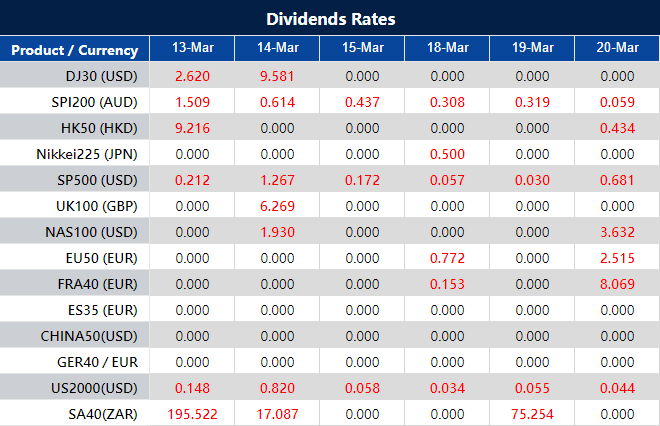

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

On Tuesday, financial markets experienced significant gains following the release of U.S. inflation data that aligned with expectations, fueling a surge in tech stocks like Nvidia, Meta Platforms, and Oracle. The Dow Jones, S&P 500, and Nasdaq all posted notable increases, with the S&P 500 hitting a new record high. Meanwhile, the consumer price index’s rise mirrored forecasts, sustaining investor hopes for a Federal Reserve rate cut in June. In the currency sector, the dollar strengthened against major currencies, reacting to the inflation report and Treasury yield movements, setting the stage for the upcoming Fed meeting and economic indicators release.

Stock Market Updates

On Tuesday, the stock market witnessed notable gains, driven by U.S. inflation data that aligned with expectations, fueling investor enthusiasm towards tech giants such as Nvidia and Meta Platforms. The Dow Jones Industrial Average rose by 235.83 points (0.61%) to 39,005.49, the S&P 500 increased by 1.12% to a record close of 5,175.27, and the Nasdaq Composite advanced by 1.54% to 16,265.64. Notable movers included Nvidia, which jumped over 7%, Microsoft and Meta with increases of 2.6% and 3.3% respectively, and Oracle, which surged more than 11% following earnings that surpassed Wall Street’s forecasts.

The inflation update, with the consumer price index (CPI) rising by 0.4% for February and 3.2% year-over-year, was closely watched by the market. These figures met economists’ expectations and signaled a stabilizing inflation environment, albeit with core inflation rising slightly above forecasts at 0.4%. This data prompted analysts to maintain their outlook for a potential Federal Reserve rate cut in June, despite acknowledging the unpredictable path to the Fed’s 2% inflation target.

Currency Market Updates

In the currency markets, the dollar index experienced a slight uplift of 0.2%, responding to the inflation data that pushed Treasury yields higher and adjusted the market’s expectations for Federal Reserve rate cuts in 2024. The yield on two-year Treasuries increased, and the overall sentiment shifted slightly, reducing the anticipated Fed rate cuts for the year, though a cut in June is still highly probable. The EUR/USD pair showed resilience, bouncing back after an initial drop, as market participants digested the implications of the CPI data and its impact on U.S. and European interest rate differentials.

Investors are now redirecting their focus towards other significant economic indicators and events, including the upcoming U.S. retail sales, Producer Price Index (PPI), and jobless claims reports. These data points, alongside the next Federal Reserve meeting scheduled for March 19-20, are expected to provide further clarity on the economic landscape and the central bank’s monetary policy direction. Additionally, the currency market remains attuned to developments around the globe, including the Bank of Japan’s potential rate decisions and the economic recovery signals from the U.S. and Europe.

As the financial world looks ahead, the anticipation builds for the Federal Reserve’s next moves, especially in light of recent economic data and global financial trends. The market’s reaction to the inflation reports, combined with upcoming economic indicators, underscores the delicate balance the Fed seeks to maintain between fostering economic growth and controlling inflation. With discussions and speculations around interest rate paths and policy adjustments, investors and analysts alike remain vigilant, ready to adapt to the evolving economic narrative.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD extends decline amidst US dollar resurgence and inflation concerns

The US Dollar’s (USD) continuous recovery has applied additional pressure on EUR/USD, resulting in the pair’s decline for the third consecutive session towards the 1.0900 support level. This movement coincides with the USD Index (DXY) experiencing an uptick to the 103.20 area, driven by higher-than-anticipated US Consumer Price Index (CPI) inflation figures. The resurgence in the Dollar is echoed by gains in US yields across various maturities, paralleled by the German 10-year bund yields nearing 2.35%.

