Schmid believes the FOMC can assess the inflation impact of tariffs before making rate decisions.

Jeff Schmid is the president and CEO of the Federal Reserve Bank of Kansas City. He notes that jobs and inflation are nearly where the Federal Reserve wants them to be.

The central bank has time to explore how tariffs might impact inflation before making decisions about changing interest rates. The strength of the economy allows the Fed to take a cautious wait-and-see approach on possible rate cuts.

NZD/USD pair climbs to 0.6035 as new buyers enter around 0.6000 level

The NZD/USD pair is currently trading near its weekly high at about 0.6035, thanks to a weaker US Dollar. This follows a three-day rebound from a recent one-month low, as investors expect the Federal Reserve to lower borrowing costs.

The USD Index is close to a one-week low, despite Fed Chair Powell’s aggressive remarks. Optimism around a ceasefire between Israel and Iran, along with a positive market atmosphere, is reducing the Greenback’s appeal as a safe haven, benefiting the Kiwi currency.

New Zealand Trade Data

New Zealand’s trade data exceeded expectations, supporting the NZD/USD pair. The monthly trade surplus was NZ$1.235 billion, while the annual deficit was NZ$3.79 billion in May. Expectations for further rate cuts by the Reserve Bank of New Zealand could limit significant gains for the NZD. The repeated difficulties near the 0.6065-0.6070 resistance levels make traders cautious, as they wait for a clear breakout above this barrier. The Kiwi’s value is influenced by the state of New Zealand’s economy, central bank policies, and China’s economic performance. Changes in dairy prices, New Zealand’s main export, also impact the currency’s value. The Reserve Bank aims for medium-term inflation between 1% and 3%, which affects the NZD/USD relationship. Looking at the recent price movement of the NZD/USD pair, the current rise around 0.6035 is mainly due to a softer US Dollar rather than strong Kiwi performance. This shift reflects changing expectations about the Federal Reserve’s future borrowing costs. Even though Powell kept a hawkish tone, markets are sensing some potential for rate relief in the medium term. This difference has led the USD Index to drop to a one-week low. Safe-haven demand is also waning as geopolitical concerns, especially in the Middle East, ease. A temporary ceasefire reduces the Greenback’s appeal, shifting interest toward risk-sensitive currencies like the NZD.Technical Dynamics and Market Sentiment

Domestically, New Zealand’s trade balance data exceeded forecasts with a monthly surplus of NZ$1.235 billion. While the annual trade gap is more cautious, this immediate boost in exports is significant for those monitoring the Kiwi. A positive trade performance helps strengthen the NZD, particularly when China—an important trading partner—maintains stable demand. However, challenges remain. The Reserve Bank of New Zealand is navigating ongoing price pressures and declining domestic demand. Market discussions are trending toward more dovish policies in the upcoming months, which could limit substantial upward momentum for the NZD. Technically, the 0.6065 to 0.6070 zone has proven to be a strong resistance level. The price has struggled here multiple times, indicating uncertainty that keeps short-term excitement in check. Until we see a clear break above downward trends or former resistance levels, optimism will be cautious at best. The currency is influenced by several factors. Commodity prices, especially dairy (New Zealand’s main export), are critical drivers. Changes in global milk powder auctions affect exchange rates, so monitoring upcoming GDT releases is essential. Additionally, domestic inflation targeting within the 1% to 3% range guides RBNZ policy, and any fluctuations will impact interest rate futures and the NZD. Traders need to stay flexible. Support for the pair is near the 0.6000 mark, and falling below this level could lead to a broader drop towards early-June levels. Volatility will likely stem from various sources: US economic data, market sentiment shifts, and changes in expectations regarding China’s growth. Ultimately, patience is key, and traders should balance short-term price signals with broader, slower-moving macro factors. Create your live VT Markets account and start trading now.US and Israeli strikes reportedly delay Iran’s nuclear program by two years amid concerns of rebuilding

The early US intelligence assessment indicates that recent strikes on Iran didn’t cause major damage to the country’s nuclear sites. However, Israeli officials believe that the combined military actions of the US and Israel have delayed Iran’s nuclear program by two years.

