The Japanese leading economic index was 109.9, falling short of expectations.

Japan’s Coincident Index decreases to 114.9 from 115.2

Japan’s coincident index dropped to 114.9 in November, down from 115.2. This change comes amid various market shifts and currency pair movements.

The EUR/USD pair is close to a four-year high at 1.1920. In contrast, the GBP/USD trades positively around 1.3660 after strong economic data from the UK.

Market Rally Influencers

Gold is on a six-day rally, hitting $5,100 during the Asian session. Bitcoin, Ethereum, and Ripple have shown signs of recovery after major corrections. In trade news, the U.S. has pulled back its proposed tariffs on key European economies. Cardano (ADA) is now priced around $0.34, following weeks of adjustments. A variety of broker options for 2026 are available, including those with low spreads, high leverage, and market-specific features. These options aim to meet different trader needs and preferences. With Gold exceeding $5,100, there is a clear movement towards safety due to global uncertainty. This dramatic price action indicates high implied volatility, making it a good time to explore protective put options on broader equity indices. This trend aligns with record central bank gold purchases in the second half of 2025, similar to the significant buying we saw in 2022 and 2023.Currency Market Dynamics

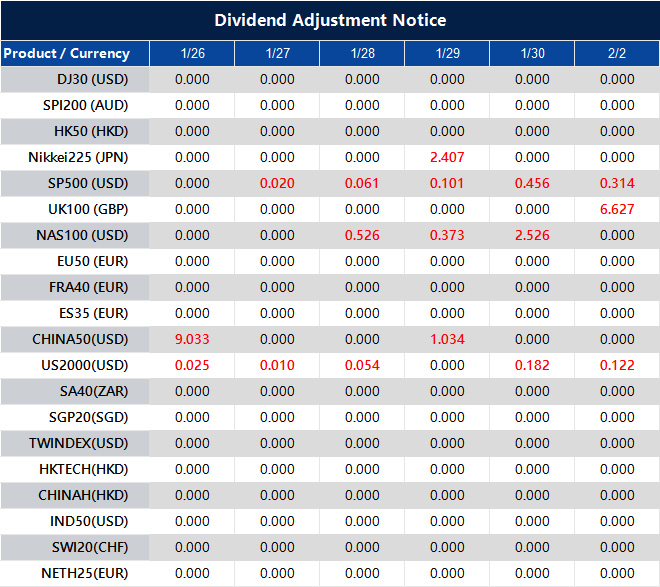

The US Dollar’s ongoing weakness is a key focus ahead of the Federal Reserve’s meeting this Wednesday. In this context, we expect EUR/USD and GBP/USD to remain strong, making long call options a smart strategy for capturing potential gains while limiting risks. Current market pricing suggests over an 85% chance that the Fed will indicate a dovish approach, putting further pressure on the dollar, similar to the trends seen in late 2023. We should closely watch the Japanese Yen, which is strengthening amid expectations of a hawkish Bank of Japan. This speculation is driven by core inflation figures that have stayed above the bank’s 2% goal for much of 2025, a situation not seen in decades. However, the risk of official action to weaken the Yen is significant, creating a volatile trading environment ideal for option straddles on USD/JPY. The Euro and British Pound are gaining from the dollar’s decline, with GBP/USD reaching levels not seen since September 2025. This strength is supported by solid UK economic data from late last year, but traders should be cautious as this rally largely stems from a weak dollar. Utilizing bull call spreads on EUR/USD could enable traders to profit from a continued rise toward 1.2000 while managing risk. Global trade tensions are affecting energy markets, keeping WTI crude oil prices steady around $61 a barrel. Ongoing supply concerns from transatlantic tariff disputes that emerged in late 2025 suggest this price strength may persist. Traders might consider buying futures contracts for short-term exposure or using call options to speculate on further price spikes if tensions escalate. Create your live VT Markets account and start trading now.Dividend Adjustment Notice – Jan 26 ,2026

Dear Client,

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

Industrial production in Singapore missed projections, showing an 8.3% decrease instead of the expected 10.1% drop.

