Gold prices rise in Pakistan today, according to the latest data.

**Gold Prices and Global Market Influences**

Gold prices in Pakistan rose on Thursday to 30,269.47 Pakistani Rupees (PKR) per gram, up from 30,073.52 PKR on Wednesday. The price per tola increased to 353,058.20 PKR from 350,771.70 PKR.

The US House of Representatives is advancing President Trump’s tax and spending bill, which could add $3 trillion to $5 trillion to the national debt. Recent treasury bond auctions showed low demand, raising concerns about the growing US budget deficit.

Moody’s downgraded the US credit rating, causing the US Dollar to weaken. This contributed to higher gold prices. Global tensions, including US-China trade relations and ongoing conflicts, increased demand for gold.

Central banks are significant buyers of gold as they aim to strengthen their economies. In 2022, they added 1,136 tonnes of gold, worth around $70 billion, to their reserves.

Gold prices are influenced by geopolitical events, currency values, and interest rates, since gold is priced in US Dollars. Changes in the Dollar can inversely impact gold prices.

**Impact of Market Instability on Gold Prices**

The recent rise in gold prices—from 30,073.52 PKR to 30,269.47 PKR per gram and nearly 2,300 PKR per tola—reflects overall global market trends rather than issues specific to Pakistan. This trend suggests a deeper story; as gold rises, the US Dollar weakens, highlighting global economic factors at play.

The tax and spending bill advancing in the House has raised concerns, as it may increase US debt by up to $5 trillion. This, along with poor demand in treasury bond auctions, has made the market more cautious. Bond traders are reacting to the growing debt and uncertain fiscal policies, leading to a reevaluation of their US-backed asset investments.

Moody’s downgrade of the US credit rating reinforces this caution. Such downgrades signal that fiscal discipline is lacking, which decreases the appeal of Dollar-denominated assets and contributes to the Dollar’s decline. When the Dollar weakens, gold tends to increase, which is a pattern traders consistently watch.

Geopolitical tensions also continue to rise. While there are signs of cooperation between the US and China, dependable stability remains elusive, and other conflicts persist. This uncertainty encourages increased gold buying, motivated not just by speculative reasons but also for protection. Both retail investors and central banks are driving this demand.

Central banks, in particular, have made significant moves. Adding 1,136 tonnes of gold in one year indicates a strategy to guard against currency risk and inflation. Institutions are responding to the same economic indicators as traders—credit quality, fiscal policy, and political stability—by accumulating gold for the long term.

So, where do we stand? With bonds losing appeal and the Dollar facing potential further weakening, gold appears to be a wise choice—not as a sign of excitement but as a safe haven. This situation prompts options traders to monitor implied volatility levels on metals and adjust strike positions, especially for US-denominated assets. Premiums might shift due to macro hedging efforts, especially if central banks remain active.

The yield curve is also important to consider. An inverted yield curve paired with a weakening Dollar makes precious metals attractive for rate-sensitive investments. Keep an eye on growing open interest near critical resistance levels in gold; a price increase without solid support could indicate instability instead of ongoing strength.

In conclusion, these events are interconnected and present a clear narrative regarding US fiscal policy and global reactions to instability. The responses in the gold market are insightful, and adjusting derivative strategies will be necessary to navigate conditions that are unlikely to change in the short term.

Create your live VT Markets account and start trading now.

New Zealand announces NZ$4 billion increase in bond program over four years, says Willis

New Zealand’s Budget predicts a deficit of NZ$-14.74 billion for 2024/25 and NZ$-15.60 billion for 2025/26. Net debt is expected to be 42.7% of GDP in 2024/25, with a projected cash balance deficit of NZ$-9.99 billion.

For 2024/25, GDP is estimated to drop by 0.8%, but a recovery is expected in 2025/26 and 2026/27, with growth rates of 2.9% and 3.0% respectively. Inflation is projected to stay within the 1% to 3% target band for the next five years.

