Gold edges above $5,050 as US-Iran tensions linger despite strong jobs data, with markets awaiting the CPI release

Gold traded slightly higher near $5,060 in early Asian trading on Thursday, holding above $5,050. It rose even after strong US jobs data. Traders are now focused on Friday’s US CPI inflation report.

Safe-haven demand supported gold as tensions between the US and Iran continued. Donald Trump said he wants talks with Iran to continue after meeting Benjamin Netanyahu. He also warned he may act against Tehran if no nuclear deal is reached.

In January, the UK’s RICS house price balance beat forecasts, reaching -10% versus -11% expected

The Royal Institution of Chartered Surveyors (RICS) UK house price balance for January was **-10%**. This was slightly better than expectations of **-11%**.

A negative balance means more survey respondents reported house prices **falling** than **rising**. The figure is still within the forecast range.

Uk Housing Downturn Shows Signs Of Stabilizing

January’s housing data is still negative, but it suggests the UK property downturn is starting to lose pace. The **-10%** reading is a clear improvement versus expectations and may signal that the worst of the price correction seen through 2025 is now behind us. That lowers the risk of a major economic shock coming from housing. This is supportive for the British Pound. If the housing market is holding up, the Bank of England has less pressure to deliver large rate cuts. With inflation still sticky and ending last year at **2.9%**, this report gives the BoE more room to keep rates on hold. One approach could be buying **GBP call options** versus currencies where central banks look more dovish. Rate markets may also be pricing the timing and size of future cuts too aggressively. The sharp hiking cycle of 2023–2024 is over, but a steadier housing market points to a slower, more cautious easing path. Selling **short-term interest rate futures** could be one way to position for the BoE staying cautious longer than markets expect. There may also be opportunities in UK equity derivatives, especially those linked to domestic sectors such as **housebuilders** and **banks**. This upside surprise, along with Bank of England data showing **mortgage approvals rising for three straight months**, could help re-rate the sector. In the coming weeks, it may be worth considering **call options on a home construction ETF** or exposure to the more UK-focused **FTSE 250** via futures or options.Potential Positioning Across Rates Fx And Equities