With both the Federal Reserve (Fed) and the European Central Bank (ECB) anticipated to start their easing cycles in early summer, likely in June, the focus shifts to the pace at which interest rate cuts will unfold. Although the ECB may not significantly trail the Fed in this regard, the central banks’ strategies could highlight differences in their approaches to monetary policy easing.

Market sentiment, as gauged by the FedWatch Tool from CME Group, now shows an increased probability of about 60% for a rate cut in June. This adjustment in expectations comes amidst a backdrop where the solid resilience of the US economy starkly contrasts with the euro area’s more subdued fundamentals. This dynamic fosters a medium-term outlook favoring a stronger Dollar, especially with both central banks on the verge of commencing their easing programs nearly in tandem. Under such conditions, EUR/USD may face a deeper correction, initially aiming for its year-to-date low around 1.0700, with a potential extension towards the late October 2023/early November lows in the 1.0500 vicinity.

On Tuesday, the EUR/USD moved lower and reached the lower band of the Bollinger Bands. Currently, the price is moving just below the middle band, suggesting a potential higher movement, and may reach the upper band. Notably, the Relative Strength Index (RSI) maintains its position at 54, signaling a neutral outlook for this currency pair.

Sydney, Australia, 12 March, 2024 – VT Markets proudly proclaims the successful conclusion of its esteemed trading festival, the King of the Hill Trading Contest, which ran from November 2023 to January 2024. Building upon the momentum of the previous edition, this latest illustrious contest not only captivated the global trading fraternity but also set new standards of excellence and international camaraderie.

The King of the Hill Trading Contest 2023-2024 marked another milestone for VT Markets, with over a thousand participants from various corners of the world showcasing their trading prowess. This diverse participation underscored the truly global reach of VT Markets, as traders from different regions converged in a spirited competition.

This edition of the contest saw several millions of dollars being traded across the 3 months, demonstrating the scale and significance of the event within the trading community. While the focus remained on the thrill of competition and the pursuit of excellence, the contest also served as a platform for traders to engage, learn, and grow their skills.

Reflecting on the success of the contest, a spokesperson from VT Markets expressed gratitude towards the vibrant community of traders who contributed to its success. “The King of the Hill Trading Contest continues to surpass expectations, thanks to the passion and dedication of our participants,” said the spokesperson. “We are thrilled to see traders from around the world come together to compete and showcase their abilities. This event truly embodies the spirit of innovation and excellence that makes VT Markets special.”

One winner from Spain, wanting to be known as Lopez said, “Participating in the King of the Hill Trading Contest has been a transformative journey. It’s not just about profits; it’s about the camaraderie, the learning, and the sheer exhilaration of pushing one’s personal growth targets. VT Markets has truly crafted a platform that inspires greatness.”

As the competition concludes and the VT Markets team presents prizes to the winners of the King of the Hill Trading Contest, look ahead with excitement to future opportunities and initiatives. Traders are encouraged to stay tuned for upcoming campaigns and events that promise to deliver excitement and rewards.

For all the latest news and updates from VT Markets, please visit our official website and stay connected with us on social media. Thank you to all participants, supporters, and partners who made the King of the Hill Trading Contest a remarkable success.

About VT Markets:

VT Markets is a regulated multi-asset broker with a presence in over 160 countries. To date, it has won numerous international accolades including Best Customer Service and Fastest Growing Broker.

In line with its mission to make trading accessible to all, VT Markets currently offers unfettered access to over 1,000 financial instruments and a seamless trading experience via its award-winning mobile app.

