Data show that gold prices in the Philippines declined, based on figures compiled from market sources and reported accordingly

Gold prices fell in the Philippines on Thursday, FXStreet data showed. Gold was priced at PHP 9,276.30 per gram, down from PHP 9,295.22 on Wednesday.

Gold slipped to PHP 108,198.50 per tola from PHP 108,417.60 a day earlier. Other listed prices were PHP 92,759.34 for 10 grams and PHP 288,523.60 per troy ounce.

In the United Arab Emirates, FXStreet-compiled data shows that gold prices declined today

Gold prices in the United Arab Emirates fell on Thursday, according to FXStreet data. Gold traded at AED 586.92 per gram, down from AED 588.60 on Wednesday.

The price per tola dropped to AED 6,846.01, from AED 6,865.30 the day before. Other listed rates were AED 5,869.45 for 10 grams and AED 18,254.09 per troy ounce.

How Local Gold Prices Are Calculated

FXStreet calculates local gold prices by converting international prices using the USD/AED exchange rate and local measurement units. Prices are updated daily at the time of publication, but local market rates may differ slightly. Gold has long been used as a store of value and a form of money. It is also widely used in jewellery. Many investors buy gold during times of market stress, high inflation, or currency weakness. Central banks hold the largest gold reserves and may buy gold to diversify their assets. According to the World Gold Council, central banks bought 1,136 tonnes of gold worth about $70 billion in 2022, the highest annual total on record. Gold often moves in the opposite direction of the US Dollar and US Treasury yields. It can also move differently from risk assets, such as stocks. Gold prices are influenced by geopolitical events, recession worries, interest rates, and the strength of the US Dollar, since gold is priced in dollars (XAU/USD).Market Outlook And Trading Considerations

Gold prices are slightly lower today, February 19, 2026. This looks like mild profit-taking, not a major shift in the broader trend. For traders, the pullback may offer a short-term entry point if they expect the uptrend to resume. This move should be seen in the context of the wider economic picture. The Federal Reserve’s interest-rate cuts through 2025 have been a key reason gold has stayed strong. With the Fed Funds rate now at 3.50%, lower rates make bonds less attractive compared with gold, which does not pay interest. This policy has also kept the US Dollar Index relatively weak, hovering near 98, which has historically supported gold. Inflation remains important. While inflation has eased, the latest CPI reading for January 2026 was still high at 2.8%, which keeps gold appealing as a hedge. Central banks also continued buying in 2025. World Gold Council data shows they added more than 1,050 tonnes to reserves last year. This steady institutional demand helps support prices. With these supportive factors in place, derivative traders may look at strategies that profit from a move higher in the coming weeks. One option is to buy call options with April or May expiries to benefit if the uptrend continues. Another approach is to sell out-of-the-money put options to earn premium, based on the view that strong demand will limit any major downside. Create your live VT Markets account and start trading now.Early European buying lifts EUR/JPY near 183.00, keeping the bullish tone intact

EUR/JPY rose to around 182.90 in early European trading on Thursday. The move came as markets priced in the ECB keeping its benchmark rate at 2.0% for the rest of this year, with possible increases next year.

Japan’s National CPI is due on Friday. Annual inflation eased to 2.1% in December 2025, the lowest level since March 2022. A stronger CPI print could lift expectations for an earlier BoJ rate hike.

Technical Outlook On The Daily Chart

On the daily chart, EUR/JPY is still trading above the rising 100-day EMA, which keeps the medium-term trend positive. The RSI is at 47.83 and would signal improving momentum if it moves above 50. Bollinger Bands are tightening, which points to lower volatility. Price is below the midline but above the lower band. Resistance sits at 183.35 and support is at 180.75. A daily close above 183.35 could open the way to 186.00, while a break below 180.75 may expose 180.68. The Yen is driven by Japan’s economic performance, BoJ policy, yield spreads versus US bonds, and overall risk sentiment. The BoJ has intervened in markets at times. Ultra-loose policy from 2013 to 2024 weakened the Yen, while a gradual policy unwind since 2024 has offered some support. With EUR/JPY near 182.90, our near-term focus is the gap between central bank expectations. The market is pricing an ECB rate of 2.0% through the year, which supports the Euro. That view was reinforced last week when Eurozone HICP inflation for January came in a touch sticky at 2.4%, which reduced hopes for early rate cuts. The main event risk is Japan’s National CPI report, due tomorrow. After inflation cooled to 2.1% in December 2025, consensus expects a small rebound to 2.2% for January. A much higher reading would likely fuel talk that the Bank of Japan could speed up policy normalization. That would support the Yen and could push this pair lower.Options Strategy Considerations

