HCOB Manufacturing PMI for the Eurozone drops to 48.4, missing expectations of 49.3

The Eurozone’s HCOB Manufacturing PMI dropped to 48.4 in May, missing the expected 49.3. This signals a decline in business activity in the private sector.

The EUR/USD remains above 1.1300, but the weak PMI data suggests that the Euro may not gain much. On the other hand, the UK’s S&P Global Composite PMI rose to 49.4 in May from 48.5 in April.

In May, Germany’s HCOB Manufacturing PMI reported a figure of 48.8, which was below expectations.

In May, Germany’s HCOB Manufacturing PMI was 48.8, slightly lower than the expected 48.9. This small difference shows a slight dip in manufacturing performance during this time.

The PMI is an important measure of the health of Germany’s manufacturing sector. A PMI below 50 usually indicates a decline, while a figure above 50 suggests growth.

Challenges in Manufacturing

The PMI result hints at challenges or a slowdown in the manufacturing industry. It suggests that production levels or business conditions might be worse than expected. Such metrics are closely watched to understand economic trends and to inform future business or policy decisions. Even though the difference is small, it still reflects the current state of the sector. Even though May’s reading was just 0.1 below the forecast, it’s significant when considered in context. The 48.8 score keeps Germany’s manufacturing PMI below the 50 mark for another month, reinforcing the idea that the sector is still in decline. While not a drastic change, consistently low numbers indicate that activity remains sluggish, despite hopes for a rebound.Investor Sentiment and Market Impacts

For traders in interest-sensitive assets or short-term index products, this suggests that investor sentiment toward the eurozone’s manufacturing base is weak. Although the contraction isn’t worsening quickly, it also isn’t improving, which becomes increasingly important over time. We should also consider how central banks interpret these numbers. A small miss usually doesn’t change monetary policy views on its own, but repeated underperformance—even if slight—can strengthen dovish expectations or delay any changes in tone from officials. Combined with low inflation readings and upcoming consumer sentiment reports, this could lead to cautious positioning ahead of central bank meetings. Traders with bets on a recovery in European manufacturing may need to reduce their positions or tighten risk controls, as indicators aren’t giving a strong basis for confidence. For options strategies, implied volatility could provide more opportunities than directional bets in this current climate. Looking at the situation more closely, the manufacturing sector’s ongoing difficulty crossing the 50 threshold decreases confidence in short-term domestic demand growth from industrial producers. While export-focused companies have some flexibility, the domestic downturn affects purchasing and hiring, impacting GDP more broadly. We should also watch for supply chain remarks in the July PMI reports. Any rise in delivery times or price pressures amid declining output could indicate deeper issues rather than just temporary weakness. This adds another layer of complexity for traders, especially when analyzing long-term interest rate futures. Timing market entries is crucial. With German output soft but not collapsing, traders looking for direction might find more clarity from incoming orders or Q2 corporate earnings than from the overall PMI numbers. Although the PMI slipped slightly below expectations, its continued position below 50 suggests stagnation rather than volatility. This slower pace can lead to dullness in some derivatives markets unless triggered by unexpected events or policy changes. Overall, the slight miss is less a one-time occurrence and more of a sign of ongoing macro conditions, such as low growth, shaky momentum, and cautious investor sentiment. Create your live VT Markets account and start trading now.Notification of Server Upgrade – May 22 ,2025

Dear Client,

As part of our commitment to provide the most reliable service to our clients, there will be maintenance this weekend.

Maintenance Details:

Please note that the following aspects might be affected during the maintenance:

1. The price quote and trading management will be temporarily disabled during the maintenance. You will not be able to open new positions, close open positions, or make any adjustments to the trades.

2. There might be a gap between the original price and the price after maintenance. The gaps between Pending Orders, Stop Loss, and Take Profit will be filled at the market price once the maintenance is completed. It is suggested that you manage the account properly.

The above data is for reference only. Please refer to the MT4/MT5 software for the specific maintenance completion and marketing opening time.

Thank you for your patience and understanding about this important initiative.

If you’d like more information, please don’t hesitate to contact [email protected].

US Dollar recovery leads to a drop in the Australian Dollar’s recent gains

The Australian Dollar (AUD) is slightly up against the US Dollar (USD) but has pulled back from earlier gains. This comes after the release of Australia’s initial S&P Global Purchasing Managers Index (PMI) data.

In May, Australia’s Manufacturing PMI stayed at 51.7. However, the Services PMI dropped from 51.0 to 50.5, and the Composite PMI fell from 51.0 to 50.6. The Reserve Bank of Australia reduced the Official Cash Rate by 25 basis points to handle inflation and indicated they might take further action if needed.