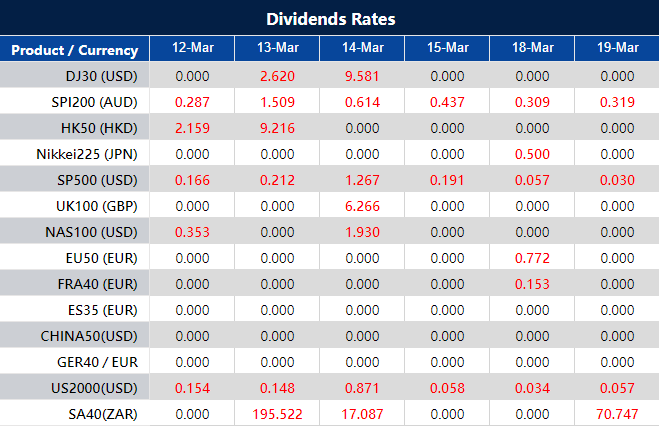

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

On Monday, the stock market saw mixed results as the recent rally slowed down. The S&P 500 and the Nasdaq Composite experienced declines, with technology stocks, including Super Micro Computer and Nvidia, facing notable losses. The Dow Jones, however, managed a slight increase. Concerns over the future performance of AI-related stocks and anticipation of the upcoming consumer price index report were key factors influencing the market’s movement. Additionally, the currency market observed the dollar index strengthening as investors awaited the CPI data, which could impact Federal Reserve’s rate decisions. Market analysts remain cautious, suggesting the Federal Reserve may need to maintain a careful approach to rate cuts in 2024.

Stock Market Updates

On Monday, the stock market experienced a slight downturn, interrupting the recent rally that had propelled major indexes to unprecedented heights. The S&P 500 edged down by 0.11% to close at 5,117.94, while the technology-heavy Nasdaq Composite dropped by 0.41% to end the day at 16,019.27. Both indexes recorded their second consecutive day of losses. Conversely, the Dow Jones Industrial Average managed to buck the trend by gaining 46.97 points, a modest increase of 0.12%, to close at 38,769.66.

In the tech sector, notable declines were seen in shares of Super Micro Computer, which fell by more than 5%, and Nvidia, down 2%, as investors began to question the sustainability of the recent surge in stocks linked to artificial intelligence. Meta Platforms, the parent company of Facebook, also faced a significant setback, dropping 4.4%. Additionally, the pharmaceutical giant Eli Lilly saw its stock decrease by over 3%.

These movements come as the market anticipates the release of the Consumer Price Index (CPI) for February, expected on Tuesday. According to forecasts by economists surveyed by Dow Jones, the CPI is projected to rise by 0.4% from January to February and by 3.1% on an annual basis. The core CPI, which excludes the volatile food and energy sectors, is anticipated to increase by 0.3% for the month and 3.7% annually.

Later in the week, the focus will shift to the producer price index, setting the stage for the Federal Reserve’s policy meeting in March. Some analysts, suggests that market optimism regarding the Fed’s capacity to cut rates in 2024 may be premature, with the upcoming inflation data likely reinforcing the need for a cautious approach by the Fed.

Currency Market Updates

In the currency markets, the dollar index saw a slight increase of 0.18% on Monday, stabilizing after the previous week’s decline. This adjustment comes as investors eagerly await the CPI report, which could clarify the current disparity between market expectations of nearly four rate cuts this year and the Fed’s December projections of three cuts.

The EUR/USD pair dipped slightly by 0.15%, maintaining its position above 1.0900 following a rally last week. The anticipation of the CPI data and its potential impact on the Federal Reserve’s next moves adds to the cautious sentiment observed in the currency markets.

Moreover, the New York Fed’s consumer survey highlighted rising inflation expectations over the next three to five years, predominantly among respondents with a high school education or less, further complicating the economic outlook.

As the financial world braces for the upcoming CPI report and its implications for interest rate decisions, the stock and currency markets reflect a mix of caution and anticipation. The outcomes of these economic indicators will likely play a crucial role in shaping the Federal Reserve’s policy direction in the coming months, with significant ramifications for investors and the broader economy.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD faces pressure as US dollar rebounds amid easing cycle anticipations

The US dollar’s modest rebound has put EUR/USD on the back foot, marking the start of the new trading week with its second day of losses. This comes as investors digest the latest US Non-farm Payrolls report, which showed a significant job addition but with a slight uptick in the jobless rate and a cooling in wage inflation. The dollar’s recovery is mirrored by a modest increase in US yields and the German 10-year bund yields climbing back to 2.30%.

Both the Federal Reserve and the European Central Bank are expected to begin their easing cycles in June, with the pace of interest rate reductions potentially setting them apart. Despite the ECB’s cautious stance, as expressed by Board member P. Kazimir, it’s unlikely to lag significantly behind the Fed in easing measures. With market expectations leaning towards a June rate cut, the economic fundamentals of the euro area, in comparison to the US’s resilience, suggest a stronger dollar in the medium term. This scenario could lead EUR/USD towards a deeper correction, initially aiming for its year-to-date low around 1.0700 and possibly extending towards late 2023 lows in the 1.0500 range.

On Monday, the EUR/USD moved lower and was able to reach the middle band of the Bollinger Bands. Currently, the price is moving at the middle band, suggesting a potential consolidation movement and may create narrower bands. Notably, the Relative Strength Index (RSI) maintains its position at 57, signaling a neutral outlook for this currency pair.

