Analysts Warren Patterson and Ewa Manthey note that nuclear discussions are affecting oil prices, leading to risk premiums for Brent and an increase in speculative net longs.

Constructive talks between the US and Iran regarding nuclear issues are currently impacting oil prices. However, uncertainty is keeping a risk premium in Brent crude oil. We’re seeing a rise in speculative net longs in ICE Brent, along with a bullish volatility skew.

Upcoming reports from the EIA, OPEC, and IEA may cause further changes in both Crude Oil and Brent benchmarks. Oil prices fell in early Asian trading after a positive outlook on these talks emerged.

This ongoing uncertainty prompts the market to consider a risk premium. Participants in the options market are preparing for a possible price increase, as shown by the bullish volatility skew in Brent.

Speculators are cautious about short-selling oil due to this existing uncertainty. Journalists report on expert market observations and insights from both internal and external analysts to capture this landscape.

This week, oil prices are softening as reports from Vienna suggest progress in US-Iran nuclear discussions. A potential deal could add over a million barrels per day back into the market, a significant bearish factor. Still, this downward pressure is met with a built-in risk premium in current Brent prices.

This nervousness is understandable, especially after last week’s EIA report, which revealed an unexpected crude draw of 2.1 million barrels, contrary to expectations of an increase. This follows the OPEC+ Joint Ministerial Monitoring Committee’s recommendation to maintain current production quotas through March, due to a fragile demand recovery in parts of Asia. These supply issues keep sellers cautious.

In the derivatives market, the tension is evident in recent positioning data, showing speculative net longs in ICE Brent have risen to a three-month high. The options market indicates a similar trend, with a pronounced bullish volatility skew, meaning traders are paying more for call options than for puts. This suggests they are more concerned about a sudden price spike than a gradual drop from a potential Iran deal.

Reflecting on the sharp price rally in the fourth quarter of 2025, when geopolitical tensions in the Strait of Hormuz increased, it’s clear why few want to short oil. In the coming weeks, this environment may favor strategies that take advantage of upward-moving volatility, such as bull call spreads. This strategy allows participation in a potential rally while defining risk in case the Iran news leads to a sudden price drop.

The S&P 500 might pull back before rising again, or it could keep going up.

The analysis looks at the current S&P 500 chart using the Elliott Wave structure. It explores whether a quick pullback is coming or if the momentum will push it to new highs. Two scenarios are considered: if wave C has ended or if another downturn is likely.

The session focuses on understanding the Elliott Wave flat structure, alternative wave counts, and potential downsides. It aims to provide scenario-based insights, guiding traders without exaggeration. Neerav Yadav, a skilled Futures trader with over ten years of market experience, shares knowledgeable perspectives that prioritize structure over hype.

Related content discusses various economic and market topics, including the rising silver price, Japan’s fiscal changes, and concerns regarding the GBP/USD. There’s also information on the best brokers for 2026, tailored to different regions and trading needs.

This content is for informational purposes only and does not claim to be infallible or always up-to-date. Readers should be aware of the risks involved with open markets and the importance of conducting their own research. The author emphasizes their independence and lack of compensation from any mentioned companies, taking no responsibility for investment decisions made based on this article.

We are at a crucial decision point for the S&P 500 after it crossed the 6200 level. The key question is whether the momentum can propel the index higher or if a brief pullback is necessary first. January’s CPI data, slightly lower than expected at 2.8%, is boosting optimism among buyers.

The case for a straight rally is supported by a Federal Reserve that seems to be maintaining its stance. The markets are pricing in a 60% chance of a rate cut by the third quarter of 2026. This favorable outlook encourages buying during any strength. For derivatives traders, this scenario suggests that short-dated at-the-money call options could keep performing well.

However, the market structure indicates that one more downward movement, a final C wave, might still happen before a steady rise to new highs. We recall the market behavior in the third quarter of 2025, where a quick correction shook out weaker investors before the year-end rally. A similar brief dip now could serve as a healthy consolidation.

