XAU/USD approaches $4,345 during early Asian trading amid rate cut speculation and geopolitical tensions

Gold prices have risen to around $4,345 during the early Asian trading session, supported by anticipated Federal Reserve rate cuts and ongoing geopolitical tensions. In 2025, gold experienced a remarkable annual increase of 65%, the highest yearly gain since 1979.

In December, the Federal Reserve cut interest rates by 25 basis points to a range of 3.50%–3.75%. Lower interest rates can make gold a more appealing investment by lowering holding costs. Fed minutes indicate that further rate cuts are likely if inflation decreases.

Predictions for early 2026 came true as prices varied between the 6,920s and 6,950s.

The S&P 500 saw some ups and downs, especially around the 6,920 and 6,936 levels. After a brief jump into the high 6,950s, prices fell back before bouncing to the mid 6,930s. These changes were related to year-end strategies and tax plans.

In the market, TSLA, HOOD, and PLTR performed well, while NKE excelled among discretionary stocks. Even though rates went up, the dollar didn’t rise significantly, indicating cautious behavior. We expect a slow trading day, with attention on stock positioning for 2026.

Gold And Currency Movements

Gold prices climbed toward $4,350, driven by expectations of Federal Reserve rate cuts and geopolitical tensions. Currency pairs like USD/JPY and EUR/USD showed minor changes due to careful central bank policies as we near the end of 2025. This article offers financial insights but not specific investment advice. It acknowledges errors and limitations, urging readers to do their own research. FXStreet and the author do not provide personalized recommendations or take responsibility for investment choices based on this article. The S&P 500 has clearly rejected the 6,950s, making 6,936 a key resistance level now. As sellers gain control towards the end of 2025, we should keep an eye out for continued weakness below this level. If we don’t manage to reclaim and hold above 6,936 in the coming sessions, consider buying puts or setting up put debit spreads on the SPY or ES futures.Market Volatility And Stock Divergence

Volatility is expected to rise after the holiday break, and recent selling might be more than just year-end tax adjustments. The VIX, which stayed in the low teens for much of late 2025, has risen to 15.2, showing increasing uncertainty. We could use VIX call options as a low-cost hedge against a possible market drop in the first quarter. The market is clearly showing differences, so we should concentrate on individual stock opportunities rather than betting on broad indexes. For instance, Nike’s strength stands out against the weakness seen in the overall consumer discretionary ETF (XRT), impacted by record-high consumer credit card debt exceeding $1.15 trillion at the end of 2025. A pairs trade—buying NKE calls and XRT puts—might capitalize on this trend. Keep a close watch on the US Dollar Index, which struggled to stay above 98.30 even as short-term rates rose last year. A weak dollar is usually good news for large-cap companies with significant overseas sales, as it increases the value of their foreign earnings. If the dollar continues its weak trend from late 2025, look for opportunities in call options on multinational tech and industrial companies. Create your live VT Markets account and start trading now.The S&P 500’s strong upward trend started from the cyclical panic low of 3492.

The S&P 500 had a strong rally from a low of 3492, climbing to 6165. This surge was backed by plenty of liquidity and support from institutional investors. After a dip to 4842, which was close to the pre-COVID high of 4804, the index consolidated. This was a moment when more funds started investing, and hedging activities declined.

From the range of 4842-4804, the index jumped to 7000. This rise was driven by trend-following strategies and less volatility. However, the pattern above 6900 showed signs of “parabolic exhaustion.” Leveraged funds took short positions as protection while dealers absorbed institutional demand, noted in shifting COT structure.

Market Trend Analysis

As the index approaches 7000 and aims for 7240, it appears to be late in the current cycle. If it goes past 7240 with strong volume, it might face resistance between 7480-7550, with 7800 being a key target. A pullback from 7240 could lead to a decline to 6600-6420 or even 5140, which corresponds with the midpoint of the 3492-7000 range, all while maintaining a long-term bullish trend. The long-term trend remains positive; however, exhaustion is setting in. A pullback from 7240 is likely to happen before the index attempts to climb above 7800. Traders should prepare for volatility, shifts in hedging, and a correction phase before the next rise. The rally beginning from the 3492 panic low is still the key long-term driver, and the market is now close to a crucial point near 7000. This surge has been bolstered by years of liquidity and a drop in volatility, which has pushed the S&P 500 into what looks like a late vertical rise. We have seen similar movements before, especially during the late 2025 surge, which led to the levels we see today.Investment Strategies in a Bull Market