Currency Reaction

The New Zealand Dollar has barely reacted to the budget news, trading 0.25% lower at around 0.5925. The government does not expect to see an operating balance surplus in the next five fiscal years, and trade tariffs remain influential on how quickly the economy can recover. Although the deficit figures may seem alarming—especially with a deeper deficit forecast for 2025/26—the government is prioritizing fiscal support over spending cuts. The projected 0.8% GDP contraction next year reflects this broader borrowing strategy which favors economic stimulus. Despite these challenges, core inflation remains steady. The forecast keeps inflation within the 1% to 3% band, indicating that price stability is not currently at risk. This allows monetary policy to stay stable without needing an immediate response. As the government increases bond issuance, funding costs may rise, but the Reserve Bank doesn’t need to react aggressively right away. The currency’s slight dip suggests that the market was prepared for these projections. The Kiwi dropped only 0.25%, indicating that investors are becoming more accustomed to deficit announcements when inflation and growth seem stable. This indicates a calm response regarding interest rates and currency fluctuations.Trade and Interest Rates

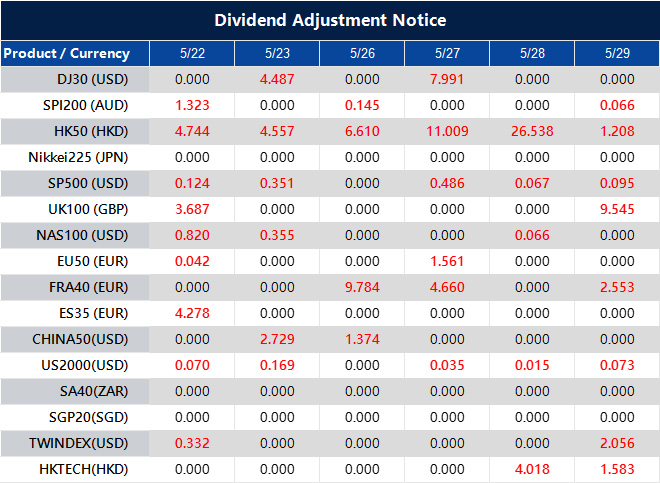

The balance of risks largely depends on timing. While the multi-year recovery looks promising from 2025 onward, the current economic downturn will impact interest rates. Expect the yield curve to remain relatively flat over the next two quarters, especially if international factors remain subdued. It’s essential to analyze future expectations. Export tariffs continue to impede predicted trade growth, which adds uncertainty to the recovery but is less affected by domestic policies. Positions that consider a slow or uneven improvement in trade balances may perform better than fixed growth expectations. Short-term interest rate trades may stay stable unless the Reserve Bank changes its approach sooner than anticipated. However, for longer-term rates, any increase in bond issuance could widen spreads, especially during periods of weaker GDP. We are focusing on how interest rates in New Zealand compare to global benchmarks, noting how the budget plan aligns with monetary policy. For those trading volatility, a stable inflation outlook suggests limited upward movement in break-evens and inflation swaps in the short to medium term. However, with growing deficits and borrowing needs, concerns about sovereign credit can arise intermittently. Option pricing might remain low, but could rise if debt issuance outpaces market absorption. Robertson’s budget figures did not significantly impact the Kiwi, but the ongoing debt dynamics and changing long-term growth rates create opportunities—especially as policy differences emerge. Be cautious with long Kiwi positions during global rate changes or demand shocks. The real challenge will be watching whether the anticipated bounce in 2025/26 overcomes initial hurdles or if downward revisions threaten the projected 3% growth targets. Create your live VT Markets account and start trading now.Dividend Adjustment Notice – May 22 ,2025

Dear Client,

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

Asahi Noguchi, a BoJ board member, notes Japan’s economy is steadily growing and may require policy adjustments.

The Bank of Japan (BoJ) has noted that Japan’s economy is growing steadily, with possible changes to policy rates on the horizon. The central bank is closely monitoring if inflation remains stable at around 2%, emphasizing the importance of sustainable inflation and rising wages.

Recently, the economy faces external risks due to increasing pressures from international tariff policies. In March, the yield on the 10-year Japanese Government Bond was close to 1.6%. The BoJ intends to maintain its loose monetary policy because the primary cause of inflation stems from rising import costs.