This uncertainty is also evident in the options market, where the VIX sits at a low level of 14.5, indicating complacency. This makes protective puts relatively inexpensive for those looking to guard against a sudden drop. It also presents an opportunity to buy call spreads, which can profit from an increase while keeping initial costs low.

A cautious approach for the next couple of weeks is to manage these two possibilities. Consider using options to set your risk. You might buy call options with longer expirations to ride out any potential dip. Additionally, staggering your entries could be beneficial, allowing you to add to a bullish position at a better price if we see a minor pullback toward the 6100 support level.

Euro weakens against yen to nearly 185.55 after Japan’s ruling party victory

The EUR/JPY pair fell to around 185.55 during the early European session on Monday. This drop came after Japan’s ruling Liberal Democratic Party (LDP) won decisively in the lower house elections, which strengthened the Yen against the Euro.

Although the LDP achieved a supermajority—the largest in post-war Japan—this initially weakened the Yen. Concerns about Japan’s high public debt may continue to pressure the Yen, and plans to reduce the sales tax on food could complicate fiscal policy further.

European Central Bank Approach

The European Central Bank (ECB) has kept its interest rate steady at 2.0% for five meetings in a row. ECB President Lagarde highlighted a data-driven, meeting-by-meeting approach, consistent with economists’ predictions for stable rates through 2026. The Japanese Yen’s value is affected by several factors, such as the Bank of Japan’s policies and the differences in bond yields between Japan and the U.S. Historically, the Bank of Japan’s (BoJ) very loose monetary policy has led to Yen depreciation. However, recent adjustments to these policies have supported the Yen. During market stress, the Yen is seen as a safe haven, leading to increased demand. Broader market sentiment changes can significantly influence the Yen’s value against other currencies. The LDP’s substantial victory has strengthened the Yen in the short term, pushing the EUR/JPY rate toward 185.50. Traders reacted quickly to the expected outcome, and profit-taking boosted the Yen, illustrating a typical market reaction to confirmed news. This political stability provides a strong foundation for the Yen’s value in the near future.Impact of Bank of Japan Policies

This trend follows the Bank of Japan’s gradual shift away from its extremely loose monetary policy that began in 2024. This slow normalization has narrowed the interest rate gap that once heavily favored the Euro. This policy adjustment is crucial long-term support for the Yen. In contrast, the European Central Bank is likely to maintain its benchmark rate at 2.0%. With Eurozone inflation falling from peaks in 2023 to a more manageable 2.1% in January 2026, the ECB has little reason to change its strategy. This limits the Euro’s chance for a major rally. The main risk to a stronger Yen is Japan’s financial situation, which needs careful monitoring. With Japan’s debt-to-GDP ratio expected to exceed 260% by the end of 2025, the new government’s spending plans could unsettle bond markets. Any signs of distress in Japanese government bonds would serve as a major warning sign. For derivatives traders, selling into any rallies in the EUR/JPY pair might be a smart strategy in the coming weeks. Given the risks associated with Japan’s debt, buying puts on EUR/JPY may be a way to capitalize on further Yen strength while clearly limiting potential losses. The tension between Japan’s political stability and its fiscal issues will likely lead to market volatility, making options a beneficial tool. Create your live VT Markets account and start trading now.Concerns over the US-Iran conflict ease, leading WTI oil to trade around $62.70 per barrel

West Texas Intermediate (WTI) oil is currently around $62.50 as tensions between the US and Iran ease with new diplomatic talks. Both countries are continuing indirect negotiations about nuclear issues after positive discussions in Oman.

Indian refiners are choosing to avoid buying Russian oil that is scheduled for April. This decision aligns with India’s goal of securing a trade agreement with the US. Such choices may affect the global oil supply since the Strait of Hormuz is a key route for about 20% of the world’s oil shipments.

