GBP/USD trades near 1.3380 during Asian hours after previous modest losses and with bearish expectations.

**GBP/USD Decline**

GBP/USD is below 1.3400 as the US dollar gains strength due to expectations that the Federal Reserve will keep interest rates steady. The pair traded around 1.3380 during Asian hours on Friday, showing a slight recovery after previous losses. However, it may continue to fall as the USD gains momentum.

Recent data from the US Department of Labor shows that Initial Jobless Claims dropped to 198K for the week ending January 10, better than the expected 215K. This decline suggests a stable labor market, despite ongoing high borrowing rates, which boosts the US dollar.

Currently, GBP/USD is nearing 1.3370 as strong US data supports a rise in the dollar, overshadowing positive GDP figures from the UK. The pair is currently at 1.3367, reflecting a 0.53% decrease, mainly due to robust US economic indicators outweighing UK economic news.

Thursday’s positive sentiment was fueled by the Jobless Claims report, showing a drop to 198K, alongside improvements in manufacturing indexes. The New York Empire State Manufacturing Index rose from -3.7 to 7.7, while the Philadelphia Fed Manufacturing Survey increased by 12.6, exceeding expectations.

The author has no positions in the mentioned stocks and is compensated solely by FXStreet. This article does not offer financial advice or personalized recommendations; the information should not be viewed as investment advice.

**Market Reaction in 2025**

Reflecting on this period in 2025, the market responded positively to strong US labor data that kept the Federal Reserve’s stance steady. Initial jobless claims at 198K, much lower than expected, indicated a strong economy, leading the dollar to outperform the pound.

This trend has continued, with the Fed taking a cautious approach through 2025, which supports the dollar. The latest jobless claims for the week ending January 9, 2026, are steady at 210,000, confirming a tight labor market and giving the Fed little reason to cut interest rates from the current 5.25% level.

Consequently, the GBP/USD pair has declined over the past year and is now trading near 1.3150, significantly lower than the 1.3380 level in January 2025. The difference in interest rates between the US and the UK remains a key driver for currency traders, as the narrative of a stronger US economy still puts pressure on the pound.

**UK Economic Pressures**

Attention is now turning to the Bank of England, which faces different economic challenges. UK inflation has decreased to 2.5% in the latest report, leading the markets to predict that the BoE may cut rates before the Fed. This anticipated policy shift is likely to increase downward pressure on the GBP/USD pair in the coming weeks.

Given this outlook, buying put options on GBP/USD is a straightforward way to prepare for potential further weakness in the pound. This strategy allows traders to profit if the exchange rate drops below a certain level, while limiting the initial risk to the premium paid for the option. It’s a direct bet on a strong dollar and a potentially weaker pound.

Since implied volatility often spikes around central bank meetings, a bear put spread could also be a smart strategy. By selling a lower-strike put against a purchased put, traders can lower the upfront cost of their position. This method caps potential profits, but offers a more capital-efficient way to bet on a moderate decline in GBP/USD.

Create your live VT Markets account and start trading now.

The US dollar weakens as risk appetite in financial markets improves

The US Dollar has weakened against major currencies, including the New Zealand Dollar, wiping out earlier gains. Strong US economic data has reduced the likelihood of immediate interest rate cuts by the Federal Reserve, with forecasts now pointing to cuts in mid to late 2024.

US economic data is robust, and with Fed Governor Michelle Bowman’s speech on the horizon, market focus remains sharp. The Australian Dollar has increased amidst cautious optimism regarding the Reserve Bank of Australia’s future decisions, while the Japanese Yen is facing intervention due to its ongoing weakness.

