China’s M2 money supply exceeds predictions with an 8.5% year-on-year increase in December

In December, China saw its M2 money supply rise by 8.5% compared to last year, exceeding predictions of 8%. This stronger-than-expected growth could influence economic choices.

Several currencies shifted in value, with EUR/USD dropping below 1.1650 as strong US economic data impacted the Federal Reserve’s interest rate plans. On the other hand, GBP/USD stayed above 1.3400 after a surge due to positive data on UK growth and industry.

In December, new loans in China reached 910 billion, surpassing the expected 800 billion.

China’s new loans in December 2025 hit 910 billion yuan, exceeding the expected 800 billion yuan. This increase has sparked optimism about the country’s economic recovery despite global challenges.

The data is important for the markets because it shows demand for credit and overall economic activity in China. Analysts see this rise in loans as a sign of economic strength, which could ease worries about slow growth.

Impact On Sectors

Broader implications of the lending increase are positive for sectors like real estate and infrastructure, which are crucial for China’s growth. This trend may also affect central bank policies and how markets view credit growth in the world’s second-largest economy. As the situation evolves, further updates will be provided as markets react to these numbers. The unexpected rise in loans from December 2025 is a bullish sign for China’s economic momentum as we approach the new year. It indicates that policy support is translating into real economic activity. This might lead to a reassessment of bearish positions and a shift toward strategies that capitalize on a cyclical recovery.Impact On Commodities

This growth in credit is vital for industrial commodities since lending often supports infrastructure and property development. We have seen iron ore futures rise above $138 per tonne this month due to renewed optimism for demand from Chinese steel mills. We are considering call options on ETFs that track industrial metals and major miners to take advantage of this trend. In the stock market, we expect this news to support Chinese indices that faced difficulties last year. A smart strategy is to use bull call spreads on large-cap Chinese ETFs to position for a potential rebound while managing our risk. We recall similar credit-driven rallies in the past, like in 2016, led by these sectors. The currency market offers another opportunity to express this outlook, as a stronger Chinese economy usually boosts commodity-linked currencies. The Australian dollar has already strengthened against the US dollar, climbing above 0.6780 since this news emerged. We see potential in taking long positions in AUD/USD through futures or options. This surge in credit comes ahead of the full Q4 2025 GDP figures, which recently reported at 4.9%, slightly better than expected. With this confirmation, implied volatility on Chinese assets may begin to drop as uncertainty decreases. This environment makes selling out-of-the-money puts on select Chinese stocks an appealing, income-generating strategy. Create your live VT Markets account and start trading now.Dividend Adjustment Notice – Jan 15 ,2026

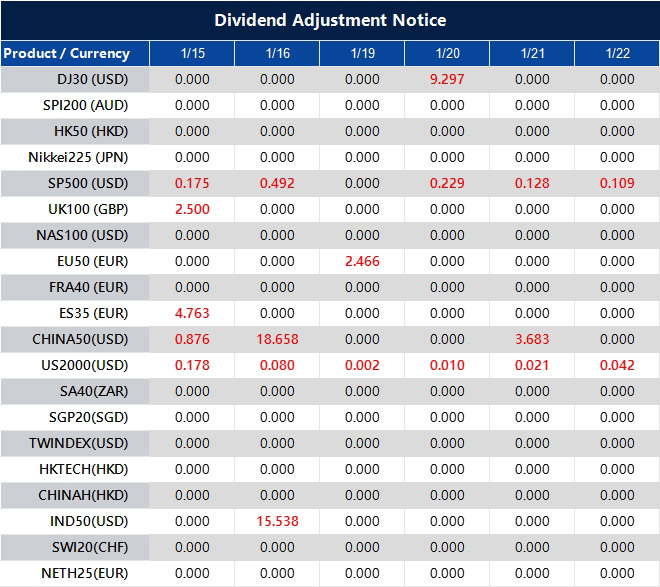

Dear Client,

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

In November, UK manufacturing production exceeded predictions, reaching 2.1% instead of the expected -0.3%.

In November, UK manufacturing production rose by 2.1% compared to last year, outperforming the predicted -0.3%. This indicates that the manufacturing sector is performing better than expected.

Following this positive news, the EUR/GBP exchange rate fell toward the 0.8650 level. Analysts from the UOB Group expect GBP/USD to trade within the range of 1.3410 to 1.3460.