US Dollar Index Performance

The US Dollar Index has declined for the fourth consecutive session and is trading around 99.50. Investors are looking ahead to the S&P Global US PMI data, expecting stable growth in business activity for May. There are ongoing developments in US politics and the economy. A tax-cut bill from President Trump is waiting for a House vote, amid economic concerns raised by the Cleveland and San Francisco Fed Presidents. The Atlanta Fed President warned about issues with trade logistics. Moody’s recently downgraded the US credit rating, predicting federal debt to rise by 2035. US economic indicators show inflation easing, with both CPI and PPI revealing reduced price pressures. This has led to hopes for interest rate cuts in 2025. Weak Retail Sales numbers have heightened worries about a prolonged economic slowdown. China criticized the US’s chip export measures, labeling them protectionist. The People’s Bank of China lowered Loan Prime Rates to support the market. Meanwhile, in Australia, the Labor Party regained power after the coalition collapsed.Australian Dollar Against Other Currencies

The AUD/USD pair is currently around 0.6440, with support from technical indicators positioned above important moving averages. Resistance levels are seen at 0.6515 and 0.6687, while support is located at 0.6427 and 0.6367. A drop below these levels could challenge the March 2020 low of 0.5914. Against other currencies, the AUD performed best against the New Zealand Dollar, while its performance was mixed against the USD, EUR, and CAD. The S&P Global Composite PMI data, based on surveys of executives, serves as an indicator of US private business activity. Traders are keenly awaiting upcoming data to understand market trends. Today’s market shows the Australian Dollar holding on to a small portion of earlier gains against the US Dollar after the PMI figures. The Manufacturing sector has remained steady, but Services and Composite numbers have slightly decreased. These modest changes suggest a slight loss of momentum in Australia’s economy, which might be concerning for those investing in growth-sensitive assets. The Reserve Bank’s decision to cut the Official Cash Rate by 25 basis points reflects their concerns about ongoing price pressures. Their message indicates that further reductions could happen if inflation remains a problem. For investors, this introduces the chance of further support for risk assets, while also raising the risk of a deeper economic slowdown if demand falls too quickly. On the other hand, the US Dollar is under pressure, having dropped for a fourth session. The Dollar Index dipping towards 99.50 shows a decreasing appetite for safe-haven assets due to softer inflation data. Lower Consumer and Producer Price Index figures suggest easing cost pressures, which supports speculation that the Federal Reserve might cut rates in 2025. The focus now shifts to upcoming US PMI numbers. If these figures show steady output from private companies, it could alleviate fears of contraction but also challenge expectations for rate cuts. Adjustments may be needed based on any positive surprises that could strengthen the Dollar and alter positioning, especially for those with a short USD bias. In Washington, discussions around former President Trump’s tax policies continue, adding uncertainty to the near-term outlook. Concerns have been raised by multiple Federal Reserve branch executives about ongoing economic challenges, particularly from the Cleveland and San Francisco Fed Presidents. The Atlanta Fed President has pointed out disruptions in transport channels. These issues contribute to uncertainty and may increase market volatility. Additionally, structural debt concerns remain, with Moody’s downgrade of US sovereign credit highlighting long-term fiscal risks. In Asia, tensions have escalated again. Beijing has accused Washington of limiting technological competition through chip export controls, keeping traders on edge in tech-related sectors. The People’s Bank of China has reduced its Loan Prime Rates to support domestic credit markets, providing relief to struggling areas of the economy. This introduces another loose policy element into the macro mix, affecting cross-border flows. Back in Australia, political shifts have brought the Labor Party back to power after a coalition collapse, adding another layer of uncertainty around fiscal priorities and regulations. While this is not currently moving markets, it could influence sentiment depending on future policy signals. Currently, the AUD/USD trades near 0.6440, supported by momentum indicators and remaining above short-term moving averages. Resistance is fairly close at 0.6515 and extends to 0.6687. A sustained dip below minor support levels at 0.6427 or 0.6367 could lead to prices not seen since early 2020. Heightened global risk aversion could increase this pressure quickly. Of note with other currencies, the Aussie has strengthened most notably against the New Zealand Dollar, while its performance has been mixed against the USD, EUR, and CAD. Differences in policy directions, especially between central banks, may influence price action in the upcoming weeks. Observing forthcoming releases, particularly those related to services and labor markets, is crucial, as these may provide a clearer outlook than manufacturing data. Moving forward, timing and execution will be key. Liquidity could thin out before significant macroeconomic updates, raising the likelihood of sharp intraday movements. While sentiment currently favors softer US data supporting the carry trade, this support relies on mild inflation and labor figures. Our focus is clear—monitor rates, follow policy discussions, and stay adaptable as technical levels come into play. Create your live VT Markets account and start trading now.Here are the FX option expiries for the NY cut at 10:00 AM Eastern Time.

