During Asian trading, GBP/USD holds near 1.3565, preserving weekly gains as trade-policy uncertainty weighs on the US Dollar

Sterling held weekly gains near 1.3565 against the Dollar in Thursday’s Asian session. The Dollar stayed under pressure as traders faced uncertainty over US trade policy. The US Dollar Index (DXY) edged lower to around 97.55.

GBP/USD rose 0.42% on Wednesday and moved back toward 1.3600. The pair had traded for several days in a roughly 1.3450 to 1.3520 range. The rebound followed a pullback from the late-January high near 1.3870 and pushed price back toward the 20-day EMA.

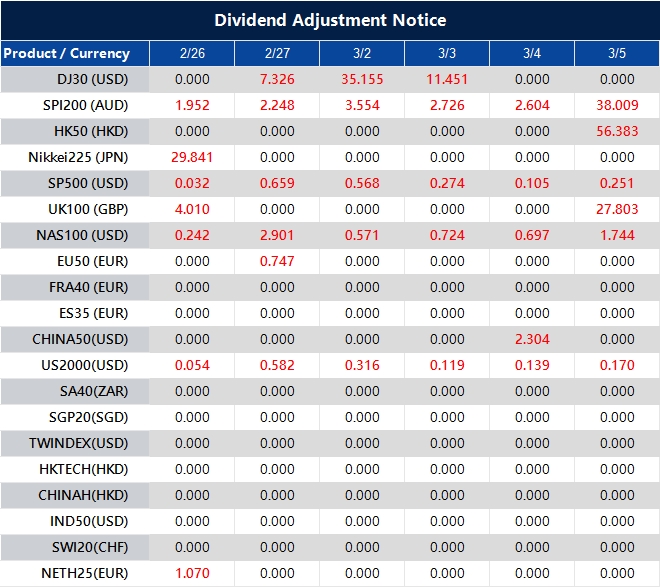

Dividend Adjustment Notice – Feb 26 ,2026

Dear Client,

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

Trump’s Tariffs Ruling: When Consumers Lose, But Corporations Stand To Gain

On 20 February 2026, the US Supreme Court delivered one of the most consequential trade rulings in modern American history.

In a 6-3 decision on Learning Resources v. Trump, the Court struck down 70% of the tariffs imposed under President Trump’s “Liberation Day” executive orders, ruling that the International Emergency Economic Powers Act (IEEPA) does not grant the President the power to tax, a right strictly reserved for Congress.

The ruling was widely hailed as a return to constitutional order.

But the immediate aftermath has been anything but orderly. Markets are recalibrating, the dollar is under pressure, and a $175 billion question now hangs over the economy.

Here is what traders need to understand about the financial fallout, and whether these tariffs ever made economic sense in the first place.

The Financial Fallout

The Court’s decision has created an immediate fiscal vacuum. Since April 2025, the US government collected roughly $175 billion in duties that are now considered unlawful, and the refund process is shaping up to be a costly ordeal.

Large corporations, like Walmart, Costco, and LVMH have the legal firepower to file thousands of claims and are first in line to reclaim billions. The problem is that roughly 90% of those tariff costs were already passed down to consumers through higher retail prices.

Ordinary shoppers will see none of that $175 billion return. Instead, the money flows back to corporate balance sheets, where it is more likely to fuel stock buybacks than lower the price of goods.

Within hours of the ruling, the White House moved to plug the gap. The administration invoked Section 122 of the Trade Act of 1974, imposing a temporary 15% global surcharge as a strategic bridge while it explores more durable measures under Sections 301 and 232.

However, experts are already pushing back. Section 122 was designed for the gold-standard era of the 1970s and is widely considered ill-suited to today’s floating exchange rate environment. That near-guarantees a fresh round of litigation and prolonged uncertainty for businesses trying to plan.

The Fiscal-Monetary Intersection

The ruling has fundamentally reshaped the outlook for both the US dollar and equity markets, and the effects are moving through two distinct channels: fiscal and monetary, with the Federal Reserve sitting squarely at the centre of the storm.