Israel argues that Iran’s program was already delayed by two years before the US operation. However, Israeli officials are determined to stop Iran from easily rebuilding its nuclear capabilities.

The situation remains tense and could lead to conflicts unless there is a change in the Iranian leadership, which is often left out of discussions. It seems Israel will keep watch and may try to disrupt Iran’s nuclear activities.

This scenario blends intelligence with military strategy amid ongoing tension between long-time rivals. Initial American intelligence suggests little physical damage to Iran’s nuclear infrastructure, which may seem to lessen the impact of the strikes. Nonetheless, this does not capture the broader goals of their joint mission.

From Tel Aviv’s viewpoint, Iran’s timeline for nuclear development has already been extended by two years, a conclusion reached even before the latest strikes. This implies that Israeli officials see the recent attacks not as a start but as a continuation of efforts to maintain that delay and prevent any swift rebuilding. Their strategy is an ongoing campaign rather than a single action.

Netanyahu and his defense team show readiness to act consistently instead of just reacting in urgency. Their aim goes beyond halting progress; they want to create regular disruptions. It’s no longer about one-off attacks. They’ve established a pattern to keep up pressure, even if growth seems to be stalled. This strategy depends heavily on surveillance and timely action as much as it does on airstrikes and sabotage.

The underlying theme requires constant vigilance. Acceleration in Iran’s nuclear activities could happen quietly, without any headlines, and Israel cannot afford to give them any space. Their goal is to restrict not just figuratively but literally the ability to enrich uranium or develop missile sites. Air bases, logistics, and enrichment facilities are all targets under this strategy.

Raisi’s silence on the issue has been noteworthy, and what he doesn’t say is significant. In military and political circles, this silence suggests a lack of confidence or perhaps indicates that Iran is still assessing the damage, which could signify hesitation in their response. When public statements are absent, covert adjustments are likely taking place.

For those interested in future developments, the risk premiums related to geopolitical tension aren’t merely speculative; they’re based on actual state actions and efforts to limit the growth of adversarial capabilities. This creates temporary imbalances in anticipated market volatility, leading to sudden shifts not grounded in material change. High volatility related to Gulf assets may not be limited to oil prices alone.

In summary, we need to consider factors beyond just visible weaponry or public statements. Timelines, hesitations, and strategic targeting create a pattern that demands responsive actions rather than mere predictions. Short-term options are more appealing not just because of macro changes, but due to the nature of immediate retaliation and sudden changes in tactics.

We should also examine trailing indicators—like logistics delays, power fluctuations near known development sites, and shifts in air defense systems. These are all part of a broader strategy. Calculated patience doesn’t equate to inaction.

As traders, it’s crucial to understand how responsive measures can turn into proactive disruptions. Those with advanced intelligence can act before news breaks. Movements in regional currencies, defense stocks, and shipping indexes might serve as an early warning system. Given the events of the past month, we should be preparing for ongoing pressure in various forms rather than waiting for a climactic moment.

GBP/USD remains on an upward trend above 1.3600, recently hitting 1.3648, its highest level since February 2022.

The GBP/USD is rising as the US Dollar weakens because of reduced demand for safe-haven assets following a ceasefire between Israel and Iran. Comments from Fed Chair Powell indicate that rate cuts may be delayed until the fourth quarter. Meanwhile, the British Pound (GBP) could face challenges due to the Bank of England’s (BoE) dovish policies.

The GBP/USD pair has increased for three sessions in a row, trading near 1.3620 during the Asian trading hours on Wednesday. It is close to a peak of 1.3648, the highest level since February 2022. Improved risk sentiment after tensions in the Middle East eased is boosting the GBP/USD.