Investment Risks in Open Markets

The markets and instruments mentioned here are for information only; no recommendations are being made. It’s crucial to do your research before making any investment decisions. Be aware that investing in open markets comes with risks, including the possibility of losing your entire investment. As we approach the expiration date on May 22, we may see increased volatility around key price levels, especially in major currency pairs where large options are about to expire. These levels can act like magnets, drawing spot prices closer as positions are adjusted. In the case of EUR/USD, there is a significant interest of 2.1 billion euros at the 1.1175 level, which is much larger than the usual daily expirations. Such high volume can create a gravitational pull on prices if they trade near this level, especially when traders are adjusting their risks. If the price moves toward 1.12, we could see additional resistance or support depending on market flows. The higher level at 1.1400 has a 751 million euro interest as well, but it has less impact unless strong price movements occur leading into the expiration.Recognizing Positioning Pressure

Sterling traders should keep an eye on the 778 million GBP set to expire at 1.3260. This level is slightly above current market prices, suggesting that a slight upward movement may happen, especially in a bullish market. The same logic applies to the yen market. Although the 601 million USD at 143.50 isn’t overly significant, it can still provide resistance or support if prices move up. The situation with USD/CHF looks different. The 598 million around 0.8525 could offer minor technical resistance, but it doesn’t have the volume needed to be a strong attractor. It’s worth considering, especially on days with low liquidity. For AUD/USD, while the volumes of 204 million and 286 million AUD are lower compared to other pairs, the range between 0.6100 and 0.6700 is important. The lower end may serve as a support level during risk-off periods, while reaching the higher level of 0.6700 will likely require major economic changes. That upper level is currently out of reach without a significant market impulse. Create your live VT Markets account and start trading now.Gold prices rise in Pakistan today, according to the latest data.

**Gold Prices and Global Market Influences**

Gold prices in Pakistan rose on Thursday to 30,269.47 Pakistani Rupees (PKR) per gram, up from 30,073.52 PKR on Wednesday. The price per tola increased to 353,058.20 PKR from 350,771.70 PKR.

The US House of Representatives is advancing President Trump’s tax and spending bill, which could add $3 trillion to $5 trillion to the national debt. Recent treasury bond auctions showed low demand, raising concerns about the growing US budget deficit.

Moody’s downgraded the US credit rating, causing the US Dollar to weaken. This contributed to higher gold prices. Global tensions, including US-China trade relations and ongoing conflicts, increased demand for gold.

Central banks are significant buyers of gold as they aim to strengthen their economies. In 2022, they added 1,136 tonnes of gold, worth around $70 billion, to their reserves.

Gold prices are influenced by geopolitical events, currency values, and interest rates, since gold is priced in US Dollars. Changes in the Dollar can inversely impact gold prices.

**Impact of Market Instability on Gold Prices**

The recent rise in gold prices—from 30,073.52 PKR to 30,269.47 PKR per gram and nearly 2,300 PKR per tola—reflects overall global market trends rather than issues specific to Pakistan. This trend suggests a deeper story; as gold rises, the US Dollar weakens, highlighting global economic factors at play.

The tax and spending bill advancing in the House has raised concerns, as it may increase US debt by up to $5 trillion. This, along with poor demand in treasury bond auctions, has made the market more cautious. Bond traders are reacting to the growing debt and uncertain fiscal policies, leading to a reevaluation of their US-backed asset investments.

Moody’s downgrade of the US credit rating reinforces this caution. Such downgrades signal that fiscal discipline is lacking, which decreases the appeal of Dollar-denominated assets and contributes to the Dollar’s decline. When the Dollar weakens, gold tends to increase, which is a pattern traders consistently watch.

Geopolitical tensions also continue to rise. While there are signs of cooperation between the US and China, dependable stability remains elusive, and other conflicts persist. This uncertainty encourages increased gold buying, motivated not just by speculative reasons but also for protection. Both retail investors and central banks are driving this demand.

Central banks, in particular, have made significant moves. Adding 1,136 tonnes of gold in one year indicates a strategy to guard against currency risk and inflation. Institutions are responding to the same economic indicators as traders—credit quality, fiscal policy, and political stability—by accumulating gold for the long term.