The most immediate pressure point is the federal budget. The sudden loss of approximately $150 billion in annual tariff revenue has punched a significant hole in a budget already under considerable strain, with the national debt standing near $38.7 trillion.

To offset that lost revenue, the government will need to increase Treasury issuance. That means more debt flooding into the bond market.

That surge in supply is pushing yields higher, particularly at the long end of the curve. For equity markets, this “yield squeeze” cuts both ways. Higher yields raise the cost of borrowing and crowd out private investment, weighing most heavily on tech-heavy stocks that are especially sensitive to rising rates.

On the currency side, the near-term picture points to mild downside pressure on the dollar. With tariff removal easing imported inflation, markets are increasingly pricing in earlier or deeper rate cuts from the Federal Reserve, which narrows the interest rate differentials that had previously supported the greenback.

The medium-term trajectory, however, is defined by a deeper tension. If interest payments on the ballooning national debt continue to outpace primary government expenditure, the US could find itself effectively printing money to cover the shortfall.

It’s a scenario that would inflict significant structural damage on the dollar.

To defend the dollar’s reserve currency status, the Federal Reserve under Kevin Warsh may need to adopt aggressive hard money tactics.

That could mean cutting rates strategically to ease the government’s interest burden, halting Treasury bill purchases to stop further monetary expansion, and uncapping bank cash-holding ratios to drive internal demand for the dollar within the financial system.

Did The Tariffs Actually Help the US?

To answer that fairly, the rhetoric needs to be set aside and the 2025 data examined on its own terms.

The primary justification for the tariffs was to close the trade gap. According to the Bureau of Economic Analysis, the 2025 trade deficit came in at $901.5 billion, a negligible 0.2% improvement from 2024.

Even where imports were disrupted, the adjustment largely came through trade diversion rather than the promised reshoring of American industry. Companies simply sourced from alternative countries, while retaliatory measures from trading partners dampened demand for US exports.

The jobs story is equally sobering. The tariffs were marketed as a lifeline for the American heartland, but between April and December 2025, the manufacturing sector shed 72,000 jobs.

Because roughly half of US imports are inputs for domestic production, like parts, chemicals, and raw metals, the tariffs effectively acted as a tax on American factories, eroding their global competitiveness rather than strengthening it.

On the fiscal side, tariff revenues proved largely cosmetic.

Once stripped out, the federal deficit under the tariff regime was larger than headline figures suggested, leaving the structural problem of fiscal overspending completely untouched.

With federal debt now approaching $39 trillion, the Court’s ruling has exposed an uncomfortable truth: tariffs were never a durable solution to America’s budget imbalance.

Final Verdict: Was The US Better Off?

Financially and structurally, the answer is no. A handful of primary metal producers saw a brief uptick in activity, but the broader economy absorbed higher consumer costs and a contraction in manufacturing employment. The gains were narrow; the pain was widespread.

The Supreme Court has corrected a constitutional overreach, and that matters. But the ruling has also laid bare what might be described as a robbery in plain sight. The public paid the tax, the government spent the revenue, and now corporations will keep the change. The $175 billion does not return to the people who funded it.

FAQ

What should traders be aware of following this Supreme Court ruling?

Watch Treasury yields for signs of further upward pressure as debt issuance rises. Monitor the dollar closely. Near-term weakness is likely as rate cut expectations build, but the medium-term picture depends heavily on how aggressively the Fed moves to shore up dollar credibility.

Finally, keep an eye on equity markets, particularly the tech sector, where the yield squeeze will continue to test valuations.

What does Section 122 say about tariffs?

Section 122 is a part of the Trade Act of 1974 that gives the US President a temporary authority to impose tariffs without long investigations or detailed reviews. This provision allows the US president to impose tariffs of up to 15%.

Trade activities under this provision can only last for 150 days unless extended through other trade authorities.

How did the Federal Reserve react to the US Supreme Court ruling on Trump’s tariffs?

Federal Reserve officials downplayed major policy shifts.

