New Zealand’s Westpac Consumer Survey rose to 94.7 in the fourth quarter. It was 90.9 in the previous quarter.

We saw that piece of data on consumer confidence at the end of 2025, which showed a welcome improvement to 94.7. At the time, it suggested households were becoming less pessimistic, which was a tentative good sign for future spending. However, a reading below 100 still means there are more pessimists than optimists.

Implications For Rbnz Policy

This data from last year was one of the early signals that the Reserve Bank of New Zealand (RBNZ) might have to hold interest rates high for longer than many anticipated. Increased confidence, even if small, can translate into more spending, making it harder to bring inflation down. This supported our view that the market was too aggressive in pricing in rate cuts for 2026.

Now that we are in March 2026, that caution was warranted, as the most recent quarterly inflation data showed core inflation remaining sticky at 4.3%, well above the RBNZ’s target band. The central bank has signaled no immediate plans to lower its 5.5% official cash rate, reinforcing a “higher for longer” stance. Gross Domestic Product data from late 2025 also showed the economy contracting by 0.2%, confirming a technical recession and complicating the RBNZ’s task.

In the coming weeks, traders should consider positioning for sustained high interest rates. This involves looking at interest rate swaps that pay a fixed rate, essentially betting that the official cash rate will not be cut as soon as the market hopes. Volatility in the rates market may also decline as the RBNZ’s path becomes more predictable, making strategies like selling strangles on bond futures potentially profitable.

This interest rate outlook should continue to support the New Zealand dollar. With our rates holding firm while other central banks are signaling cuts, the NZD becomes more attractive. We should look at using currency options to bet on the Kiwi dollar strengthening, perhaps buying NZD/USD call options with a three-month expiry.

Equity Derivatives Positioning

For equity derivatives, the situation suggests a cautious approach. While better consumer sentiment is a positive, persistent high interest rates are a headwind for company earnings and valuations. Using NZX 50 index put options could be a prudent way to hedge against potential downside in the stock market over the next quarter.

Create your live VT Markets account and start trading now.

Start trading now – Click here to create your real VT Markets account

UOB economists Enrico Tanuwidjaja and Sathit Talaengsatya forecast that the Bank of Thailand will keep the 1-D Repo Rate at 1.00% through at least 1Q27, even with higher headline inflation linked to an oil shock. They also expect the policy rate to remain at 1.00% in 2026.

The focus is on whether higher inflation spreads beyond the initial rise into transport fares, prepared food, service prices, wage-setting, or inflation expectations. The central bank is expected to watch for these follow-on effects.

Steady Policy And Targeted Fiscal Support

The suggested policy mix is steady monetary policy alongside fiscal measures that are targeted and temporary. Fiscal support is framed around helping vulnerable households, public transport, and other sensitive users.

Broad, open-ended subsidies are described as harder to finance and less transparent over time. The article notes it was produced with assistance from an AI tool and reviewed by an editor.

We expect the Bank of Thailand to keep its policy rate at 1.00% through next year, creating a stable interest rate environment. This view holds even as February’s headline inflation came in at 3.4%, which is above the central bank’s official target range. The bank appears focused on supporting the economy rather than reacting to the oil price shock we saw late last year.

For us, the key is not the headline inflation itself, but whether it spreads into wages, transport fares, and other core services. The central bank is signaling it will remain patient, looking for these second-round effects before making any changes. Upcoming labor market reports and core inflation data will therefore be far more important to watch than the headline numbers.

Swap And Currency Implications

This stable outlook on rates suggests that receiving fixed payments on Thai interest rate swaps continues to be a viable strategy. We have seen the 2-year swap rate hold steady around 1.15%, showing that the market is already pricing in this long pause. Any temporary jumps in swap rates caused by inflation headlines could be seen as good entry points.

With Thai interest rates anchored at a low level, the Baht will likely stay under pressure against currencies with higher interest rates. The USD/THB has been trading near 36.50, and we see few reasons for the Baht to strengthen significantly in the coming weeks. Using options to position for further, gradual Baht weakness seems like a logical approach.

This patient monetary policy is very similar to the approach we observed throughout 2025, when the bank also chose to support the economic recovery instead of reacting to early price increases. That experience showed us the BoT has a high tolerance for inflation temporarily going over its target. The government is expected to use targeted spending, not rate hikes, to provide relief to the public.

Create your live VT Markets account and start trading now.

Start trading now – Click here to create your real VT Markets account

New Zealand’s current account-to-GDP ratio fell to -3.7% in the fourth quarter. It was -3.5% in the previous quarter.