The Impact On WTI Oil Prices

WTI, a key indicator for oil markets, was trading around $62.70 per barrel early Monday in Europe. Several factors influence WTI oil prices, including the actions of suppliers, geopolitical events, OPEC’s production decisions, and the value of the US Dollar. Weekly reports on oil inventories from the American Petroleum Institute and the Energy Information Administration (EIA) are also important for WTI prices. When inventories decline, it usually indicates higher demand, which can push prices up. Conversely, rising inventories suggest a surplus and may lower prices. These reports are published weekly, with EIA’s data considered more reliable because it comes from a government source. Currently, WTI prices are having difficulty staying above $62 per barrel, mainly due to less geopolitical risk from the Middle East. The positive outcome from US-Iran talks indicates that immediate supply issues in the Strait of Hormuz are less probable. This cautious outlook was reinforced by the latest EIA report, which revealed an unexpected increase in crude inventories of 2.1 million barrels last week, contrary to expectations of a decrease.Market Implications And Strategies

It’s also important to consider the evolving situation with India, which is halting its purchases of Russian crude for upcoming deliveries. Back in 2025, India was importing nearly 1.8 million barrels per day from Russia, making it a major player in the global market. If India now turns to alternatives like WTI for its oil, it could significantly tighten the market and push prices higher in the second quarter. This creates a mixed outlook for the coming weeks, as negative geopolitical news counteracts strong demand fundamentals. Given this uncertainty, we suggest that traders consider strategies that can take advantage of potential volatility, rather than trying to predict a clear price direction. For instance, buying long-dated straddles or strangles could be a smart way to prepare for larger price movements without committing to a specific direction. From a technical viewpoint, the $62.50 mark is significant; it reflects a low not seen since the third quarter of 2025. While OPEC+ has indicated it will keep current production limits until its March meeting, any concerns about falling prices could help stabilize the market. For now, we see this level as a potential support area, but a clear drop below it might lead to prices in the $58-$60 range. Create your live VT Markets account and start trading now.Week Ahead: Gold And Dollar Recover As NFP Comes Into Focus

Gold (XAUUSD) inched higher towards the $5,045 mark during early Asian trade on Monday, extending its recent recovery. The move has been underpinned by a softer US dollar and ongoing accumulation from central banks. Attention now shifts to the postponed US January jobs report, due for release on Wednesday.

At the same time, US Treasury Secretary Scott Bessent said on Thursday that a criminal investigation into Kevin Warsh, President Donald Trump’s nominee for Federal Reserve Chair, could not be ruled out should Warsh ultimately resist pressure to lower interest rates. Persistent concerns over the Federal Reserve’s independence have continued to weigh on the dollar, providing indirect support to dollar-priced assets, including gold.

Nikkei Jumps To Record Levels As PM Takaichi Secures Election Win

Japan’s ruling coalition, led by Prime Minister Sanae Takaichi, is heading for a commanding victory in Sunday’s snap general election.

Projections from public broadcaster NHK indicate that the coalition led by Takaichi’s Liberal Democratic Party (LDP) has captured 352 of the 465 seats in the House of Representatives, with the LDP itself securing a clear majority of 316 seats.

Japanese equities recorded their strongest advance since April, as Takaichi’s landmark election win boosted expectations of expanded fiscal spending across major sectors of the economy.

The Nikkei 225 jumped as much as 5.7% to a new all-time high of 57,337.07 by mid-morning local time, while the broader Topix index gained up to 3.4% to reach a record level. Technology and machinery stocks led the rally, with several semiconductor equipment makers posting gains of more than 10%.

Market Movements Of The Week

Gold (XAUUSD)

– XAUUSD found strong support at the 4650 level.

– If bullish momentum holds, it could head toward the 5070 resistance level.

– A breakout of the 5070 resistance level could mean higher prices.