Fed Governor Christopher Waller stated the ruling would not significantly alter his interest rate outlook, supporting a pause on cuts if labour markets stabilise, and emphasised looking past temporary tariff effects on inflation.

Chicago Fed President Austan Goolsbee suggested the decision could help cool inflation.

St. Louis Fed President Alberto Musalem noted that replacement tariffs under other laws like Section 122 would leave his forecasts largely unchanged, though he plans to speak with CEOs to understand the impact of tariff uncertainty on companies.

Silver rises for a second day amid White House policy uncertainty, nearing $90 in Asian trading hours

Silver rose for a second straight day, trading near $90.00 per troy ounce during Asian hours on Thursday. Demand for safe-haven assets increased as uncertainty grew around White House economic policy.

In Tuesday’s State of the Union address, Donald Trump gave no sign that tariffs will ease. Section 122 tariffs were raised to 10%, after earlier threats of 15%. This followed a Supreme Court ruling 10 months ago that struck down country-specific tariffs under IEEPA.

Geopolitical Risks Support Prices

Geopolitical tensions also lifted prices. Trump threatened military action against Iran if talks fail. Iran said US bases in the Middle East would be targets, putting tens of thousands of US service members at risk. US-Iran nuclear talks were scheduled for Thursday in Geneva. Silver’s gains may be capped as expectations for near-term Federal Reserve rate cuts fade. Austan Goolsbee said progress on inflation has stalled and that 3% inflation is still above the 2% target. Susan Collins said keeping rates steady for some time appears appropriate. IMF Managing Director Kristalina Georgieva said tariffs have partly pushed up US goods inflation. She added that a federal funds rate of 3.25%–3.5% would support a return to full employment, and that reducing public debt will require decisive fiscal action. With silver near $90.00, markets are facing elevated uncertainty tied to US policy and Middle East tensions. This backdrop points to large price swings in the weeks ahead. Derivatives traders may be better served preparing for volatility rather than betting on a single direction.Positioning For Volatility

The Geneva talks with Iran are a key catalyst that could drive prices higher. If negotiations break down, silver could move toward $100 as safe-haven demand grows. One way to position for this is with call options, which can capture upside while limiting risk if diplomacy succeeds. At the same time, the Federal Reserve remains focused on inflation, which is still near 3%. In 2024, inflation stayed stubbornly high—often above 3.1%—and that delayed rate cuts. If the economy shows continued strength, the market could lean further into a “higher for longer” rate outlook. In that case, put options can help hedge against a sharp pullback from current highs. With strong forces on both sides, a strategy that benefits from a big move either way—such as a long straddle—may make sense. It could profit from a surge driven by conflict or a drop if Fed hawkishness takes over sentiment. Today’s price is far above the $25–$30 range seen through much of 2024 and 2025, which suggests a quick return to calm is unlikely. Silver is also outperforming its peers. The gold-to-silver ratio has tightened sharply from around 85:1 in 2024, which suggests silver is currently the preferred safe-haven. Traders should watch this ratio closely, as a reversal may be an early sign that momentum is shifting away from silver. Create your live VT Markets account and start trading now.As US-Iran nuclear talks near, traders support the Canadian dollar, pushing USD/CAD lower near 1.3665

USD/CAD fell for a second straight day on Thursday, pulling back from the monthly high set earlier in the week. It traded near 1.3665, down almost 0.20% on the day. Losses were limited as traders waited for US-Iran nuclear talks.

The US dollar weakened as uncertainty returned around US President Donald Trump’s trade policy. This followed a Supreme Court ruling last Friday that blocked broad tariffs. Trump then announced a new framework, keeping the overall trade agenda in place.