Ceasefire’s Impact on Forex Markets

US President Trump announced a ceasefire between Iran and Israel, creating hope for an end to their 12-day conflict. However, uncertainties about the ceasefire’s durability remain, especially regarding potential nuclear talks and the status of Iran’s enriched uranium. In his testimony, Fed Chair Powell suggested that rate cuts should be delayed until later this year. Kansas City Fed President Schmid advocates for waiting to see the economic effects of tariffs. The dovish comments from BoE officials could affect the GBP, as BoE Governor Bailey has expressed concerns over the reliability of labor data. The Pound Sterling is the UK’s official currency and plays a vital role in global foreign exchange trading. The BoE’s monetary policy, especially through interest rate changes, significantly influences its value, particularly in managing inflation. Economic indicators like GDP, PMI, and trade balances also affect the strength of Sterling. The GBP/USD pair has sustained its upward movement and is nearing levels not seen since early 2022. This rally coincides with improved global risk appetite, shifting flows away from safe-haven currencies like the US dollar. The fragile ceasefire in the Middle East serves as temporary relief for global markets, giving the Sterling more space to rise.Monetary Policies and Market Reactions

While US officials claim that military tensions have eased, there is still low confidence in the ceasefire’s stability. As we watch for the potential restart of nuclear negotiations and their implications, any setback could reverse the current favorable mood and bring demand back to the dollar. Until then, lighter trading volumes are likely to favor risk-oriented currency pairs. On the monetary policy front, Powell’s comments emphasized patience. He noted that inflation remains stubborn and the US job market has been stronger for longer than expected. His remarks suggest that interest rate cuts are unlikely in the near term, pushing expectations for the first cut potentially toward late 2024. Schmid supported this view by noting that new tariffs could change growth and inflation dynamics in ways that will take time to reflect in the data. This indicates a reluctance to make premature cuts to monetary policy. In contrast, the Bank of England has a different outlook. Bailey’s concerns about the inconsistencies in labor market data raise worries about ongoing wage pressures. Without clear employment trends, policymakers may feel limited. If revisions show weaker job growth, it could point toward earlier rate cuts in the UK. Recent communications from BoE officials have leaned toward caution, reflecting discomfort with maintaining tight policies amid uncertainties about economic slack. In the coming weeks, we will closely monitor the UK’s GDP figures and upcoming PMI surveys. Any signs of weakness may reinforce dovish expectations and limit the Pound’s gains, even if the dollar remains weak. In the US, inflation data and employment reports will be scrutinized for signs of slowing, which could lead markets to adjust their timelines for Fed easing. Markets are currently testing assumptions around central bank reactions daily. We expect increased sensitivity to speeches and unexpected data. The widening gap between Fed and BoE rate trajectories could lead to more volatility, especially if geopolitical risks resurface. For instance, Victoria at the BoE earlier stressed the importance of looking past one-off price shocks, showing their tendency to under-react. This stance contrasts with US officials, who are currently less flexible. From a trading perspective, market positioning appears skewed toward expectations of slower US rate cuts, but this could change rapidly. For now, the Pound remains strong, but this depends on ongoing optimism that attracts capital to risk trades. With market pricing potentially shifting quickly due to unexpected data, we should be prepared for changes. Create your live VT Markets account and start trading now.Members voice concerns about tariffs, wages, inflation, and economic stagnation at recent meeting

During the June meeting, participants shared different views on Japan’s economic situation, especially regarding the impact of U.S. tariffs. Concerns were raised about how these tariffs could affect business confidence and the overall economy. Despite these worries, many companies are likely to continue tackling labor shortages and making investments.

The Japanese economy is at a critical point, balancing between growth fueled by wages and investments or falling into stagflation. Alongside tariff worries, there are also concerns about domestic wage growth and a slightly higher-than-expected consumer price index (CPI). Rice prices have emerged as a significant factor influencing inflation expectations.