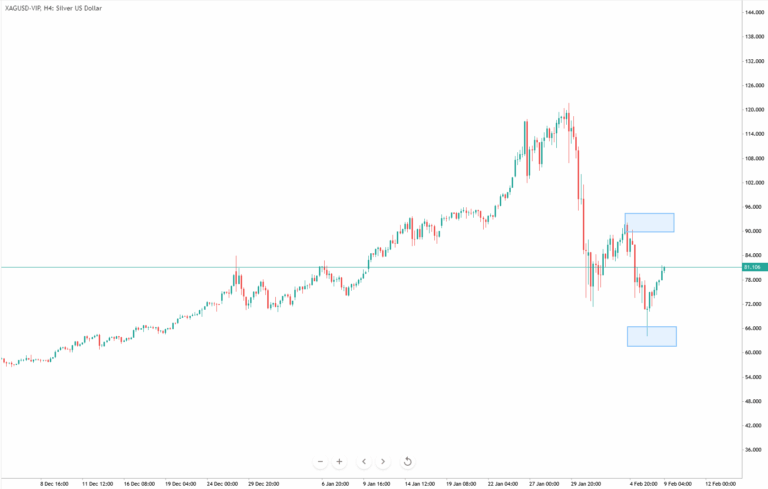

Silver (XAGUSD)

– XAGUSD found support at the 65 level.

– Buyers could be pushing Silver back to the 91 level.

– Upcoming NFP data is crucial for Silver’s movements.

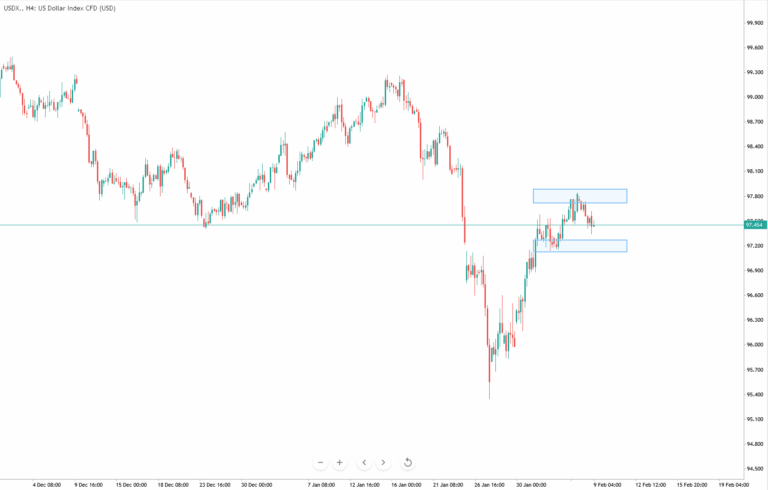

US Dollar Index (USDX)

– USDX surges past and has retested the 97.2 level.

– USDX fails trade higher than the 97.85 resistance level.

– 97.85 resistance level is crucial for USDX, upcoming CPI could decide USDX’s movements.

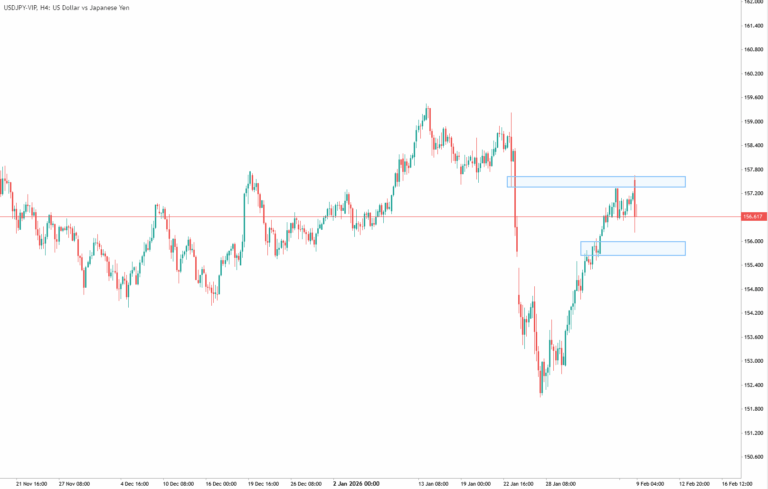

USDJPY

– USD/JPY rejects trading higher facing 157.600 resistance level.

– USD/JPY currently trades above 156.000 support level.

– If USD/JPY fails to hold above 156.000 it could seek for previous lows.

