The Nasdaq shows tight trading around VWAP, suggesting indecision and offering cautious bullish and bearish strategies.

Nasdaq Futures are currently at $21,748, close to today’s VWAP, which shows a narrow trading range continuing from yesterday. The doji-like pattern indicates indecision in the market, with limited price movement suggesting little confidence in making big changes.

A cautiously bullish outlook exists above $21,750, near the VWAP. Trading at this level has the potential for better rewards versus risks, although it comes with some uncertainty due to tighter stop placements. The Volume Profile highlights where the most trading activity occurs, with these high-volume areas providing strong support and resistance.

The Asian market stays quiet, awaiting ECB decisions, even as China’s Services PMI shows growth

During the Asian trading session on Thursday, June 5, 2025, major currencies showed little movement. There was not much news, with attention mainly on Japan’s wage data and the Caixin Services PMI from China.

In Japan, wages rose year-on-year in April, marking the fastest growth in four months. However, inflation continued to impact household purchasing power, causing real wages to drop for the fourth month in a row. This situation creates challenges for the Bank of Japan concerning its monetary policy adjustments.

In China, the Caixin/S&P Global Services PMI for May increased to 51.1 from April’s 50.7, indicating 29 months of ongoing growth since January 2023. This figure slightly surpassed expectations set at 51.0, boosted by stronger domestic demand and improved business confidence. However, foreign demand contracted for the first time this year. The Composite PMI fell to 49.6, the lowest since December 2022, primarily due to weak manufacturing data.

The FX market remained calm as traders awaited the European Central Bank’s decision, with a 25 basis point rate cut expected. The ECB decision is set for 12:15 GMT / 8:15 AM US Eastern Time, followed by a press conference with Lagarde.

Most Asian currencies stayed stable, making Thursday feel more like a waiting room than a trading day. Traders focused on news from Tokyo and Beijing. In Japan, while the rise in base wages might seem promising, inflation tells a different story. Real household buying power has dropped for four months, erasing any wage growth. Monetary policy struggles to address daily living costs that keep rising.

In China, the situation is mixed. The service sector continued its growth, extending a two-and-a-half-year streak. While the data slightly beat expectations, it wasn’t remarkable. The domestic economy showed some strength, likely due to internal demand and a small boost in business confidence. However, the decline in foreign demand is concerning, marking the first downturn in overseas services since December. Additionally, the overall composite PMI dropped below 50 due to weak factory output, indicating one part of the economy is improving while another lags.

Most attention was on Frankfurt, where the ECB’s anticipated rate cut was expected. The market was ready for this move. What remains unclear is Lagarde’s tone during the press conference. If she delivers anything unexpected, volatility could increase. Historically, the euro tends to remain stable post-decision, only reacting during press conferences as interpretations come into play.

The key takeaway is that major central banks are implementing different monetary policies, impacting relative yields—especially in Europe and Asia. Japan is cautious. China is selective. Europe aims to ease. Harmony is no longer expected. Yield differences are now more influenced by future guidance than traditional factors like inflation or employment goals. This shifts how traders should position themselves.

Additionally, implied volatility in short-term rates might become more responsive rather than indicative. Traders face risks when central bank narratives aren’t aligned. They must now consider not only data releases but also how the market reacts to central bank statements—making the trading landscape feel less predictable.

In the upcoming weeks, a more cautious approach is advisable. Traders should monitor changes in cross-currency swaps, particularly involving euro and yen pairs, as widening differentials may indicate shifts in funding preferences and interest rate spreads. These changes will directly affect forward pricing and volatility.

Lagarde’s message on Thursday afternoon may be reasonable, but the reaction in rates and the FX market will hinge on her ability to balance incoming data with future policy paths. Her wording must be clear to avoid unsettling the markets. That pressure shifts to traders using margin through options and futures linked to monetary signals. Timing—even by just a few hours—becomes crucial.

Kugler and Harker will speak about economic matters and policies at upcoming events.

Federal Reserve Board Governor Adriana Kugler will speak about the economic outlook and monetary policy. Her speech is scheduled for 16:00 GMT / 12:00 US Eastern Time during a luncheon hosted by the Economic Club of New York.

At the same event, Federal Reserve Bank of Kansas City President Jeffrey Schmid will address banking policy. His speech is set for 17:30 GMT / 13:30 US Eastern Time during a conference called “The Future of Banking: Navigating Change,” organized by the Federal Reserve Bank of Kansas City.