Temporary Tariffs And Trade Uncertainty

On Wednesday, Trump said the White House would apply temporary global tariffs of 10% for 150 days under Section 122. He also said the administration is aiming to raise duties to 15%. That raised concerns about retaliation and supply chain disruptions. A stronger tone in equity markets also reduced demand for the dollar as a safe haven. Oil prices stayed near the weekly low after a sharp rise in US stockpiles, although supply risks tied to a possible US-Iran conflict helped support prices. Lower oil prices offered only limited support to the Canadian dollar, which often moves with commodities. Without clearer follow-through, this may limit further downside in USD/CAD. USD/CAD is also trading with a softer tone around 1.3450, reflecting ongoing uncertainty around the US dollar. This is similar to the volatility seen last year, after temporary 10% global tariffs were announced in early 2025. Those policy moves also had lasting effects on inflation expectations in both countries.Inflation And Central Bank Divergence

The effect of those tariffs is now showing up in inflation data. With US CPI at 3.1% and Canadian CPI slightly lower at 2.9%, traders are expecting central bank policy to diverge. This small gap is supporting the view that the Bank of Canada may cut rates sooner than the Federal Reserve. This potential split in policy is a key factor pushing the pair lower. Markets are pricing in about a 60% chance of a Bank of Canada rate cut by June, while expectations for a Fed cut have shifted into the third quarter. This outlook supports a weaker USD versus the CAD over the medium term. However, weaker commodities are limiting CAD strength. WTI crude is struggling to stay above $78 a barrel after the latest EIA report showed a surprise build of 3.5 million barrels in US inventories. Softer oil prices are weighing on the loonie and keeping USD/CAD from falling faster. In options markets, one-month implied volatility for USD/CAD is near a low of 5.8%, suggesting traders do not expect large near-term swings. Even so, risk reversals show a small bias toward CAD calls. This suggests options traders are positioning for modest CAD strength. In other words, while spot trading looks cautious, broader sentiment still points to lower USD/CAD. With mixed signals, traders may prefer strategies that benefit from a gradual decline in the pair. Buying out-of-the-money CAD call options can be a low-cost way to position for a drop in USD/CAD while limiting risk. Caution is still needed, because weak oil prices could cap Canadian dollar gains. Create your live VT Markets account and start trading now.BoJ board member Hajime Takata says the central bank should keep raising rates gradually and cautiously

BoJ board member Hajime Takata said the bank should keep raising rates, but do so slowly. He said policy normalisation should avoid market moves that go beyond the risk premium investors have already priced in.

He said overseas economies are growing at a moderate pace, though some regions are weakening. He added that Japan’s deflation risks have eased, so the BoJ should pay more attention to rising prices.

Policy Normalisation Stays Gradual

He said a sharp US-style slowdown caused by tighter credit looks unlikely. He also said Japan’s real short-term interest rates are still well below zero, even after the December rate increase. He warned that if Japan’s policy path keeps diverging from other countries, volatility could rise—especially in foreign exchange markets. He said the BoJ is now at a point where it should consider shrinking its balance sheet and slowly reducing its purchases of Japanese government bonds (JGBs). He said weak demand for super-long JGBs needs close monitoring, including at the June interim review of the taper plan. He added that the BoJ may need to respond flexibly—including buying JGBs—if market functioning deteriorates. USD/JPY was 0.35% lower at 155.90. The BoJ aims for about 2% inflation and raised rates in March 2024 after years of QQE, negative rates, and yield curve control.Implications For Traders And Markets

The Bank of Japan’s message points to continued, gradual rate hikes in the weeks ahead. Core inflation has stayed above the 2% target for most of 2025, and it was 2.6% in January 2026. That gives the central bank room to keep normalising policy. For currency traders, this supports the case for a stronger yen. The policy gap that drove the yen lower in 2022 and 2023 is now narrowing. That makes long-yen positions—using options or forwards—look more attractive. It may make sense to position for a steady decline in USD/JPY, potentially toward 150, rather than expecting a sudden, volatile fall. In rates markets, the easier path for JGB yields still looks higher. The 10-year JGB yield has already risen from under 1% in early 2025 to around 1.25%. Trades that benefit from higher yields, such as shorting JGB futures, may fit this trend. At the same time, the BoJ has made it clear it wants to avoid a disorderly sell-off, especially in the super-long end of the curve. The repeated focus on avoiding “significant market volatility” is also a warning not to take overly aggressive positions. The direction may be clear, but the BoJ could step in if it thinks moves are happening too fast. That creates a risk of sharp, short-term reversals. Because of this, options strategies that cap downside risk—or that benefit from a slow, low-volatility move—may be a better fit. Create your live VT Markets account and start trading now.China’s central bank fixed USD/CNY at 6.9228, down from 6.9321 and below Reuters’ 6.8605 estimate