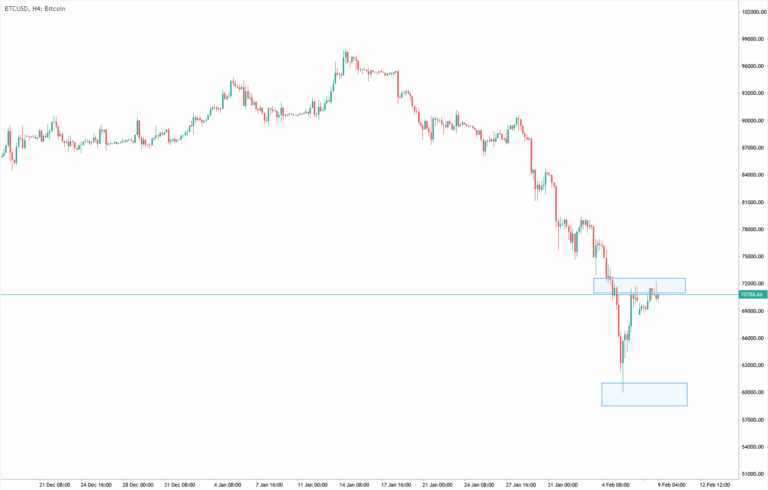

Bitcoin (BTCUSD)

– Bitcoin traded below $60,000 but has quickly rebounded.

– The current $70,000 level is crucial for Bitcoin as it has failed to break it several times.

– Current condition for Bitcoin is still very bearish; it could still retest the $60,000 level.

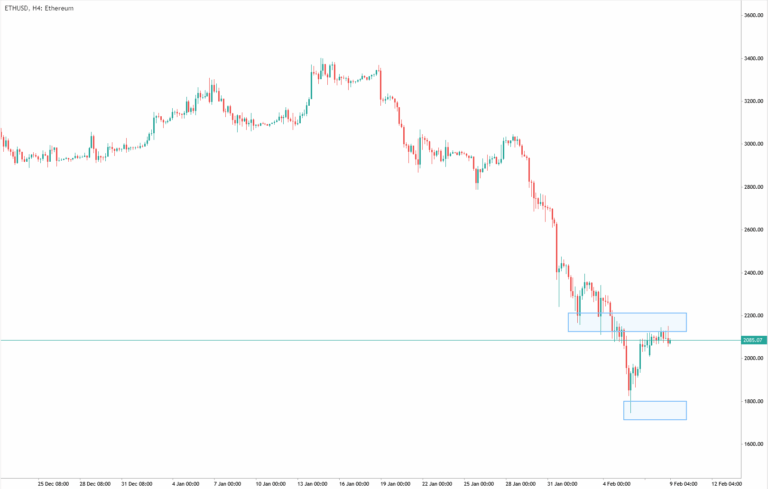

Ethereum (ETHUSD)

– Ethereum traded to a low of $1750 but has rebounded above $2,000.

– Ethereum is testing the resistance level priced at $2,000.

– The next resistance level is priced at $2,400 if buyers strengthen.

Key Events This Week

10 February

1. US Retail Sales, Forecast: 0.40%, Previous: 0:60%

Weaker consumer activity could put pressure on the Dollar.

11 February

1. US Average Hourly Earnings m/m, Forecast: 0.30%, Previous: 0.30%

High wages would favour Warsh’s hawkish side

2. US Non-Farm Employment Change, Forecast: 70K, Previous: 50K

A strong beat could seal Gold’s fate below $5,000.

3. US Unemployment Rate, Forecast: 4.40%, Previous: 4.40%

A rising rate could reinforce a softer Fed tone.

13 February

1. US Core CPI, Forecast: 0.30%, Previous: 0.20%

A higher inflation rate could resume rate hikes.

Bottom Line

Anticipation of more aggressive interest rate cuts by the US Federal Reserve in 2026, reinforced by emerging signs of softness in the US labour market, has become an additional pillar of support for the non-yielding yellow metal.

