Start trading now – Click here to create your real VT Markets account

Back

Start trading now – Click here to create your real VT Markets account

Key Points

Oil prices pushed higher on Thursday as the widening conflict between the United States and Iran continued to disrupt flows through the Middle East. Brent crude rose $1.67, or 2.05%, to $83.07 per barrel by 0141 GMT, while U.S. West Texas Intermediate climbed $1.94, or 2.60%, to $76.60.

The move reflects growing anxiety in the energy market after shipping through the Strait of Hormuz, one of the world’s most critical energy corridors, slowed to a near halt.

The route normally carries close to one-fifth of global energy consumption, which makes even short disruptions highly sensitive for traders and governments.

Markets also reacted to the expansion of the U.S.–Iran war. On Wednesday, a U.S. strike hit an Iranian warship off Sri Lanka, and U.S. Senate Republicans voted against a bipartisan resolution that aimed to stop the air war and require Congress to authorise hostilities.

This political backing signals that the military campaign could continue in the near term.

If tensions persist, traders may continue to price a geopolitical premium into crude. However, the market still watches how long the disruption lasts. Short conflicts often lead to fast spikes that fade once shipping resumes.

Shipping through the Strait of Hormuz has ground to a near halt for the fifth day, creating a sudden bottleneck for energy exports. J.P. Morgan estimates that about 329 oil vessels are stuck in the Gulf, unable to safely move cargo through the narrow channel.

Security concerns remain high after Britain’s maritime trade operations agency reported a large explosion heard and seen by the master of a tanker anchored 30 nautical miles southeast of Kuwait’s Mubarak Al Kabeer. A small craft was later seen leaving the area, adding to fears that commercial vessels may become targets.

Even though Iran has avoided striking most major energy infrastructure so far, shipping risk remains elevated. Traders often respond to such risks by bidding up crude futures to secure supply, which partly explains the current rally.

If the blockage continues, refiners in Asia and Europe may face delayed shipments. That scenario could tighten physical markets and push prices further upward in the short term. If naval patrols reopen the route quickly, price pressure may ease.

At the same time, production disruptions across the region have reduced the buffer normally available during geopolitical crises.

Iraq, the second-largest crude producer in OPEC, has cut output by nearly 1.5 million barrels a day due to storage shortages and the lack of a viable export route. With exports constrained, producers cannot move crude even if wells remain operational.

Meanwhile, Qatar declared force majeure on gas exports, with sources indicating that a return to normal production volumes may take at least a month. Qatar remains the largest liquefied natural gas producer in the Gulf, so any prolonged halt may tighten global gas markets as well.

These developments arrive at a time when energy inventories in several regions already sit near seasonal averages. Reduced output combined with blocked shipping could create short-term shortages in some markets, which would support oil prices if the situation drags on.

WTI crude oil (CL-OIL) is trading near $76.97, up around 1.17%, extending the strong upward momentum that has been building since the December low near $54.87. The daily chart shows a clear bullish trend, with price continuing to print higher highs and higher lows while accelerating into the upper range of the recent rally.

From a technical perspective, price is trading well above its key moving averages. The 5-day moving average (73.22) and 10-day (69.57) are rising sharply, while the 20-day (66.77) and 30-day (65.61) remain significantly below the current price level.

This widening spread between price and the longer-term averages reflects strong bullish momentum following the breakout above the $70 area.

Immediate resistance is seen around $77.50–$78.00, where the latest rally is approaching a short-term ceiling. A sustained break above this zone could open the path toward $79.80–$80.00, a key psychological and technical level.

On the downside, initial support is located near $73.00–$74.00, followed by stronger structural support around $70.00, where the short-term moving averages are clustered.

Overall, the trend remains constructive while prices hold above the $73–$74 region, though the sharp upward move may invite periods of consolidation before the next directional push.

Learn more about trading Energies on VT Markets here.