As the index nears the 7240 resistance level, signs of exhaustion are becoming clearer, presenting opportunities for derivative traders. The CBOE Volatility Index (VIX) has remained low, closing 2025 with several weeks below 14. This usually suggests high complacency right before a jump in volatility. It indicates that option premiums, especially for puts, are relatively inexpensive ahead of a potential pullback. Market indicators from the fourth quarter of 2025 support a cautious approach. The NYSE Advance-Decline line did not confirm the index’s new highs, showing a bearish divergence with fewer stocks participating in the rally. This situation resembles the market conditions of late 1999, just before the major drop in 2000. Consequently, positioning for a sharp pullback by buying out-of-the-money put spreads targeting a decline to 6600 could provide a favorable risk-reward scenario. A correction from the 7240 area would act as a healthy reset, not the end of the primary bull trend. This kind of move would likely expand implied volatility, making it a great time to hedge long-only portfolios. A decline toward the 6600-6420 support zone would match a typical technical retracement. Once the correction stabilizes, probably in the coming months, the focus should shift back to the long-term upward trend. The ultimate target for this cycle remains near 7800. Traders could then look to position for this final rise by selling expensive puts or starting bull call spreads to take advantage of renewed upward momentum. Create your live VT Markets account and start trading now.The S&P 500’s strong upward trend started from the cyclical panic low of 3492.

The S&P 500 had a strong rally from a low of 3492, climbing to 6165. This surge was backed by plenty of liquidity and support from institutional investors. After a dip to 4842, which was close to the pre-COVID high of 4804, the index consolidated. This was a moment when more funds started investing, and hedging activities declined.

From the range of 4842-4804, the index jumped to 7000. This rise was driven by trend-following strategies and less volatility. However, the pattern above 6900 showed signs of “parabolic exhaustion.” Leveraged funds took short positions as protection while dealers absorbed institutional demand, noted in shifting COT structure.

Market Trend Analysis

As the index approaches 7000 and aims for 7240, it appears to be late in the current cycle. If it goes past 7240 with strong volume, it might face resistance between 7480-7550, with 7800 being a key target. A pullback from 7240 could lead to a decline to 6600-6420 or even 5140, which corresponds with the midpoint of the 3492-7000 range, all while maintaining a long-term bullish trend. The long-term trend remains positive; however, exhaustion is setting in. A pullback from 7240 is likely to happen before the index attempts to climb above 7800. Traders should prepare for volatility, shifts in hedging, and a correction phase before the next rise. The rally beginning from the 3492 panic low is still the key long-term driver, and the market is now close to a crucial point near 7000. This surge has been bolstered by years of liquidity and a drop in volatility, which has pushed the S&P 500 into what looks like a late vertical rise. We have seen similar movements before, especially during the late 2025 surge, which led to the levels we see today.Investment Strategies in a Bull Market

As the index nears the 7240 resistance level, signs of exhaustion are becoming clearer, presenting opportunities for derivative traders. The CBOE Volatility Index (VIX) has remained low, closing 2025 with several weeks below 14. This usually suggests high complacency right before a jump in volatility. It indicates that option premiums, especially for puts, are relatively inexpensive ahead of a potential pullback. Market indicators from the fourth quarter of 2025 support a cautious approach. The NYSE Advance-Decline line did not confirm the index’s new highs, showing a bearish divergence with fewer stocks participating in the rally. This situation resembles the market conditions of late 1999, just before the major drop in 2000. Consequently, positioning for a sharp pullback by buying out-of-the-money put spreads targeting a decline to 6600 could provide a favorable risk-reward scenario. A correction from the 7240 area would act as a healthy reset, not the end of the primary bull trend. This kind of move would likely expand implied volatility, making it a great time to hedge long-only portfolios. A decline toward the 6600-6420 support zone would match a typical technical retracement. Once the correction stabilizes, probably in the coming months, the focus should shift back to the long-term upward trend. The ultimate target for this cycle remains near 7800. Traders could then look to position for this final rise by selling expensive puts or starting bull call spreads to take advantage of renewed upward momentum. Create your live VT Markets account and start trading now.<Click here to set up a live account on VT Markets now

US dollar rises above 156.50, putting pressure on Japanese yen due to BoJ’s cautious policies

The USD/JPY rose to about 156.75 during the early Asian session on Friday. The Japanese Yen weakened against the US Dollar due to the slow pace of the Bank of Japan’s monetary tightening.

The Bank of Japan increased its policy rate to 0.75% from 0.50%, the highest rate in 30 years. However, traders were disappointed by the lack of guidance on future rate increases, which negatively affected the Yen.