Impact of UK GDP Growth

The growth in UK GDP helped the GBP/JPY pair recover from earlier losses. Meanwhile, silver prices dropped below $89.50 as interest in safe-haven assets diminished. In the financial markets, the EUR/USD fell below 1.1650. Additionally, the crypto market took a hit as the Senate postponed talks on a market-structure bill after Coinbase withdrew. Looking ahead to 2026, potential brokers for currency trading are being discussed, including specific recommendations for various regions and trading types. However, it is important to note that all information provided includes risks, and FXStreet does not offer personalized investment advice. The unexpected rise in UK manufacturing, showing 2.1% growth in November 2025 rather than the forecasted decline, has surprised the market. For much of last year, manufacturing PMI figures from the S&P Global/CIPS survey were below the 50.0 no-change mark, making this a significant shift. This one data point suggests that the economy is stronger than previously thought.Economic Implications of UK Manufacturing Growth

This strong performance challenges the belief that the Bank of England would start lowering its 4.25% policy rate early this year. We now need to consider that the Monetary Policy Committee may hold off on any rate cuts to see if this trend continues. Market expectations, which last month indicated a 70% chance of a rate cut by March, will likely shift to a more cautious approach. Given this situation, there is an opportunity to invest in the options market for a stronger Pound Sterling, especially since GBP/USD remains above 1.3400. Buying call options on the pound provides a way to potentially profit from a shift toward a more aggressive stance by the Bank of England. Historically, similar economic surprises in 2023 led to quick, short-term gains in the currency, benefiting those who positioned themselves for a rise. On the other hand, this economic growth might pose challenges for UK stocks. The possibility of sustained higher interest rates makes bonds more appealing to investors. It’s important to monitor the FTSE 100, as a stronger pound often impacts large-cap companies that earn revenue in foreign currencies negatively. Traders might consider using interest rate swaps to speculate on the Bank of England keeping its restrictive policies for longer than expected. Create your live VT Markets account and start trading now.In November, UK industrial production rose to 2.3%, beating the -0.4% forecast.

In November, the UK’s industrial production rose by 2.3% compared to the previous year, exceeding the expected decline of 0.4%. This encouraging development contributed to stronger UK growth, influencing currency trading. The GBP/USD pair remained above 1.3400, even with a rising US Dollar.

Recent US economic data suggests that the Federal Reserve may pause interest rate changes. This includes higher-than-anticipated numbers in the Producer Price Index and Retail Sales, along with a drop in the Unemployment Rate. Consequently, gold prices have stabilized around $4,600 after previously hitting a record high.

Cryptocurrency Market Declines

The cryptocurrency market faced a downturn after the US Senate Banking Committee delayed discussions on crypto regulations. This postponement occurred after Coinbase withdrew support, highlighting unresolved issues. The information shared is for informational purposes only and should not be seen as recommendations. Individuals should conduct in-depth research before making any investment choices, as the data may contain errors or uncertainties. Investing carries risks, including the potential loss of the entire investment. Both FXStreet and the author do not accept responsibility for any losses or inaccuracies. The unexpectedly strong UK’s industrial production data from last November, showing a 2.3% growth instead of a contraction, has shifted the landscape. This positive momentum was confirmed with the recent inflation data for December 2025, which showed a rate of 2.1%. This puts pressure on the Bank of England, and we might consider purchasing GBP call options during any downturn, especially since the central bank recently showed a 7-2 split in favor of a potential rate hike.US Economy Shows Robust Strength

Meanwhile, the US economy is demonstrating notable strength, which is limiting the pound’s rise against the dollar. The strong Non-Farm Payrolls report for December 2025 added 210,000 jobs, reinforcing the expectation that the Federal Reserve will keep interest rates steady. This economic tug-of-war suggests using range-bound strategies for GBP/USD, such as selling straddles or iron condors with boundaries around the 1.3400 and 1.3460 levels. This economic disparity places the Euro in a weak spot against the pound. Recent PMI data from the Eurozone shows a continued contraction in manufacturing, suggesting that the EUR/GBP may trend lower. Bearish strategies, such as buying put options on this pair, appear attractive in the coming weeks. The Federal Reserve’s likely pause on interest rates will continue to bolster the US Dollar, creating a ceiling for commodity prices. Gold is struggling to surpass last week’s record highs near $4,640. We see this as an opportunity to sell call spreads on gold, betting that a strong dollar will hinder any significant rally. Create your live VT Markets account and start trading now.In November, the UK’s monthly GDP exceeded expectations with a 0.3% increase.