Start trading now – Click here to create your real VT Markets account

Start trading now – Click here to create your real VT Markets account

Start trading now – Click here to create your real VT Markets account

Start trading now – Click here to create your real VT Markets account

Start trading now – Click here to create your real VT Markets account

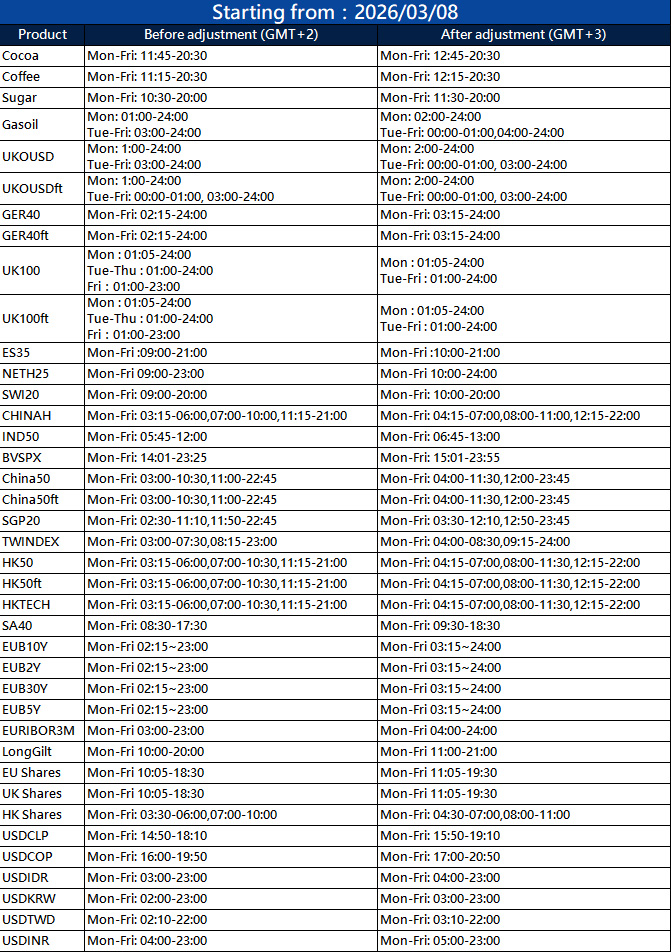

Dear Client,

The trading hours of some MT4/MT5 products will change due to the upcoming Daylight-Saving Time change in US.

Please refer to the table below outlining the affected instruments:

Notification of Trading Adjustment

System time will be adjusted from winter time GMT+2 to daylight saving time GMT+3.

The above information is provided for reference only; please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected]

Mexico is entering an economic landscape that reflects both strengths and challenges. Macroeconomic stability remains moderate, with GDP growth projections between 1.2% and 1.5%, low formal unemployment, and an exchange rate of less than 18 pesos per dollar. However, inflation has shown a slight acceleration, reaching 3.77% in the first half of January, which calls for greater vigilance in monetary policies.

Fintech sector dynamics

Mexico’s fintech ecosystem continues to mature, focusing on digital payments, crypto assets, and innovative Defi solutions that respond to the demand for financial inclusion. In 2025, 131 new ventures were registered, contributing to growing revenues and an expanding market, in which regulation and technology adoption play a key role. This growth positions Mexico as a regional hub, attracting investment and specialized talent in a predictable but cautious economic environment.

Money Expo Mexico 2026

This event is celebrating its fourth edition on February 18 and 19 at the Banamex Center, establishing itself as the most important financial event for trading, investment, fintech, and blockchain in the country. In a context of regional fintech growth, it offers workshops, market analysis, and B2B opportunities for professionals and institutions.

VT Markets returns after participating in the inaugural edition in 2023, highlighting its commitment to the global financial community. This year, it intensified its presence with two activities led by Eduardo Romero, senior market analyst, on the first day, with a round table discussion entitled “Preparing for the future: what will really change the markets in 2026?”; and a presentation on the second day of the event, entitled “The new trading game: how professionals operate in highly uncertain markets.”

“Since last year, with Donald Trump’s presidency, we’ve seen a series of aggressive trade measures that have increased market volatility and kept investors and traders on constant alert. High-profile issues like the political situation between Iran and the United States trigger market movements,” says Eduardo Ramos, Senior Market Analyst at VT Market.

As an investor, navigating market uncertainty can be a constant challenge. Therefore, Eduardo Ramos, drawing on his expertise, emphasizes that “stability coexists with periods of uncertainty; the difference lies not in predicting the market, but in operating with a solid method for reading and analyzing data.”

This participation underscores the collaboration with industry professionals in a rising fintech hub such as Mexico.

Start trading now – Click here to create your real VT Markets account

Start trading now – Click here to create your real VT Markets account

Hello there 👋

Hello there 👋

Scan the QR code with your smartphone to start a chat with us, or click here.

Don’t have the Telegram App or Desktop installed? Use Web Telegram instead.

{kind=link}