Start trading now – Click here to create your real VT Markets account

Back

Start trading now – Click here to create your real VT Markets account

Start trading now – Click here to create your real VT Markets account

Start trading now – Click here to create your real VT Markets account

Start trading now – Click here to create your real VT Markets account

Start trading now – Click here to create your real VT Markets account

Start trading now – Click here to create your real VT Markets account

Start trading now – Click here to create your real VT Markets account

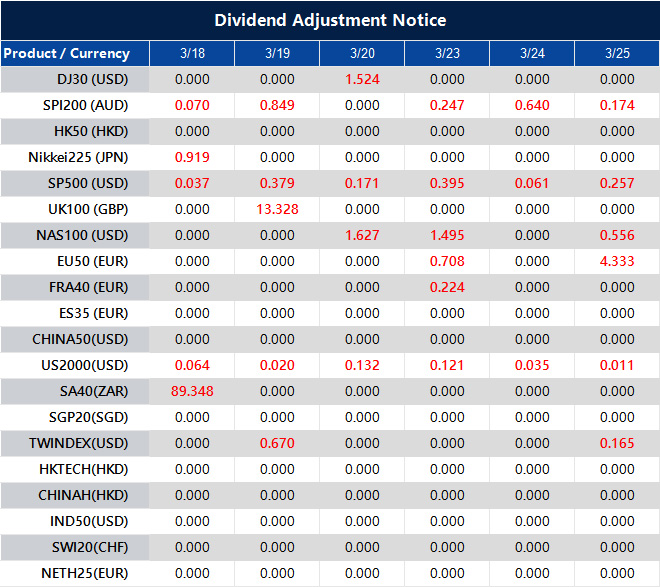

Dear Client,

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

Key Points

The U.S. dollar softened on Wednesday, giving back some of its recent safe-haven gains as oil prices eased and market sentiment improved ahead of a pivotal week for global central banks.

The US Dollar Index (USDX) is trading near 99.26, down -0.03%, marking a third consecutive session of declines. The move follows a strong rally last week that pushed the dollar to a 10-month high, driven by escalating geopolitical tensions and surging energy prices.

However, with oil prices pausing and pulling back modestly, markets have begun to reintroduce risk exposure, reducing demand for the dollar.

If oil continues to stabilise or decline, the dollar may face further short-term pressure as risk sentiment improves.

The key driver behind the dollar’s recent weakness has been the easing in oil prices. Crude declined after Iraqi and Kurdish authorities agreed to resume exports via Turkey’s Ceyhan port, helping to ease immediate supply concerns.

While Brent crude remains above $100 per barrel, the pause in its upward momentum has been enough to shift market positioning, at least temporarily.

Lower oil prices can reduce inflation fears and ease pressure on global growth, encouraging traders to move away from defensive assets like the U.S. dollar.

If oil resumes its upward trend, safe-haven demand for the dollar could return quickly.

Markets are now firmly focused on a series of central bank meetings, starting with the Federal Reserve, followed by the European Central Bank, Bank of England, and Bank of Japan.

All are widely expected to keep interest rates unchanged, but traders will be closely watching for forward guidance, particularly regarding inflation and growth risks stemming from the ongoing Middle East conflict.

The key question for policymakers is whether the energy shock will primarily slow economic activity or lead to more persistent inflation.

A more hawkish tone from central banks could limit further dollar weakness, while a cautious or balanced outlook may support risk assets and weigh on the greenback.

The US Dollar Index (USDX) is trading near 99.26, marginally lower on the session (-0.03%), as the recent recovery rally begins to lose momentum just below the psychological 100 level. After rebounding strongly from the 95.33 low, the dollar has entered a phase of consolidation, suggesting the market is reassessing directional conviction.

From a technical standpoint, short-term momentum is starting to soften. The 5-day moving average (99.52) has begun to turn lower, while the 10-day (99.17) sits just beneath current price, acting as near-term support.

The 20-day (98.58) and 30-day (98.08) remain upward sloping, indicating that the broader recovery structure is still intact despite the current pause.

Immediate support is seen around 99.00–99.10, with a break below this zone potentially exposing downside toward 98.50, where the 20-day average aligns.

On the upside, resistance is firmly positioned at 100.30–100.70, a region that has repeatedly capped bullish attempts and remains a key barrier for further upside continuation.

Overall, the USDX appears to be consolidating below major resistance, with the broader bias still constructive following its recovery from February lows.

However, failure to reclaim the 100 level may lead to further sideways movement or a modest pullback, especially if macro catalysts—such as shifting rate expectations—begin to weigh on dollar strength.

The dollar now sits at a crossroads between geopolitical risk and improving sentiment. Key drivers to monitor include:

For now, the dollar’s pullback appears to be a reaction to easing oil prices rather than a full reversal, with broader trends still dependent on how geopolitical and macroeconomic risks evolve.

Learn more about trading Indices on VT Markets today.

Why is the US Dollar Falling Today?

The US dollar is weakening because oil prices have eased, reducing safe-haven demand and allowing investors to shift back into risk assets ahead of central bank decisions.

What is Causing USD Weakness Right Now?

A combination of lower oil prices, improved market sentiment, and positioning ahead of central bank meetings is putting short-term pressure on the dollar.

Is the Dollar Still in an Uptrend?

Yes, the broader trend remains supported by geopolitical risks and earlier safe-haven demand. However, the current pullback suggests a short-term correction or consolidation phase.

How Do Oil Prices Affect the US Dollar?

Rising oil prices tend to support the dollar due to its safe-haven status and the U.S. being a net energy exporter. When oil falls, this support weakens, and the dollar can decline.

Why is the Yen Strengthening Against the Dollar?

The yen is gaining as risk sentiment improves and as USDJPY moves away from the 160 level, where markets had expected potential intervention from Japanese authorities.

Why is the Euro Rising Against the Dollar?

The euro is strengthening ahead of the European Central Bank meeting, as traders position for policy guidance and potential shifts in inflation outlook.

What Are Markets Expecting From the Federal Reserve?

Markets widely expect the Federal Reserve to keep interest rates unchanged, but are focused on forward guidance regarding inflation and future rate cuts.

Start trading now – Click here to create your real VT Markets account

Start trading now – Click here to create your real VT Markets account

Hello there 👋

Hello there 👋

Scan the QR code with your smartphone to start a chat with us, or click here.

Don’t have the Telegram App or Desktop installed? Use Web Telegram instead.