US And UK Economic Developments

US President Donald Trump mentioned a decrease in Iran’s crackdown on protests and warned of repercussions if violence continues. Meanwhile, in the UK, a positive GDP report helped push the GBP to around 1.3385, reflecting a 0.3% growth in November, which exceeded forecasts. Gold prices have fallen from record highs because eased tensions in Iran reduced demand for gold as a safe haven. WTI Oil prices have remained steady despite ongoing geopolitical tensions with Russia and Ukraine, as Ukraine escalates attacks on Russian tankers. The value of the Japanese Yen is shaped by Japan’s economy and the Bank of Japan’s policies, which range from very loose to gradually tightening, affecting bond yields and market sentiment. The market is adjusting to the possibility that Federal Reserve rate cuts may not happen as soon as previously thought, shifting expectations to June or September. This adjustment follows strong US economic data, reminiscent of early 2025 when solid job growth consistently delayed thoughts of easing. Traders in derivatives might consider strategies that profit from this delay, like selling near-term call options on interest rate futures priced for earlier cuts. With USD/JPY around 158.50, the risk of direct intervention from Japan’s Ministry of Finance has become a concern. Historically, Japan intervened multiple times in autumn 2022 when the pair exceeded 150, causing swift reversals. Given this background, buying relatively inexpensive, out-of-the-money put options on USD/JPY could be a smart way to hedge against any sudden strength in the yen.The Impact Of Central Bank Policies

The strong performance of the UK economy, highlighted by a 0.3% monthly GDP growth, indicates that the Bank of England may keep interest rates higher for longer. UK inflation has remained stubbornly above the 3.5% mark into late 2025, and this new growth data strengthens the case for patience in policy. This context makes call options on GBP/USD an intriguing opportunity, betting that the pound will be supported by its domestic economy. The Australian and New Zealand dollars are thriving as market risk appetite increases. We observed this dynamic in the latter part of 2024 when easing global inflation fears lifted these commodity-linked currencies. Traders might capitalize on this trend through strategies like bull call spreads on AUD/USD to gain upside exposure while clearly managing their maximum risk. In commodities, gold prices are retreating from their record highs as tensions in Iran decrease, lessening its allure as a safe haven. This may present a chance to sell covered calls against current gold holdings to generate income while prices stabilize. On the other hand, heightened attacks on Russian oil tankers pose fresh supply risks for crude oil, making call options on WTI futures useful for hedging against possible price surges. Create your live VT Markets account and start trading now.USD/JPY drops 0.18% to near 158.35 as Yen strengthens

The USD/JPY pair has dropped to about 158.35 due to discussions about potential Japanese intervention. Japan’s Finance Minister stated that all options, including currency intervention, are on the table to address the Yen’s decline.

The Federal Reserve is expected to keep interest rates unchanged this month, which will impact currency trends. The US Dollar is generally strong but has slightly decreased ahead of the long weekend in the US.

Technical Analysis

Currently, the USD/JPY is stabilizing around 158.00. Over the last two months, it has fluctuated between 154.40 and 157.90. The 20-day EMA at 157.33 supports an ongoing uptrend, while the RSI at 62 indicates continued momentum. If prices stay above the 20-day EMA, the upward trend may persist, with support likely during any pullbacks. The US Dollar is the official currency of the United States and makes up over 88% of global foreign exchange transactions, averaging $6.6 trillion per day in 2022. Federal Reserve actions, like changing monetary policy or using unconventional measures such as quantitative easing or tightening, can significantly impact the USD’s value by affecting credit in the economy. These decisions are aimed at managing inflation and boosting employment, which in turn affects the USD’s status worldwide. The USD/JPY is trading close to 158.35, raising concerns about potential intervention from Japanese authorities. Officials have made it clear that they are prepared to tackle excessive moves against the yen. This situation is reminiscent of 2024 when authorities spent over 9 trillion yen to defend the currency around the 155-160 range, making current warnings seem credible. At the same time, the Federal Reserve is largely expected to keep interest rates steady during this month’s meeting. Data from late 2025 indicated core inflation remained persistent at 2.7%, and the labor market added a solid 195,000 jobs in December, leaving the Fed little reason to consider lowering rates. This difference in policy between the US and Japan is the main factor keeping the dollar strong.Risk Management Strategies