So, where do we stand? With bonds losing appeal and the Dollar facing potential further weakening, gold appears to be a wise choice—not as a sign of excitement but as a safe haven. This situation prompts options traders to monitor implied volatility levels on metals and adjust strike positions, especially for US-denominated assets. Premiums might shift due to macro hedging efforts, especially if central banks remain active.

The yield curve is also important to consider. An inverted yield curve paired with a weakening Dollar makes precious metals attractive for rate-sensitive investments. Keep an eye on growing open interest near critical resistance levels in gold; a price increase without solid support could indicate instability instead of ongoing strength.

In conclusion, these events are interconnected and present a clear narrative regarding US fiscal policy and global reactions to instability. The responses in the gold market are insightful, and adjusting derivative strategies will be necessary to navigate conditions that are unlikely to change in the short term.

Create your live VT Markets account and start trading now.

New Zealand announces NZ$4 billion increase in bond program over four years, says Willis

New Zealand’s Budget predicts a deficit of NZ$-14.74 billion for 2024/25 and NZ$-15.60 billion for 2025/26. Net debt is expected to be 42.7% of GDP in 2024/25, with a projected cash balance deficit of NZ$-9.99 billion.

For 2024/25, GDP is estimated to drop by 0.8%, but a recovery is expected in 2025/26 and 2026/27, with growth rates of 2.9% and 3.0% respectively. Inflation is projected to stay within the 1% to 3% target band for the next five years.

Currency Reaction

The New Zealand Dollar has barely reacted to the budget news, trading 0.25% lower at around 0.5925. The government does not expect to see an operating balance surplus in the next five fiscal years, and trade tariffs remain influential on how quickly the economy can recover. Although the deficit figures may seem alarming—especially with a deeper deficit forecast for 2025/26—the government is prioritizing fiscal support over spending cuts. The projected 0.8% GDP contraction next year reflects this broader borrowing strategy which favors economic stimulus. Despite these challenges, core inflation remains steady. The forecast keeps inflation within the 1% to 3% band, indicating that price stability is not currently at risk. This allows monetary policy to stay stable without needing an immediate response. As the government increases bond issuance, funding costs may rise, but the Reserve Bank doesn’t need to react aggressively right away. The currency’s slight dip suggests that the market was prepared for these projections. The Kiwi dropped only 0.25%, indicating that investors are becoming more accustomed to deficit announcements when inflation and growth seem stable. This indicates a calm response regarding interest rates and currency fluctuations.Trade and Interest Rates

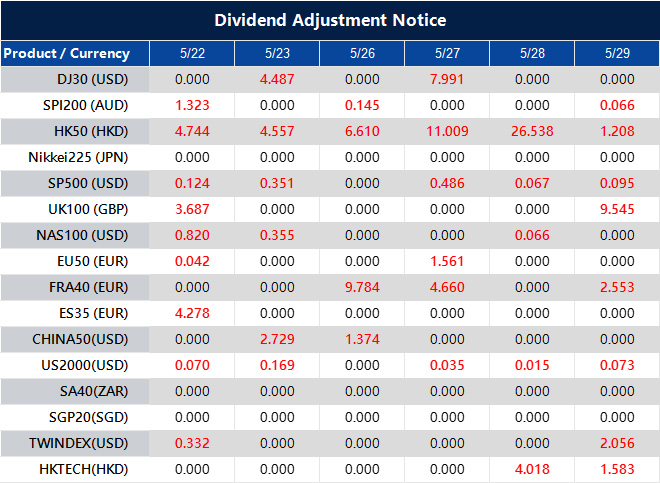

The balance of risks largely depends on timing. While the multi-year recovery looks promising from 2025 onward, the current economic downturn will impact interest rates. Expect the yield curve to remain relatively flat over the next two quarters, especially if international factors remain subdued. It’s essential to analyze future expectations. Export tariffs continue to impede predicted trade growth, which adds uncertainty to the recovery but is less affected by domestic policies. Positions that consider a slow or uneven improvement in trade balances may perform better than fixed growth expectations. Short-term interest rate trades may stay stable unless the Reserve Bank changes its approach sooner than anticipated. However, for longer-term rates, any increase in bond issuance could widen spreads, especially during periods of weaker GDP. We are focusing on how interest rates in New Zealand compare to global benchmarks, noting how the budget plan aligns with monetary policy. For those trading volatility, a stable inflation outlook suggests limited upward movement in break-evens and inflation swaps in the short to medium term. However, with growing deficits and borrowing needs, concerns about sovereign credit can arise intermittently. Option pricing might remain low, but could rise if debt issuance outpaces market absorption. Robertson’s budget figures did not significantly impact the Kiwi, but the ongoing debt dynamics and changing long-term growth rates create opportunities—especially as policy differences emerge. Be cautious with long Kiwi positions during global rate changes or demand shocks. The real challenge will be watching whether the anticipated bounce in 2025/26 overcomes initial hurdles or if downward revisions threaten the projected 3% growth targets. Create your live VT Markets account and start trading now.Dividend Adjustment Notice – May 22 ,2025

Dear Client,

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

Asahi Noguchi, a BoJ board member, notes Japan’s economy is steadily growing and may require policy adjustments.

