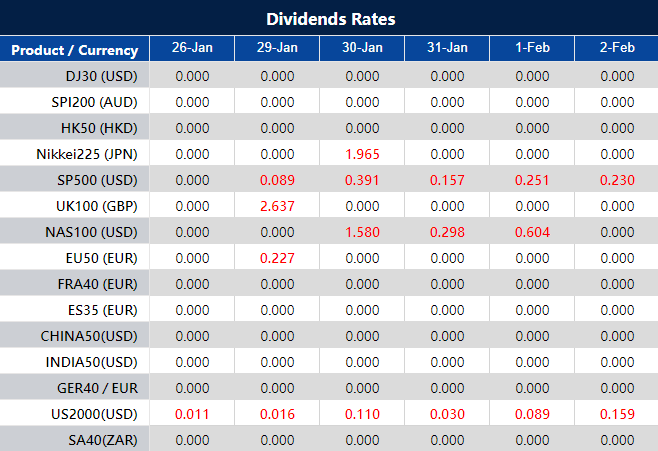

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

The S&P 500 achieved a new record high, climbing to 4,927.93, driven by anticipation of major tech company earnings and the upcoming Federal Reserve rate policy decision. This week is pivotal with 19% of S&P 500 companies, including tech giants like Microsoft and Apple, due to report earnings. The Dow Jones and Nasdaq also saw significant gains. Concurrently, the Federal Open Market Committee is expected to maintain steady rates, with a 97% probability against a rate cut. In currency markets, the dollar index rose, influenced by various global events and market uncertainties. The Euro and Japanese yen weakened against the dollar, while the Sterling remained stable. These financial movements occur amidst global geopolitical tensions and economic concerns, notably in China and the Eurozone.

Stock Market Updates

On Monday, the S&P 500 achieved a new record high, driven by anticipation of tech giant earnings reports and the upcoming Federal Reserve rate policy decision. The index rose 0.76% to 4,927.93, surpassing its previous record close of 4,894.16 set on January 25. Similarly, the Dow Jones Industrial Average increased by 224.02 points (0.59%) to close at 38,333.45, while the Nasdaq Composite gained 1.12%, ending at 15,628.04. This marked the sixth record close for both the S&P 500 and the Dow.

The focus this week is on the earnings season, with 19% of the S&P 500 companies set to report their earnings. High-profile tech companies such as Microsoft, Apple, Meta, Amazon, and Alphabet, which have significantly contributed to this year’s market rally, are among those scheduled to release their results. Additionally, investors are keeping a close watch on earnings from major Dow components like Boeing and Merck. Meanwhile, the Federal Open Market Committee is commencing its two-day policy meeting, with market participants almost certain that the Fed will maintain steady rates. According to the CME Group, there’s approximately a 97% probability that the Fed will not reduce rates in the upcoming meeting.