Also at this time, Federal Reserve Bank of Philadelphia President Patrick Harker will talk about the economic outlook. His presentation is at 17:30 GMT / 13:30 US Eastern Time for the Philadelphia Council for Business Economics in Philadelphia, Pennsylvania.

Federal Reserve Speeches Impact

The speeches from Kugler, Schmid, and Harker will shed light on the Federal Reserve’s views on monetary policy, regulation, and banking conditions. Kugler’s comments are important as they will be delivered at a luncheon with many market participants. She is likely to discuss interest rates, inflation trends, the strength of the job market, and the impacts of previous tightening measures. These topics can significantly affect short-term trading, especially on interest rate expectations. Therefore, any changes in tone or references to timing for policy adjustments must be closely monitored. Schmid will focus more on banking issues than on interest rates. His thoughts on regional banks’ strength and the regulatory environment may influence views on financial stability. If he highlights concerns about funding stress or risks from deposit withdrawals amid rising rates, it will likely attract attention to the Fed’s focus on the broader effects of tighter policy. Any mention of contingency plans or changes in supervision could trigger volatility in bank-related financial products. Harker’s comments may echo Kugler’s themes but usually feature more anecdotal evidence. Markets are attentive to his insights on regional economies, including spending habits, service sectors, and employment patterns. If Harker emphasizes a “higher-for-longer” approach—especially with mentions of wage persistence or inflation in housing—it could lead to fewer expected rate cuts than futures currently predict. Recent market responses to Fed officials with voting power indicate that SOFR and Treasury option markets have reacted swiftly following similar speeches. Although volatility has decreased, it can quickly change based on the tone and wording of policymakers.Market Reaction Strategy

With all three speeches timed closely together, it makes sense to stay flexible with interest rate positioning this afternoon. While one comment may not change the market significantly, the combined messages over a short time can influence expectations for rate cuts, especially in light of Tuesday’s CPI data and recent jobless claims. Our strategy suggests maintaining a neutral stance and being cautious ahead of these speeches. Be ready to quickly adapt if the remarks lean more hawkish or dovish; even slight changes in language can impact the market when all three officials speak nearly at once. Create your live VT Markets account and start trading now.PBOC may cut RRR to support liquidity in 2025, according to a state media report.

The People’s Bank of China (PBOC) may take further action in late 2025, like lowering the reserve requirement ratio (RRR), if needed. This move aims to keep long-term liquidity steady and ensure there’s enough money in the market during mid and late 2025. The goal is to create a supportive monetary environment for economic recovery.

Recently, the PBOC injected about RMB1 trillion into the market by cutting the RRR. The RRR is the amount of money that banks must hold in reserve against customer deposits. The PBOC controls this ratio to impact how much banks can lend. Increasing the RRR reduces the money supply because banks must hold more funds in reserve, while lowering it allows banks to lend more, boosting the money supply and encouraging economic activity.

By cutting the reserve requirement, the central bank has opened up more lending capacity in the system. This means banks can use the extra capital to lend more money, which helps circulate funds in the Chinese economy. This method doesn’t directly inject cash but makes credit more available without large fiscal measures.

This policy often indicates an intention to influence overall market sentiment. Loosening reserve levels typically responds to signs of weaker growth or internal imbalances that need minor adjustments rather than major reforms. The timing suggests a desire to improve liquidity conditions before any potential stress later in the year. The idea is to prevent a tightening of credit markets by giving banks more flexibility now instead of waiting for issues to arise.

For those of us following derivatives, these signals are significant. When central banks lower reserve requirements, bond yields may see slight downward pressure. Forward rates, especially in yuan-based interest rate futures, might start to expect lower borrowing costs. Currently, volatility remains relatively stable in short-term contracts, but there’s increasing asymmetry in longer-term contracts.

Zhou’s earlier statements about maintaining “reasonably ample” liquidity show a careful approach. There’s no rush to flood the markets; the goal is simply to support the financial system where it’s needed. This strategy encourages us to reconsider short volatility positions, especially in long-term interest rate options. We’ve noticed growing directional bias since the start of the quarter.

Looking ahead, those modeling liquidity metrics should also pay attention to potential phantom tightening. This is when liquidity seems stable on the surface, but interbank lending and repo market signals are weakening. We’ve seen this before, especially when mild easing hides deeper structural issues. Over-hedging against immediate rate cuts may be ineffective, but creating layered protection against shifts in the slope appears wiser.

Lastly, the significant RMB1 trillion injection has a psychological impact on traders. It signals a readiness to take substantial action again, which helps shape policy expectations and lessens the unpredictability of short-term rates. However, it’s less clear how much this will translate into private credit extensions or affect risk sentiment.