Monetary Policy Overview

Japan’s current monetary policy includes Quantitative and Qualitative Easing, a strategy that began in 2013 to help boost inflation. Negative interest rates and yield control were introduced in 2016, leading to a shift in 2024 when interest rates increased. This change caused the yen to weaken, prompting policy adjustments as inflation surpassed the 2% target. The BoJ’s policy adjustments reflect concerns about the yen’s weakness and rising global energy prices. Wage increases are crucial for sustaining inflation, which influences the BoJ’s considerations regarding its previously established ultra-loose policy. The USD/JPY exchange rate was at 143.30, showing recent market trends. Policymakers in Tokyo now believe the economy is growing steadily. The focus is on whether domestic price trends, especially underlying inflation, can consistently stay around 2% without external boosts. The emphasis is on wage growth to support consumer spending and create stable inflation. Any changes to interest rates will likely be gradual and based on improved wages across various industries. External factors, including tariff changes and global political conditions, may still affect prices negatively. Japan, as a significant energy importer, is notably vulnerable here. In March, rising yields on government debt close to 1.6% indicated that markets are preparing for tighter conditions, even if policy hasn’t shifted entirely yet. This suggests that they are anticipating persistent inflation before adjusting further. Since 2013, the BoJ has injected funds into the economy through aggressive asset purchases—both quantitative and qualitative. This approach included deeply negative rates and yield curve control starting in 2016. These measures were aimed at addressing ongoing shortfalls in inflation targets. As we move into 2024, rising interest rates became necessary, especially as consumer prices exceeded the Bank’s target. This shift was driven not just by inflation but also by the yen’s significant decline against the US dollar.Implications for Derivatives Markets

For those in the derivatives market, changes in Japan’s monetary policy have several immediate effects. Pricing options or futures related to JGBs or FX pairs like USD/JPY now requires monitoring not only policy statements but also labor data. If wage figures suggest strong consumption growth, sharp movements in the yen could signal the likelihood of higher rates. As the BoJ’s approach gradually changes, derivative trades on rate-sensitive instruments should consider various scenarios—some where inflation slows down and others where wage growth propels it. The transition won’t happen suddenly, but it is in progress. Traders need to incorporate these developments, considering how companies might respond to expected cost rises. We have observed the yen reacting strongly during past tightening cycles, even minor ones. Monitoring 10-year yields and their impact on rate differentials with the U.S. may help timing decisions for currency contracts. The forward market typically adjusts prices faster than spot traders may anticipate. Experience shows that BoJ policy moves are cautious yet impactful. Statements regarding wage conditions or inflation expectations should be viewed as directional indicators. Thus, option positions may benefit from broader implied volatility bands as the market reflects on data uncertainties. In the coming weeks, interest in inflation reports and wage negotiations, especially among Japan’s larger companies, is expected to grow. Any sign that these metrics are holding steady—even slightly—may support policy changes. When market consensus leans strongly in one direction, it could create contrarian timing opportunities in rates and currency markets. Currently, the tone is one of caution but also readiness to act. This dual perspective is where traders can find an advantage. Carefully timing rate exposure while staying responsive to wage and consumer behavior will likely yield better results than static positions. Create your live VT Markets account and start trading now.PBOC sets the USD/CNY central rate at 7.1903, lower than before

The People’s Bank of China (PBOC) has set the USD/CNY central rate at 7.1903 for the latest trading session. This is slightly lower than the previous rate of 7.1937 and also lower than the expected rate of 7.2009 predicted by Reuters.

The PBOC aims to keep prices and exchange rates stable while supporting the economy. It is owned by the People’s Republic of China and overseen by the Chinese Communist Party Committee Secretary.

PBOC Monetary Policies

The PBOC uses several tools for its monetary policy, including the seven-day Reverse Repo Rate and the Medium-term Lending Facility. Changes to the Loan Prime Rate (LPR) can affect the Renminbi’s exchange rates. Private banks are allowed in China, with 19 currently in operation. The largest ones are digital lenders WeBank and MYbank, associated with Tencent and Ant Group. All provided information is for informational purposes only and should not be construed as financial advice. It’s important to do thorough research before making investment decisions. The recent adjustment in the USD/CNY central parity rate, from 7.1937 to 7.1903, though small, reflects the PBOC’s ongoing efforts to manage the Renminbi’s strength within controlled limits. The average forecast from Reuters expected 7.2009, indicating that the central bank aims to apply subtle pressure on the USD/CNY rate. This move suggests a policy preference for a stronger local currency, possibly to show domestic confidence or to limit imported inflation. The PBOC closely monitors monetary conditions, and any difference from market expectations in its daily fixing provides insight into its policy direction. Short-term traders focusing on rate differences or market momentum should pay attention to these small but intentional changes. These adjustments usually signal a trend that lasts for several trading sessions, influencing implied volatility based on the interpretation of the central bank’s intentions.Recent Market Dynamics