Global Economic Policies

Global economic policies and their effects on Japan were discussed, highlighting potential inflationary pressures. Several members emphasized the need to keep current interest rates and financial conditions stable due to ongoing uncertainties from global geopolitical issues. They noted the risk of unintended market effects from international events and rising bond market volatility. Even with inflation higher than expected, some members supported maintaining current policies due to these uncertainties. Meanwhile, the USD/JPY exchange rate remains stable. Recent discussions have clearly shown opposing forces at play domestically. On one side, businesses display a moderate resilience, particularly those focused on investment and keeping labor amid structural shortages, despite external shocks. This ongoing commitment indicates a long-term confidence in internal growth. However, these positive actions must also deal with external risks that are not temporary or minor. The stability of the dollar-to-yen exchange rate may seem reassuring, but it should not lead to complacency. It reflects investor expectations that policy changes are unlikely to happen abruptly without significant data shifts. If bond markets become more sensitive—experiencing increased volatility from abroad—the assumption of stable rates could be challenged. Any sharp reactions in rates could impact leveraged positions, especially those linked to long-term instruments, as yield predictions influence margin behaviors. Interestingly, rice prices, less discussed in Western markets, are rising enough to shape public inflation expectations, affecting future pricing behaviors. If not addressed through policy discussions or economic developments, these effects could build up, prompting yield changes in instruments that track household consumption. The latest Consumer Price Index figures support this notion, slightly ahead of consensus predictions, suggesting even well-prepared portfolios may need adjustments.Corporate Sentiment and Tariff Policies

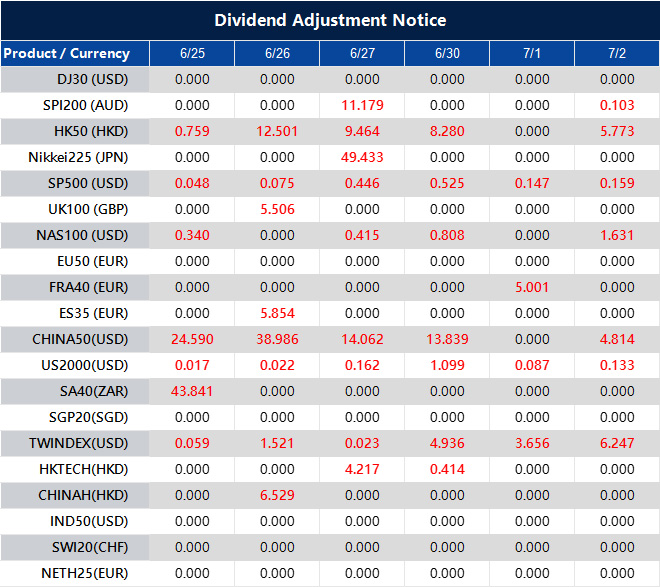

Pressure from foreign tariff policies, particularly those from Washington, is affecting corporate sentiment. While the direct impact might take time, senior management teams are adopting a cautious approach, which could influence hiring and domestic capital expenditures. Any decline in forward business confidence indicators—especially in export-sensitive sectors—should be taken into account regarding implied volatility. Wage growth remains a glimmer of hope. Sustained upward pressure could indicate wage-driven inflation instead of cost-driven inflation, changing how official releases are interpreted in the next three quarters. This could also influence implied rate volatility, especially if policymakers do not take counteractive tightening measures. Some policymakers might prefer to pause rather than act preemptively, waiting for more data before making changes. This caution is understandable given the current uncertainties, but it means there will be a heightened focus on upcoming domestic inflation and global trade data, which may broaden implied curve trades. From our perspective, a near-term shift seems unlikely unless prompted by significant external events. In the meantime, paying attention to subtle changes in yield curvature and slope steepening may prove beneficial as the market adjusts its expectations for forward guidance. Monitoring open interest in bond-related futures and options shows no sudden shifts yet, but increased activity in contracts further out may indicate greater confidence in hedging against rate surprises down the line. Therefore, closely watching how sentiment shifts regarding commodity-linked inflation, currency alignment with rate policies, and relative differences between Japan and its main trading partners could provide clearer entry and exit points. With market pricing very finely balanced, minor disturbances—whether from geopolitical changes or short-term data fluctuations—could lead to temporary but significant disruptions. Create your live VT Markets account and start trading now.Dividend Adjustment Notice – Jun 25 ,2025

Dear Client,

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

Japan’s services producer price index rises 3.3% annually, exceeding expectations of 3.1%

The Bank of Japan released its Services Producer Price Index (PPI) for May 2025, showing a 3.3% increase compared to last year.

This rise exceeded the expected 3.1% and was higher than last month’s figure of 3.1%. This data offers a glimpse into price changes in Japan’s service sector.

The new Services PPI is higher than both forecasts and the previous month, indicating continued cost pressures in the service industry. This steady 3.3% rise suggests a real trend rather than a mere fluctuation. It shows that businesses are regularly passing increased costs to consumers.