Meanwhile, the White House reiterated that diplomacy remains President Donald Trump’s preferred route in managing relations with Iran, while stressing that military options remain available if needed.

This combination keeps geopolitical risks elevated and continues to underpin demand for gold as a safe haven.

Further tailwinds come from renewed selling pressure on the US dollar, which offers additional support to precious metals. That said, expectations that incoming Fed Chair Kevin Warsh may take a firmer, less dovish policy stance could cap further upside in gold, suggesting a more cautious approach is warranted when positioning for additional gains.

HSBC Asset Management observed that volatility in 2025 impacted the diversifying role of gold and silver.

In 2025, gold and silver prices changed dramatically. This shift began with geopolitical tensions and worries about the Federal Reserve’s independence. The situation quickly became fueled by retail investors, leading analysts to warn that leveraged selling could increase their correlation with stocks.

Despite this, central banks are moving away from the US dollar, and ongoing demand during crises is supporting the case for precious metals. Retail activity has boosted returns but added a level of volatility to gold and silver, which usually act as safe havens.

The recent ups and downs in gold and silver show that no single safe-haven asset is perfect. This highlights the importance of a diversified investment strategy. Using an active, multi-asset approach can help create uncorrelated performance across different assets.

Last year’s price movements in gold and silver started with geopolitical concerns and ended with a speculative rush from retail traders. While that frenzy has faded, the market’s memory is short. A key takeaway from 2025 is that precious metals can act like tech stocks when speculation runs high.

The increased volatility last year also challenged gold and silver’s role as simple portfolio diversifiers. Their connection to stocks surged during leveraged selling in the fourth quarter. The Gold Volatility Index (GVZ), which briefly exceeded 35 in late 2025, has now returned to a more typical 16-18 range.

Even though prices have pulled back from last year’s highs, the case for precious metals remains strong. Central banks purchased over 1,000 tonnes of gold for the second consecutive year in 2025, continuing a powerful trend away from the dollar. This steady institutional demand stabilizes the market, providing support that retail speculation cannot.

In the coming weeks, options traders have a unique opportunity. The tension between steady institutional buying and the risk of another speculative surge means that trading volatility is key. Buying long straddles or strangles on gold and silver ETFs may effectively position investors for significant price shifts, regardless of direction.

Currently, implied volatility in the options market is much lower than during the peaks of 2025. This makes purchasing options relatively inexpensive, with a clear risk and the possibility of high rewards. Essentially, we are buying insurance against sudden downturns or a repeat of last year’s speculation.

This situation is similar to what we experienced in some equity markets back in 2021. After the initial retail-driven excitement faded, the affected stocks still faced sudden and sharp swings for an extended period. Precious metals may now find themselves in a similar situation, where calm periods could signal the next significant price movement.

Analysts Quek Ser Leang and Lee Sue Ann predict slight upward momentum for the Euro against the Dollar, with a possible rise to 1.1840, but expect resistance at 1.1860 to hold.

UOB analysts say the Euro is showing slight upward pressure against the US Dollar. It may rise to 1.1840, but it’s unlikely to surpass 1.1860. To continue this upward trend, it needs to stay above 1.1785.

Right now, the Euro might increase a bit, but weak momentum could limit its rise at 1.1840. The 1.1860 resistance level is strong unless the Euro falls below 1.1765 soon, which would lower the risk of a downward move. If the Euro does break above 1.1860, we could see a period of range trading.