It’s important to know that the PBOC has multiple tools it can use quickly, such as open market operations like reverse repos, term lending through the Medium-term Lending Facility, or changes to the Loan Prime Rate. These are practical measures employed to adjust policies without indicating long-term commitments. Recent actions, particularly around the LPR, have been either neutral or dovish, suggesting ongoing support for growth, but within limits. With strict capital controls and low consumer inflation, the PBOC might be strategically keeping the Renminbi stable to better manage external pressures and support confidence in key economic sectors. Online banks like WeBank and MYbank may not significantly impact large capital flows, but they show that funding innovation is still active. Their roles as credit providers within the fintech umbrella reflect consumer demand and liquidity distribution, especially for small and medium enterprises. Keep an eye on how authorities encourage or discourage credit use through these platforms, as it can significantly impact consumer sentiment and market expectations. In the near term, reactions from other central banks—particularly the Fed—will influence adjustments in USD/CNY positioning. The PBOC’s daily fixings suggest it wants some flexibility, which could reduce volatility in this currency pair. Options traders may need to revise delta hedges if the range remains tight; carry trades could emerge if implied yields exceed hedging costs. No one makes policy changes in isolation. Adjustments are purposeful and carefully timed. It’s essential to understand the fixings and support them with the tools available. There’s usually no ambiguity in these actions. Create your live VT Markets account and start trading now.Singapore’s GDP declined 0.6% in the first quarter, less than the predicted 1% drop.

Singapore’s Gross Domestic Product (GDP) decreased by 0.6% in the first quarter compared to the previous quarter. This result is better than the expected drop of 1%.

GDP data is important because it shows how well Singapore’s economy is doing and can affect economic policies.

Understanding Economic Contraction

This contraction means economic activity has slowed down from the last quarter. However, the actual decline was not as bad as predicted. This information can impact market outlook and influence business and investment choices. It’s crucial to grasp GDP trends to understand broader economic changes. Though a 0.6% decline in Singapore’s GDP may seem worrying, it turned out to be less severe than the expected 1% drop, which is a small positive surprise. This indicates that while growth has slowed, the economy performed slightly better than feared, especially given high interest rates and weak global demand. These changes are not as drastic as those seen during a financial crisis but still show reduced growth in major sectors. At this point in the year, this performance suggests we should remain cautious, but also that the worst-case scenarios haven’t occurred yet. A quarterly decline alone doesn’t automatically mean a downturn, but consecutive drops after low activity are taken seriously by economists. GDP figures often influence market sentiment because they can indicate shifts in spending, employment, and confidence. Currently, what matters is whether this contraction is a temporary situation or the start of a trend. Policymakers watch this figure closely because it helps them adjust spending expectations. Even though the performance was slightly better than expected, a narrow margin of improvement shouldn’t be seen as a sign of strength, especially with external demand still shaky.Market Reactions to GDP Data

For those keeping an eye on derivatives, the key takeaway is to prepare for a long period of moderate volatility rather than any sudden changes in inflation or growth. The shorter end of the yield curve usually reacts first to GDP data, and spreads began widening last week in anticipation of weaker activity. This data reduces the urgency to hedge against aggressive policy changes, but there is no new momentum to support risk-seeking trades. Borrowing costs remain high, and tight financial conditions have not fully impacted the economy, keeping downside risks in mind. In derivative pricing, what matters is not just where the data lands but how far off consensus was from reality. In this case, the slight positive surprise is unlikely to significantly change forward guidance. Hedging strategies might still favor options linked to declines in production in the second quarter. Macro positions are sensitive to open interest, and unless there’s a rebound or changes in trade volumes, risk premiums are unlikely to lessen. Lim’s team has noted that any further weakness in trade or manufacturing—whether caused by China or regional issues—could lower projections for the third quarter. Currently, the main concern is growth, more so than inflation, which is already reflected in interest rate futures. The GDP figure shouldn’t be ignored just because it didn’t meet the worst-case predictions. The 0.6% drop confirms that economic activity has significantly cooled. We are closely watching how this affects capital allocation. Yield curves, forward rates, and longer-term swaps are adjusting, but not enough to indicate a major shift. As some market players test boundaries, especially in FX and rates volatility, the bias leans toward neutral or lower growth expectations. Upcoming releases, especially export volumes and purchasing managers’ indexes, will help determine if this contraction is a one-time event or a sign of a continuing trend. Risk models are likely to revise near-term demand expectations unless there’s an improvement in trade flows soon. Until then, avoiding aggressive positioning is probably the best strategy. Create your live VT Markets account and start trading now.In March, Japan’s machinery orders rose 8.4% year-on-year, surpassing forecasts of -2.2%.