We’re already observing the impact in local funding curves. As the gap narrows between state and commercial lenders, correlations of volatility across different assets are decreasing. This is a slightly positive sign for carry strategies, although it’s essential to monitor duration exposure closely.

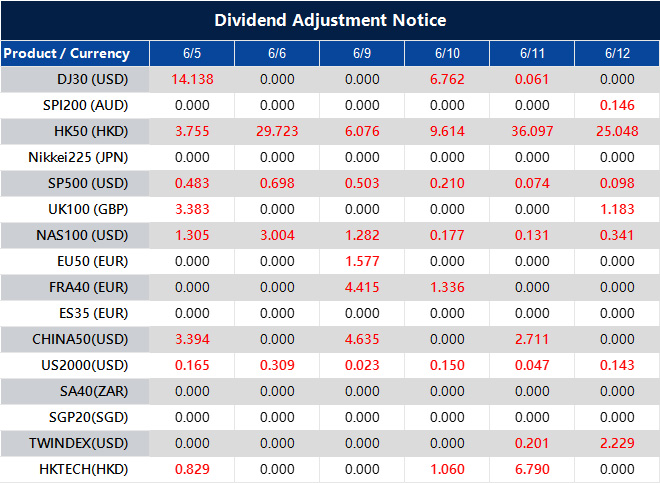

Dividend Adjustment Notice – Jun 05 ,2025

Dear Client,

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

China’s services sector improves in May, but foreign demand contracts for the first time this year

China’s Caixin/S&P PMI for May 2025 reported a services score of 51.1, slightly above the expected 51.0 and last month’s 50.7. This indicates a rise in overall demand and business confidence.

However, foreign demand shrank for the first time this year. New export business saw a small decline, the first since December. The job market showed a slight improvement, breaking a two-month downturn and reaching a six-month high.

Input costs rose at the fastest rate in seven months, mainly due to increasing purchase prices and labor expenses. Despite this, prices charged to customers dropped for the fourth month in a row.

The composite index fell to 49.6, driven by a lower manufacturing PMI of 48.3, down from the previous 50.4. This composite figure is the lowest since December 2022, compared to the earlier score of 51.1.

The latest data presents a mixed picture of economic activity. Some service-related indicators show growth, while broader measures are starting to decline. The services PMI of 51.1 indicates mild growth—not remarkable, but still a positive trend after the previous month’s reading of 50.7. This increase suggests more business activity and a slightly better outlook among service firms.

However, the decline in new export orders raises concerns. This slip in external demand—especially after steady growth this year—could signal challenges in global demand, hinting that the external sector may not be as strong as domestic activity right now. Notably, this marks the first decline in new foreign business since December, suggesting a shift in trends rather than just a single drop.

The labor market seems to be stabilizing. A small increase in employment, after two months of job losses, indicates that employers are slowly regaining confidence and may be preparing for anticipated demand, even if current figures don’t warrant major hiring. We’re also seeing the highest employment growth in six months, albeit slight, suggesting hiring managers expect demand to hold up in the near future.

Cost pressures are building. Input costs surged at their fastest rate in seven months due to higher raw material and wage costs. This situation is uncomfortable, especially since prices charged to customers continue to fall for the fourth consecutive month. The gap between rising input costs and declining output prices could eventually force businesses to respond.

When we combine the numbers in the composite PMI, we see a sharp decline to 49.6. This is below the neutral mark of 50, indicating a slowdown in overall activity. It’s the lowest score since December 2022. While this doesn’t mean services are contracting, the significant drop in the manufacturing PMI to 48.3 from 50.4 is noteworthy. This decline shows a retreat in factory activity, which raises caution, especially as it reflects weaknesses in new orders and production.

In the upcoming weeks, it will be important to monitor the disparity between the resilient service sector and the declining manufacturing sector. We are entering a phase of tightening margins, mixed volume signals, and waning external demand. Additionally, consumer resistance to price increases is apparent as businesses struggle to pass on higher costs. This can negatively impact business models more than the surface-level figures suggest.

In the short term, it might be prudent to look at the performance differences between service-related sectors and those reliant on international manufacturing orders. Changes in how companies handle wage pressures and pricing strategies could lead to greater fluctuations in producer margins and potentially earnings. Keeping an eye on firms facing rising costs while struggling to adjust prices is essential.

Lastly, employment data deserves attention. While it’s encouraging to see job growth, if it doesn’t lead to stronger output, it could cause inefficiencies. Employers may soon face challenges regarding productivity. If input cost pressures stay high, we might see adjustments in capital allocation, favoring automation or moving away from labor-intensive areas. This shift could impact expectations in the near future.