The slight worsening of our current account deficit to -3.7% of GDP is a bearish signal for the New Zealand dollar. This indicates we are more reliant on foreign capital to fund our spending, putting fundamental pressure on the currency’s value. We should anticipate this data weighing on the NZD against major trading partners in the near term.

Options Strategy For NzduSD Downside

Given this outlook, we see an opportunity in buying NZD/USD put options. With the spot rate currently hovering around 0.6150, options with a strike price of 0.6000 expiring in late April could provide a cost-effective way to speculate on further downside. This strategy defines our risk to the premium paid while offering significant upside if the currency weakens as expected.

This data complicates the picture for the Reserve Bank of New Zealand, making it less likely they will cut the Official Cash Rate from its current 5.50% anytime soon. Lowering rates would likely weaken the currency further, fueling inflation on imported goods, which is already sticky at an annualized rate of 3.8%. The central bank is effectively constrained by this external imbalance.

We must remember this trend is not new, as we look back at the economic performance in 2025. We saw then that demand for our key exports, particularly from China, softened considerably in the second half of the year. Statistics from last year showed dairy and meat exports fell by a combined 7% in the final six months, a headwind that is clearly continuing.

This sustained pressure suggests implied volatility on the Kiwi may begin to rise from its current lows. Traders with existing long NZD exposure should consider hedging by selling NZD futures contracts. This can protect portfolios against a potential break below the critical 0.6100 psychological support level in the coming weeks.

New Zealand’s current account balance for the fourth quarter came in below forecasts. The forecast was a deficit of $-4.75B.

The actual outcome was a larger deficit of $-5.98B. This means the shortfall was $-1.23B wider than expected.

Current Account Shock Hits NZD

The fourth-quarter current account deficit from 2025 came in significantly wider than anyone expected, showing the country is spending much more overseas than it is earning. This is a clear negative signal for the New Zealand dollar (NZD). We should anticipate immediate and sustained selling pressure on the currency in the coming weeks.

This weak performance reflects the broader global slowdown we saw impacting export demand in the second half of 2025, particularly for dairy products. Looking back, Fonterra’s Global Dairy Trade index showed prices consistently falling in that period, directly hitting New Zealand’s trade balance. This data confirms that the economic headwinds from last year are carrying over into 2026.

The result puts the Reserve Bank of New Zealand in a difficult position, making it much harder for them to justify keeping interest rates high. Swap markets are already reacting, with the implied probability of an interest rate cut by the end of 2026 jumping from 20% to nearly 50% in overnight trading. This shift in rate expectations will weigh heavily on the NZD.

For traders, this surprise boosts market volatility, which we can use to our advantage. Implied volatility on one-month NZD/USD options has already spiked from 9% to over 13%, making strategies like buying put options attractive to profit from further downside. This allows for a defined-risk way to bet against the currency.

Cross Pair Trade Setup

We should also look at cross-currency pairs, specifically shorting the NZD against the Australian dollar (AUD). As New Zealand’s economic data disappoints, the NZD/AUD exchange rate is likely to break below key technical support levels established earlier this year. This could present a more compelling trade than simply selling NZD against the US dollar.

Create your live VT Markets account and start trading now.

Start trading now – Click here to create your real VT Markets account

The Australian Dollar rose for a second day after the Reserve Bank of Australia increased rates by 25 basis points to 4.10% on a 5-4 vote. AUD/USD was at 0.7104, up 0.48%.

US equities rose by 0.10% to 0.47% as risk appetite improved before the Federal Reserve decision. The US Dollar Index fell 0.29% on the day and nearly 1% on the week, and stood at 99.57.

Rba Decision And Market Reaction

RBA Governor Michelle Bullock said the vote reflected timing rather than direction, and mentioned discussion about holding until May. This was linked to waiting for more data and uncertainty around the Middle East conflict.

US data showed the ADP Employment Change 4-week average fell from 14.75K to 9K. February Pending Home Sales rose 1.8% month-on-month after a 1% fall in January.

The Fed meeting runs from 17 March and ends Wednesday with a statement and updated projections. Markets expect no March change, with one 25 basis-point cut priced for later this year, followed by Chair Jerome Powell’s press conference.

Technically, AUD/USD is above the 50/100/200-day averages near 0.69, with RSI near 55. Support is around 0.7040 and 0.6980, with resistance at 0.7150 and 0.7210.