Japan’s machinery orders in March rose by 8.4% compared to last year, surpassing expectations of a -2.2% decrease. This strong growth comes despite uncertainties in the global economy.

The results indicate solid demand in Japan’s machinery sector, going against earlier predictions of a decline. An ongoing increase in machinery orders may boost overall economic activity.

Currency Markets Overview

In the currency markets, the AUD/USD stays above 0.6400, influenced by possible rate cuts from the Reserve Bank of Australia and a weak US Dollar. Meanwhile, USD/JPY is near 143.50, showing mixed expectations between US and Japanese monetary policies. Gold prices are rising, getting close to $3,350 as anticipation builds around US PMI data. Bitcoin has surged to a new all-time high over $111,800 after a brief dip caused by weak US Treasury bond auction results. The forex and commodities markets are lively, influenced by changing trade tensions and policy adjustments. Keeping an eye on these factors is crucial for understanding potential market shifts. Although Japan’s machinery orders in March exceeded expectations by a large margin, rising 8.4% year-on-year compared to the forecast contraction of 2.2%, this doesn’t necessarily indicate a broad recovery in domestic business investment. Instead, it shows a strong sub-sector that could help support overall demand, especially as companies remain cautious about capital spending. We believe this level of outperformance, amidst global manufacturing and trade uncertainties, suggests steady industrial momentum in Japan that is not yet reflected in broader market indicators.Implications for Market Participants

For investors in Japanese equities or index futures, the renewed demand for machinery could act as a buffer against potential risks if corporate spending picks up. However, the sustainability of this trend relies on stable export demand, particularly from other Asian countries. A rise in industrial production or inventory trends could strengthen the positive signal from machinery data. In the currency markets, the Australian Dollar hovers above 0.6400 against the US Dollar, influenced by two opposing factors. On one side, dovish remarks and soft domestic data suggest further rate cuts from the Reserve Bank of Australia; on the other, a weaker US Dollar has supported the pair. This zone may act as a short-term base if US economic data remains inconsistent. Traders should prepare for more significant swings around inflation or wage data releases from either country, especially as realized volatility remains low. The USD/JPY near 143.50 indicates market uncertainty about differing rate outlooks. The Federal Reserve has kept the market guessing with mixed signals regarding inflation and potential cuts, while Japanese policymakers are gradually moving away from overly loose policies. Frequent comments from Tokyo officials suggest concern over erratic yen movements. Implied volatilities for near-term USD/JPY options are high, anticipating possible government action or policy changes. Traders in this pair may want to consider accumulating positions ahead of key events for favorable risk-reward opportunities, particularly if economic data surprises. In commodities, gold is inching closer to $3,350 as interest in inflation hedging grows. Weak demand from a recent Treasury auction has slightly pressured real yields, benefiting this non-yielding asset. Upcoming US PMI data could shift sentiment again, depending on perceived growth momentum. We suggest traders adjust their expectations to respond short-term to macro data, as positioning in gold has become crowded. Even minor pullbacks could trigger stop-loss levels and prompt rapid market movements. Bitcoin’s rise past $111,800 raises questions about its sustainability. The bounce back after a recent dip—caused by a poor Treasury auction—indicates ongoing interest in digital assets when traditional ones underperform. Institutional flows seem to be returning, and if macro risk sentiment stabilizes, it could support further gains. Short-term traders should assess whether chasing momentum is wise or if more cautious entries would offer better risk-reward opportunities, especially during quarterly settlements or liquidation sessions from derivatives exchanges. Overall, we observe that asset classes are reacting to shorter macro cycles and data interpretations rather than following a definitive trend. Expectations on rates, policy approaches, and supply-side factors are reshaping market prices, favoring agility. It’s important to focus on precise position sizing, selective risk exposure, and clear trigger points that could invalidate core strategies. Create your live VT Markets account and start trading now.Gold prices rise above $3,300 amid geopolitical tensions and US debt concerns