Eur Usd Pair and the Federal Reserve

The EUR/USD pair went up by 0.36%, nearing four-year highs because the US Dollar weakened. Traders are keeping an eye on this pair as the Federal Reserve prepares to announce its policies. The GBP/USD pair has risen above 1.3650, showing positive movement thanks to strong UK economic data. Investors are now looking at the US Durable Goods Orders report for further guidance. Bitcoin, Ethereum, and Ripple are recovering slightly, staying close to important support levels after recent drops. Their price actions suggest possible stabilization or further recovery soon. In other updates, Cardano’s price is at $0.34, but ongoing corrections may lead to more declines. A drop in Open Interest indicates that fewer market players are involved.Weakness in the US Dollar Continues

The move towards safety in the market is speeding up, making long positions in gold an easy choice. Central banks have consistently bought over 1,000 tonnes of gold in 2025, providing strong support. Traders might consider call options on gold futures or gold-backed ETFs to benefit from rising prices while managing their risk. It looks like the US Dollar will continue to weaken, especially with the Federal Reserve meeting this week. The US Consumer Price Index has missed expectations for two months straight, dropping to an annualized rate of 2.1% in December 2025, which gives the Fed room to be more cautious. A direct way to take advantage of this trend is to short the US Dollar Index (DXY) using futures contracts. On the other hand, the British Pound is gaining strength, supported by strong domestic economic data. The latest S&P Global UK Composite PMI for January was 54.1, the highest in over a year, indicating that the UK economy is doing well. We believe that buying call spreads on GBP/USD is attractive for trading this divergence. Disappointing industrial production numbers from Singapore suggest potential challenges for the wider Asian export market. This data follows last week’s Caixin Manufacturing PMI from China, which dropped back to 49.8, indicating contraction and affecting regional sentiment. Buying put options on equity ETFs focused on Asia could be a useful hedge in the weeks ahead. Volatility is increasing across different asset classes, and the Japanese Yen is gaining from both safe-haven demand and a strict central bank. With the Bank of Japan signaling a possible exit from its negative interest rate policy by March, a stronger yen seems likely. We see value in buying put options on the USD/JPY pair, aiming for a drop below 140.00. Create your live VT Markets account and start trading now.Singapore’s industrial production fell by 13.3% month-on-month, better than the predicted decline of 15.2%.

Singapore’s industrial production fell by 13.3% in December compared to the previous month, which was better than the anticipated 15.2% drop. This indicates ongoing challenges in the manufacturing sector, influenced by global supply chain issues and economic uncertainties.

The manufacturing sector is crucial for the economy, and this result hints at some resilience, although the overall trends still look concerning.

Global Economic Factors

The global economy is influenced by geopolitical tensions, trade disputes, and shifts in monetary policy. As countries navigate these challenges, potential patterns may emerge that could impact future economic forecasts. At the close of last year, Singapore’s industrial production dropped 13.3%, a significant decline but still an improvement over the expected 15.2% decrease. This slight outperformance suggests the manufacturing sector might be stabilizing, creating a sense of cautious hope as we began the new year. Recent flash manufacturing PMI data for January supports this outlook, showing a score of 49.8, up from 47.5 in December 2025. While it still indicates slight contraction, this improvement suggests that the worst of the decline may have passed. Traders should keep an eye out for signs of stabilization in economic activity.Electronics Cluster Impact

The electronics cluster, vital to the local industry, is rebounding as global semiconductor sales saw their first monthly rise in six months. This has helped strengthen the Singapore dollar, with the USD/SGD exchange rate decreasing from its late 2025 peak of around 1.3800. The reduced anxiety is also reflected in lower implied volatility for SGD options. In light of this situation, it may be wise to focus on strategies that take advantage of stabilization instead of a rapid rebound. Bull call spreads on the Straits Times Index (STI) offer a defined-risk approach to positioning for modest gains in the coming weeks. Alternatively, selling out-of-the-money puts on solid industrial stocks could provide a way to collect premium, with the belief that a major collapse is now less likely. Create your live VT Markets account and start trading now.Gold prices rise today in the United Arab Emirates, according to market data

Gold prices in the United Arab Emirates rose on Monday, according to FXStreet. The price per gram increased to 598.30 AED from Friday’s 588.18 AED.

The price for gold per tola went up to 6,978.52 AED from 6,860.36 AED. Other measurements show that 10 grams of gold now costs 5,983.06 AED, and a troy ounce is priced at 18,609.49 AED.