The People’s Bank of China (PBOC) set the USD/CNY central rate for Thursday at 6.9228. This compared with the prior day’s fix of 6.9321 and a Reuters estimate of 6.8605.

The PBOC’s main policy goals are to keep prices stable, including the exchange rate, and support economic growth. It also focuses on financial reforms, such as opening and developing China’s financial markets.

Central Bank Governance Structure

The PBOC is owned by the People’s Republic of China and is not considered fully independent. The Chinese Communist Party committee secretary, nominated by the chairman of the State Council, has major influence over the bank’s management and direction. Pan Gongsheng holds both roles. The bank uses many policy tools, including the seven-day reverse repo rate, the Medium-term Lending Facility, and foreign exchange intervention. It also uses the Reserve Requirement Ratio (RRR) and the Loan Prime Rate (LPR). These affect loan, mortgage, and savings rates, and can also influence the renminbi exchange rate. China allows private banks, with 19 in total. The largest are digital lenders WeBank and MYbank, backed by Tencent and Ant Group. Rules introduced in 2014 allowed privately funded domestic lenders to operate alongside the state-led system. Today’s daily yuan fixing was set much weaker than the market expected. This suggests authorities may be more comfortable with a softer currency. The gap between the official fixing and market expectations is where we see potential opportunity. We should read this as a sign that policymakers may put near-term economic support ahead of strict currency stability.Market Strategy Implications

This move likely responds to weaker economic momentum. China’s January 2026 export data showed a 1.5% year-on-year decline, missing the consensus forecast. A weaker yuan makes Chinese goods cheaper overseas, so we should expect policy to keep leaning in that direction. This supports the view that the most likely path for the currency is lower in the coming weeks. We saw similar weaker-than-expected fixings throughout 2025. These often came before periods of managed depreciation. This history suggests the central bank is using a familiar approach to support the economy. As a result, trading against this policy signal would likely be a low-probability approach. Given this backdrop, we should consider buying volatility through options on the offshore yuan (CNH). Policy uncertainty often leads to larger price swings. The CNH implied volatility index has already risen to 6.8% this week, its highest level since the fourth quarter of 2025. Strategies that benefit from a directional move—such as buying USD/CNH call options—now look more attractive. The next key catalyst is the National People’s Congress, which begins next week and will set the official 2026 GDP growth target. A modest target below 5% would likely confirm this easing bias and strengthen the case for short-yuan positions. We will watch for any wording from policymakers that clearly puts growth ahead of reform. Create your live VT Markets account and start trading now.Rubio says Iran has long threatened America; refusal to discuss missiles complicates negotiations as talks focus on its nuclear programme

US Secretary of State Marco Rubio said Iran has been a serious threat to the United States for a long time. He said Thursday’s talks will mainly focus on Iran’s nuclear program.

Rubio said Iran is not enriching uranium right now, but is trying to reach that capability. He also said Iran has conventional weapons designed to attack the United States.

Irans Ballistic Missile Issue

He said Iran is trying to develop intercontinental ballistic missiles. Rubio said Iran’s refusal to discuss ballistic missiles is a major problem. Rubio said diplomacy should still be on the table. He called Thursday’s meeting the next opportunity for talks. He also said the current situation in Cuba cannot continue. He said Cuba needs major change. In market moves, gold (XAU/USD) was up 0.05% at $5,167 at the time of writing. West Texas Intermediate (WTI) was down 1.01% at $65.60.Trading Implications And Risk