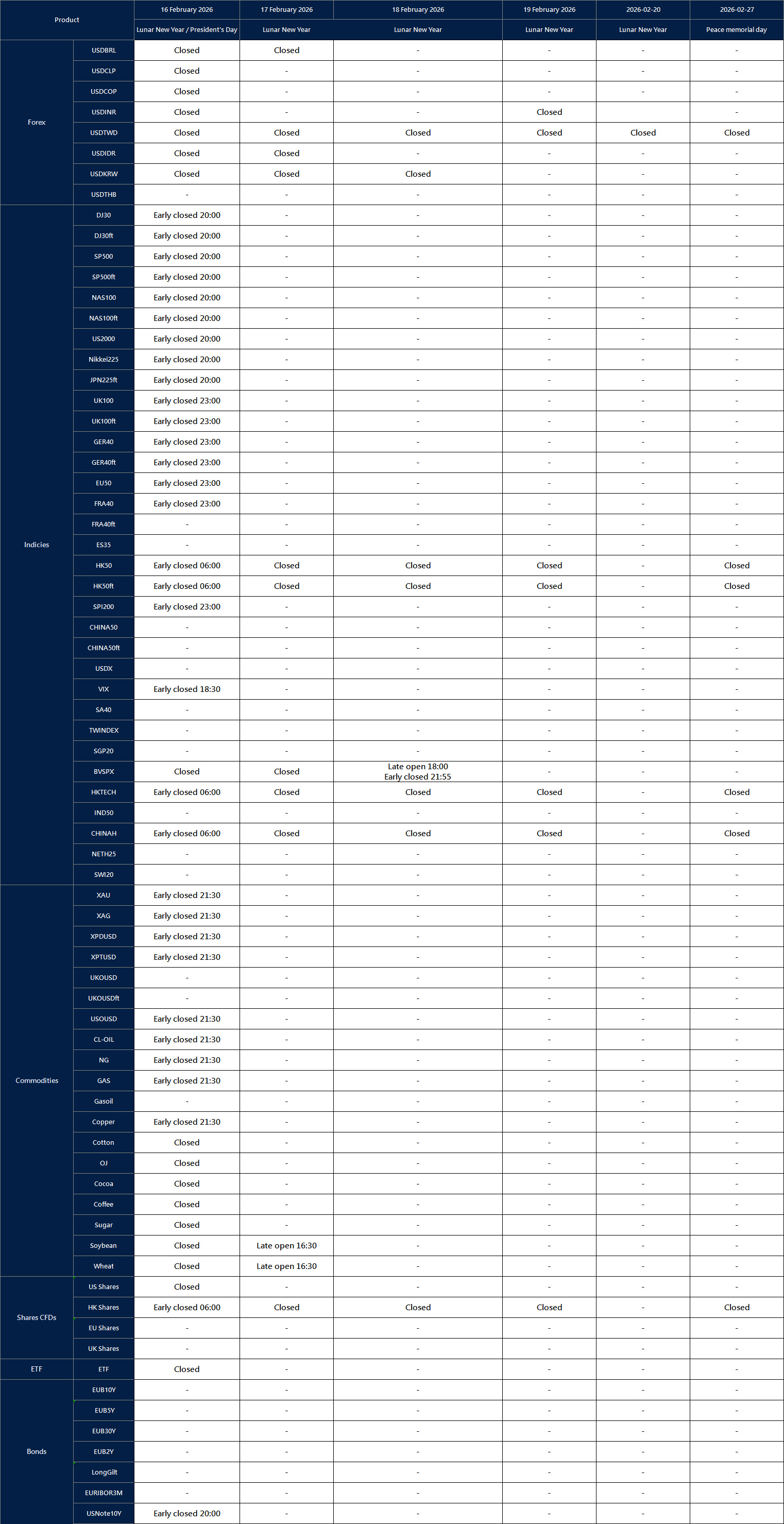

Create your live VT Markets account and start trading now.Holiday Trading Adjustment Notice – Feb 12 ,2026

Dear Client,

Affected by international holidays, the trading hours of some VT Markets products will be adjusted. Please check the following link for the affected products:

Holiday Trading Adjustment Notice

Note: The dash sign (-) indicates normal trading hours.

Friendly Reminder:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

Before the session, sterling pulled back from multi-year highs amid a dovish BoE stance and UK political uncertainty

Sterling slipped slightly on Wednesday after hitting four-year highs. The move came as the Bank of England (BoE) sounded more dovish and UK politics added uncertainty. The BoE held rates, but the Monetary Policy Committee (MPC) vote split 5-4, with four members calling for an immediate 25 basis point cut.

The BoE said inflation could reach 2% sooner than expected. Markets are now pricing in 50 basis points of rate cuts in 2026. UK politics also drew attention after Anas Sarwar called on Prime Minister Keir Starmer to resign over the Peter Mandelson scandal, although later support from the cabinet helped calm the situation.

Thursday brings the UK’s preliminary GDP data for Q4 2025. Consensus expects 0.2% quarter-on-quarter (up from 0.1% in Q3) and 1.2% year-on-year (down from 1.3%). December industrial and manufacturing production figures are also due. These releases follow the BoE’s decision to cut its 2026 GDP forecast to 0.9% from 1.2%.

On Friday, MPC member Pill is scheduled to speak, and the delayed US January CPI report is due. Headline inflation is expected at 2.5% year-on-year, with core inflation seen at 0.3% month-on-month. GBP/USD traded at 1.3627, down 0.12%, below 1.3869 but above the 50-day EMA (1.3516) and 200-day EMA (1.3312).

Support is seen at 1.3585 to 1.3620, then 1.3516 and 1.3380 to 1.3400. Resistance is at 1.3735 and 1.3869. The Stochastic Oscillator (14, 5, 5) read 47.10/52.91.

The latest BoE meeting has created real uncertainty. The 5-4 vote, with four members pushing for an immediate cut, signals a clear dovish shift. That shift is now weighing on Sterling. This makes trading harder because the weaker Pound is moving against a US Dollar that is also starting to soften.

With UK GDP for the final quarter of 2025 due today, we should be ready for a downside surprise, especially after the BoE lowered its 2026 growth forecast. One-week implied volatility in the options market has already risen above 8%, showing that traders expect a sharp move after this release and tomorrow’s US inflation data. With volatility this high, holding a simple directional trade carries extra risk.

Because the upcoming data could lead to a big move either way, a long-volatility trade such as a straddle may make sense. This would benefit from a large move in either direction, whether driven by a weak UK GDP result or a softer US CPI print. The goal is to capture a breakout, not to guess the direction.

Another approach is for those who think support near 1.3600 will hold. In that case, selling put options with a strike below 1.3550 could generate income. A similar pattern appeared in late 2023: the UK fell into a technical recession, but the currency still found a floor. However, if price breaks below support in a clear way, buying puts becomes a better hedge against deeper losses.