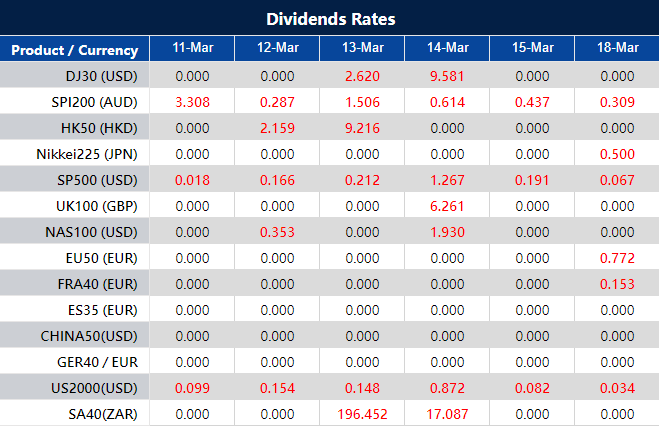

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

As we approach the week starting February 12, 2024, the financial community is on high alert, gearing up for a series of pivotal economic updates. These reports are crucial as they could significantly influence central bank decisions in the near term, particularly those of the Federal Reserve and the Bank of England. With the backdrop of ongoing global economic adjustments, the forthcoming data releases are set to provide critical insights into the current economic landscape.

The spotlight this week is on the US and UK, with both nations poised to release vital inflation and GDP figures. For the US, the Consumer Price Index (CPI) data stands out as a key indicator, offering fresh insights into inflation trends and potentially guiding the Federal Reserve’s rate cut expectations. Market participants are keenly awaiting this update, especially after recent labor market data suggested a more robust economic stance than anticipated.

In the UK, the focus shifts to a comprehensive economic update, including Q4 GDP figures, January inflation data, and labor market statistics. These releases are especially significant as they could hint at whether the UK economy is edging towards a recession, a scenario that would have profound implications for monetary policy and market sentiment.

Additionally, the Eurozone is not to be overlooked, with its own set of economic indicators due for release. Employment and industrial production figures will be closely watched for signs of economic resilience or weakness, potentially impacting Eurozone GDP revisions and broader market expectations.

For market analysts and forex traders, these developments are of paramount importance. The US CPI data, alongside the UK’s economic updates, not only shed light on the respective economies’ health but also offer valuable cues for currency market dynamics and trading strategies. Understanding these indicators is essential for navigating the complexities of the global financial markets effectively.

Key Highlights for the Week:

US CPI Data: A critical measure of inflation that could influence Federal Reserve rate cut expectations.

UK Economic Updates: Including Q4 GDP, January inflation, and labor market statistics, providing a comprehensive view of the UK’s economic health.

Eurozone Indicators: Employment and industrial production figures could signal economic trends and impact GDP revisions.

As we delve into this significant week, staying informed and agile is crucial for market participants. The upcoming economic indicators and central bank insights will not only enhance understanding of the current economic environment but also assist in refining trading strategies and market approaches.

Stay Ahead with Insightful Analysis: Keep abreast of these developments with our expert commentary and analysis, ensuring you’re well-equipped to make informed decisions in the ever-evolving financial markets.

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

On Thursday, the stock market witnessed significant gains, with the S&P 500 and Nasdaq Composite reaching new record highs, driven by investor optimism over easing inflation and robust gains in the technology sector. The S&P 500 increased by 1.03% to 5,157.36, while the Nasdaq Composite climbed 1.51% to 16,273.38, marking a notable recovery for Wall Street midweek. This positive momentum was fueled by optimistic global inflation trends signaled by the European Central Bank’s updated forecasts and Federal Reserve Chair Jerome Powell’s hints at potential interest rate cuts within the year. Additionally, the upcoming U.S. jobs report is eagerly awaited for further insights into the labor market’s resilience. The day’s market performance was also influenced by significant movements in the currency market, following dovish indications from the Federal Reserve, impacting major currency pairs and contributing to a cautiously optimistic market sentiment.

Stock Market Updates

Stocks experienced a notable rise on Thursday, propelling the S&P 500 and Nasdaq Composite to new record highs, fueled by optimism regarding easing inflation and a surge in technology sector gains, contributing to Wall Street’s recovery midweek. The S&P 500 ascended by 1.03% to reach 5,157.36, and the Nasdaq Composite saw a 1.51% increase to 16,273.38, both marking record highs during the trading session, with the S&P 500 also achieving a record close. The Dow Jones Industrial Average experienced a more modest rise, gaining 130.30 points, or 0.34%, to conclude at 38,791.35. Leading the charge in the S&P 500, information technology, and communication services stocks, particularly Intel, stood out with a gain of over 3%, highlighting the sector’s significant contribution to the day’s positive market performance.