Gold prices have increased by over 0.50%, staying above $3,300. This rise comes as traders worry about the US tax bill vote and ongoing tensions in the Middle East. Currently, XAU/USD is trading at $3,317, having bounced back from a low of $3,285.

US equity markets are down, and US Treasury bond yields are on the rise. A tax-cut bill’s potential approval could add nearly $3.8 trillion to the national debt.

US Dollar Index Dip

The US Dollar Index (DXY) dropped 0.52% to 99.49 after a downgrade of US debt, which supports higher gold prices. Meanwhile, tensions in the Middle East persist, even as China and the US reduce tariffs ahead of upcoming talks. Traders are keeping an eye on Federal Reserve speeches, Flash PMIs, housing data, and Initial Jobless Claims. US Treasury yields are climbing, with the 10-year yield up by nine and a half basis points to 4.58%. Gold prices are gaining from concerns about US debt following the downgrade of the government’s credit rating. The Federal Reserve believes that current monetary policy is sufficient and is aware of the inflationary effects of rising US tariffs. Gold may test $3,350, with additional targets at $3,400 and $3,500. If prices turn bearish, they must fall below $3,300, with support at $3,204.Federal Reserve Impact on Gold

The Federal Reserve’s interest rate decisions influence the strength of the US Dollar. The Committee meets eight times a year to evaluate economic conditions and decide on monetary policy, which may include quantitative easing or tightening. Gold’s recent price increase reflects market anxiety driven mainly by fiscal and geopolitical uncertainties. As prices recover from lows and surpass the $3,300 mark, traders are shifting toward safe-haven assets amid worries about the US’s fiscal responsibility and rising global tensions. While equities have struggled, Treasury yields are rising—particularly the 10-year yield, which is approaching 4.6%. Generally, higher yields reduce the appeal of non-yielding assets like gold. However, concerns about the US’s future debt levels, especially with the tax changes projected to add over $3.5 trillion, seem to outweigh the impact of yields. As markets digest the downgrade of US debt quality, the US Dollar Index fell below 99.5. This decline in the dollar has strengthened gold since the metal is priced in dollars. A weaker dollar increases purchasing power for foreign buyers, which boosts gold prices. Additionally, tensions in the Middle East are contributing to gold’s upward momentum. Although US-China tariffs have eased slightly to facilitate discussions, it hasn’t alleviated worries about global stability. Markets are shifting focus to various economic indicators this week, including manufacturing flash PMIs, housing market data, and new jobless claims. These will likely influence short-term sentiment regarding monetary policy and inflation trends. Rising bond yields indicate ongoing inflation concerns, despite the Federal Reserve’s claims that its current stance is adequate. From a strategy perspective, prices have held just above major support at $3,285, and the upward momentum appears strong as gold moves toward $3,350. Breaking through this level could lead to targets of $3,400 and $3,500 if macroeconomic issues don’t reverse the trend into commodities. It’s crucial to consider the Committee’s recent statement. The central bankers are maintaining steady policy, indicating that current interest rates align with their inflation goals. They have also recognized that increasing tariffs push prices higher. They might let data influence their next move; however, with inflation below target and core readings being informative, a pause might be preferable over risking greater uncertainty. Unless there are significant geopolitical changes, there’s a limited volatility window driven by macro announcements and scheduled Fed speeches. Reactions to these events, especially if they differ from the Fed’s wider messaging, could quickly shift dynamics. Those watching derivatives should stay alert for increased implied volatility, especially regarding gold and currency pairs linked to Treasury shifts. While support is around $3,204, prices above $3,300 indicate a strong bullish trend for now. A clear drop below this level could change the outlook, but currently, the upward trend holds unless data or central bank comments significantly ease current fears. Create your live VT Markets account and start trading now.US Treasury yields rise sharply after disappointing 20-year bond auction and upcoming budget vote

US Treasury yields rose sharply on Wednesday. This increase followed a weak auction for 20-year US bonds and came just before a crucial budget vote in Congress. The yield on the 10-year Treasury note jumped by 11 basis points to 4.601%.