For a bullish setup, consider buying call options with strikes above the 183.35 resistance level, such as 183.50 or 184.00. If Japanese CPI is soft and price breaks above this barrier, these calls would provide leveraged exposure to a potential move toward the 186.00 target. Today’s low volatility (shown by tighter Bollinger Bands) also makes these options relatively cheaper. To hedge against, or potentially profit from, an upside surprise in Japanese inflation, consider buying put options. Our trigger would be a break below the key 100-day EMA at 180.75, so puts with a strike around 180.50 could fit. In 2024 and 2025, the JPY often rallied sharply when the BoJ even hinted at tightening, so it is important to plan for downside risk. Because tomorrow’s release could drive a large move, a volatility strategy may also make sense. One approach is a long straddle: buy both a call and a put with the same strike price and expiration. This benefits from a big move in either direction and can work well when volatility is low ahead of a major catalyst. Create your live VT Markets account and start trading now.In Pakistan, gold prices declined on Thursday, according to compiled data

Gold prices in Pakistan fell on Thursday, according to data compiled by FXStreet. Gold was priced at PKR 44,813.80 per gram, down from PKR 44,948.43 on Wednesday.

The price per tola fell to PKR 522,715.80 from PKR 524,269.60 the previous day. Other listed prices were PKR 448,151.10 for 10 grams and PKR 1,393,866.00 per troy ounce.

How Local Gold Prices Are Calculated

FXStreet calculates local gold prices by converting international prices using the USD/PKR exchange rate and local units. Prices are updated daily using market rates at the time of publication, so local prices may vary slightly. Central banks hold more gold than any other group. According to the World Gold Council, they added 1,136 tonnes (worth about $70 billion) in 2022. This was the largest yearly total since records began. Gold often moves in the opposite direction of the US Dollar and US Treasuries. It can also move against risk assets like stocks. Key drivers include geopolitical tension, recession concerns, interest rates, and shifts in the US Dollar, since gold is priced in USD (XAU/USD). Local prices are only slightly lower, but the bigger story for derivatives depends on global forces. Gold’s inverse link with the US Dollar matters most. With the Dollar Index (DXY) down nearly 4% since last autumn to around 101.5, gold has a stronger base of support. This is an important trend to watch in the weeks ahead.Interest Rates And Derivatives Outlook

