Key Points

BRP sits in a unique position within the consumer discretionary sector. Its products are not essential, but they are aspirational, which makes the stock a useful signal of how confident consumers really are.

- BRP is a premium discretionary brand, tied to leisure spending rather than necessity.

- Higher interest rates are starting to pressure financing-driven demand.

- The key question is whether higher-income consumers can sustain spending.

Consumer spending rarely weakens evenly. Instead, it fragments, with different income groups and categories adjusting at different speeds. This makes premium discretionary stocks particularly useful as indicators of underlying economic conditions.

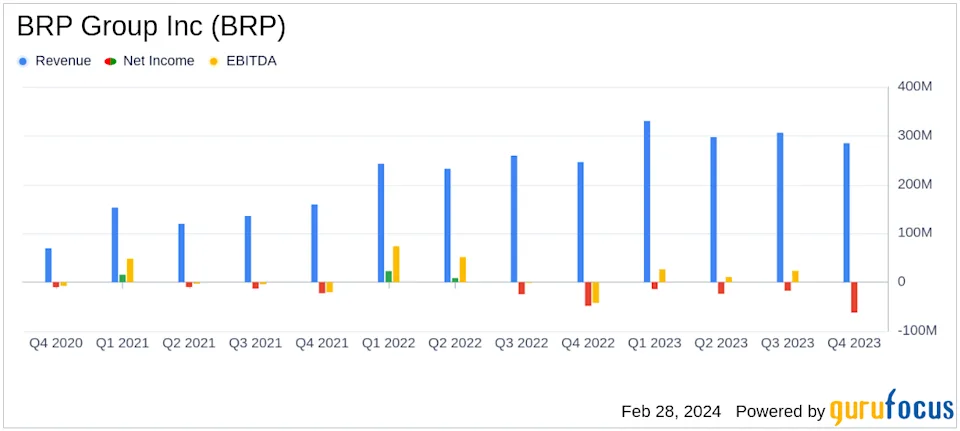

Companies like BRP Inc. offer one view into this dynamic. Their products, including recreational vehicles and leisure equipment, are high-ticket purchases tied to lifestyle and confidence rather than necessity. Recent results, including quarterly revenue of C$2.46 billion, up 16% year on year, suggest that demand remains present, but the composition of that demand is shifting.

Source: Yahoo Finance

Rather than focusing on a single company, the more important question is broader. Can premium consumer spending as a whole remain resilient as financial conditions tighten?

Premium Spending is Not Uniform

The resilience of premium spending is often misunderstood. It does not mean that demand remains strong across all segments. It means that it behaves differently.

Higher-income consumers tend to be less sensitive to short-term economic pressure. Their spending is influenced more by long-term wealth and asset values than by immediate income constraints. This allows premium brands to hold up longer during slowdowns.

However, recent trends suggest that even this segment is beginning to show signs of adjustment. Companies like Diageo, a leader in premium spirits, have faced pressure as consumers become more selective, particularly in markets where discretionary budgets are tightening.

This creates a layered demand environment. Spending does not collapse, but it becomes more uneven, with some categories holding up better than others and growth becoming harder to sustain.

Interest Rates are Reshaping Discretionary Demand

Interest rates are one of the most important drivers of this shift. Higher borrowing costs reduce flexibility across the consumer base, particularly for high-ticket purchases that rely on financing.

In sectors such as recreational vehicles, the impact is direct. Higher monthly payments reduce affordability, lengthen purchase cycles, and lead to more cautious decision-making. In other areas, such as premium goods and lifestyle spending, the effect is more indirect but still meaningful.

Consumers respond by becoming more selective. Purchases are delayed, spending is prioritised, and discretionary budgets are reassessed. This does not eliminate demand, but it changes its timing and intensity.

For traders, this is where the signal becomes valuable. Rate-sensitive consumer stocks often move ahead of broader economic data, reflecting real-time shifts in behaviour.

As interest rate expectations evolve, traders often track these effects across a range of global equities. CFD Shares on the VT Markets platform provide access to companies exposed to these same macro forces.

From Pandemic Boom to Demand Normalisation

The current environment cannot be understood without considering the demand surge during the pandemic period. Between 2020 and 2022, consumers redirected spending toward goods, particularly those linked to outdoor and lifestyle activities.

Source: BRP

This created a powerful growth cycle across premium discretionary sectors. Companies benefited from elevated demand, strong pricing power, and accelerated customer acquisition.

That surge also pulled forward future demand. Many purchases that would have occurred later were brought forward, leaving a gap in subsequent periods.

Now, the market is adjusting. Growth is moderating, replacement cycles are extending, and new demand is entering at a slower pace. This is not necessarily a sign of weakness, but a transition toward more sustainable levels.

Similar patterns can be observed across sectors. From recreational products to premium consumer goods and even technology, many industries are now moving through a phase of recalibration following unusually strong growth, . Ttake Allbirds’ complete overhaul into AI this week.