Policy Divergence And Trading Implications

The landscape has shifted considerably from this time in 2025. We remember the Australian Dollar trading above 0.7100 after the RBA hiked, but today it struggles around 0.6550. This weakness reflects a fundamental divergence in central bank policy that has developed over the last year.

Last year, the RBA was still raising its cash rate to 4.10% amid a hawkish debate. Now, the rate sits at 3.60%, and the central bank’s tone is decidedly more cautious, with the latest quarterly CPI data showing inflation has eased to 3.4%. This suggests their next move is more likely a cut than a hike, putting sustained pressure on the currency.

Meanwhile, the US Dollar Index, which was below 100 in March 2025, is now trading firmly around 104.50. This strength is underpinned by a Federal Reserve that has held rates in the 5.00-5.25% range, citing persistent core inflation and a surprisingly robust labor market that added over 250,000 jobs last month. The market’s expectation of a single rate cut has evaporated, replaced by a “higher for longer” narrative from the Fed.

For derivative traders, this environment suggests that selling rallies in AUD/USD remains the primary strategy. Buying put options on the AUD/USD offers a direct way to profit from further downside while defining risk. For those with a more neutral but bearish view, selling out-of-the-money call spreads could be an effective way to collect premium as long as the pair remains capped.

Looking at the charts, the key support we were watching at 0.6900 in 2025 is a distant memory. The immediate focus is now on the 0.6500 psychological level, a break of which could trigger a swift move toward the lows seen in late 2025. Any rallies are likely to find significant resistance near the 50-day moving average, currently around 0.6620.

Create your live VT Markets account and start trading now.

Start trading now – Click here to create your real VT Markets account

US weekly crude oil stocks, reported by the API, rose by 6.6 million barrels for the week ending 13 March.

This was above expectations, which had pointed to a 0.6 million barrel fall.

Inventory Surprise Signals Bearish Momentum

The report from last week in 2025, showing a 6.6 million barrel build in crude oil when a small draw was expected, is a strong bearish signal. This massive surprise suggests that supply is overwhelming demand in the market. We should anticipate immediate downward pressure on WTI and Brent crude prices.

For derivative traders, this points towards buying put options on crude oil futures. This strategy allows us to profit from a potential drop in price over the next several weeks. We can look at strike prices below key support levels, such as the $75 per barrel mark for WTI, as a potential target.

This large inventory build is especially concerning when we consider recent global economic signals from last year. We saw in February 2025 that China’s Caixin Manufacturing PMI registered at 51.6, which, while in expansion territory, was part of a broader global picture of moderating growth. The oversupply in the U.S. hints that this slowdown in demand may be more pronounced than previously thought.

We must now watch the official EIA inventory report very closely to confirm the API’s numbers. Historically, while the two reports are correlated, the EIA data is considered the market benchmark. The size of this build also happened during the 2025 refinery maintenance season, which can sometimes inflate crude stock numbers temporarily.

USD/CHF fell 0.20% in the North American session on Tuesday and traded near 0.7850. The move followed a rejection near the 100-day simple moving average (SMA) at 0.7897, ahead of the Federal Reserve decision on Wednesday.

After failing to reach 0.8000, the pair dipped to a three-day low of 0.7843. Recent trading has produced higher highs and higher lows, while the Relative Strength Index (RSI) points to stronger buying pressure.

Key Resistance Levels Ahead

A break above 0.7900 would bring the 200-day SMA at 0.7946 into view. If the price then clears 0.8000, the next level referenced is the 4 November 2025 daily high at 0.8108.

If USD/CHF drops below 0.7800, attention shifts to 0.7700. Further weakness would expose the yearly low at 0.7601.

We saw this exact setup back in late 2025, when the USD/CHF was coiling around the 0.7850 level ahead of a key Federal Reserve decision. The market was watching to see if the pair could break the significant resistance near the 0.7900 mark. That failure to break higher then ultimately led to a period of consolidation before the dollar found renewed strength.

Given today is March 18, 2026, the fundamental picture now strongly favors dollar strength due to policy divergence. Recent data shows US inflation remains persistent at 3.1%, while Swiss inflation has fallen to just 1.3%, giving the Swiss National Bank room to be more lenient. This widening interest rate differential should continue to push the USD/CHF pair higher.

Options Strategies For Breakout Or Hedge

Derivative traders should consider buying call options to capitalize on a potential break above the old resistance levels. A call option with a 0.8000 strike price expiring in May 2026 would offer a cost-effective way to profit from a move toward the 0.8108 high we saw in November 2025. This strategy limits downside risk to the premium paid for the option.