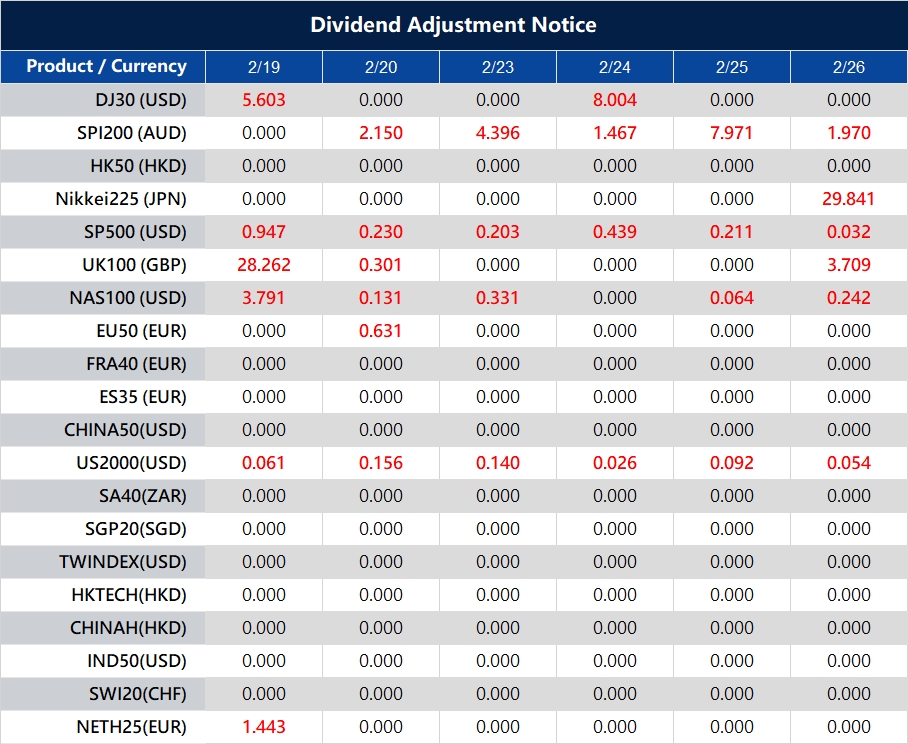

Interest rate expectations are the main driver of gold. The sharp rate hikes of 2023 and 2024 are now in the past. Markets are pricing in possible US Federal Reserve rate cuts later this year. The cooler-than-expected January 2026 inflation reading of 2.8% supports that view, and it often helps non-yielding assets like gold. Steady demand from central banks also matters. After record buying in 2022, central banks added another 1,050 tonnes to reserves through 2025. This ongoing official buying helps support prices and can limit how far gold falls. Gold’s safe-haven role is becoming important again. After a strong run for much of last year, stock markets are showing more volatility, and company guidance for the next quarter is mixed. This uncertainty may lead some traders to add gold derivatives as a hedge. Geopolitical tensions and trade disputes also continue to support gold. When these risks rise, investors often move to safer assets. Because of this, sharp price drops may offer chances to position for higher volatility. Create your live VT Markets account and start trading now.Dividend Adjustment Notice – Feb 19 ,2026

Dear Client,

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

Sterling stays below 1.3500 against the dollar, hovering near four-week lows amid expectations of a BoE rate cut

GBP/USD steadied after three straight days of losses this week. It traded in a narrow range near a four-week low during Thursday’s Asian session. The pair was just below 1.3500 and still looked vulnerable to further downside.

Sterling weakened as markets raised the odds of a Bank of England rate cut at the March meeting. This came after a soft UK jobs report and a fall in UK consumer inflation to its lowest level in almost a year.

Dollar Strength And Policy Divergence

A stronger US Dollar added pressure. Support came from the Federal Reserve’s January meeting minutes, released on Wednesday. Policymakers were divided on whether more rate cuts were needed and when they should happen. They weighed stubborn inflation against the 2% target. Geopolitical risk also stayed high after reports that the US military could strike Iran as soon as this weekend. This helped boost demand for the US Dollar and kept GBP/USD tilted lower, with any bounce seen as limited. Traders watched Thursday’s US data, including Weekly Initial Jobless Claims, the Philly Fed Manufacturing Index, and Pending Home Sales. Markets also looked to speeches from FOMC members and Friday’s US PCE Price Index for clearer direction. At this time last year, markets were already positioning for the Bank of England to cut rates in March 2025. That pushed GBP/USD down toward 1.3500. The outlook was driven by weaker UK jobs data and inflation falling to its lowest level in nearly a year. It set the tone for a longer period of sterling weakness.Volatility Focused Derivatives Approach

Now, we can see the effect of that earlier mood, with the pair trading much lower near 1.2680. But the backdrop has changed. January 2026 data shows UK inflation holding firm at 4.0%, which is double the BoE’s target. With the BoE base rate at 5.25%, the case for near-term rate cuts is much weaker than it was in 2025. On the US side, the Dollar’s strength tells a similar story to early 2025, when Fed officials did not want to cut rates too quickly. The latest Core PCE Price Index for January 2026 sits at 2.9%, still well above the 2% goal. This supports the Federal Reserve keeping its funds rate in the 5.25% to 5.50% range. That puts both central banks in a tough spot and increases uncertainty—something derivatives traders can use. Rather than taking a strong directional view, the next few weeks may suit strategies that benefit from volatility as markets react to each new inflation or jobs update. Options such as long straddles or long strangles may work well, as they can profit from a large move in either direction. Create your live VT Markets account and start trading now.During Asian trading, EUR/JPY rises toward 182.80, extending gains as yen support may limit further upside

EUR/JPY rose for a second session and traded near 182.80 during Asian hours on Thursday. Upside may be capped as the Japanese yen finds support from expectations of further Bank of Japan (BoJ) tightening.

Reuters reported that markets price in nearly an 80% chance of a BoJ rate hike in April 2026. Policymakers are expected to review new data before taking any further steps.