Fueling investor optimism, the European Central Bank (ECB) revised its forecasts to show lower expected annual inflation and growth rates, yet maintained steady key interest rates, a move interpreted as a positive indicator concerning global inflation trends. This development followed Federal Reserve Chair Jerome Powell’s address to Congress, where he anticipated a reduction in interest rates within the year, despite not being immediately prepared to initiate cuts. He expressed to the Senate Banking Committee that the Federal Reserve was nearing the confidence needed concerning inflation to commence rate reductions. Meanwhile, the market’s attention is drawn towards the upcoming U.S. jobs report, seeking insights into the labor market’s condition amidst ongoing resilience against the backdrop of higher interest rates. Notably, while the S&P 500 and Nasdaq displayed weekly gains, the Dow still faced a slight decline, underscoring the mixed yet cautiously optimistic sentiment prevailing in the market.

Currency Market Updates

The currency market saw significant movements following dovish signals from the Federal Reserve, as outlined by Fed Chair Jerome Powell during his congressional testimony. Powell’s indication of a potential rate cut in 2024, bolstered by his confidence in nearing the Fed’s 2% inflation target, led to a downward adjustment in the USD index, which fell by 0.38%. This dovish stance was further echoed in the adjustments of short-term interest rate futures, with expectations now set for 92 basis points of cuts by the December 18 FOMC meeting. This shift in sentiment has reversed some of the dollar’s gains from February, influencing major currency pairs, notably with the EUR/USD rallying by 0.34% to 1.0934, despite the European Central Bank’s (ECB) decision to hold rates steady and a somewhat less dovish commentary from ECB President Christine Lagarde.

In the Asian currency markets, the USD/JPY pair witnessed a notable decline, dropping by 0.87% to 148.09, influenced by the dovish Fed outlook and speculative adjustments ahead of the Bank of Japan’s (BoJ) meeting. Market participants are closely watching for any signs of a policy shift by the BoJ, which could predate the Fed’s anticipated rate cuts. Meanwhile, the GBP/USD pair reached a new high for 2024 at 1.2798, buoyed by the relative firmness of the pound against a backdrop of dovish stances from both the ECB and the Fed, and sustained by higher UK inflation expectations relative to the U.S. and the Eurozone. Additionally, broader market movements were seen in the rise of Bitcoin and gold prices, both benefiting from the lower rate environment suggested by the Fed’s dovish outlook, highlighting the interconnectedness of global financial markets and the significant impact of central bank policies on currency valuations.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD breaks past 1.0900 amidst dovish central bank outlooks and weak US dollar

EUR/USD has successfully breached the significant 1.0900 level, reaching multi-week highs as the US dollar faces heightened selling pressure following Chair Jerome Powell’s testimony and disappointing US labor market data. The US dollar index (DXY) continued its decline for the fifth session, hitting five-week lows, amidst ongoing speculation of a Fed rate cut in June. Concurrently, German 10-year bund yields hit multi-week lows after the ECB maintained interest rates, reflecting a cautious market sentiment.

Fed Chair Powell’s comments hinted at potential interest rate cuts within the year, contingent on a confident trajectory towards the 2% inflation target, with market expectations of a June rate cut rising to 60%. Meanwhile, the ECB’s steady outlook forecasts moderate economic growth and a gradual reduction in inflation, despite acknowledging challenges such as labor demand slowdown and domestic price pressures.

Despite the ECB’s and the Fed’s dovish stances potentially indicating the start of easing cycles, the stagnant euro area fundamentals against the backdrop of the resilient US economy suggest a stronger dollar in the medium term. This dynamic sets the stage for a possible deeper correction in EUR/USD, targeting its year-to-date low around 1.0700 and potentially extending towards late 2023 lows in the 1.0500 area, reflecting the nuanced interplay of monetary policies and economic indicators in currency market movements.

On Thursday, the EUR/USD moved higher and was able to reach the upper band of the Bollinger Bands. Currently, the price is moving just below the upper band, suggesting a potential upward movement to reach above the next resistance level. Notably, the Relative Strength Index (RSI) maintains its position at 71, signaling a bullish outlook for this currency pair.