Over the next few weeks, the market pricing of 50 basis points of cuts in 2026 will likely limit any major Sterling rally. If Pill sounds more hawkish on Friday, markets may reassess in the short term, but the broader dovish pressure remains. For that reason, we should be careful about chasing GBP/USD strength above 1.3800.

Near multi-month highs, the New Zealand dollar stays firm against the US dollar after payroll data revisions overshadow job gains

NZD/USD stayed near multi-month highs on Wednesday and remained bullish into the second half of the week. The US Non-Farm Payrolls report showed 130K jobs added in January versus a 70K forecast. However, an 898K downward benchmark revision to 2025 payroll data weighed on the US Dollar.

The Federal Reserve kept rates at 3.50% to 3.75% at its January meeting, and markets are pricing in two cuts this year. In New Zealand, the Reserve Bank of New Zealand is expected to hold the Official Cash Rate at 2.25% on 18 February. The bank has already delivered six cuts through 2025, taking rates from 5.50% to 2.25%.

Key Data And Central Bank Focus

Inflation is near the top of the 1% to 3% target band. Key releases ahead include the Business NZ PMI for January on Thursday and RBNZ Inflation Expectations for Q1 on Friday. Friday also brings the US CPI for January. Consensus is 2.5% year-on-year for headline CPI and 0.3% month-on-month for the core reading. On the daily chart, NZD/USD was at 0.6051, up 0.10%, and just below resistance at 0.6094. The pair is above the 50-day EMA at 0.5881 and the 200-day EMA at 0.5833. It has been consolidating between 0.5960 and 0.6094, with a November low near 0.5580. NZD/USD is holding near 0.6050 and consolidating after a strong rally. The main driver is a weaker outlook for the US labour market, reinforced by the 898,000 downward revision to 2025 job numbers. Weekly initial jobless claims around 220,000 also support the view that the US economy is cooling. The main theme for the coming weeks is policy divergence between the Federal Reserve and the Reserve Bank of New Zealand (RBNZ). The Fed is widely expected to cut rates at least twice more this year. In contrast, the RBNZ faces firmer inflation pressures at home. With New Zealand’s Q4 2025 inflation still high at 4.7% year-on-year, the RBNZ is likely to keep its cash rate unchanged at 2.25% at the 18 February meeting. The Kiwi is also supported by stronger dairy prices, a key New Zealand export. The Global Dairy Trade Price Index has risen in four of the last five auctions, which can help improve New Zealand’s trade balance. This contrasts with broad pressure on the US Dollar as markets price in more Fed easing.Strategy And Risk Management

For derivatives traders, this setup suggests positioning for a possible upside break in NZD/USD. Buying call options with strike prices above the key 0.6094 resistance could offer exposure to a move toward 0.6150 and 0.6200. However, US CPI on Friday is a key risk. A hotter-than-expected inflation print could trigger short-term volatility and support the US Dollar. Risk management matters because the pair has been ranging for about a week. A sustained break below support at 0.5960 would suggest bullish momentum is fading, and could open a pullback toward the 0.5880 area. Traders may use these levels to set stop-loss orders, or consider put options to hedge against a downside reversal. Create your live VT Markets account and start trading now.After Takaichi’s landslide win, the yen strengthens, pushing USD/JPY toward 153.20 despite strong US jobs data

USD/JPY slipped to around 153.20 in early Asian trading on Thursday, as the Japanese Yen strengthened above 153.00. The move followed Prime Minister Sanae Takaichi’s landslide election win, while markets waited for Friday’s US CPI inflation report.

Traders also bought Japanese equities on hopes for consumer support and new measures to help Japanese firms. That demand lifted the Yen and pushed USD/JPY lower.

Dollar Data Limits Downside

US data helped limit the Dollar’s losses. January Nonfarm Payrolls rose by 130,000, beating the 70,000 forecast. This followed a revised 48,000 gain in December (previously 50,000). The Unemployment Rate dipped to 4.3% in January from 4.4% in December. After the release, markets priced in a 94% chance the Federal Reserve will keep rates unchanged at its next meeting, up from 80% the day before, according to CME FedWatch. Right now, USD/JPY is being pulled in two directions. Optimism around the new Takaichi administration is supporting Japan’s outlook and strengthening the Yen, which drags the pair lower. At the same time, strong US jobs data lowers the odds of a Fed rate cut, which supports the Dollar. This optimism is showing up in market flows. Foreign buying of the Nikkei 225 last week hit its highest level in more than six months. Rising demand for Japanese assets is a key reason the Yen is firming, as traders position for stronger domestic growth under the new leadership.Options Markets Signal Volatility