Japan Data And Yen Support

Japan’s core machinery orders rose 19.1% month on month to ¥1,052.5 billion in December 2025. This followed an 11% drop in November and beat forecasts for a 4.5% rise. The jump was linked to large, one-off orders from refineries and nuclear fuel producers. Private-sector orders rose 16.8% year on year in December, after a 6.4% fall in November. This also beat forecasts for a 3.9% gain. The Financial Times reported that ECB President Christine Lagarde may step down before October 2027. It did not give a timeline. Focus now shifts to Japan’s national CPI on Friday, along with early PMI data for Germany and the Eurozone. The BoJ targets inflation of around 2%. It used QQE from 2013, added negative rates and yield curve control in 2016, and raised rates in March 2024.Key Risks And Trading Outlook

EUR/JPY is moving higher, but the rally looks fragile, so caution is warranted. The market strongly expects the BoJ to raise rates in April, with close to an 80% probability priced in. That expectation could act as a firm cap on the pair in the weeks ahead. The case for a stronger yen is growing. Japan’s national core CPI for January 2026 held at 2.4%, staying above the BoJ’s target. While the surge in December 2025 machinery orders was seen as a one-off, it still supports the view that the economy can handle tighter policy. Friday’s national CPI report will be key for confirming (or challenging) this trend. On the other side, the euro faces headwinds from political uncertainty around the ECB presidency. Leadership doubts can weigh on a currency even when economic data is stable. The latest Eurozone Composite PMI for January 2026 was 48.5, which still signals contraction and makes the euro’s strength look less convincing. For derivatives traders, this backdrop points to higher volatility into the April BoJ meeting. One-month implied volatility for EUR/JPY has already risen to a six-month high of 9.5%, suggesting the market is preparing for a larger move. In this environment, buying puts to hedge against a downside pullback, or using straddles to trade a volatility rise, may be sensible. A similar setup played out in 2025. When expectations for a BoJ shift peaked, the yen strengthened quickly and EUR/JPY dropped sharply. The current upswing feels like the type of run-up that has come before past corrections. Create your live VT Markets account and start trading now.During Asian trading, USD/JPY approaches 155.00 as hawkish Fed minutes boost the dollar against the yen

USD/JPY rose slightly to near 155.00 in early Asian trade on Thursday. The move came as the US Dollar strengthened after hawkish signals in the Federal Reserve’s meeting minutes. Traders are now waiting for Japan’s National CPI report on Friday for the next cue.

The Fed has cut its benchmark rate by a total of 0.75 percentage points across moves in September, October, and December. This brought the target range to 3.5%–3.75%. Minutes from the January meeting showed officials were divided on what comes next, with several saying rate hikes could still be on the table.

Japan Political And Fiscal Backdrop

In Japan, Prime Minister Sanae Takaichi’s recent election win has lifted expectations for looser fiscal policy. This includes talk of a two-year suspension of the food sales tax. The IMF has warned Japan against such tax cuts, arguing they could undermine fiscal stability. Markets currently see the next Bank of Japan rate hike as most likely in April. Some also see March as possible if wage growth and inflation stay strong. Expectations for more BoJ tightening by April or July are generally supportive for the Yen and could weigh on USD/JPY. The Yen is driven by Japan’s economic data, BoJ policy, the US–Japan bond yield gap, and overall risk sentiment. Direct BoJ intervention is rare. Meanwhile, the BoJ’s ultra-loose policy from 2013 to 2024 helped weaken the Yen, until the central bank began a gradual shift in 2024. Earlier in 2025, USD/JPY pushed toward 155.00 due to hawkish Fed signals and a more cautious BoJ. Now, on February 19, 2026, the pair trades much lower near 148.50 as central bank policy paths have moved away from last year’s expectations. This change reflects the steady, but clear, policy tightening Japan has delivered over the past 12 months.Policy Divergence And Trading Implications