From a technical viewpoint, the upward trend remains valid as long as the price stays above the important support level of 157.33, which is the 20-day moving average and the breakout point from previous consolidation. A daily close below this level would indicate that a deeper correction could be on the way. For derivative traders, the tension between a stable trend and the risk of a sudden reversal creates a high-volatility environment. This suggests that options pricing will reflect this uncertainty, making strategies that benefit from significant price swings appealing. Traders might consider buying straddles or strangles to take advantage of any major moves, regardless of direction. Those holding long positions in USD/JPY futures should think about buying put options to protect against a sudden drop due to intervention. These puts can act as insurance, safeguarding profits or limiting losses if Japanese officials act on their warnings. This approach is a wise way to manage the evident downside risk in the coming weeks. Create your live VT Markets account and start trading now.USD/CHF stays near 0.8020 despite a decline, with USD recovery potential

The USD/CHF is currently trading around 0.8020, slightly down from its recent highs. The US Dollar shows signs of recovery. The Federal Reserve plans to keep interest rates steady, with a 95% chance of no change, according to the CME Group’s FedWatch tool. Expectations for a rate cut have been pushed to June.

Initial Jobless Claims in the US dropped to 198K, lower than the 215K estimate. This points to a strong job market despite high borrowing costs. The Swiss Franc may weaken against the US Dollar as concerns about Iranian tensions ease and due to changes in Fed leadership, highlighted by remarks from US President Donald Trump.

Market Sentiment and The Swiss Franc

The value of the Swiss Franc is shaped by market sentiment, the Swiss economy, and the actions of the Swiss National Bank (SNB). Historically, the Franc has been linked to the Euro and remains strongly correlated with it. It is seen as a safe haven because of Switzerland’s stable economy, strong exports, and neutral political stance. Decisions made by the Swiss National Bank, including changes in interest rates, greatly influence the Franc’s value. Higher rates typically attract more investors. The Swiss economy’s performance, including growth and inflation, also impacts the Franc and often reflects Eurozone conditions due to their close relationship. The USD/CHF is testing the 0.8000 level again, but the reasons are different this time. Last year, January 2025, we saw a strong US job market. Now, the recent data indicates a softening with initial jobless claims rising to 230,000 for the week ending January 9, 2026. This change in the job market is shifting expectations for the Federal Reserve. Unlike last year when hopes for a rate cut were pushed to June 2025, the market is now anticipating action sooner. The CME FedWatch Tool shows a 70% chance of a rate cut by the March 2026 meeting.The Central Bank Divergence

Conversely, the Swiss National Bank is backing the Franc. Their choice to hold rates steady in December 2025 surprised many because inflation remained stubborn at 1.9% for that month. This is different from other central banks that are considering easing. This difference between a possibly dovish Fed and a relatively hawkish SNB suggests a downward trend for USD/CHF. Traders might look at put options to hedge against or speculate on further declines in the coming weeks. We should remember the SNB’s sudden removal of the EUR peg in January 2015, which shows their ability to make impactful moves. The main risk to this outlook is a sudden rebound in US economic strength or more aggressive comments from Fed officials. Therefore, we need to keep an eye on upcoming US Industrial Production data. The US Dollar’s status as a safe haven could return if global risk sentiment weakens. Create your live VT Markets account and start trading now.Exxon Mobil (XOM) reaches a new all-time high, signaling bullish momentum and continued trend

Exxon Mobil has hit a new high, showing a positive trend. This upward movement began from a low point on November 26, 2025, and is following a five-wave pattern. Wave (1) ended at $125.93, then wave (2) dropped to $118.27, forming a zigzag shape. In wave (2), wave A hit $122.39, wave B peaked at $126.20, and wave C fell to $117.90, completing this correction.

Wave 3 Progression

Next, the stock rose in wave (3). Wave 1 reached a high of $124.86, then wave 2 retraced to $122.56. The increase continued in wave 3, ending at $131.72, followed by a pullback in wave 4 which settled at $128.30. This pattern hints at the possibility of another gain in wave 5 of (3). After wave 5 finishes, we expect an adjustment phase in wave (4) that will correct from the low on January 8, 2026, before the longer-term trend resumes. In the short term, as long as the support level at $117.90 holds, any decline is likely to stabilize within a 3, 7, or 11 swing pattern. This indicates a promising future for Exxon Mobil, with sustained strength expected after any short-term corrections. Currently, Exxon Mobil appears to be in the final stage of a strong upward trend that started back in November 2025. This suggests the stock has some additional upside potential in the short term. This setup may favor short-term bullish strategies, like buying near-term call options, to take advantage of this last upward move. However, once this final upward push is complete, we expect a corrective pullback. Traders should be ready to take profits from any bullish positions as momentum peaks. Shifting to a bearish approach, such as buying put options, could be a way to benefit from this anticipated temporary decline.Market Support Factors