These comments about Iran’s ballistic missile program being a “major problem” add real uncertainty, and markets often reprice quickly when uncertainty rises. With WTI near $65, the market may be underestimating the risk that diplomacy fails, which could threaten oil supply through the Strait of Hormuz. One approach is to buy out-of-the-money call options on crude oil futures. They can be a lower-cost way to benefit from a sudden price jump if tensions escalate. Supply shocks like the disruptions in 2025 show how fast prices can spike. Recent shipping data says more than 20% of the world’s daily oil supply moved through the Strait of Hormuz last year. Any military activity in that corridor would disrupt global shipping and likely push oil prices higher, which would support those call options. Gold is already above $5,100, which suggests investors are seeking safer assets. Central banks have been steady buyers over the past year, and inflation data from late 2025 has stayed stubbornly high, helping support prices. If rhetoric on Iran stays intense, gold could attract even more demand. Call spreads may offer a way to target further upside while limiting the high cost of outright calls. This geopolitical tension can also spark broader volatility, which has been fairly low so far this quarter. The VIX, a measure of expected market volatility, is up about 10% over the last two weeks from its February lows. Buying VIX futures or call options is a direct way to position for a breakdown in talks that could trigger a wider sell-off and a jump in fear. Still, diplomacy has not been ruled out. A breakthrough would likely reduce tensions, push oil prices lower, and support a market rally. To hedge that outcome, we could consider buying puts on major energy-sector ETFs as insurance in case unexpectedly positive news defuses the standoff. Create your live VT Markets account and start trading now.TD Securities expects USD/CNY to ease steadily toward 6.7, with authorities limiting volatility while tolerating yuan strength

TD Securities strategists expect Chinese authorities to keep USD/CNY volatility low through China’s 2026 Two Sessions. They do not expect officials to push back against a stronger yuan during this period.

They forecast USD/CNY will drift down to 6.7 by the end of 2026, in line with broader US dollar weakness. They add that the pair could reach 6.7 by mid-2026 if the current pace continues.

Post Two Sessions Policy Outlook

After the Two Sessions end on 11 March, they expect possible changes to structural foreign exchange settings. These steps would aim to slow further yuan gains and reduce one-sided moves in the exchange rate. Authorities are likely to keep USD/CNY volatility very low during China’s most important political event of the year. TD Securities believes the People’s Bank of China is not resisting appreciation and would allow a gradual decline in the exchange rate. Their forecast points to a move toward 6.7 by year-end, in line with broad US dollar weakness. Recent data supports this view. China’s exports rose 5.2% year-on-year in January, beating expectations. This strength may give officials more comfort to let the currency firm. The PBoC has also been setting the daily fixing stronger than market estimates, which signals it is comfortable with the current trend. On the other side, the US dollar has been under pressure after a softer-than-expected Core PCE inflation report last month. Core PCE rose just 0.2%, which increased market expectations that the Federal Reserve could ease policy later this year. The dollar index also fell sharply through much of 2025 as the global recovery became more broad-based.Strategy Implications For Options Traders

For the next two weeks, until the Two Sessions conclude on March 11, low volatility looks like the most likely outcome. This could favor selling volatility—such as short straddles or strangles—to collect premium. USD/CNY is trading near 6.82, and they expect it to remain in a tight range. After mid-March, positioning for a further decline in USD/CNY may make sense. Buying put options with second-quarter expiries could capture a move toward the 6.7 level. The pace of appreciation has been fast, and TD Securities’ year-end forecast could be reached as early as this summer. However, traders should watch for policy tweaks after the political event. If the yuan strengthens too quickly, authorities may adjust FX settings to slow the move. That could create risk for traders who are positioned too aggressively for further yuan strength after March. Create your live VT Markets account and start trading now.IMF’s Georgieva said tariffs have partly influenced US goods inflation

IMF Managing Director Kristalina Georgieva said tariffs have had some effect on US goods inflation. She also said a federal funds rate of 3.25% to 3.5% fits with the US economy returning to full employment.

She said bringing US public debt down will take firm, sustained action. She added that the IMF shares the Trump administration’s concern about rising US trade and current account deficits.