Conversely, for those looking to hedge or speculate on a downturn, put options are the logical tool. If the pair fails to hold its current gains and drops below 0.7800, a put option with a 0.7750 strike could provide significant returns. This protects against any unexpected dovish shift from the Federal Reserve or a surprise intervention from the SNB.

We must remember the history of this pair, especially the massive volatility event in early 2015 when the Swiss National Bank unexpectedly removed the franc’s peg to the euro. Upcoming inflation reports and central bank commentary will inject volatility, making options a useful way to manage risk and speculate on direction. Holding options through these key data releases could capture any sharp, unexpected price movements.

Create your live VT Markets account and start trading now.

Start trading now – Click here to create your real VT Markets account

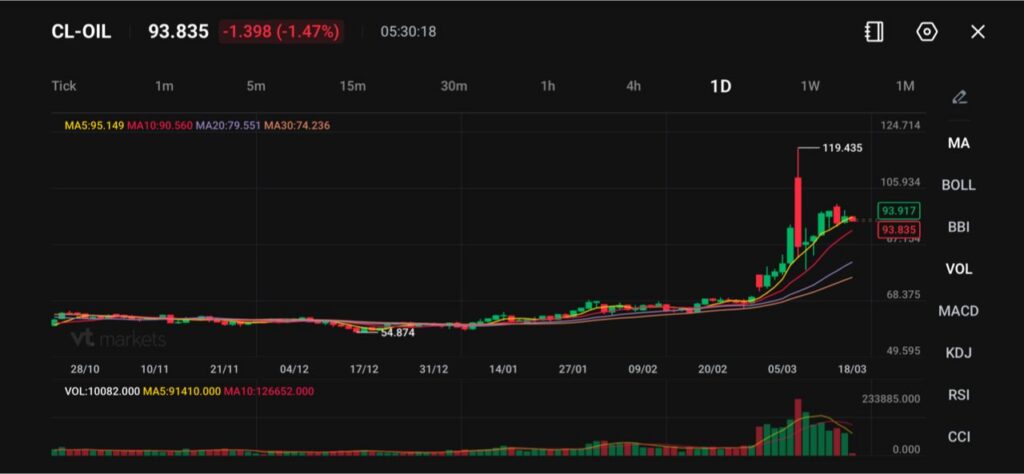

WTI crude trades near 93.83, down -1.398 (-1.47%), as oil pauses after a sharp rally.

Brent crude slips to $102.28, offering temporary relief to global equity markets.

Markets now turn to the Federal Reserve decision, with risks of a more hawkish outlook amid persistent inflation pressures.

Oil prices pulled back slightly on Wednesday, offering a brief reprieve to global markets after a period of intense volatility driven by escalating tensions in the Middle East.

WTI crude is trading at 93.83, down -1.47%, while Brent crude eased 1% to $102.28 per barrel. The decline reflects a temporary pause rather than a structural shift, as underlying supply risks remain firmly in place.

Despite the pullback, the broader narrative has not changed. The Strait of Hormuz remains largely shut, and geopolitical tensions continue to disrupt energy flows, keeping markets on edge.

The Strait of Hormuz remains effectively shut with no real conclusion to the Iran war in sight. What does this mean for trade and foreign policy?

If disruptions persist, oil prices may resume their upward trajectory after this consolidation phase.

Geopolitical Escalation Keeps Supply Tight

The latest developments in the Middle East continue to reinforce supply concerns. Israel has intensified its military actions, while Iran has renewed strikes on oil infrastructure in the United Arab Emirates.

At the same time, signals from Iranian leadership suggest no near-term de-escalation, increasing the likelihood of a prolonged disruption to global energy markets.

Iran has stepped up attacks on Saudi Arabia in recent days, signaling it’s targeting the oil-rich kingdom more aggressively than earlier in the war https://t.co/1ygjEMiht7

The Strait of Hormuz, a critical artery for global oil shipments, remains a key focal point. Any sustained closure or restriction of traffic through the strait could tighten supply conditions significantly.

According to JPMorgan, the current stability in oil prices may reflect temporary buffers such as regional inventories and policy interventions. However, if the strait remains constrained, markets may need to reprice oil higher as global inventories are drawn down.

Focus Shifts to Federal Reserve Outlook

With oil volatility dominating recent market moves, attention has now turned to the Federal Reserve’s policy decision, which is expected later in the day.

The Fed is widely expected to keep interest rates unchanged, but the key focus will be on updated economic projections and the “dot plot,” which could signal fewer or no rate cuts in the near term.