This technical outlook is backed by the broader market, with WTI crude prices recently surpassing $95 a barrel for the first time since late 2024. This increase comes from OPEC+’s continued production discipline throughout 2025 and a recent government report showing a significant drop in U.S. oil inventories. These factors strengthen the overall positive case for energy stocks. We have seen similar patterns before, especially during the rally in the second quarter of 2025. Back then, the stock experienced a rapid rise followed by a healthy pullback that set the stage for the next big advancement. This history suggests that the expected correction could provide a good opportunity to enter longer-term bullish positions. The key support level to monitor is the $117.90 mark, which was the low point during the corrective wave in late December 2025. As long as the stock remains above this level, the bullish trend is considered valid. Any defensive strategies—like setting stop-loss orders on long positions or selecting strike prices for put options—should be based around this important threshold. Create your live VT Markets account and start trading now.AUD/JPY pair drops to about 106.10 as the Yen strengthens amid intervention concerns

The AUD/JPY currency pair dropped to around 106.10 during the early European session on Friday. Japan’s finance minister announced that all options, including direct currency intervention, are available to support the Yen.

Japan’s Prime Minister Sanae Takaichi may advocate for more spending policies, which could also impact the Yen. Takaichi plans to dissolve parliament next week and call for a snap election, which may influence the currency’s value.

Technical Analysis And Indicators

In the charts, AUD/JPY remains above the rising 100-day EMA at 101.52, showing a bullish trend. The pair is trading between Bollinger Bands at 106.52 and 105.21, indicating strong buying interest. The RSI is at 66, suggesting strong momentum. If AUD/JPY closes above the upper Bollinger Band, it may see further gains. However, a pullback could lead to consolidation in the support range between 105.21 and 103.90. The overall technical outlook looks good for buying dips as long as the EMA remains upward. The Yen’s value is influenced by the Bank of Japan’s policies, bond yield differences, and overall risk sentiment. Recent adjustments in the Bank of Japan’s policies have also helped the Yen against major currencies. The AUD/JPY pair is currently around 106.10, facing immediate resistance around 106.50. This resistance is supported by warnings from Japanese officials about possible intervention to support the Yen. Traders should be aware of this potential risk over the coming weeks.Trading Strategies And Risks

The overall trend remains positive, with the pair staying well above its 100-day moving average, a key support level. We suggest buying call options during any dips towards the 105.20 area. This approach allows traders to capture potential gains while managing risks if fears of intervention arise. The main risk is a sudden action from the Bank of Japan, which oversees currency control. Thus, holding some out-of-the-money put options can provide a low-cost hedge against a sharp decline. This strategy protects long positions from rapid Yen strengthening triggered by official warnings. We’ve seen this happen before, especially during interventions in late 2022 and again in 2024. In those situations, verbal warnings from the Ministry of Finance led to sharp, multi-day declines in Yen pairs before the underlying uptrend resumed. For instance, USD/JPY fell nearly 6% in just one day in October 2022 after intervention was confirmed. Fundamentally, the difference in policies still supports a higher AUD/JPY. Australia’s recent quarterly CPI report showed inflation at 3.1%, above the Reserve Bank of Australia’s target, while Japan’s core inflation remains stubbornly under 2%. This interest rate gap is a key reason we continue to recommend buying on dips. The tension between a strong technical trend and the risk of intervention is likely to heighten implied volatility. Traders may consider straddles or strangles if they expect significant price movements but are uncertain about the direction. This strategy can profit from a breakout above 106.50 or a sharp drop below 105.00, taking advantage of the uncertainty. Create your live VT Markets account and start trading now.Gold prices decline today in Saudi Arabia, according to market analysis

Gold prices in Saudi Arabia decreased on Friday. The price per gram is now 554.44 Saudi Riyals (SAR), down from 555.24 SAR the day before. The price for one tola of gold is now SAR 6,466.87, down from SAR 6,476.25.