Potential Risks to the USD

The US Federal Reserve may cut interest rates further by 2026, posing a risk to the US Dollar against the Yen. President Trump’s support for a dovish Federal Reserve Chair raises concerns about the Fed’s independence. The Yen is influenced by the Bank of Japan’s policies, bond yield differences, and market sentiment. The recent easing of the BoJ’s ultra-loose policy offers some support to the Yen against other major currencies. During stressful times, the Yen is seen as a reliable choice. The BoJ’s gradual policy changes and interest-rate cuts in other countries also affect currency movements. The outlook for USD/JPY depends on central bank policies and overall market sentiment. Financial markets are closely watching upcoming decisions from both the Bank of Japan and the US Federal Reserve.Market Disappointment Continues

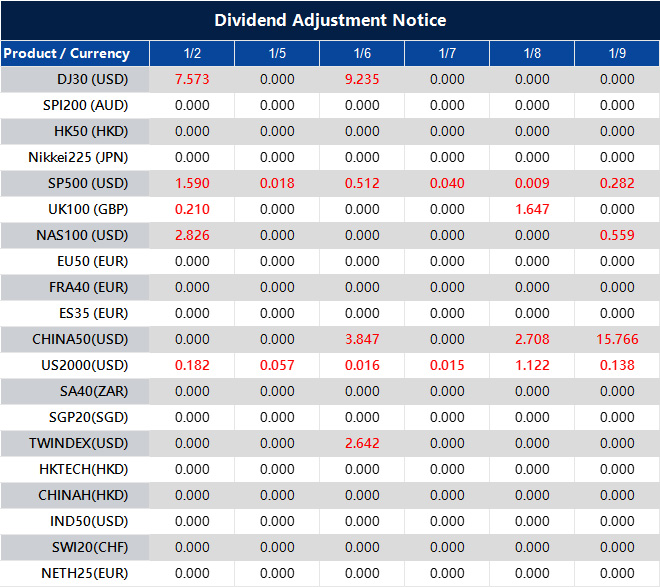

With USD/JPY near 156.75, the market’s disappointment in the Bank of Japan’s slow pace is clear. The BoJ’s small rate hike to 0.75% in December 2025 didn’t provide enough tightening to strengthen the Yen. This cautious approach continues to support a stronger Dollar against the Yen for now. However, we must also consider the pressure on the US Dollar. In 2025, the Federal Reserve cut rates three times. The latest jobs report from December 2025 showed only 155,000 jobs added, which raises the likelihood of more cuts. This situation suggests that the upward movement of USD/JPY may be limited in the coming weeks. Given the weak Yen and a potentially weakening Dollar, traders should think about strategies that benefit from increased volatility. Options strategies like straddles could work well, especially given the political uncertainty surrounding the Fed’s leadership, which could cause sharp price movements. The current high price makes long positions risky. Historically, we are nearing levels that have led to market intervention. The last time USD/JPY was this high was during the significant interventions of 2024, and before that, in 1990 when it exceeded 160. This suggests that purchasing far out-of-the-money call options could be a costly mistake if authorities decide to intervene to support the Yen. On the Japanese side, recent data shows that Tokyo’s core inflation for December 2025 remained at 2.4%, staying above the BoJ’s 2% target for more than a year and a half. This ongoing inflation puts pressure on the central bank to act more decisively than indicated in their December meeting. Any sign of an accelerated rate hiking schedule would likely strengthen the Yen quickly. Meanwhile, uncertainty about the Fed’s independence is a major concern. As we start 2026, the CME FedWatch Tool shows a 22% chance of a rate cut in the January meeting. This reflects growing market worry that political pressure could influence the Fed, which may limit how high USD/JPY can rise. Create your live VT Markets account and start trading now.Dividend Adjustment Notice – Jan 02 ,2026

Dear Client,

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

In December, Australia’s S&P Global Manufacturing PMI fell from 52.2 to 51.6.

Australia’s S&P Global Manufacturing PMI dropped to 51.6 in December, down from 52.2 in November. This decline suggests a slowdown in manufacturing, indicating possible challenges as the year comes to a close.

The PMI is a key indicator of the manufacturing sector’s health, based on surveys from private firms. A score above 50 indicates growth, while below 50 signals a decline. The current decrease raises concerns about economic stability and future growth.

