Click here to create your real VT Markets account

Gold (XAU/USD) fell to about $5,075 in early Asian trade on Monday, down 1.52% and below $5,100. The move came as the US Dollar strengthened and markets assessed inflation risks linked to higher oil prices.

Rising crude oil prices increased inflation fears, which led traders to reduce expectations for further Federal Reserve easing. Higher interest rates tend to weigh on gold because it does not pay interest.

Fed Policy Outlook Shifts

The Fed is expected to keep rates unchanged at its 17–18 March meeting. Many economists forecast the next rate cut may not come until June or July 2026.

Traders are also watching the US-Iran situation and wider Middle East risks. US CPI inflation data due on Wednesday is expected to be a key focus.

A weaker US labour report may limit gold’s losses by weighing on the dollar. February Nonfarm Payrolls showed a drop of 92,000, and the unemployment rate rose to 4.4% from 4.3% in January.

Given the sharp drop in gold to the $5,075 level, we see a clear reaction to renewed inflation fears driven by surging oil prices. WTI crude has breached $145 a barrel, its highest level since the 2022 energy crisis, fundamentally altering the market’s outlook on inflation. This suggests that the environment of falling inflation that we saw through most of 2025 is now being seriously questioned.

Trading Strategy Considerations

We must adjust our expectations for Federal Reserve policy, as the focus shifts from a weak labor market back to price stability. Just a month ago, markets were pricing in a 70% probability of a rate cut by June, but CME FedWatch data now shows this has plummeted to below 30%. The upcoming Fed meeting on March 18 is therefore critical, where we now expect a decidedly more cautious, if not hawkish, tone.

The US Consumer Price Index report this Wednesday is the next major catalyst. Consensus forecasts are already creeping higher toward 3.7% year-over-year, and a number hotter than that could trigger another leg down in gold toward the $5,000 psychological support level. Buying puts or establishing bear put spreads on XAU/USD are strategies to consider for traders anticipating a continued slide.

However, we cannot entirely discount the weak February jobs report, which showed a 92,000 payroll decline and a rising unemployment rate of 4.4%. This creates a conflicting, stagflationary backdrop for policymakers and could provide some support for gold if recession fears begin to outweigh inflation concerns. Any de-escalation of geopolitical tensions in the Middle East would also cause a sharp reversal in oil and a potential spike in gold prices.

This clash between rising inflation and a weakening economy increases overall market volatility, which is a key takeaway for us. The VIX index has already climbed over 5% in the last week, reflecting growing uncertainty. Therefore, option strategies that profit from large price movements in either direction, such as long straddles on gold futures, could be effective in the coming weeks.

Create your live VT Markets account and start trading now.

Start trading now – Click here to create your real VT Markets account

NZD/USD edged down to about 0.5865 in early Asian trading on Monday. The US Dollar strengthened against the New Zealand Dollar as the US-Israeli war with Iran continued, supporting demand for safer assets.

China’s Consumer Price Index rose 1.3% year on year in February, up from 0.2% in January and above the 0.8% forecast. China’s Producer Price Index fell 0.9% year on year in February, improving from a 1.4% decline in January and beating the -1.1% expectation.

China Inflation Update

On a monthly basis, China’s CPI increased 1.0% in February, compared with 0.2% previously. Despite these figures, the Australian Dollar did not gain, as markets stayed cautious due to Middle East tensions.

Iran named Mojtaba Khamenei as supreme leader a little over a week after Ayatollah Ali Khamenei was killed in US-Israeli strikes. US President Donald Trump said a leader chosen without US approval would “not last long”, adding to concerns about a longer conflict.

We recall that around this time last year, in early 2025, the NZD/USD was softening on fears of a prolonged Middle East war. This drove safe-haven demand for the US Dollar, even as China posted some surprisingly strong inflation data. That dynamic of geopolitics trumping economics set a clear tone for the market.

Those fears have proven to be well-founded, as tensions have kept the CBOE Volatility Index (VIX) elevated, averaging above 20 for most of the past year. This persistent risk-off sentiment has provided a steady tailwind for the US Dollar. The situation in Iran following the leadership change has not stabilized, continuing to fuel uncertainty in global energy markets and supporting the dollar’s safe-haven status.

Trading Implications For Nzdusd

Meanwhile, the optimism from China’s February 2025 CPI print of 1.3% has since faded. We have seen recent data from early 2026 showing Chinese inflation has cooled back to 0.7%, with producer prices remaining in deflationary territory. This slowdown weighs heavily on proxy currencies, and New Zealand’s export receipts have reflected this weakness.