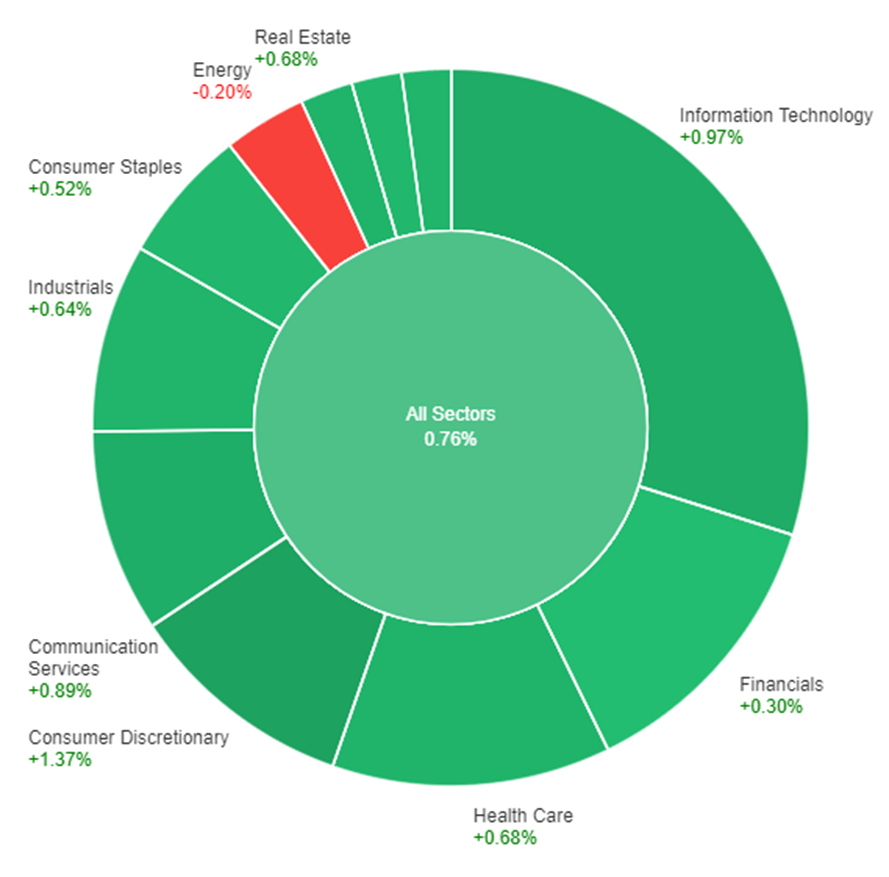

On Monday, the stock market experienced overall positive movement, with all sectors combined showing a gain of +0.76%. Notably, the Consumer Discretionary sector led the advances with a +1.37% increase, followed closely by Information Technology and Communication Services, which rose by +0.97% and +0.89% respectively. Health Care, Real Estate, Utilities, and Industrials also saw moderate gains, each climbing by approximately +0.68% and +0.64%. More modest growth was observed in Consumer Staples and Materials, both up by +0.52%, while Financials lagged slightly behind with a +0.30% increase. In contrast to the general upward trend, the Energy sector was the only one to experience a decline, dropping by -0.20%.

Currency Market Updates

In the recent currency market update, the dollar index experienced a 0.25% rise, largely driven by gains against major currencies, with the notable exception of the Japanese yen. This shift in the currency market comes amidst a variety of global events contributing to a heightened sense of risk. These include uncertainties surrounding key U.S. labor data, Eurozone inflation reports, and upcoming policy meetings of the Federal Reserve and the Bank of England. Additionally, increasing tensions in the Middle East and concerns over China’s economic future have added to the market’s cautious sentiment.

The Euro to U.S. Dollar (EUR/USD) pair saw a notable decline of 0.35%, significantly contributing to the dollar’s overall strength. This decline was influenced by weak economic conditions in Germany and a mild recession in the Eurozone. Moreover, a growing number of dovish European Central Bank policymakers has led the market to anticipate a 25 basis point rate cut by the ECB in April. The USD/JPY pair also experienced a 0.33% fall, influenced by a decrease in Treasury yields and a slight increase in Japanese Government Bond yields, challenging the uptrend driven by speculations and expectations of policy convergence between the Federal Reserve and the Bank of Japan. In addition to these currency movements, Sterling displayed a modest drop of 0.19%, maintaining its range for the seventh consecutive week, while oil prices fluctuated amid geopolitical tensions and concerns over Chinese economic stability.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Decline Amidst Dovish ECB Stance and Strong USD

The EUR/USD pair experienced a notable decline, falling below 1.0800 for the first time since mid-December, primarily due to the persistent strength of the US dollar and dovish signals from the European Central Bank (ECB). The ECB’s decision to leave policy rates unchanged, coupled with President Lagarde’s emphasis on a data-dependent approach and potential interest rate cuts in the summer, contributed to a subdued Euro. Contrasting views within the ECB, such as Board member Centeno’s unexpected support for earlier rate cuts, failed to reverse the Euro’s downward trend. Additionally, anticipation of the upcoming Federal Reserve meeting, with expectations of maintaining the Federal Funds Target Rate (FFTR) between 5.25%–5.50%, further pressured the EUR/USD. Investors are now focusing on the possibility of a US rate cut, potentially delayed to May, as indicated by the CME Group’s FedWatch Tool.