The Fed issues its latest interest rate decision Wednesday. Here's what to expect https://t.co/iCgRzS9EFN

Markets are particularly sensitive to how policymakers interpret the oil shock. The key question is whether it will primarily slow economic growth or drive persistent inflation.

Analysts warn that if the Fed leans toward the inflation narrative, it could adopt a more hawkish stance, reinforcing higher interest rates for longer.

A hawkish shift in Fed expectations could strengthen the dollar and weigh on commodities, including oil, in the near term.

Technical Outlook

Crude oil (CL-OIL) is trading around $93.83, down roughly 1.47% on the session, as the market pauses following an aggressive rally that pushed prices to a recent high near $119.43.

The pullback appears corrective rather than structural at this stage, with price action still well-supported above prior breakout levels.

Technically, the trend remains firmly bullish despite the near-term retracement. Price is holding above the 10-day moving average (90.56) and well above the 20-day (79.55) and 30-day (74.23), indicating that the broader uptrend remains intact.

The 5-day moving average (95.15) is now starting to flatten and roll slightly lower, reflecting short-term exhaustion after the sharp vertical move.

In terms of key levels, immediate support is seen around $90–91, aligning with the 10-day average and recent consolidation.

A deeper pullback could test $87–88, where prior breakout structure sits. On the upside, resistance remains near $100–105, followed by the spike high at $119.43, which now acts as a major technical ceiling.

Overall, oil appears to be entering a consolidation phase after a parabolic rally, with momentum cooling but the underlying trend still supported by elevated risk premiums.

As long as prices hold above the $90 region, the bullish structure remains valid, though further sideways movement or short-term pullbacks are likely before any attempt to retest recent highs.

What Traders Should Watch Next

Markets remain highly sensitive to both geopolitical and policy developments. Traders should monitor:

Updates on the Strait of Hormuz and Middle East conflict

The Federal Reserve decision and forward guidance

Whether oil can hold above the 90–95 range

Signs of renewed supply disruption or inventory drawdowns

For now, oil’s pullback appears to be a pause rather than a reversal, with geopolitical risks still firmly anchoring the market’s upside bias.

Learn more about trading Energies on VT Markets here.

Frequently Asked Questions

Why Did Oil Prices Pull Back After Rallying? Oil prices eased as markets paused after a sharp rally driven by geopolitical tensions. The pullback reflects short-term profit-taking and temporary stability rather than a shift in the broader bullish trend.

Where is Oil Trading Right Now? WTI crude is trading around 93.83, down -1.47%, while Brent crude has slipped to $102.28 per barrel.

Is the Oil Rally Over? Not necessarily. The broader trend remains supported by supply risks, particularly with disruptions linked to the Middle East conflict and restricted flows through the Strait of Hormuz.

Why is the Strait of Hormuz So Important? The Strait of Hormuz is a key global energy route, handling roughly 20% of the world’s oil shipments. Any disruption can significantly tighten global supply and push prices higher.

How Are Geopolitical Tensions Affecting Oil? Escalating conflict, including attacks on energy infrastructure, increases uncertainty and raises the risk of supply disruptions, which tends to support higher oil prices.

Start trading now – Click here to create your real VT Markets account

NZD/USD traded near 0.5860 on Tuesday, trimming most intraday losses as the US Dollar weakened amid an escalating war in the Middle East. US President Donald Trump said NATO allies were not willing to intervene in the US and Israel war against Iran, and added that the US no longer needed or wanted help from Japan, Australia, and South Korea.

The Federal Reserve will announce its interest rate decision on Wednesday, with rates expected to remain unchanged. Focus is set to shift to updated economic projections and comments from Fed Chair Jerome Powell, while higher oil prices raise inflation risks.

Us Hiring Momentum Slows

US private-sector hiring data showed slower momentum late in February. The NER Pulse version of the weekly ADP National Employment Report reported an average of 9K jobs per week in the four weeks to February 28, down from 14.5K the previous week.

In New Zealand, the Reserve Bank of New Zealand is due to decide on rates on 8 April, with a hold expected. Statistics New Zealand will publish Q4 GDP on Wednesday, with growth forecast at 1.7% year on year.

On the 4-hour chart, NZD/USD was at 0.5857, below the 100-period SMA and near the 20-period SMA, with RSI around 50. Resistance levels were 0.5870 and 0.5916, while support was seen at 0.5836 and 0.5816, with recent lows near 0.5800.