Given the strong dollar and the weak Kiwi, the NZD/USD pair has trended lower, now sitting near 0.5750. Derivative traders should therefore consider strategies that profit from continued or accelerated downside in the pair. Buying NZD/USD put options could be an effective way to position for a further drop while limiting upfront risk.

Historically, we’ve seen this pattern before, such as during the 2020 market panic when the Kiwi fell sharply against the greenback. Looking ahead, traders should be positioned for further NZD weakness, especially if upcoming statements from the Reserve Bank of New Zealand reflect concerns over the slowdown in China. Any dovish tilt from the RBNZ would likely act as the next major catalyst for a move lower.

Create your live VT Markets account and start trading now.

Start trading now – Click here to create your real VT Markets account

USD/JPY rose for a third session, trading near 158.60 in Asian hours on Monday as the US Dollar gained on safe-haven demand. The Iran war entered its second week with no clear outcome.

Mojtaba Khamenei was appointed Iran’s supreme leader just over a week after Ali Khamenei was killed in US-Israeli strikes. Donald Trump said the appointment would be “unacceptable” and suggested the US should have a role in choosing Iran’s next supreme leader.

Safe Haven Demand Lifts The Dollar

The US Dollar also drew support as WTI crude oil moved above $100.00 per barrel on fears the conflict could disrupt global energy supplies. Trump called higher oil prices a “very small price to pay” for defeating Iran and ensuring global peace.

Traders also adjusted inflation expectations after the outbreak of hostilities last week, supporting views that the Federal Reserve may delay interest rate cuts. This added to the US Dollar’s strength against the Yen.

Japan’s Labour Cash Earnings rose 3% year-on-year in January 2026 after a 2.5% rise in December 2025. Japan’s Current Account surplus was ¥941.6B in January versus ¥960.0B expected, and up from ¥728.8B previously.

With the conflict in Iran entering its second week, we see the US Dollar strengthening as a primary safe-haven asset. The surge in WTI crude oil above $100 per barrel, a level not consistently seen since the energy crisis of 2022, is fueling this demand for dollars. This geopolitical tension is currently the single most important factor driving currency markets.

Rate Expectations And Intervention Risk

The inflationary shock from higher energy costs is forcing a rapid recalculation of the Federal Reserve’s plans. We have seen fed funds futures shift dramatically in the past week, with the market now pricing in less than a 20% chance of a rate cut before the third quarter of 2026. This reinforces the interest rate advantage the US Dollar holds over other major currencies.

For the USD/JPY pair, this has created a powerful upward trend, pushing it towards the 160 level. While the Yen is traditionally a safe haven, the widening gap between US and Japanese interest rate expectations is the dominant force. We must remain highly alert for intervention, as Japanese authorities previously stepped in to defend the Yen back in 2022 and 2024 when the pair crossed the 150-152 range.

Given the high probability of sudden, sharp moves, buying outright spot positions is risky. We should consider using options to manage this uncertainty, such as purchasing USD/JPY call options to gain upside exposure while strictly capping potential losses if intervention does occur. Market volatility has also spiked, with the VIX, a key measure of fear, jumping over 30% last week, making strategies that profit from price swings attractive.

Finally, we cannot ignore domestic Japanese data, which shows a significant 3% rise in labor cash earnings for January. This is the strongest wage growth we have seen in several years and could pressure the Bank of Japan to adopt a more hawkish stance later this year. For now, the global crisis is in control, but this underlying domestic strength could cause a rapid reversal in USD/JPY if geopolitical tensions ease.

Create your live VT Markets account and start trading now.

Start trading now – Click here to create your real VT Markets account

Silver (XAG/USD) fell at the start of the week and hit a four-day low in the Asian session. It traded in the mid-$80.00s, down 4% on the day, after failing near the 100-hour EMA.

A move accepted below the $80.00 level is seen as a trigger for further falls. The MACD is in negative territory, with its line below the signal line and a widening negative histogram.

The RSI is at 31.92, just above oversold, which points to ongoing selling pressure. It also suggests the price is near a level where short-term rebounds can occur.

Support sits near $79.50, then $78.50, with $78.00 as a further downside level. Resistance is at $81.50, and a push above it could lead towards $82.50.

The price remains below the 100-period EMA near $84.50, keeping the downside bias in place. A sustained move above that level would weaken the bearish view and point to a steadier recovery.

The analysis was produced with help from an AI tool.