The United Kingdom’s Gross Domestic Product (GDP) rose by 0.3% in November, exceeding the expected increase of 0.1%. This faster growth has helped the pound sterling rebound slightly, keeping the GBP/USD pair above the 1.3400 level.

Gold and US Economic Indicators

In other news, gold is currently trading around $4,600 per troy ounce after retreating from its record high of $4,643. This decline follows positive US economic data that supports the Federal Reserve’s decision to maintain interest rates. The cryptocurrency market experienced a drop after the US Senate delayed a discussion on market structure. This delay occurred after Coinbase withdrew its support due to various issues. Experts suggest that traders should explore different brokers while weighing the pros and cons of major platforms in various regions. Anyone investing should be aware of potential risks and research thoroughly before making financial decisions. The unexpected 0.3% increase in UK GDP for November indicates a stronger economy than expected. This news is particularly welcome after a difficult 2025, which saw stagnant growth reminiscent of the technical recession confirmed by the Office for National Statistics in early 2024. This resilience could help support the Pound, but its inability to stay above 1.3450 shows that the US Dollar remains strong.US Economy and Interest Rates

A strong US economy is currently the main driver for the market, pushing the dollar higher. Solid producer price and retail sales figures back the Federal Reserve’s commitment to keep interest rates high for longer. The US labor market has continually surpassed slow-down expectations throughout 2024, maintaining a trend of strong job creation. For those dealing in interest rate derivatives, the market is quickly reversing expectations for near-term Fed rate cuts. This is a sharp change from late 2024, when Fed forecasts suggested several cuts for 2025 that never materialized. We anticipate a volatile but steady period for US rates, especially as Jerome Powell’s term as Fed Chair comes to an end. Gold’s fall from its record high over $4,600 is directly linked to the strong dollar and stable US interest rates. As the cost of holding non-yielding gold increases, we could see more selling pressure soon. This presents an opportunity to explore strategies that might benefit from either a pullback or a consolidation phase, such as selling covered call options on existing holdings. Create your live VT Markets account and start trading now.USD/CAD pair sees a slight increase in early European trading, approaching the 1.3900 level

The USD/CAD pair is nearing 1.3900 as the US Dollar gains strength. This rise comes from expectations that the Federal Reserve will keep interest rates steady later this month. This anticipation follows the steady increase in the US Consumer Price Index for December. The US Dollar Index, which measures the dollar against six major currencies, is close to its monthly peak at 99.26.

On the other hand, the Canadian Dollar is facing challenges due to weak job market data, with unemployment rising to 6.8% in December. This increase may lead the Bank of Canada to consider lowering interest rates. Technical analysis of USD/CAD shows the pair close to 1.3900, while the 200-day EMA is holding it back from further increases. A solid break above this average could push it toward 1.4000.

US Dollar’s Global Impact

The US Dollar is the most traded currency in the world, making up over 88% of global foreign exchange transactions. The Federal Reserve controls its value mainly through interest rate changes. In times of financial stress, the Fed might use quantitative easing to add cash to the market, which can weaken the dollar. On the flip side, quantitative tightening generally strengthens the dollar as the Fed buys fewer bonds. Last year, around early 2025, USD/CAD was set for a major move as it approached the 1.3900 level. The market was clear, with a strong US Dollar due to a Federal Reserve reluctant to cut rates, and a weak Canadian Dollar affected by rising unemployment. This split in economic outlooks was a crucial factor. Throughout 2025, this trend continued as US inflation remained stubborn. The last December 2025 Consumer Price Index report showed a 3.4% annual increase, prompting the Federal Reserve to keep interest rates higher to manage price pressures. This has supported the US Dollar against most major currencies. Meanwhile, the Canadian job market remains weak, with the unemployment rate recently rising to 7.1%. This situation led the Bank of Canada to start an easing cycle late last year, reducing its key interest rate to help the struggling economy. The ongoing gap between US and Canadian monetary policies heavily impacts the loonie.Trading Strategies for USD/CAD

In the upcoming weeks, the likely trend for USD/CAD seems to be upward, making bullish derivative positions appealing. Traders could consider buying call options with strike prices around 1.4250 or 1.4300 to take advantage of this expected trend. This strategy allows for potential gains while clearly defining the maximum risk involved. Create your live VT Markets account and start trading now.Notification of Server Upgrade – Jan 15 ,2026

Dear Client,

As part of our commitment to providing the most reliable service to our clients, parts of the product will be optimised this weekend.