As expected, the Federal Reserve cut rates into the 3.50%–3.75% range late last year. But US inflation has remained stubborn. The latest Core PCE reading is still above 3%, which has kept the Fed on hold since December 2025. This has helped prevent a larger drop in the US Dollar and has kept it relatively firm against other currencies. In contrast, the Bank of Japan followed through with the rate hikes expected in 2025. It lifted its policy rate to 0.25% through two separate increases. This was a major shift away from negative rates and has supported the Japanese Yen. Traders are now looking for the BoJ’s next signal, which will depend heavily on upcoming data. In the weeks ahead, one major event for traders is Japan’s annual “Shunto” spring wage talks. Early reports suggest large unions are seeking wage gains above 5%, a level not seen in decades. If the final wage deals are strong, the BoJ may feel pressure to tighten further to contain inflation, which would likely support the Yen. With that setup, derivatives traders may look to position for more Yen strength, which would mean a lower USD/JPY. One straightforward approach is buying USD/JPY put options expiring in April or May 2026 to target a possible post-Shunto rate hike. Put spreads—buying one put and selling another at a lower strike—may offer a lower-cost way to express the same view. Still, the US–Japan rate gap remains wide. The US 10-year Treasury yield is around 4.2%, while Japan’s 10-year yield is near 0.9%. This gap supports carry trades and can keep demand under USD/JPY. So while momentum may favor a lower USD/JPY, pullbacks could attract strong buyers. Create your live VT Markets account and start trading now.DXY steadies near 97.70 in Asian trading after rising to a one-week high, keeping upside potential

The US Dollar Index (DXY), which measures the US dollar against a basket of major currencies, traded in a narrow range during Thursday’s Asian session. This came after it climbed to a more than one-week high. It held near 97.70 and was little changed on the day.

Minutes from the January FOMC meeting showed officials were divided on whether, and when, to cut interest rates. Inflation remained the main concern. Some officials said cuts could be needed if inflation drops as expected. Others warned that cutting too soon could put the Federal Reserve’s 2% inflation goal at risk.

Fed Minutes Jobs Data And Geopolitical Risk

The minutes followed last week’s strong January Nonfarm Payrolls report. That report lowered expectations for faster policy easing and helped support the dollar. Reports that the US military could be ready to strike Iran as early as this weekend also kept geopolitical risk in focus. This supported demand for the dollar as a safe-haven. Markets still price in at least two Federal Reserve rate cuts in 2026 after softer US consumer inflation data last Friday. Traders stayed cautious despite a positive market mood. Attention now turns to Friday’s US Personal Consumption Expenditure (PCE) Price Index, which is likely to drive the next move. This same time last year, in early 2025, the US Dollar Index was also consolidating near 97.70 as the Federal Reserve remained deeply divided. Strong jobs data was balanced by expectations that at least two rate cuts were coming. That created a tense standoff for the Greenback. Geopolitical risks tied to Iran also helped support the dollar by keeping its safe-haven appeal in place. Today, conditions look very different. The dollar has strengthened, and the DXY now trades around 104.55. The Fed ended up holding rates steady through most of 2025 because inflation stayed persistent. That outcome went against the market’s earlier hopes for aggressive easing. The gap between those expectations and the Fed’s actual path has been a major reason for the dollar’s rise over the past year.Inflation Labor And Volatility Signals

Recent data still gives the Federal Reserve—and the dollar—a mixed outlook. The January 2026 Consumer Price Index (CPI) report, released last week, showed core inflation edging down to 3.1%. That is still well above the Fed’s 2% target. At the same time, the latest Nonfarm Payrolls report showed a solid gain of 195,000 jobs. That points to a resilient economy and makes the timing of any rate cuts this year harder to judge. For derivatives traders, stubborn inflation combined with steady growth suggests volatility in rate-sensitive assets may stay high. Options strategies, such as buying straddles on euro or yen futures, can help traders position for a large move without having to pick a direction. Implied volatility for these currency pairs has risen to a three-month high of 9.2%, highlighting current uncertainty. Looking ahead, the focus shifts to the upcoming PCE Price Index, the Fed’s preferred inflation measure. A stronger-than-expected reading could push back expected rate cuts. That could lift the DXY and pressure equity index futures. Traders should be prepared for choppy trading and stay flexible around key data releases in the weeks ahead. Create your live VT Markets account and start trading now.Geopolitical tensions keep WTI above $65 despite slipping in Asian trading after a 4.9% fall

WTI traded near $65.00 a barrel during Asian hours on Thursday, after dropping 4.9% in the previous session. Prices stayed supported by supply risks tied to US-Iran tensions and stalled Ukraine-Russia talks.

US-Iran negotiations remain unresolved. Tehran said there was a “general agreement” on the framework for a possible nuclear deal. US officials said Iran has not met US conditions. US President Donald Trump said military action is still possible, and reports suggest it could turn into a long campaign.