A sale of $16 billion in 20-year bonds saw weak demand, with yields climbing to 5.047%, up from 4.810% in the previous auction. US government debt yields increased after Moody’s downgraded US credit ratings, citing ongoing fiscal challenges.

Concerns About the Budget

Sources report that worries are growing about US budget deficits, with new tax law estimates potentially adding trillions to the deficit. The yield on the 20-year note reached 5.125%, its highest since November 2023. Economic policies from former President Donald Trump drove Treasury yields higher as tariffs contributed to inflation, which pressures the bond market. The House of Representatives is expected to vote on Trump’s budget soon. The Federal Reserve’s choice to keep interest rates steady impacted short-term yields, pushing the 2-year Treasury note yield up to 4.022%. Interest rates affect currencies and gold prices, while the Fed funds rate shapes market expectations and stability. Yields on US government bonds surged midweek, mainly due to weak interest in the $16 billion 20-year bond auction. Investors showed fatigue when demand was low, making markets hesitant, especially with increasing supply and worries about America’s long-term fiscal health. Yields reached 5.047%, significantly higher than in the last auction—indicating that buyers wanted more compensation for their investment. Such demand shortfalls not only cast doubt on future auctions but also affect the broader fixed income market, raising borrowing costs and shaking confidence in upcoming bond sales.Market Responses and Future Outlook

After Moody’s downgrade, which pointed to continuing budget deficits and rising debt levels, the markets reacted quickly. The yield on the 10-year Treasury note rose sharply, reflecting changing risk perceptions. Institutions must rethink their pricing strategies, particularly with long-term yields climbing. The 20-year yield reached its highest level since last November, signaling a serious challenge to confidence in America’s fiscal direction, where each poorly received auction becomes increasingly significant. There are wider concerns about the fiscal approach being taken, especially with trillions in new obligations expected. The budget debates in Congress are no longer just routine; they’ve become critical moments for markets already grappling with heavy issuance. For traders, it’s clear that much of the pressure arises from policy decisions rather than mere economic trends. Bond pricing is now influenced not just by inflation expectations or job data but by governmental indecision. Short-term yields are also climbing, especially the 2-year yield, which has moved above 4% as market participants expect rates to remain high for the foreseeable future. With the Federal Reserve holding its benchmark interest rate steady, focus has shifted to how persistent inflation might become and if enough tightening has already occurred. The yield curve remains inverted, signaling skepticism about growth prospects and doubts regarding future inflation management. In this challenging environment, investors should consider making cautious adjustments and practicing careful risk management. It’s important to concentrate on actual yields and market volatility related to policy changes. Auction dynamics also provide key insights; observing bid-to-cover ratios, tail sizes, and indirect bidder activity can help forecast short-term yield movements, particularly for intermediate and long durations. Currency and precious metals are also under pressure from these developments, mainly due to changing monetary policy expectations. The dollar’s strength is somewhat bolstered by the Fed’s current stance that rate cuts are not on the horizon, making dollar-denominated assets more appealing. However, monitoring dollar funding costs and repo activity is essential for signs of stress. In summary, yields are sending a clear message: the balance between fiscal challenges and central bank policies is precarious. If weekly auctions continue to disappoint and deficits grow unchecked, we may see more volatility in yields. This environment presents opportunities for dislocations and potential outperformance. Active management of exposure, especially with interest-rate-sensitive assets, will be crucial in the near future. Create your live VT Markets account and start trading now.Since President Trump’s term began, WTI Crude Oil has faced resistance at $64 for several reasons.

WTI crude oil has dropped below $62.00 per barrel. The rising supply levels reported by the Energy Information Administration (EIA) are putting pressure on prices.

Oil prices have struggled since Donald Trump became president. Concerns about a recession, an increase in global supply, and a weaker US Dollar have added to the challenges. Last year, prices were supported by strong demand after the pandemic and limited supply.