How UAE Gold Prices are Set

FXStreet sets local gold prices by converting international rates into UAE currency and units, with daily updates. Gold has long been valued as a secure investment and a hedge against inflation. Demand for gold often increases during economic uncertainty. Central banks are significant buyers of gold, bolstering their reserves to instill economic confidence. In 2022, they added 1,136 tonnes, marking the highest amount on record. The price of gold typically moves in the opposite direction of the US Dollar and riskier assets. Gold tends to gain when interest rates are low and economic conditions are unsettled. Factors like geopolitical events, interest rates, and the strength of the US Dollar impact gold prices. When the Dollar weakens, gold prices usually rise.Current Market Trends

Gold prices have seen a noticeable rise, indicating a steady demand for safe investments. This comes after a stable period in the last quarter of 2025. Derivative traders should watch this upward trend as an important signal for the upcoming weeks. This price increase is supported by ongoing purchases from central banks. Recent data from the World Gold Council shows that emerging market banks bought over 850 tonnes of gold in 2025, creating a strong support level in the market. We expect this trend to continue as countries seek to move away from reliance on the US dollar. Minutes from the US Federal Reserve indicate a more cautious approach, with lower inflation figures for December 2025 at 2.8%. Lower interest rates lessen the cost of holding gold, making it a more attractive investment. This situation favors buying call options or long futures positions. Additionally, we are observing more shipping disruptions in major trade routes, adding geopolitical risk to the market. Such uncertainty often increases gold’s appeal as a safe asset. Buying protective put options on stock indices could be a smart strategy to hedge against this risk. In the derivatives market, we have noticed a rise in implied volatility for gold options, with the CBOE Gold Volatility Index (GVZ) increasing by 15% since the beginning of the year. This suggests that the market expects larger price swings soon. Traders might consider strategies like straddles or strangles to take advantage of this anticipated volatility, regardless of the direction. Create your live VT Markets account and start trading now.USD/CHF rises towards 0.7800 after a lower opening, driven by dollar strength from tariff concerns

USD/CHF has risen towards 0.7800, influenced by President Trump’s threat of a 100% tariff on Canada if it reaches a trade deal with China. When trading began, the pair was at about 0.7770, after starting lower during Monday’s Asian session. The US Dollar has since bounced back from earlier losses.

There are concerns that the US Dollar might decline due to rumors about efforts to support the Yen. Reports suggest that the New York Federal Reserve has performed a rate check with major banks, hinting at possible market interventions to help the Japanese Yen.

Swiss Franc as a Top Hedge

The Swiss Franc may receive backing as Goldman Sachs sees it as a strong hedge against risks from central banks. Switzerland’s solid fiscal position makes the Franc a safe choice, keeping it strong against global inflation pressures. Market sentiment, economic indicators, and the Swiss National Bank’s (SNB) policy decisions all influence the Swiss Franc. The currency is also affected by the stability of the Eurozone due to Switzerland’s close economic links. The economic health of Switzerland and the SNB’s monetary policies, including interest rate changes, can alter the Franc’s value. Reflecting on the tariff threats from late 2025, we noted how geopolitical risks can quickly strengthen the US Dollar. This scenario pushed USD/CHF closer to 0.7800, highlighting the impact of political news on market sentiment. As of late January 2026, the focus has returned to fundamental factors that still support a strong Dollar. Recent US inflation data from December 2025 showed a rate of 3.4%, which was higher than expected. Additionally, the job market remains robust with over 200,000 jobs added. This situation suggests that the Federal Reserve will be cautious about cutting interest rates, helping the USD remain strong.Potential for Increased Volatility

However, the Swiss Franc’s strength against inflation is now being tested. With Switzerland’s latest inflation rate steady at a low 1.7%, the Swiss National Bank may cut rates sooner than other major central banks. This difference in monetary policy could limit the Franc’s strength in the short term. With these mixed signals, we expect increased volatility in the USD/CHF pair. Implied volatility for one-month options has risen to 7.8%, up from 7.2% last month, indicating market uncertainty. Traders might consider strategies like long straddles to benefit from a significant price movement in either direction without predicting the outcome. We must also consider the intervention rumors from last year. The possibility of coordinated actions to weaken the US Dollar, especially to support the Yen, remains a notable risk for those with long USD positions. Such actions could drive USD/CHF down sharply, regardless of the interest rate differences. Create your live VT Markets account and start trading now.EUR/USD rises towards 1.1900 during Asian session as USD weakens

Euro Focus

This week, we’re focusing on the Eurozone’s Q4 GDP and Germany’s HICP data for January. Currently, the EUR/USD is trading at about 1.1866, staying above the 20-day EMA at 1.1713, which indicates a positive trend. Technical indicators show strong momentum, with the 14-day RSI close to overbought territory at 69.49. If the upward trend continues, EUR/USD could surpass its four-year high of 1.1919, with support seen at the 20-day EMA. The Federal Reserve can affect the US Dollar by changing interest rates to maintain price stability and full employment. Quantitative Easing (QE) generally weakens the Dollar, while Quantitative Tightening (QT) strengthens it. Always conduct individual research before making market decisions. Remember, all investments carry risks, including potential losses.Opportunities in Euro