Insights from FXStreet

This information comes from the FXStreet Insights Team, who gather views from market experts. It includes commercial notes and perspectives from various analysts. Currently, the Euro is under slight upward pressure, but this happens amid mixed economic signals. Eurozone inflation has recently dropped to 2.5%, while the latest US jobs report showed a strong gain of over 210,000 jobs, supporting the dollar. As a result, the Euro is having difficulty staying above the 1.0800 mark.Trader Strategies and Market Levels

For traders in derivatives, this means focusing on key market levels in the next few weeks. Any rise in the Euro will likely be capped at the 1.0850 resistance area, with the bigger barrier at 1.0880 seeming untouchable. To keep moving up, the Euro needs to hold above the support level at 1.0750. Downward momentum has slowed down, but if the Euro breaks and stays below 1.0720, it would signal renewed risks for a drop, similar to the volatility seen in late 2025. On the other hand, if the Euro moves steadily above the strong resistance at 1.0880, it would suggest a shift into range trading. This could make strategies like short strangles for trading volatility more appealing. Create your live VT Markets account and start trading now.Asian equities soar, with Japan’s Nikkei 225 hitting a record high following elections

Asian stocks soared on Monday, with Japan’s Nikkei 225 hitting an all-time high after Prime Minister Sanae Takaichi’s strong election win. The Nikkei 225 rose by 4.45% to 56,660, as the coalition led by the Liberal Democratic Party secured 352 out of 465 seats, taking a majority in Japan’s House of Representatives.

South Korea’s Kospi Index climbed 4.2% to 5,305, boosted by a renewed appetite for risk following a significant rebound in US stock indexes. China’s SHANGHAI Index increased 1.25% to 4,115, while the Hong Kong Stock Exchange rose 1.57% to 26,975. Additionally, India’s Nifty50 grew by 0.66%, and Taiwan’s Taiex gained 1.96% to 32,405. Australia’s S&P/ASX 200 saw an increase of 1.85% to 8,870. Other Southeast Asian markets also posted positive results.

Key Sectors in Asian Stock Markets

Important sectors in Asian stock markets include technology, financial services, manufacturing, retail, and e-commerce. These markets are influenced by company earnings, economic conditions, central bank policies, and various political and technological factors. However, risks such as political instability, geopolitical tensions, natural disasters, and currency fluctuations can also affect market performance. Japan’s decisive election win is a key indicator right now, driving the Nikkei 225 to an all-time high. With Prime Minister Takaichi receiving a strong mandate, we can expect policies favoring exporters, likely putting continued pressure on the yen. Traders might want to position themselves for further increases through Nikkei 225 call options or futures, as the political stability is a significant driver. This rally is supported by a weak currency, a trend we anticipate will continue. The Japanese yen is currently trading around 168 to the US dollar, its lowest in over 20 years, making Japanese exports much more competitive. A similar situation occurred in 2025 when a weaker yen significantly boosted corporate profits, and this election result will likely enhance that in the upcoming weeks. Volatility is an essential factor to monitor now. After a single-day surge of more than 4%, the Nikkei Volatility Index has jumped over 25, creating an opportunity for sellers of premium options. Selling out-of-the-money puts or using bull put spreads on the Nikkei 225 can be smart strategies, taking advantage of the upward trend and the increased market fear.Positive Sentiment and Market Strategies

A positive sentiment is spreading through Asia, with Japan and South Korea leading with over 4% gains. There are significant capital inflows, with global funds investing over $20 billion in developed Asian markets in January 2026, reversing the outflows from late 2025. This overall risk-on attitude, buoyed by a strong finish on Wall Street, indicates it’s a good time to invest in regional indices. Nonetheless, we should also prepare for a potential short-term pullback after such a sharp increase. Buying protective puts on the Kospi 200 or Taiwan’s Taiex, which heavily feature the cyclical tech sector, could be a cost-effective hedge. We remember the mid-2025 market pullbacks when rallies became too stretched, so allocating some funds to bearish positions could safeguard profits. While the region is thriving, the gains in the Chinese and Hong Kong markets are less pronounced. This difference presents a clear opportunity for pair trading. Taking a long position on the Nikkei 225 while shorting the Hang Seng Index might be profitable, as China continues to face challenges in its property sector and regulatory issues. Create your live VT Markets account and start trading now.Traders watch the US Dollar Index stay close to 97.50 while waiting for key economic data releases.