In April, Australia saw a 2.4% decrease in exports and a 3.7% increase in household spending.

Australia’s trade balance in April 2025 had a surplus of 5,413 million AUD. This was below the expected surplus of 6,000 million AUD and down from the previous month’s 6,900 million AUD.

Exports fell by 2.4% compared to the previous month, following a significant 7.6% increase in March. Meanwhile, imports grew by 1.1%, bouncing back from a 2.2% decline earlier.

Trade Impacts

In March, exports surged ahead of new tariffs, but April saw a decline—particularly in gold exports, which had previously hit record highs. Household spending in April rose by 3.7% from the same month last year, slightly exceeding the expected 3.6% and the previous year’s 3.5%. On a monthly basis, spending increased by 0.1%, reversing a slight decline from the previous month. Overall, Australia’s trade surplus narrowed in April. The surplus of AUD 5.41 billion fell short of market expectations and decreased from March. Exports dropped by 2.4% after a significant increase the previous month, while imports rose by 1.1% after a prior decrease. Gold exports, which spiked due to the anticipation of tariffs, were a key factor in this decline. Household consumption showed a small positive surprise, slightly stronger than expected. While the monthly gains were modest, they indicated a revival from a flat March.Future Market Considerations

Currently, there is a subtle shift in the market. Capital flows are still happening but lack the urgency seen before March. Some of the export drop is due to changes in delivery patterns caused by the recent tariffs. This volatility might be front-loaded and could stabilize. For short-term contracts related to commodities and Australian rates, it’s essential to consider the recent import increase. Is this due to actual consumer demand or early signs of restocking? The annual rise in consumer spending shows resilience in domestic demand, though it hasn’t yet boosted retail inventories significantly. If the trade terms continue to soften while consumption remains steady, inflation pressures may ease. It’s important to keep an eye on iron ore and LNG, as their impact on revenue is much larger than the recent drop in gold. If these prices decrease and do not see any replacements, expectations for improvements in the current account may need to be reassessed. When tracking shorter-term currency exposures sensitive to exports, we need to consider how these trade changes may gradually influence the AUD over time. There is a noticeable reduction in risk-reversal pricing, indicating that traders may be adjusting their bullish currency positions due to a diminished yield advantage. Market placement should also take into account that while household spending showed a slight uptick, there hasn’t been a significant shift that would prompt a stronger response from the central bank. The policy outlook remains cautious, influencing front-end and volatility exposures. In the upcoming week, forecasts on energy exports and industrial input volumes might hold more weight than general consumption data. This is especially true if China’s trade patterns remain uncertain, as minor adjustments in forward hedges could minimize short-term losses associated with optimistic commodity placements. We will continue to observe option skews around the 3-month mark for hints on forward hedging against potential AUD shifts. If pricing trends continue leftward, it could suggest that the market is less worried about immediate inflation but more cautious about growth concerns linked to trade. Create your live VT Markets account and start trading now.US auto suppliers group calls for urgent action on China’s rare earth export restrictions

A U.S. auto supplier group has raised alarms about China’s limits on rare earth and critical mineral exports. According to the Vehicle Suppliers Association (MEMA), parts manufacturers are facing “serious, real-time risks” to their supply chains.

The association stressed that the problem is ongoing, with worries about potential disruptions growing. They are calling for “immediate and decisive action” to prevent major disruption and economic fallout in the vehicle supply sector.

U.S.-based manufacturers pointed out that restrictions from Beijing on key materials used in magnets and batteries are starting to affect operations. These materials—rare earth elements and critical minerals—are hard to replace, and their production is largely concentrated in a few countries, with China being the main player. When these materials are slowed or stopped, the effects are felt quickly, especially for those managing supply timelines that are already under strain.

The association’s warning is clear. They are not speculating; real challenges are hitting manufacturing pipelines now. China’s export controls have not only been put in place but are also being updated and tightened, leading to delays and increasing uncertainty. For businesses that depend on precise materials—needed for cooling systems, electric powertrains, microelectronics, and more—time is running out.

This isn’t just a theoretical concern about geopolitical risk. The bottlenecks they mention, especially with materials like graphite, dysprosium, and neodymium, impact everything from brake systems to motor coils. What was once a predictable supply chain is now unpredictable, raising concerns not just about costs but also about the availability of these materials.

In earlier quarters, companies coped by relying on inventories and alternative contracts, extending agreements when necessary. However, this strategy can’t last forever. Now, as procurement teams receive updated supplier information, a clear shift is happening from manageable issues to disruptive ones.