FXStreet calculates local gold prices by adjusting international figures and updating them daily. These prices serve as a reference and may vary slightly from local rates due to market changes.

Gold As A Global Asset

Gold is a popular global asset because of its stability. It acts as a protection against inflation and currency drops. Central banks hold large amounts of gold, with 1,136 tonnes bought in 2022. Several factors influence gold prices, like geopolitical stability, interest rates, and the US Dollar exchange rate. Generally, gold prices rise when the Dollar weakens or during uncertain economic times. Central banks are major buyers, boosting their reserves to improve economic confidence. Countries like China, India, and Turkey are increasing their gold holdings a lot. Gold has an opposite relationship with the US Dollar and riskier assets. Its price typically reacts inversely to stock market changes.Gold Prices As An Opportunity

A slight drop in gold prices should be seen as a chance to buy, not a sign of weakness. This small decline follows a period of steady gains in the latter half of 2025. The overall economic conditions still support gold strongly. The U.S. Federal Reserve’s supportive stance in late 2025 is crucial, with the CME FedWatch Tool showing over a 70% chance of a rate cut by March 2026. This has weakened the US Dollar, which has dropped from its 2024 highs, with the DXY index around 101. A weaker dollar and lower future interest rates usually create a good environment for gold. Central banks continue to buy gold aggressively, continuing a trend that started in 2022. The World Gold Council reported that central banks added over 800 metric tons to their reserves in 2025, with emerging markets leading the trend to diversify away from the dollar. This demand from institutions supports the price of gold. Given these factors, traders should consider call options on gold futures to take advantage of the expected price increase while minimizing risk. Ongoing, though slowing, inflation—around 3.2% in the US—remains a supportive point for gold as a safe investment. While volatility is likely, the general trend for gold seems to be upward in the coming weeks. Create your live VT Markets account and start trading now.Japan’s finance minister Satsuki Katayama says all measures, including currency intervention, are being considered for yen stability.

Japan’s Finance Minister, Satsuki Katayama, has announced that the government is considering all options, including direct intervention in the currency market, to tackle the recent weakness of the Japanese Yen. Currently, the USD/JPY pair has dropped by 0.24%, now at 158.25.

The value of the Japanese Yen largely depends on factors like Japan’s economic performance and the monetary policies of the Bank of Japan (BoJ). Additionally, it is influenced by the differences in bond yields between Japan and the US, as well as traders’ risk appetite.

Role of The Bank of Japan

The Bank of Japan (BoJ) manages currency control and sometimes intervenes in the currency markets to lower the Yen’s value. The BoJ has maintained an ultra-loose monetary policy from 2013 to 2024, which led to a weaker Yen. Recently, a shift away from this policy has started to support the Yen. The widening gap between Japanese and US bond yields is due to their different monetary policies. However, recent changes by the BoJ and rate cuts in other countries are starting to close this gap. The Yen is often viewed as a safe investment, attracting more buyers during market uncertainty, which can increase its value against riskier currencies. The Finance Minister’s remarks about taking “bold action” indicate the government is concerned about the Yen’s current weakness. With USD/JPY at 158.25, there’s a strong chance of direct intervention to bolster the Yen, similar to efforts made in late 2022 and again when the pair fell below 155 in October 2024. This situation poses a significant short-term risk for traders holding long USD/JPY positions. The main issue continues to be the interest rate difference between the US and Japan. Currently, the US 10-year Treasury yield is about 4.1%, while Japan’s 10-year government bond yield is only 1.1%. This wide gap remains attractive for carry traders and has been a key factor behind the Yen’s weakness in 2025, even as the BoJ slowly moves away from its ultra-loose policy.Impact on Derivative Traders