Looking back at the geopolitical tensions from early 2025, we remember how the conflict in the Middle East caused significant uncertainty. That situation drove a sharp, albeit temporary, spike in WTI crude oil prices, which briefly surpassed $115 per barrel in the second quarter of 2025 before pulling back. Traders should therefore consider using options to hedge against sudden flair-ups in geopolitical risk, as these events can rapidly impact commodity-linked currencies like the NZD.

Inflation And Policy Divergence

The Federal Reserve did hold interest rates at its March 2025 meeting, but the inflationary pressure from energy prices forced them into a more hawkish stance, leading to a final rate hike in May of that year. We see a similar dynamic now, with the latest February 2026 Consumer Price Index (CPI) data showing inflation remaining sticky at 2.9%, above the Fed’s target. This reinforces the need to watch inflation data closely, as it remains the primary driver of the Fed’s policy and, consequently, the US Dollar’s strength.

In New Zealand, we saw the economy avoid the technical recession that was feared back then, with the Q4 2024 GDP released in March 2025 coming in at 1.9%, slightly above expectations. The RBNZ, which held rates in April 2025, has since been forced to maintain a restrictive policy to battle its own domestic inflation. The interest rate differential between the RBNZ and the Fed will remain a key factor for the NZD/USD pair in the coming weeks.

That period in 2025 serves as a reminder of how quickly market focus can shift from weak employment data, like the soft NER Pulse report, to broader inflation risks. The NZD/USD pair eventually broke below the 0.5800 support level mentioned before finding a bottom later that year. Currently, with 30-day implied volatility for NZD/USD options sitting near 12-month lows of around 9.2%, the market may be underpricing the risk of a sudden shock.

Create your live VT Markets account and start trading now.

Start trading now – Click here to create your real VT Markets account

USD/THB has risen more than 4% month-to-date as markets reduced expectations of near-term US Federal Reserve easing. Higher oil prices have also worsened Thailand’s terms of trade.

OCBC describes the Thai baht as highly exposed to energy price moves and shifts in risk sentiment. USD/THB remains in a bullish trend even though technical indicators suggest it is overbought.

Near Term Drivers For The Baht

Lower gold prices, combined with an oil-driven terms-of-trade shock and a firmer US dollar, point to near-term pressure on THB. OCBC also links THB weakness to broader US dollar direction and regional risk sentiment.

Developments around the Strait of Hormuz may offer short-term support to THB, while the outlook depends on energy prices and geopolitics. Key support levels are 32.10 (200-day moving average and 61.8% Fibonacci retracement) and 31.90 (50% Fibonacci retracement).

We are seeing a familiar pattern in the USD/THB, reminiscent of the dynamics we noted back in early 2025. The Thai baht is again under pressure due to a combination of a strengthening U.S. dollar and a sharp rise in energy prices. This situation presents clear risks and opportunities for derivative traders in the coming weeks.

The broader rebound in the dollar is being fueled by recent U.S. economic data, with the latest Consumer Price Index coming in unexpectedly high at 3.1%, dampening expectations for a near-term Federal Reserve rate cut. Simultaneously, Brent crude oil futures have surged past $95 per barrel for the first time in over a year amid fresh geopolitical tensions in the Middle East. As Thailand is a net oil importer, this directly hurts its economic outlook.

Trade Setups And Key Levels

Given these headwinds, traders should consider strategies that benefit from further baht weakness. Buying USD/THB call options with strike prices around 37.00 could offer leveraged exposure to the upside while limiting downside risk. This approach is particularly suitable as the pair shows bullish momentum, even if technical indicators suggest it is becoming overbought.

We view the baht as one of the region’s most vulnerable currencies to swings in energy prices and global risk sentiment, a weakness we also saw play out in 2025. This sensitivity suggests that any further escalation in geopolitical risk or hawkish surprises from the Fed could accelerate the move higher in USD/THB. For traders anticipating a continued trend, this environment supports bullish positions.

Those looking to hedge or express a contrarian view might see current levels as an opportunity to enter into forward contracts to sell USD at more favorable rates. However, this requires a strong conviction that either energy prices will retreat sharply or that global risk sentiment will improve significantly. These factors currently show little sign of turning in the baht’s favor.

Historically, periods of synchronized dollar strength and high oil prices have consistently pushed the pair higher, as was the case in 2025. Traders should watch for the key support level of 36.20, which represents the 50-day moving average. A failure to hold this level could signal a temporary pause, but the underlying risks still point towards a softer baht for now.

Create your live VT Markets account and start trading now.

Start trading now – Click here to create your real VT Markets account