We are seeing silver begin the week with significant selling pressure, confirming the bearish technical setup. The failure to hold above the $80.00 mark is a critical signal for us in the near term. This price action suggests that downside momentum is building, and traders should be prepared for further weakness.

The broader economic environment supports this caution, as last week’s February 2026 Consumer Price Index (CPI) data came in at 4.1%, slightly below expectations. This cooler inflation reading has temporarily dampened silver’s appeal as a hedge, contributing to the current drop. The market is now factoring in a less aggressive stance from central banks, which is weighing on precious metals.

For derivative traders with a bearish bias, a sustained break below the $80.00 psychological level presents a clear opportunity. We would consider buying put options with strike prices at $79.00 or $78.50, targeting a move toward the $78.00 objective in the coming weeks. The expanding negative MACD indicator validates this strategy, signaling that the downward trend has strength.

However, we recall the powerful rally throughout 2025, which saw silver climb from the low $60s, driven by record industrial demand. The Silver Institute reported that consumption from the solar and electronics sectors grew by another 15% last year, a fundamental support that could trigger sharp bounces. The Relative Strength Index (RSI) is also nearing oversold territory, suggesting the current selling might be overextended.

Given this, traders looking for a reversal should remain patient and wait for confirmation. A potential strategy is to watch for a decisive move back above the $81.50 resistance level before initiating long positions. Buying call options above this point could be a way to capitalize on a short-term bounce toward the $82.50 area.

Ultimately, the key resistance remains the 100-period EMA near $84.50, and as long as the price stays below this line, the bears are in control. Uncertainty surrounding future industrial orders and the next move from the Federal Reserve will likely keep silver volatile. We will be watching the $80.00 level closely as the pivot point for the next major price move.

Start trading now – Click here to create your real VT Markets account

China’s Consumer Price Index rose 1.3% in February year on year, up from 0.2% in January, versus a 0.8% market forecast. CPI also increased 1.0% month on month in February, after a 0.2% rise previously.

China’s Producer Price Index fell 0.9% year on year in February, following a 1.4% drop in January. This compared with a market forecast of -1.1%.

Market Reaction And Key Context

After the release, AUD/USD was down 0.80% at 0.6965. Trading before the data was already weaker, alongside a risk-off tone and a firmer US Dollar.

Ahead of the release, the National Bureau of Statistics was due to publish the figures at 01:30 GMT. CPI and PPI are measures of price changes for consumers and producers, with year-on-year readings comparing the month with the same month a year earlier.

Price levels cited for AUD/USD included resistance at 0.7055, 0.7089 and 0.7147. Potential support levels were 0.6906, the 100-day EMA at 0.6810, and 0.6741.

Other figures referenced include the RBA’s 2–3% inflation target and iron ore exports of $118 billion a year (2021 data).

Looking back to this time in 2025, we saw China’s consumer inflation data beat expectations while producer prices were still falling. This created a mixed signal for the Australian dollar, which struggled to gain traction despite the positive consumer news. That pattern of deflationary pressure from producers was a key theme we watched throughout last year.

Implications For RBA And Audusd

Now, the most recent data for February 2026 shows a more decisive shift, with consumer prices rising a stronger-than-expected 1.8%. More importantly, producer prices have finally turned positive for the first time in over a year, with the National Bureau of Statistics reporting a 0.2% increase. This suggests that the disinflationary pressures out of China, which weighed on the global economy, may be ending.

This shift complicates things for the Reserve Bank of Australia, which we’ve seen hold its cash rate steady at 4.35% for the last several meetings. While the AUD/USD has been weak recently, currently trading around 0.6650, this data reduces the probability of near-term rate cuts. We should now watch for any hawkish adjustments in the RBA’s forward guidance.

The Australian dollar’s position is also influenced by key commodity prices. After a period of strength, iron ore prices have recently slipped below $110 per tonne, acting as a headwind for the currency. However, this positive producer price data from China, its largest customer, could provide a much-needed floor for industrial commodity prices.

Given these developments, we should consider positioning for increased volatility in the AUD/USD pair. Buying call options could be a viable strategy to capitalize on a potential rebound, with initial resistance now seen near the 0.6700 psychological level. Conversely, if global sentiment sours, put options could be used to protect against a slide back toward the year’s lows.

Ultimately, the US dollar’s role as a safe-haven asset remains a dominant factor for us to monitor. Even with this encouraging news from China, any increase in global uncertainty tends to push capital into the dollar, which can limit gains for the Aussie. Therefore, we must balance this specific data against the broader risk-on or risk-off market environment.