As a result, those watching monetary policy may reconsider how the Bank of Japan operates. The central bank has been cautious, but stronger inflation data—especially from non-traded sectors—might affect how soon rate adjustments happen. Ueda, the head of the BoJ, may face fewer obstacles in signaling restraint or even tightening measures. A change in tone may be on the way as the yen remains weak, leading to higher imported costs.

From a volatility perspective, the services inflation data suggests increased movement in yen interest rates, especially at the short end. Interest may rise for upcoming policy meetings. Those holding short-duration positions may need to reevaluate if current pricing does not reflect a more hawkish stance.

What matters now is the trend, not just the current level. The rise from April confirms that this is a widespread movement, not limited to a few categories. Areas like transport, professional services, and real estate are contributing to the overall index increase. This type of inflation tends to persist and will warrant closer attention.

This trend will likely impact future GDP deflators, supporting expectations for rate hikes. We’ve seen similar patterns in other advanced economies, where services inflation gradually builds before contributing to overall price increases. Short gamma positions on Japanese rates may feel pressure because of this context.

There will also be effects on forward guidance assumptions. Traders dealing in long-dated options will factor in higher implied policy variations—not just this month, but into the third quarter and beyond. If the sector continues to perform well and domestic demand remains strong, this case will only strengthen.

The recent data delivers a clear message: price increases are not limited or temporary. This opens the door for clearer communication from policymakers. Delta hedgers and those using calendar spreads on the JPY curve may find more benefit in using flatter structures, particularly as volatility becomes less directional and more based on mean reversion.

We have adjusted our short-term exposures accordingly. Outside Japan, investors might reassess carry trades involving the yen, as rate differences adjust to stronger domestic factors. This is especially true for leveraged positions in Asia-Pacific cross-currency pairs.

Monitoring the upcoming Tankan and BoJ summaries will now be routine. However, the key question is whether the momentum in services inflation continues into summer. If it does, delta positioning may not be enough—vega exposure could be a more critical factor in profitability in less actively traded markets.

During the World Economic Forum in Tianjin, Premier Li Qiang discusses China’s economic recovery.

China’s Premier Li Qiang announced at the World Economic Forum that the country’s economy has improved steadily in the second quarter. He shared his vision for China to transition from a major manufacturing hub to a large consumer market that welcomes global business investment.

The Premier highlighted the importance of sharing original technologies and innovative ideas while encouraging collaboration that avoids politicizing economic matters. He opposed economic decoupling and urged a focus on long-term goals and technological progress.

Factors Affecting the Australian Dollar

Following these remarks, the Australian Dollar (AUD) held steady around 0.6500. Key factors influencing the AUD include interest rates set by the Reserve Bank of Australia (RBA), iron ore prices, and the health of China’s economy, Australia’s largest trading partner. Typically, higher interest rates and a strong Chinese economy support the AUD, whereas lower interest rates or a weakening Chinese economy can have the opposite effect. As iron ore is a major export for Australia, primarily to China, its price is crucial; higher prices generally boost the AUD. A favorable Trade Balance, where exports exceed imports, strengthens the AUD, indicating higher demand for Australian goods. The document advises conducting thorough research before making any financial decisions due to the inherent risks and uncertainties. Now that Beijing is focusing on its consumer ambitions, traders may need to adjust their usual assumptions. Li’s remarks suggest a deliberate push towards boosting internal consumption, which could lead to changes in trade flows and foreign investment. If this shift is reflected in policy actions or updated consumer data, we may see increased volatility in Asia-Pacific FX pairs, especially those connected to commodity exports.Shifts in Demand and Internal Rates Expectations