The Bank of Japan (BoJ) has noted that Japan’s economy is growing steadily, with possible changes to policy rates on the horizon. The central bank is closely monitoring if inflation remains stable at around 2%, emphasizing the importance of sustainable inflation and rising wages.

Recently, the economy faces external risks due to increasing pressures from international tariff policies. In March, the yield on the 10-year Japanese Government Bond was close to 1.6%. The BoJ intends to maintain its loose monetary policy because the primary cause of inflation stems from rising import costs.

Monetary Policy Overview

Japan’s current monetary policy includes Quantitative and Qualitative Easing, a strategy that began in 2013 to help boost inflation. Negative interest rates and yield control were introduced in 2016, leading to a shift in 2024 when interest rates increased. This change caused the yen to weaken, prompting policy adjustments as inflation surpassed the 2% target. The BoJ’s policy adjustments reflect concerns about the yen’s weakness and rising global energy prices. Wage increases are crucial for sustaining inflation, which influences the BoJ’s considerations regarding its previously established ultra-loose policy. The USD/JPY exchange rate was at 143.30, showing recent market trends. Policymakers in Tokyo now believe the economy is growing steadily. The focus is on whether domestic price trends, especially underlying inflation, can consistently stay around 2% without external boosts. The emphasis is on wage growth to support consumer spending and create stable inflation. Any changes to interest rates will likely be gradual and based on improved wages across various industries. External factors, including tariff changes and global political conditions, may still affect prices negatively. Japan, as a significant energy importer, is notably vulnerable here. In March, rising yields on government debt close to 1.6% indicated that markets are preparing for tighter conditions, even if policy hasn’t shifted entirely yet. This suggests that they are anticipating persistent inflation before adjusting further. Since 2013, the BoJ has injected funds into the economy through aggressive asset purchases—both quantitative and qualitative. This approach included deeply negative rates and yield curve control starting in 2016. These measures were aimed at addressing ongoing shortfalls in inflation targets. As we move into 2024, rising interest rates became necessary, especially as consumer prices exceeded the Bank’s target. This shift was driven not just by inflation but also by the yen’s significant decline against the US dollar.Implications for Derivatives Markets

For those in the derivatives market, changes in Japan’s monetary policy have several immediate effects. Pricing options or futures related to JGBs or FX pairs like USD/JPY now requires monitoring not only policy statements but also labor data. If wage figures suggest strong consumption growth, sharp movements in the yen could signal the likelihood of higher rates. As the BoJ’s approach gradually changes, derivative trades on rate-sensitive instruments should consider various scenarios—some where inflation slows down and others where wage growth propels it. The transition won’t happen suddenly, but it is in progress. Traders need to incorporate these developments, considering how companies might respond to expected cost rises. We have observed the yen reacting strongly during past tightening cycles, even minor ones. Monitoring 10-year yields and their impact on rate differentials with the U.S. may help timing decisions for currency contracts. The forward market typically adjusts prices faster than spot traders may anticipate. Experience shows that BoJ policy moves are cautious yet impactful. Statements regarding wage conditions or inflation expectations should be viewed as directional indicators. Thus, option positions may benefit from broader implied volatility bands as the market reflects on data uncertainties. In the coming weeks, interest in inflation reports and wage negotiations, especially among Japan’s larger companies, is expected to grow. Any sign that these metrics are holding steady—even slightly—may support policy changes. When market consensus leans strongly in one direction, it could create contrarian timing opportunities in rates and currency markets. Currently, the tone is one of caution but also readiness to act. This dual perspective is where traders can find an advantage. Carefully timing rate exposure while staying responsive to wage and consumer behavior will likely yield better results than static positions. Create your live VT Markets account and start trading now.PBOC sets the USD/CNY central rate at 7.1903, lower than before

The People’s Bank of China (PBOC) has set the USD/CNY central rate at 7.1903 for the latest trading session. This is slightly lower than the previous rate of 7.1937 and also lower than the expected rate of 7.2009 predicted by Reuters.

The PBOC aims to keep prices and exchange rates stable while supporting the economy. It is owned by the People’s Republic of China and overseen by the Chinese Communist Party Committee Secretary.