Optimised Products:

SOLJPY, ADAJPY, BCHJPY, XLMJPY, XRPJPY, BTCJPY, BTCEUR, LTCJPY, ETHJPY, GRTUSD, IOTUSD, ZECUSD, NEOUSD, BTCBCH, ETHBCH, BTCETH, BTCLTC, ETHEUR, ETHLTC, BTCXAU, BTCGLD, ETHXAU, ETHGLD, USDTJPY

Optimisation Hours:

17th January 2026 (Saturday) 00:00–02:00 (GMT+2)

Please note that the following aspects might be affected during the optimisation:

1. The price quote and trading management for the optimised products will be temporarily disabled during the optimisation period.You will not be able to open new positions, close open positions, or make any adjustments to trades.

2. There might be a gap between the original price and the price after optimisation.Gaps between Pending Orders, Stop Loss, and Take Profit will be filled at the market price once the maintenance is completed. It is suggested that you manage the account properly.

Please refer to the MT4 & MT5 software for specific optimisation completion and market opening times.

Thank you for your patience and understanding regarding this important initiative.

If you’d like more information, please don’t hesitate to contact [email protected].

Recent data shows that gold prices in the United Arab Emirates declined.

Gold prices in the United Arab Emirates fell on Thursday, according to FXStreet. The price dropped to 542.57 AED per gram, down from 547.00 AED the previous day. The cost per tola also decreased to 6,329.27 AED, from 6,380.05 AED.

Current gold prices in the UAE are now:

– 1 gram: 542.57 AED

– 10 grams: 5,426.49 AED

– 1 tola: 6,329.27 AED

– 1 troy ounce: 16,875.96 AED

FXStreet updates these prices daily based on international (USD/AED) exchange rates.

Gold As A Store Of Value

Gold is seen as a safe haven and a reliable store of value, especially in uncertain times. It acts as a shield against inflation too. Central banks are significant buyers, purchasing 1,136 tonnes in 2022, the highest amount ever recorded in one year. Gold prices often move opposite to the US Dollar and Treasuries; when the Dollar weakens, gold prices usually increase. Factors like geopolitical instability, interest rates, and the US Dollar’s performance also affect gold prices. This information comes from an automation tool. On January 15, 2026, we’re noticing a slight drop in gold prices, likely due to minor profit-taking. This small change doesn’t alter the strong support for gold’s value. Remember, central bank purchases were strong at the end of 2025, with over 800 tonnes bought globally, providing a solid price base. Watch the U.S. Dollar as the primary variable. It has begun to soften after its strength late last year. With the Federal Reserve hinting at a pause in rate hikes and markets predicting cuts by the third quarter, the Dollar’s attractiveness could decline further. A weaker Dollar usually makes gold cheaper for international buyers, supporting its price.Strategy For Traders

For traders, this situation presents an opportunity to anticipate a price increase in the next few weeks. Buying call options on gold futures or ETFs can help you profit from a possible price rise while controlling your maximum risk. Look for contracts expiring in March or April 2026 to give yourself time for this scenario to unfold. With market uncertainty, we expect gold prices to become more volatile. The Cboe Gold ETF Volatility Index (GVZ), which was around 15 in late 2025, might rise to the 18-20 range. This atmosphere makes bull call spreads an appealing strategy since they can reduce entry costs compared to outright long calls. Traders willing to take on more risk might consider long positions in gold futures for direct exposure. However, using stop-loss orders is crucial to manage increased leverage and potential sharp price swings. Any rise in geopolitical tensions is likely to drive gold prices higher, making risk management essential. Create your live VT Markets account and start trading now.Gold prices in Pakistan decline today, according to recent market data

Gold prices in Pakistan fell on Thursday, according to FXStreet. The price per gram went down to 41,370.16 Pakistani Rupees (PKR) from 41,713.76 PKR the day before. The price per tola also dropped, now at PKR 482,532.90, down from PKR 486,541.20 a day earlier.

FXStreet updates gold prices daily, converting them to Pakistan’s local currency and measurement units. Gold is often seen as a safe investment and a way to protect against inflation. Central banks purchased 1,136 tonnes of gold, worth $70 billion, to enhance their reserves in 2022.