Our attention now turns to how quickly domestic demand in China reflects these policy intentions. If signs show an increase in consumer spending alongside industrial output, expectations for raw material demand—especially iron ore—might change. This could strengthen the AUD, but any movement should be supported by more than just speculation. Monitoring China’s import data and fixed asset investment in the coming cycles will be crucial. On interest rates, remember that the Reserve Bank’s current approach is more reactive than predictive. This makes short-term rate expectations a critical factor. If wage growth or services inflation unexpectedly rise, it could lead to more tightening, putting upward pressure on the currency. Conversely, if local data shows weakness or consumer confidence doesn’t recover, the RBA might hold or reduce rates, putting downward pressure on the spot rate. Traders should pay close attention to macroeconomic data from both Australia and China, especially housing starts, retail sales, and industrial production. Since iron ore prices signal the health of trade, changes in inventories and congestion at key Chinese ports could provide early insights. Observing shipping indexes could also be valuable. The overall message is to stay alert to changes in external demand and interest rate expectations. Iron ore futures often influence the AUD, but this impact relies on the alignment of trade data. This intersection is where opportunities or risks become more evident. We’re also monitoring trade balances closely. Although recent surpluses are encouraging, shifts in global growth could quickly change the outlook. A sustained decline in Chinese manufacturing could hurt Australia’s export earnings, thus weakening currency support driven by trade. Tracking the 20-day moving average against actual performance may help identify emerging trends. As Li promotes a more integrated and engaged economic strategy, markets will focus on outcomes, not just promises. For now, preparing ahead of data releases while keeping an eye on iron ore and sectors sensitive to China will be more critical than general sentiment. What truly matters is the actual consumption and industrial demand as we head into the second half of the year. Create your live VT Markets account and start trading now.The UK job market is experiencing slow growth, with wage increases falling behind inflation and a decrease in job vacancies.

Recent surveys from Brightmine and Indeed show a slowdown in the UK job market. The UK is currently the only major economy with job openings below pre-pandemic levels.

In the private sector, pay raises mostly averaged 3% in the three months leading to May. This is below the 3.4% inflation rate. About 15% of firms offered smaller raises of 2.5%, indicating caution from employers.

Job Vacancies and Graduate-Level Positions

Job vacancies in the UK dropped by 5% from late March to mid-June and are now 21% lower than before COVID-19. The number of graduate-level job ads has reached its lowest since at least 2018, with significant declines in HR, accounting, and marketing sectors. The demand for some roles may be decreasing, partly due to the impact of AI. Despite worries over rising social security costs, there are no signs of a significant drop in employment. This article describes the ongoing softness in the UK job market, with various signs of reduced hiring in white-collar jobs. Data from Brightmine and Indeed shows the UK’s decline is more pronounced compared to other developed economies. While job postings have slowed globally, the UK stands out as the only major market where vacancies have fallen below pre-pandemic levels, indicating weaker demand across various industries. In the private sector, pay raises have largely stalled at 3% through May. Since this is below inflation, real earnings are effectively decreasing. About 15% of firms even provided smaller raises of 2.5%, suggesting employers are tightening their budgets, which may signal a broader trend rather than just cautiousness.Employment Trends and Future Outlook

Vacancies decreased by 5% from late March to mid-June, now sitting 21% below pre-COVID levels. This represents a notable gap, especially in industries that offer many entry-level professional jobs. Graduate job listings have dropped to their weakest point since at least 2018, particularly in human resources, accounting, and marketing—fields at high risk for automation. Artificial intelligence may be influencing these hiring trends, reducing the need for certain job functions, especially where decisions can be automated. Despite concerns about rising labor costs, including higher National Insurance contributions, there are currently no signs of significant job losses. Companies seem to be choosing not to hire more staff. For those trading in volatile markets or betting on changes in rates and inflation expectations, the message is clear: pay close attention to future employment data, especially at the sector level, since overall figures may overlook significant contractions. Market trends regarding interest rate changes in the coming months will closely follow new developments in wage growth or hiring. From a technical standpoint, the decline in vacancies and slowing wage growth suggests a downward pressure on short-term inflation figures, potentially leading to mild disinflation in the second half of the year. We should keep an eye on how wage data impacts unit labor costs in Q3. If wage growth remains weak, inflation swaps might start falling short of short-term CPI forecasts, allowing for favorable steepening positions under the right circumstances. The forward curve seems to underestimate the impact of lower job openings if this trend continues over the summer. Any future hawkish statements will need to be viewed within this context. In particular, shorter-term rate volatility may present unique opportunities as wage data is assessed. Stay tuned to sector-specific indicators, such as the ONS Vacancy Survey by industry and real-time private job board postings. These timely releases may signal upcoming changes in official data. We will continue to monitor movements in job-sensitive assets and trade accordingly. Create your live VT Markets account and start trading now.The Swiss Franc strengthens against the US Dollar as geopolitical tensions ease following a ceasefire.