Year Ended Analysis

As 2025 wraps up, all eyes will be on manufacturing for insights into Australia’s wider economic trends. Analysts will closely watch how this PMI drop impacts other sectors and the economy as we move into 2026. The December 2025 PMI of 51.6 still shows expansion but signals a slowdown for the Australian economy. This could present challenges for the S&P/ASX 200, especially for industrial and materials companies, which are sensitive to economic changes. We are considering protective measures, like buying put options on the XJO index, to guard against a potential market downturn in early 2026. This economic slowdown is putting pressure on the Australian dollar, which is also influenced by outside factors. Iron ore prices, a key export, fell below $110 USD per tonne in the last quarter of 2025 due to weaker demand from China. As a result, we are exploring bearish positions on the AUD/USD pair—possibly through futures contracts—anticipating the currency may drop further.Reserve Bank Of Australia Considerations

The weak manufacturing data will play a significant role in upcoming meetings of the Reserve Bank of Australia (RBA). After keeping the cash rate steady at 4.35% through late 2025, this new information makes additional rate hikes less likely. Traders should watch the bond market since expectations for a more cautious RBA could create attractive opportunities in Australian government bond futures. This manufacturing slowdown isn’t happening in a vacuum; retail sales growth was flat in November 2025, according to the Australian Bureau of Statistics. This trend of weakening consumer and business activity suggests increased economic uncertainty ahead. Increased market volatility is likely, making strategies that benefit from price swings, such as VIX-related derivatives, worth considering. Create your live VT Markets account and start trading now.In December, Australia’s S&P Global Manufacturing PMI fell from 52.2 to 51.6.

Australia’s S&P Global Manufacturing PMI dropped to 51.6 in December, down from 52.2 in November. This decline suggests a slowdown in manufacturing, indicating possible challenges as the year comes to a close.

The PMI is a key indicator of the manufacturing sector’s health, based on surveys from private firms. A score above 50 indicates growth, while below 50 signals a decline. The current decrease raises concerns about economic stability and future growth.

Year Ended Analysis

As 2025 wraps up, all eyes will be on manufacturing for insights into Australia’s wider economic trends. Analysts will closely watch how this PMI drop impacts other sectors and the economy as we move into 2026. The December 2025 PMI of 51.6 still shows expansion but signals a slowdown for the Australian economy. This could present challenges for the S&P/ASX 200, especially for industrial and materials companies, which are sensitive to economic changes. We are considering protective measures, like buying put options on the XJO index, to guard against a potential market downturn in early 2026. This economic slowdown is putting pressure on the Australian dollar, which is also influenced by outside factors. Iron ore prices, a key export, fell below $110 USD per tonne in the last quarter of 2025 due to weaker demand from China. As a result, we are exploring bearish positions on the AUD/USD pair—possibly through futures contracts—anticipating the currency may drop further.Reserve Bank Of Australia Considerations

The weak manufacturing data will play a significant role in upcoming meetings of the Reserve Bank of Australia (RBA). After keeping the cash rate steady at 4.35% through late 2025, this new information makes additional rate hikes less likely. Traders should watch the bond market since expectations for a more cautious RBA could create attractive opportunities in Australian government bond futures. This manufacturing slowdown isn’t happening in a vacuum; retail sales growth was flat in November 2025, according to the Australian Bureau of Statistics. This trend of weakening consumer and business activity suggests increased economic uncertainty ahead. Increased market volatility is likely, making strategies that benefit from price swings, such as VIX-related derivatives, worth considering. Create your live VT Markets account and start trading now.<Click here to set up a live account on VT Markets now