Create your live VT Markets account and start trading now.

Start trading now – Click here to create your real VT Markets account

The CLARITY Act debate in Washington is creating uncertainty across digital asset markets as lawmakers struggle to finalise a regulatory framework for crypto.

Banking opposition to stablecoin rewards highlights a growing battle between traditional finance and the emerging digital asset economy.

The Trump administration is pushing for faster crypto regulation, arguing delays could push innovation overseas.

Traders are also watching US CPI inflation data, which may influence Federal Reserve rate expectations and US dollar strength.

Key technical levels remain in focus across major markets, including gold near $4,996, Bitcoin defending $62,502 and USDX testing resistance near 99.631.

One of the biggest developments shaping market sentiment this week is the growing political battle around the Digital Asset Market Clarity Act of 2025, widely known as the CLARITY Act.

The legislation was originally designed to reset the regulatory framework for digital assets in the United States. After passing the House of Representatives with strong bipartisan support last year, the bill aimed to clearly divide regulatory authority between the Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC).

However, progress has slowed dramatically in the Senate. What began as a technical attempt to define crypto market structure has evolved into a broader economic debate about the future of digital finance and the role of the traditional banking system.

Against the backdrop of a more accommodating regulatory tone from the Trump administration, the SEC is raising concern over increasingly aggressive fund structures. https://t.co/Hj4tH3TVbT

For traders, the outcome matters because regulatory clarity could unlock institutional participation in digital assets, while prolonged delays may continue to create volatility in crypto markets.

Why The Bill Has Stalled In Washington

The primary obstacle facing the CLARITY Act is a breakdown in negotiations over the revised Senate version of the bill.

While the House legislation moved quickly, Senate discussions encountered resistance early in 2026. A scheduled markup session in January was postponed indefinitely after several major industry participants withdrew their support for the latest draft.

Talks on landmark crypto legislation have hit a new impasse after banks said they could not back a compromise pushed by the White House, a development that cast doubt on whether the bill will pass this year and sparked criticism from President Trump who accused lenders of trying…

Crypto firms argued that the revised proposal introduced rules that were too restrictive and could limit innovation in the sector.

The White House attempted to force progress by setting a drafting deadline of March 1, 2026, but that date passed without an agreement. The delay has now become a focal point for markets watching how the United States intends to regulate the rapidly growing digital asset economy.

Banking Opposition And The Risk Of Deposit Flight

Traditional banks have emerged as some of the most vocal opponents of the current version of the legislation.

Their concerns centre around a provision that would allow stablecoin issuers and crypto platforms to offer interest-like rewards on digital dollar tokens. Banks argue that this could create a powerful incentive for consumers to move deposits away from traditional savings accounts and into crypto wallets.

Industry estimates suggest that if stablecoins begin offering yields around 5%, while conventional savings accounts remain far lower, the shift could pull substantial liquidity out of the banking system.

For financial markets, the debate highlights a deeper conflict between legacy financial institutions and emerging digital asset platforms.

Trump Administration Pushes Crypto Agenda

President Trump has taken a more direct role in the debate, framing the CLARITY Act as a key pillar of his administration’s digital asset strategy.

In recent statements, the administration has criticised major banks for lobbying against the bill, accusing them of attempting to protect their profit margins by slowing regulatory reform.

The White House has also argued that delays could push digital asset innovation overseas, particularly toward countries that are already implementing clearer regulatory frameworks.

The Trump family’s flagship crypto project is once again facing questions. https://t.co/idy1IuXgI8

From the administration’s perspective, establishing the United States as a global centre for crypto innovation is both an economic and geopolitical objective.

For traders, this political backing increases the likelihood that some form of regulatory framework will eventually emerge, although the timeline remains uncertain. Read recent economic updates connected to Trump here.

Possible Paths Toward A Compromise

Despite the current stalemate, policymakers are exploring several potential compromises.

One proposal from the White House would allow stablecoin rewards only when tokens are actively used for payments, while preventing interest-style rewards on idle balances that resemble traditional savings accounts.

Another development gaining traction is the rise of federal trust bank charters for crypto companies. Several fintech and digital asset firms have recently applied for or received these charters through the Office of the Comptroller of the Currency, allowing them to operate with a degree of federal oversight while broader legislation remains unresolved.

While these measures do not replace the CLARITY Act itself, they may offer a temporary pathway for the industry as lawmakers continue negotiations.

Legislative Timeline Traders Should Watch

The political calendar is also becoming a critical factor.