The association’s message emphasizes the need for action, not just awareness. They urge that commercial interests and coordinated sourcing strategies be prioritized immediately. They seek urgent measures to prevent delays before they affect multiple production levels.

This is crucial: delays in sourcing minerals will influence vehicle production within weeks, not months. Suppliers in the middle of the supply chain often have the least financial or operational backup. If they miss a week’s delivery due to delays in shipments of magnet-grade samarium, that loss can’t be made up with extra hours.

For traders engaged in contracts during this volatility, we must think about how changes in nickel and rare earth pricing will affect asset values. Price shifts rarely happen in isolation. Recent trends show that tighter inventories lead to spikes in futures, indicating a connection between metal futures and options premiums tied to production indices.

A reactive strategy won’t work as logistics warnings grow. We’ve seen past issues with palladium and cobalt constraints, leading not just to speculation but also to shifts in volatility and rapid price changes in components crucial for automation, electric infrastructure, and battery capacity.

The key takeaway lies not in policy but in strategic positioning. If forward contracts lack flexibility or offset clauses, margins will be tested. For those of us trading metals related to powertrains or precision electronics, it’s time to reassess those strategies.

History shows that during times of shortage, such as the semiconductor crisis, derivatives often lead price movements rather than follow them. If we misread the current situation, it could echo those past cycles. With materials affecting broader manufacturing sectors, the consequences may be even louder.

Ukraine and the US plan to create a joint minerals fund, with a board meeting anticipated.

Ukraine and the United States plan to create a joint minerals fund by the end of the year, with the first board meeting expected in July. Yulia Svyrydenko, Ukraine’s First Deputy Prime Minister, announced this during her visit to Washington.

Svyrydenko met with U.S. Treasury Secretary Scott Bessent and the U.S. Development Finance Corporation to discuss the next steps. They talked about seed capital and a long-term investment strategy for the fund.

The fund comes from a minerals development agreement signed in April after extensive negotiations. This agreement improved terms for Kyiv and received support from former U.S. President Trump. It was later approved by Ukraine’s parliament to strengthen economic ties.

The agreement aims to reduce tensions between Trump and Ukrainian President Volodymyr Zelenskiy, which emerged from their differing views on resolving Ukraine’s ongoing conflict with Russia.

This initiative signals a clear effort to strengthen economic connections through coordinated resource development. The mineral fund is designed to gather financial and strategic resources, marking a significant step toward long-term cooperation in a high-demand sector. Svyrydenko’s statement during this high-level fiscal discussion shows a commitment to maintaining progress.

Discussions about seed capital and investment strategies are complex. They involve multiple stages: first, financial commitments; then governance; and finally, funding actual development. With a board meeting already scheduled for July, it indicates that much groundwork has already been laid. The timeline for implementation is becoming clearer.

The minerals development agreement that initiated this process took time and negotiation. Kyiv did not simply accept the initial terms; it pushed for improvements. This reflects the high stakes involved in securing favorable conditions. For Ukraine, dealing with conflict and economic recovery, achieving better terms shows a focus on securing investment channels.

From a trading standpoint, this suggests enhanced economic stability from at least one party. A minerals sector supported by a structured fund reduces uncertainty. High-level engagement from policymakers like Bessent further underscores this ambition.

Where there have been foreign policy tensions, this agreement uses economics as a way to mend relationships. It acknowledges that conflict can strain partnerships, but the fund offers a chance to reset international cooperation. It indicates that all parties are willing to negotiate if there’s structure and potential returns involved.

In the coming weeks, we can expect news about the fund’s structure, board appointments, and resource priorities. These developments should not be viewed as isolated diplomatic actions, but rather as indicators of where capital may flow next. Early movement could come from companies that align with the fund’s mission, particularly those involved in extraction or logistics.

Monitoring fund composition and early policy decisions after July will be essential. Once momentum builds in these discussions, it often flows faster than anticipated. Consistent, clear signals from a multinational board will create patterns that savvy investors will track closely.

US auto supplier group stresses need for urgent action to maintain access to Chinese rare earths

The U.S. auto supplier group warns that tightening Chinese controls on rare earth exports may disrupt the automotive industry. Rare earth elements are crucial for electric motors, batteries, and advanced systems in modern vehicles.

China dominates global production and processing of these materials. Limiting exports could impact supply chains, increase costs, and delay deliveries within the automotive sector. The group stresses the need for immediate action to find alternative sources or build domestic capacity to lessen the potential economic fallout on the automotive supply chain.