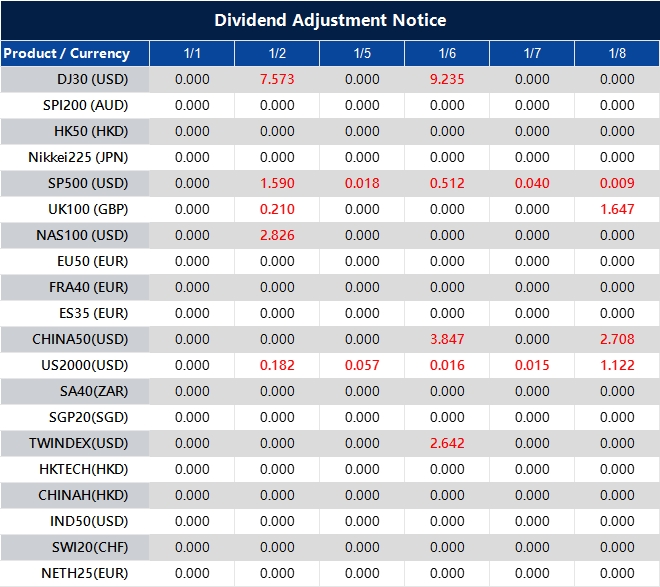

Dividend Adjustment Notice – Jan 01 ,2026

Dear Client,

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

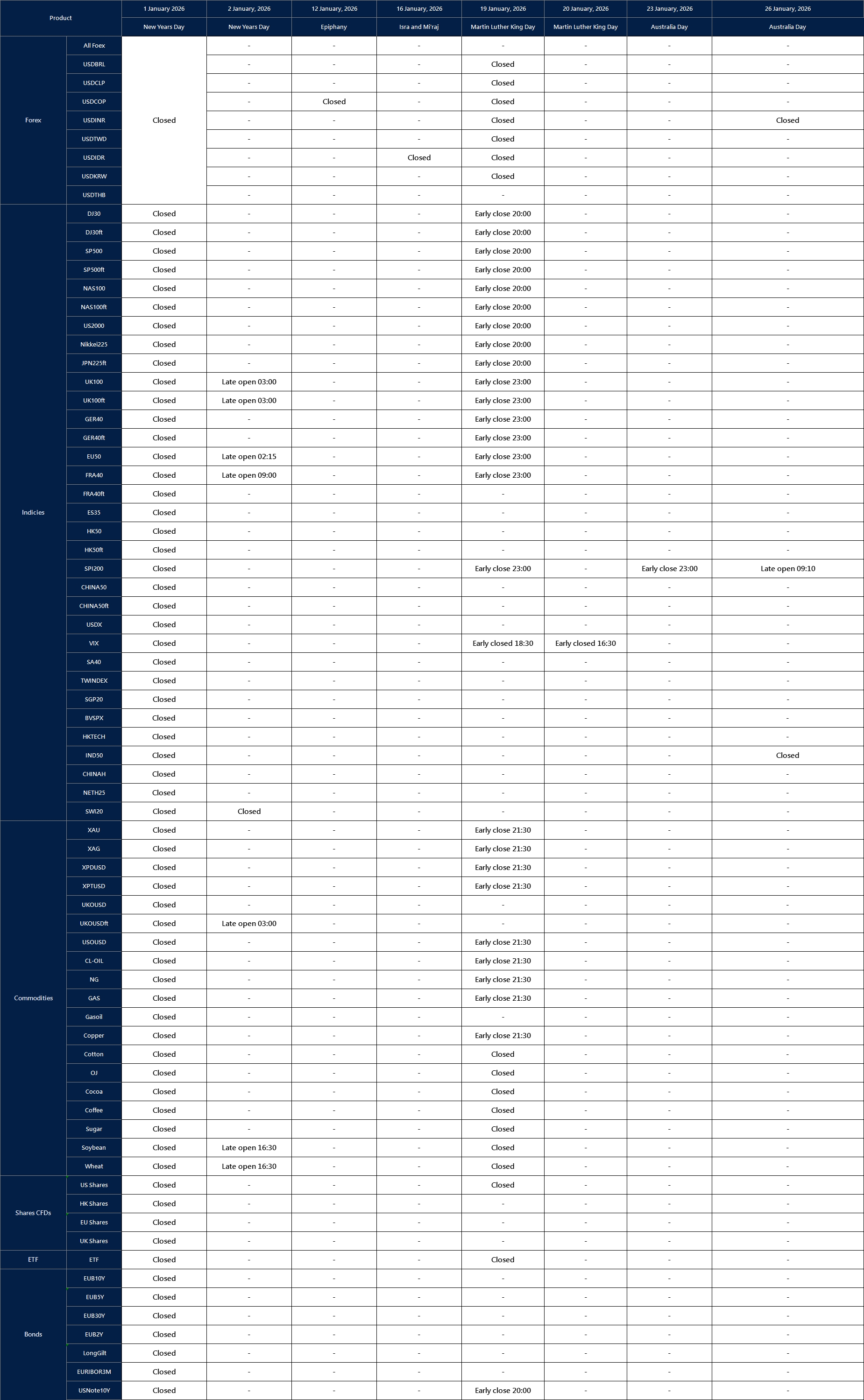

Holiday Trading Adjustment Notice – Jan 01 ,2026

Dear Client,

Affected by international holidays, the trading hours of some VT Markets products will be adjusted. Please check the following link for the affected products:

Holiday Trading Adjustment Notice

Note: The dash sign (-) indicates normal trading hours.

Friendly Reminder:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected]

{kind=link}