The US Dollar Index is currently steady around 97.50 as traders await important economic data that has been delayed due to a partial government shutdown. In January, the US Nonfarm Payrolls are projected to show stability in the labor market, with an expected addition of 70,000 jobs and an unemployment rate of 4.4%. Market sentiment improved when the Michigan Consumer Sentiment Index unexpectedly rose to 57.3 in February, beating the forecast of 55.0.

The US Dollar Index, which reflects the US Dollar’s value against six major currencies, has seen losses for the second consecutive day, trading near 97.60 during Asian trading hours on Monday. Markets expect the Federal Reserve to keep interest rates steady in March, with possible cuts in June and September. San Francisco Fed President Mary Daly noted that the economy may stay in a low-hiring and low-firing phase. In contrast, Atlanta Fed President Raphael Bostic highlighted the ongoing risk of high inflation for the Fed.

How Monetary Policy Affects the Dollar

The Federal Reserve’s monetary policy plays a crucial role in shaping the US Dollar’s value. This includes changes to interest rates and methods like quantitative easing, which is used during crises to boost credit flow but often weakens the Dollar. On the other hand, quantitative tightening, which reduces bond buying, tends to strengthen the Dollar. Currently, the Dollar is weak, trading around 97.60, as we wait for significant economic reports due to the partial government shutdown. With Wednesday’s job numbers and Friday’s inflation data on the horizon, the market is tense. This uncertainty may create opportunities. The key point is that we are likely to see a significant price movement in either direction once the data is revealed. Implied volatility for currency options has risen, with the Cboe FX Volatility Index increasing over 8% in the last two weeks. This signals that traders may want to adopt strategies that benefit from sharp movements, like straddles on major pairs such as EUR/USD. The expectation for only 70,000 new jobs in January highlights a slowdown in the labor market. If the unemployment rate holds at 4.4%, it will signal a continuing upward trend observed during the latter half of 2025, likely reinforcing the market’s bet on a Fed rate cut in June.Getting Ready for Economic Changes

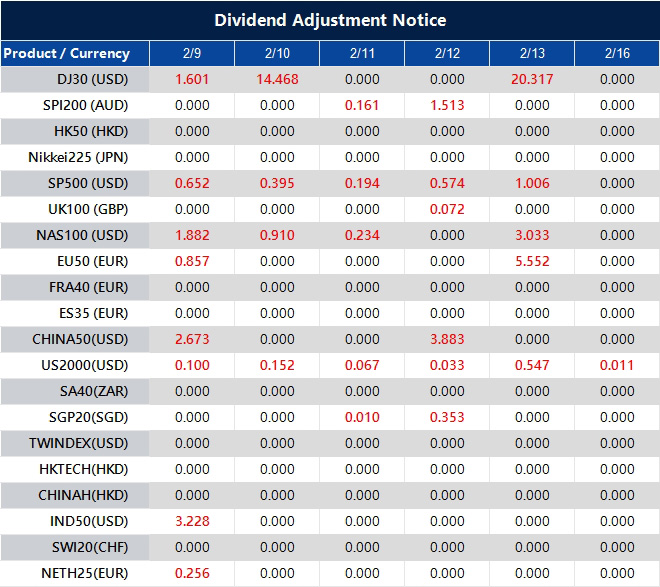

With the market already pricing in rate cuts for June and September, any sign of economic weakness could lead to more Dollar selling. To prepare, consider bearish strategies, like buying put options on the US Dollar Index, which allow for profit from a decline while clearly setting a maximum risk. However, be cautious of a sudden turnaround. Recall how a stronger-than-expected inflation report in the fall of 2025 caused a spike in the Dollar. The recent surprise in the Michigan Consumer Sentiment Index and hawkish comments from Atlanta Fed President Bostic remind us that a weak Dollar isn’t guaranteed. Therefore, any bearish strategies should include protection against unexpectedly strong economic reports. For example, if job gains exceed 150,000, this could challenge the narrative of a rate cut and create a push for the Dollar. A small out-of-the-money call option can act as a cost-effective insurance policy against such a scenario. Create your live VT Markets account and start trading now.Dividend Adjustment Notice – Feb 09 ,2026

Dear Client,

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].