With US midterm elections approaching in 2026, the window for passing the legislation is narrowing.

Current expectations suggest several key milestones:

March 2026: Closed-door negotiations continue after the missed drafting deadline.

April 2026: New rules around federal crypto charters could begin taking effect.

May 2026: Final opportunity for a Senate Banking Committee markup before election season dominates the agenda.

August 2026: Target window for a full Senate vote.

January 2027: Potential implementation date if the bill passes before year-end.

For markets, these milestones will shape expectations for regulatory clarity and could influence the trajectory of digital asset investment in the United States.

Upcoming Events

11 March 2026

1. US CPI y/y, Forecast: 2.50%, PRevious 2.40%

Inflation data may reshape Fed rate expectations.

12 March 2026

1. UK BOE Gov Bailey Speech

Markets are watching signals for upcoming rate decisions.

13 March 2026

1. US GDP m/m, Forecast: 0.20%, Previous: 0.10%

Growth data gauges economic momentum.

2. US Core PCE Price Index, Forecast: 0.40%, Previous: 0.40%

BTCUSD rejected after breaking $70,969 swing high.

$62,502 now acts as the final defence for buyers.

Crypto regulation debate adds volatility risk.

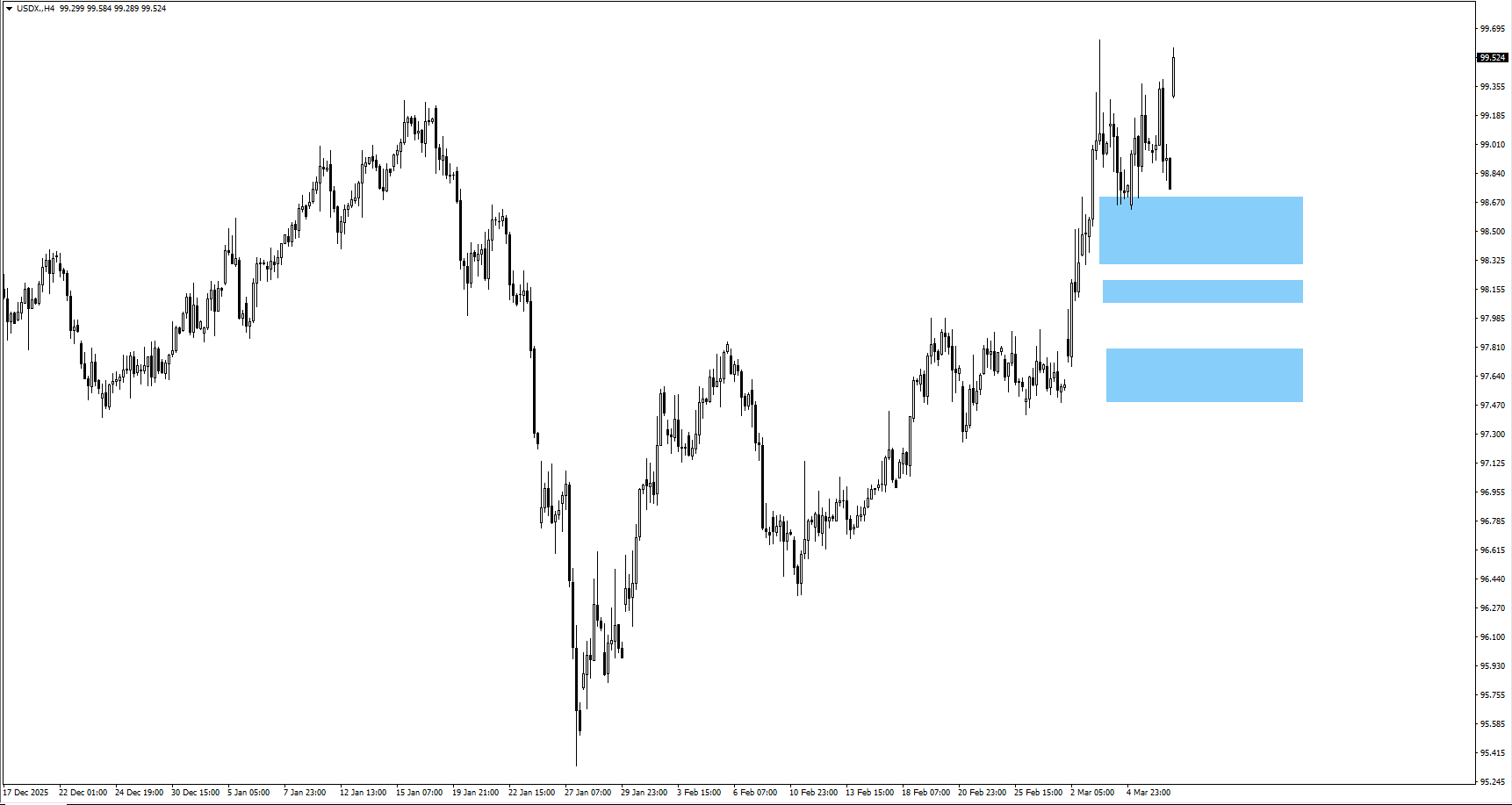

US Dollar Index (USDX)