The Swiss Franc has gained strength against the US Dollar, trading close to multi-year lows in the USD/CHF pair. This shift is driven by safe-haven flows and a weaker US Dollar. Recently, a fragile ceasefire between Iran and Israel has eased geopolitical tensions, even as both countries remain suspicious and accuse each other of ceasefire violations.

**Economic Context**

Currently, the USD/CHF is just above its 2011 low, around 0.8052 during US trading hours. The Swiss National Bank (SNB) has maintained a zero-rate policy, which has not stopped the Franc from gaining strength. This is despite the SNB’s efforts to fight deflation risks with its sixth consecutive rate cut.

Federal Reserve Chair Jerome Powell highlighted the cautious approach of US monetary policy, suggesting a possible rate cut in July if inflation improves. Vice Chair Michelle Bowman and Governor Christopher Waller indicated a similar dovish stance, recognizing progress in inflation while hinting at potential policy changes.

Switzerland’s economy is the ninth-largest in Europe, known for its strong services sector and close trade ties with the EU. Economically stable conditions generally support the Swiss Franc, though its responses to commodity prices like Gold and Oil are limited.

Even with a conservative rate policy from the SNB, the Franc continues to rise. This isn’t solely due to domestic strength; it reflects external weaknesses and global caution. The USD/CHF pair around 0.8050 shows how strong the demand for safe-haven currencies remains when geopolitical risks are present. The ongoing fragility of the Iran-Israel truce makes investors reluctant to shift toward riskier currencies while the situation is unstable.

Powell’s measured comments reveal that the Federal Reserve is closely monitoring price data but remains skeptical that inflation is back on track. Waller and Bowman shared similar views, recognizing improvements while not committing fully to changes. This indicates that the Federal Reserve is maintaining its flexibility. Though the July meeting isn’t guaranteed, a rate cut could become likely if consumer prices stabilize. Traders should remember that future easing hints are conditional, which is important for managing expectations around interest rates.

**Swiss Franc Resilience**

The SNB’s ongoing rate cuts—now at six—have surprisingly not weakened the Franc. Typically, such actions from a central bank would decrease demand for its currency, but the opposite is happening here. Why? Investors prefer currencies linked to economies with stable politics, low debt, and predictable prices, which describes Switzerland well.

Switzerland’s strong ties to the EU help buffer it from economic isolation, while its minimal reliance on volatile commodities adds extra stability. This predictability is appealing to traders. With the Franc nearing record highs and the Dollar facing downward pressure from potential Fed adjustments, traders should consider short-term options and futures with respect to this momentum—neither chasing after it nor countering it.

As we look at short-term contracts into early Q3, it’s reasonable to view the Franc as resilient rather than overbought. For the Dollar to recover, it needs to see not only surprises in CPI data but also alignment between real wage growth and employment statistics with the Fed’s soft stance. It’s crucial to monitor how these factors interact before adjusting expectations for September or later.

Currently, maintaining defensive strategies regarding USD exposure is wise. Momentum signals suggest a continuation trend rather than reversal for now. It’s also important to watch for any changes in guidance from the ECB or BOE, as shifts in Europe can impact USD/CHF through the Euro channel. While coordinated moves may be rare, overall sentiment often overlaps.

Volatility pricing appears disconnected from actual movements, particularly in short-term USD/CHF options. This mismatch might quickly align if new geopolitical tensions arise or if FOMC minutes provide clearer direction. Rolling hedges can offer cost savings and flexibility during uncertain weeks, especially near multi-year extremes.

At this moment, both charts and macro signals present a clear picture. A structured exposure approach, paired with adaptable hedging, will likely yield better results than trying to guess bottoms in the Dollar. This is an important time to observe rather than rush.

Create your live VT Markets account and start trading now.