On the US side, the surprise 130,000 job gain and the unemployment dip to 4.3% have strengthened the view that the Fed will keep rates steady. CME FedWatch now shows a 94% probability of no change at the next meeting. For derivatives traders, this push-and-pull ahead of Friday’s inflation data points to higher volatility. One-week implied volatility on USD/JPY options has already moved above 12%, the highest since the Bank of Japan policy meetings in late 2025. This suggests the market is preparing for a large move, making swing-focused strategies like straddles more appealing. The US CPI report is the near-term catalyst that could break the stalemate. A hotter-than-expected CPI reading would support a more hawkish Fed outlook and could send USD/JPY sharply higher. A softer CPI print would likely weaken the Dollar and allow the Yen’s political tailwind to push the pair further below 153.00. It is also worth remembering what happened the last time USD/JPY traded around these levels in late 2022, when the Ministry of Finance intervened directly. While the new government’s approach is not yet clear, the history of intervention above the 150–152 area is a major risk for traders betting on continued Yen weakness. This backdrop should be considered when holding long USD/JPY positions. Create your live VT Markets account and start trading now.AUD/USD hits its highest level since August 2022 as US payrolls beat forecasts, despite major downward revisions to 2025 data

AUD/USD hit its highest level since August 2022 on Wednesday. The move followed the delayed US Non-Farm Payrolls report, which showed 130K jobs added versus a 70K forecast.

The report also showed major downward revisions. March 2025 payrolls were revised 898K lower. Average monthly job gains for 2025 were revised down to 15K from 49K.

Rba Policy Shift And Inflation Focus

In Australia, the Reserve Bank of Australia raised the cash rate by 25 basis points to 3.85% on 3 February. This followed a rise in inflation in the second half of 2025. Australian Consumer Inflation Expectations for February are due on Thursday. In the US, January CPI is due on Friday. Headline year-on-year CPI is expected at 2.5% (down from 2.7%), while core month-on-month CPI is expected at 0.3%. AUD/USD traded near 0.7130 on Wednesday, up 0.77%, after reaching an intraday high of 0.7143. The pair is above the 50-day EMA at 0.6810 and the 200-day EMA at 0.6616. The December low sits at 0.6466. AUD/USD has risen more than 600 pips from around 0.6700. The stochastic (14, 5, 5) is 86.24/79.19. Resistance is at 0.7143 and 0.7200, while support is at 0.7000 and 0.6930–0.7000. After this sharp rally, the market is pricing in a clear policy split: a more hawkish RBA versus a Federal Reserve facing signs of a softer US job market. The RBA’s rate hike to 3.85% on February 3 reinforces its focus on inflation. This backdrop supports further AUD strength against the USD in the weeks ahead.Commodity Tailwinds And Options Strategy Setup

External factors are also helping the Australian dollar. Iron ore futures have moved above $135 per tonne, a 19-month high. The jump is linked to renewed demand from China after the Lunar New Year holiday. As Australia’s key export, stronger iron ore prices can provide a meaningful boost for the currency. For traders who want to take advantage of the upside momentum, buying AUD/USD call options is a simple way to position for more gains toward the 0.7200 psychological level. This approach also limits downside risk to the premium paid. Even so, caution is needed ahead of Friday’s US CPI release. A hotter-than-expected inflation print could quickly reverse the current move. With the stochastic already in overbought territory, a bull call spread may be a safer alternative. It reduces upfront cost and sets a clear risk-reward range before a potentially volatile data release. If you expect a small pullback before another push higher, 0.7000 is now a key support area. Selling put options with a strike below this level could be a way to earn income. This trade benefits if the pair stays above the strike through expiration, based on the view that any dip will be limited. In August 2022, when AUD/USD last traded around these levels, global central banks were at a different stage of their tightening cycles. The break above 0.7100 is important because it clears a multi-year range. If today’s drivers remain in place, the pair could move back toward the 2021–2022 commodity-boom levels, when it traded above 0.7400. Create your live VT Markets account and start trading now.Commerzbank’s Moses Lim: USD/MYR remains rangebound near multi-year lows as Malaysian industrial output stays strong

Malaysia’s industrial production rose 4.8% year on year in December. This was above the 4.5% Bloomberg consensus and up from 4.3% in November. Growth was driven by electronics and other export-focused manufacturing.

Mining output fell 5.2% year on year, after a 2.3% rise in November. This was the first contraction since May 2025. The drop was linked to lower natural gas production. A recovery is expected in 2026 as more facilities come online after maintenance ends.