The strong upward momentum in EUR/USD presents opportunities. With the pair nearing a four-year high around 1.1920 and the Dollar Index (DXY) dipping to 97.00, bullish strategies for the Euro look promising. Traders might consider buying call options on EUR/USD or using bull call spreads to take advantage of further gains while managing expenses. The Federal Reserve’s meeting this Wednesday is the week’s key event, though a rate hold at 3.50%-3.75% seems already expected. The Fed’s tone will be important, especially after the 75 basis points cuts in late 2025 when unemployment rose to 4.5%. Any sign of a continued dovish approach could weaken the US Dollar further. If you expect volatility from the Fed’s statement, a long straddle or strangle on EUR/USD could be effective. This strategy profits from significant price movements in either direction, removing the need to predict how the market will react to the Fed’s guidance. It’s a direct bet on increased market activity. The Dollar’s weakness extends beyond the Euro, creating chances in other currency pairs. Recent CFTC data shows that speculative net-long positions on currencies like the British Pound and Australian Dollar against the USD are increasing, reflecting a broader market sentiment we can leverage through various cross-currency derivatives. In Europe, upcoming Q4 GDP figures will be crucial for the Euro’s strength. After a -0.1% contraction in Q3 2025, any signs of economic recovery could push the EUR/USD pair even higher. Positive inflation data from Germany could further strengthen the Euro. From a technical perspective, the Relative Strength Index (RSI) is around 69.50, which suggests the market is nearing overbought conditions. Even though momentum is strong, it’s wise to avoid chasing this rally without a strategy. Consider using options to limit risk or take partial profits on current long positions before reaching the 1.1920 resistance level. Create your live VT Markets account and start trading now.Gold prices rise in Pakistan today according to data from multiple sources.

Gold prices in Pakistan have gone up, according to FXStreet. The price for one gram reached 45,105.93 Pakistani Rupees (PKR), rising from 44,363.37 PKR last Friday. The price per tola also increased to PKR 526,122.30 from PKR 517,445.70.

These numbers are based on daily updates that adjust international prices to PKR. While they provide a general reference, local prices may vary. Gold is often seen as a safe asset and a way to preserve value.

The Role of Central Banks

Gold is highly valued during uncertain times and is used as protection against inflation and currency decline. Central banks hold the most gold, which helps strengthen currencies and boost economic confidence. In 2022, they purchased 1,136 tonnes of gold, the highest amount ever recorded in a single year. Gold prices typically rise when the US Dollar falls. They tend to increase with lower interest rates and during geopolitical turmoil. The value of gold mainly depends on the US Dollar: it goes up when the dollar weakens and stabilizes when the dollar is strong. Given the economic uncertainty we faced in 2025, gold is once again seen as a safe asset. The rising price indicates that people are seeking safety due to ongoing concerns about inflation that have continued into the new year. This situation presents clear trading opportunities based on market volatility in the weeks ahead.Impact of the US Dollar and Interest Rates

We need to closely monitor central banks, as they are significant buyers of gold. Following their record purchases in 2022 and 2023, these banks have continued to increase their reserves throughout 2025. The latest data from the World Gold Council shows that this trend is steady, providing strong support for gold prices and favoring long-term investments. The relationship between gold and the US Dollar is crucial for our strategies. As the Federal Reserve hints at a less aggressive approach to interest rates compared to 2023 and 2024, the dollar has begun to weaken. This suggests that buying call options on gold futures could be a smart move, anticipating further declines in the dollar. We should also keep an eye on risk assets like stocks. The poor performance of major stock indices in the last quarter of 2025 shows that investors are cautious. Any more declines in the stock market could lead to a further spike in gold prices. Geopolitical instability continues to be a significant but unpredictable factor influencing gold prices. Ongoing tensions keep the market anxious, making volatility strategies, like straddles, potentially profitable. Even rumors of new conflicts can quickly cause price surges, so we need to be ready to respond. Create your live VT Markets account and start trading now.Gold prices in India have increased today, according to compiled data.

Gold prices in India saw an increase on Monday. The price per gram rose to 14,970.54 Indian Rupees (INR) from 14,713.91 INR on Friday. The price per tola also increased to 174,617.60 INR, compared to 171,620.10 INR at the end of last week.

FXStreet figures these prices by adjusting international rates for local currency and measurement units. The price per Troy Ounce hit 465,658.30 INR, with updates reflecting market conditions at the time of publication.