USDX gapped higher at the start of the week.

Break above 99.631 could trigger move toward 100.321.

CPI may decide the next direction.

SP500

SP500 failed near 6,902 resistance and printed a swing low.

6,517 now acts as the crucial support level.

Geopolitical tensions increase volatility.

Bottom Line

Markets are entering the week with several competing forces shaping price action. Inflation remains the central macro driver, with US CPI expected at 2.5% year on year. A stronger reading could reinforce US dollar strength and delay expectations for Federal Reserve rate cuts.

At the same time, geopolitical tensions and rising oil prices above $100 are adding risk premium to global markets. Technically, gold continues to consolidate above $4,996, Bitcoin is defending the $62,502 support level after a failed breakout above $70,969, and the US Dollar Index is testing resistance near 99.631.

These levels will likely determine the next directional move as traders react to inflation data, regulatory developments in crypto markets, and shifting global risk sentiment.

Gold (XAUUSD) is trading in consolidation while markets wait for US CPI data. The key level to watch is $4,996, which currently acts as support. If gold falls below this level, sellers may begin targeting $4,842, where stronger downside momentum could develop. Inflation data and US dollar strength will likely determine the next major move.

2. How does the CLARITY Act affect Bitcoin and crypto markets?

The Digital Asset Market Clarity Act aims to define regulatory oversight between the US Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC). However, the bill has stalled in the Senate due to disagreements around stablecoin rewards and banking oversight. This regulatory uncertainty is contributing to volatility in Bitcoin and broader digital asset markets.

3. Why did Bitcoin fall after breaking above $70,000?

Bitcoin briefly broke above the $70,969 swing high, but the move quickly reversed as traders took profit and risk sentiment weakened. The market is now defending $62,502, which has become the most important support level in the current structure. A sustained break below this level could open the door for a deeper correction.

4. Why is the US CPI important for traders?

US Consumer Price Index (CPI) data measures inflation and strongly influences expectations for Federal Reserve interest rate decisions. If inflation comes in higher than expected, the Federal Reserve may delay rate cuts, which could strengthen the US dollar and pressure assets such as gold and Bitcoin.

5. What levels should traders watch in the US Dollar Index (USDX)?

The US Dollar Index recently gapped higher, with traders watching 99.631 as the immediate resistance level. If the dollar breaks above this level, it could move toward 100.321, strengthening the currency further and potentially weighing on commodities such as gold.

China’s Producer Price Index (PPI) fell 0.9% year on year in February. This was a smaller decline than the forecast of -1.1%.

The result indicates producer prices were still lower than a year earlier. The gap versus expectations was 0.2 percentage points.

China Ppi Misses Less Than Expected

The latest data shows China’s producer prices fell 0.9% in February, a smaller drop than the 1.1% decline we were braced for. While this marks the 17th straight month of factory-gate deflation, the slower pace of decline suggests the worst pressures might be starting to ease. This slight beat on expectations is a signal we cannot ignore.

This points to a potential firming of demand for industrial commodities, as it hints at a bottoming process in China’s manufacturing sector. We’ve seen iron ore prices stabilize around $115 per tonne after dipping earlier in the year, and this PPI number could provide further support. Traders should consider positioning for modest upside in copper and oil through the coming weeks, perhaps using call spreads to define risk.

For currency traders, this data may provide a floor for the yuan. A less deflationary environment reduces the immediate pressure on the People’s Bank of China for more aggressive easing, which could temper the yuan’s weakness against the dollar. We should watch the USD/CNH pair for signs of resistance, as a break lower could gain momentum.

This improvement, however slight, could also boost sentiment for Chinese equities that were battered by pessimism throughout 2025. Better factory prices can translate into improved margins for industrial companies, potentially lifting indices like the Hang Seng. We should consider buying short-dated call options on China-focused ETFs to play a potential sentiment shift.