Ringgit Strength And Trading Range

USD/MYR fell 0.3% to around 3.92 and stayed near its lowest level since July 2018. The move was supported by foreign inflows and strong semiconductor exports. In the near term, USD/MYR is expected to trade in a 3.90 to 4.00 range. The article was produced with an AI tool and checked by an editor. Data from December 2025 pointed to strong industrial production, and that trend appears to be continuing. The Malaysian ringgit has strengthened against the dollar, pushing USD/MYR to levels not seen since mid-2018. Markets expect the pair to stay in a tight 3.90 to 4.00 band in the near term. This view is supported by new data. January trade figures, released last week, showed semiconductor exports rose 9.5% year on year, extending the strong performance from late last year. We also recorded net foreign inflows of $1.5 billion into the local bond market in January, which signals ongoing investor confidence.Volatility Strategies And Key Risks

With volatility expected to stay low, selling options may be attractive in the coming weeks. Short-dated strangles or iron condors with strikes outside the 3.90–4.00 range could benefit from time decay. One example is selling a 3.88 put and a 4.02 call. This strategy depends on the exchange rate staying within the range and avoiding major breakouts. Looking back at 2018, the last time the pair traded at these levels, it found strong support around 3.85–3.90 for several months. One risk to watch is the mining sector. If it rebounds as expected, it could add support to the ringgit and push USD/MYR toward the lower end of the range. Another key risk is a sudden rise in global risk aversion, which could lift the dollar and break above 4.00. For investors seeking yield, range accrual notes are another option. These products pay a higher coupon for each day USD/MYR closes within the 3.90–4.00 band. This matches the view that the currency will remain stable in the weeks ahead. Create your live VT Markets account and start trading now.INGING expects weak CPI to stay below 2% through 2026, allowing the PBOC to continue easing

ING expects China’s inflation trend to have only a small impact on People’s Bank of China (PBOC) policy in 2026. It expects the inflation target announced at the Two Sessions in March to be around 2% year-on-year, unchanged from 2025.

ING forecasts CPI inflation will again come in below the 2% target, as it has in recent years. It notes the target has mainly been used to limit inflation on the upside, not to lift inflation from low levels.

Inflation Target Likely Not A Constraint

Because of this, ING expects a CPI miss on the downside will not limit monetary policy. It says the PBOC is more likely to focus on broader economic conditions and the possible impact on banks and markets. ING also says recent soft domestic data supports further easing. It sees room for an initial move in the first half of 2026, including a 10bp rate cut and a 50bp Reserve Requirement Ratio (RRR) cut. With inflation likely to undershoot the 2% target again, ING sees few limits on monetary policy. Signs of a weak finish to 2025, along with January CPI of just 0.4%, strengthen the case for the PBOC to ease. The market should watch the Two Sessions in March for confirmation of economic targets, but the overall direction appears to be more support. This outlook could be positive for Chinese equities after a difficult 2025. Traders may consider buying call options on major stock indices such as the FTSE China A50 or the Hang Seng Index. This positions for a rebound that could be supported by extra liquidity in the first half of the year.Potential Trades Around Policy Easing

A rate cut would likely put downward pressure on the yuan. ING expects USD/CNY to move higher as the interest rate gap between China and the US widens. Buying call options on USD/CNY could be an appealing way to position for a weaker yuan in the coming weeks. For interest-rate traders, the chance of both a 10bp rate cut and a 50bp RRR cut supports a long position in government bonds. One way to do this is by buying Chinese government bond futures. A similar move happened after the last RRR cut in mid-2025, when bond prices rallied sharply and rewarded traders who were positioned early. Even before any decision, expectations of a policy move can lift short-term volatility. This can make options straddles on currency pairs or equity indices useful for trading a rise in market swings ahead of key PBOC announcements. Keep in mind that implied volatility often drops quickly once the policy decision is announced. Create your live VT Markets account and start trading now.Despite a 1% dip, AUD/JPY stays bullish as yen strengthens after Prime Minister Takaichi’s victory

AUD/JPY dropped more than 1% on Wednesday as demand for the Japanese yen jumped after Prime Minister Sanae Takaichi won a landslide election. At the time of writing, the pair was trading at 109.23.

The yen is also gaining support from expectations that the Bank of Japan may move toward policy normalisation, as well as the possibility that Japanese authorities could step in to support the currency in FX markets. The Nikkei Index has also climbed on speculation about more economic stimulus.

{kind=link}