Inventory, Pricing, and Margin Discipline

As demand normalises, the focus shifts to how companies manage the transition.

Inventory becomes a key indicator. When products take longer to sell, stock begins to build, creating pressure across the supply chain. This can eventually lead to discounting and margin compression if not managed carefully.

In the case of BRP, recent data suggests progress, with North American inventory declining by 17% year on year. This indicates that the company is working through excess supply while maintaining pricing discipline.

Source: U.S. Securities and Exchange Commission

The same principle applies across premium lifestyle sectors. Strong brands are better positioned to preserve margins, but they are not immune to pressure. The ability to manage inventory without aggressive discounting is often a key differentiator during this phase of the cycle.

Interest Rates Are a Key Pressure Point

Interest rates remain one of the most direct drivers of BRP’s performance. Because many purchases are financed, affordability is highly sensitive to changes in borrowing costs. Even modest increases in rates can significantly affect monthly payments, altering the total cost of ownership.

This creates a clear transmission mechanism into demand. As rates rise, financing becomes more expensive, approvals may tighten, and consumers become more cautious about committing to large purchases. These effects do not always appear immediately in revenue, but they can be observed in the operating environment.

Sales cycles tend to lengthen, dealer turnover slows, and inventory begins to build. Companies may respond with increased promotional activity or incentives to stimulate demand. In this way, BRP acts as a direct reflection of how monetary policy filters into real-world consumer decisions.

This is why rate-sensitive stocks like BRP are often watched alongside broader macro assets. Traders looking to position around interest rate shifts can also explore opportunities across global shares and indices through CFDs on the VT Markets app.

Wealth Effects and Diverging Consumers

One of the defining features of the current environment is divergence between consumer groups.

Higher-income consumers, who drive much of the demand for premium products, tend to remain more resilient. Their spending is influenced by asset values and long-term financial outlook rather than immediate income pressure.

At the same time, middle-income consumers face tighter conditions. Higher borrowing costs, reduced savings buffers, and rising living expenses all contribute to more cautious spending behaviour.

This creates a split dynamic within premium discretionary sectors. Demand may hold at the top end while weakening elsewhere, leading to changes in product mix and overall growth patterns.

For traders, this divergence helps explain why some premium stocks remain stable while others come under pressure. The underlying driver is not just income, but the distribution of financial resilience across the consumer base.

What Traders Should Watch

For traders, the key is to monitor how these figures evolve in relation to broader economic conditions. Unit sales trends provide a direct read on demand, while inventory levels offer early signals of slowing turnover. Pricing behaviour and promotional activity can indicate whether margins are under pressure, and interest rate trends remain central to understanding affordability. Consumer sentiment data adds an additional layer, helping to contextualise discretionary spending behaviour.

BRP often moves alongside consumer discretionary trends, and traders may track it in conjunction with broader retail and lifestyle sectors to gain a more complete picture of demand.

BRP often moves alongside consumer discretionary trends. Traders can explore opportunities across retail, lifestyle, and global consumer stocks through CFD Shares on VT Markets.

How Premium Lifestyle Stocks Fit Into a Broader Strategy

Premium discretionary stocks offer a targeted way to express views on consumer behaviour. They sit at the intersection of confidence, income, and financial conditions, making them particularly sensitive to changes in the economic environment.

This makes them useful in several ways. They can act as indicators of discretionary confidence, reflect the impact of interest rates on spending, and provide insight into how different consumer segments are adjusting to changing conditions.

They also offer a point of comparison with other sectors. While premium consumer stocks reflect spending behaviour, areas such as technology and AI often respond differently to the same macro drivers. Comparing these signals can help traders build a more complete view of the market.

Bottom Line

Premium lifestyle stocks are not immune to economic pressure, but they tend to adjust differently. Demand becomes more selective rather than disappearing, and resilience depends on both brand strength and the financial position of the consumer.

The current environment reflects a transition from exceptional demand to a more balanced phase. For traders, the key is understanding how this shift plays out across different sectors and consumer groups.

Create a live VT Markets account today to access our platform features, including market insights and educational content.

Trader Questions

What are premium lifestyle stocks?

Premium lifestyle stocks refer to companies that sell high-end discretionary products such as luxury goods, premium alcohol, and recreational equipment. Their performance is closely tied to consumer confidence and spending behaviour.

Why are premium brands affected by interest rates?

Higher interest rates increase borrowing costs and reduce disposable income, which can lead consumers to delay or reduce spending on non-essential purchases.

Do premium brands perform better in slow economies?

Premium brands often show more resilience because their customers tend to have higher incomes, but demand can still soften as economic pressure builds.

What stocks reflect discretionary spending trends?

Stocks in sectors such as luxury goods, premium alcohol, and lifestyle products, including companies like Diageo, often reflect broader consumer behaviour.

How can traders approach premium consumer stocks?

Traders often track a group of discretionary stocks rather than focusing on one company, using them to gauge broader trends in spending and economic conditions.

Start trading now – Click here to create your real VT Markets account