For derivative traders, the government’s warning raises the expected volatility for USD/JPY in the coming weeks. The implied volatility for one-month options has surged to over 12%, compared to an average of 9% in the last quarter of 2025. It might be wise to consider buying JPY calls or USD/JPY puts as a hedge against or a way to profit from a rapid drop triggered by intervention. Keep in mind that verbal intervention is much simpler than actual market actions, which could cost Japan billions in foreign reserves. Japan’s core inflation, which was reported at 2.3% for December 2025, does not warrant aggressive rate hikes from the BoJ just yet. Additionally, with global equity markets remaining stable, there is limited safe-haven demand to support the Yen naturally. Create your live VT Markets account and start trading now.Gold prices in the Philippines decline, according to today’s data from relevant sources

Gold prices in the Philippines dropped on Friday, as reported by FXStreet. The price per gram went down to 8,784.39 Philippine Pesos (PHP) from 8,796.89 the day before.

The price per tola also fell, decreasing to PHP 102,458.10 from PHP 102,605.10. The price of gold per Troy ounce was PHP 273,225.10. FXStreet converts international gold prices to local currency using the USD/PHP rate.

A Safe Haven Asset

Gold is seen as a safe-haven asset and a way to protect against inflation. Central banks are the biggest buyers of gold, using it to diversify their reserves and support local currencies in uncertain times. In 2022, central banks bought 1,136 tonnes of gold worth around $70 billion. Gold prices often move in the opposite direction of the US Dollar and US Treasuries. They can also change based on geopolitical events and economic conditions. Factors like interest rates, currency performance, and investor demand affect gold prices. FXStreet notes that market information is for reference only and may vary. Readers should do their own research before investing in gold or other assets. Currently, we are seeing a small decline in gold prices. This seems to be a minor adjustment rather than the beginning of a big downtrend. This short-term weakness is occurring as the US Dollar has weakened from its 2025 highs. This inverse relationship is important for our outlook in the coming weeks.Market Expectations

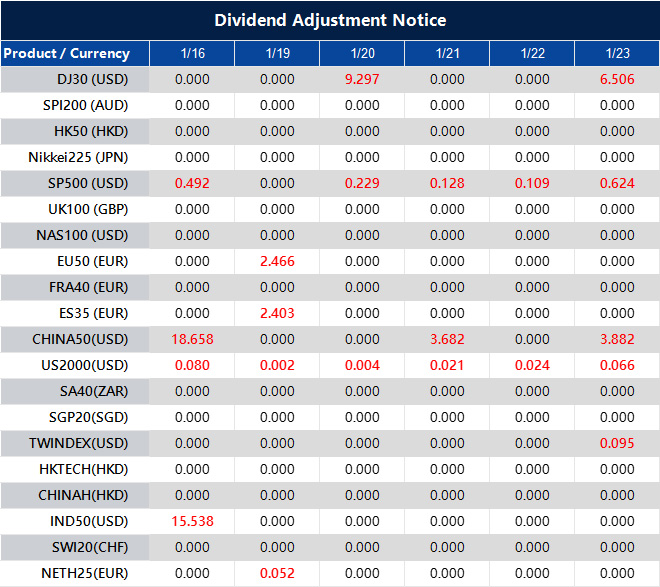

The market now anticipates possible Federal Reserve rate cuts later this year. This outlook is backed by the December 2025 jobs report, which showed a slower labor market with only 155,000 jobs added. Last week’s inflation data, showing a Consumer Price Index (CPI) of 2.9% for the year, suggests that peak interest rates may be behind us. Lower interest rates usually make non-yielding gold more attractive. We must also keep in mind the strong demand that has kept prices steady. Throughout the chaos of 2023 and 2024, central banks were major buyers. The World Gold Council’s latest report for Q4 2025 indicates that this buying spree continued, with net purchases exceeding 950 tonnes for the year. This steady buying from official sources acts as a safety net against large price drops. In the coming weeks, this dip might be a chance to prepare for a future price increase. Buying call options or setting up bull call spreads could be a smart way to gain upside exposure while managing risk. Traders who already have long positions might want to consider buying out-of-the-money put options to protect against any sudden reversals due to geopolitical de-escalation. Create your live VT Markets account and start trading now.Dividend Adjustment Notice – Jan 16 ,2026

Dear Client,

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].