On Monday, the EUR/USD moved lower, able to reach the lower band of the Bollinger Bands. Currently, the price is moving higher near the middle band, suggesting a potential upward movement to reach the middle band. Notably, the Relative Strength Index (RSI) maintains its position at 42, signaling a neutral but bearish outlook for this currency pair.

Resistance: 1.0890, 1.0954

Support: 1.0814, 1.0745

XAU/USD (4 Hours)

XAU/USD React to Geopolitical Tensions and Economic Anticipations

Gold experienced a notable rise, reaching $2,037.46, influenced by a weakening US dollar and escalating tensions in Asia, particularly due to a drone attack on US troops in the Middle East, attributed to Iran. This geopolitical unrest, coupled with mixed stock market performances and anticipation of key economic events such as the Eurozone and German GDP reports, US employment data, and the US Federal Reserve’s monetary policy decision, kept investors on edge. Additionally, the market’s reaction to European Central Bank officials’ comments on interest rate expectations further shaped the trading landscape, maintaining a cautious but vigilant environment in the financial markets.

On Monday, XAU/USD moved higher and was able to reach the upper band of the Bollinger Bands. Currently, the price is moving higher slightly below the upper band suggesting a potential upward movement to reach above the upper band. The Relative Strength Index (RSI) stands at 57, signaling a neutral with a slightly bullish outlook for this pair.

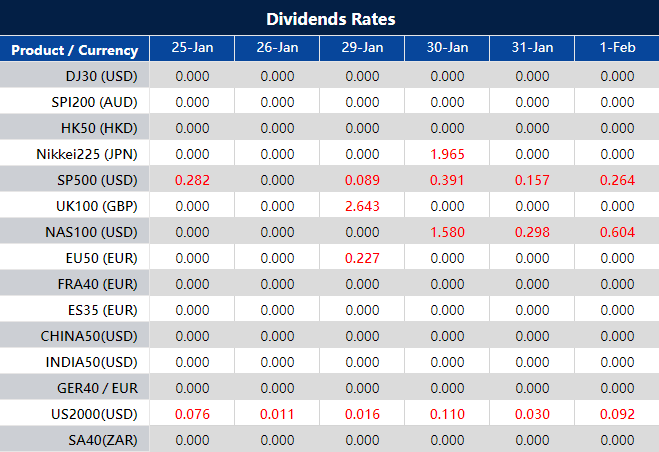

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

Looking ahead from the final week of January, traders and investors are gearing up for a bustling week filled with significant economic events. These developments are poised to shape market dynamics, with a particular focus on inflation trends, economic growth pace, and central bank strategies. Let’s delve into the crucial data points that will impact financial markets.

Australia’s Consumer Price Index (31 January 2024)

Market participants are closely monitoring the upcoming Consumer Price Index (CPI) data in Australia. After a dip in the year-on-year CPI from 4.9% in October 2023 to 4.3% in November 2023, the projected increase in CPI by 3.7% in December 2023 is of paramount importance. This inflation indicator holds significance as it could sway the Reserve Bank of Australia’s monetary policy decisions, potentially affecting the Australian Dollar.

Canada’s Gross Domestic Product (31 January 2024)

With stability observed in the Canadian economy over the past few months, the forthcoming Gross Domestic Product (GDP) data is expected to reflect a growth of 0.1%, serving as a key gauge of Canada’s economic well-being. Traders focused on the Canadian Dollar will closely analyse this release for insights into the Bank of Canada’s future monetary policy.

The Fed Interest Rate Decision (1 February 2024)

After maintaining the federal funds rate at 5.50% since December 2023, the Federal Reserve’s upcoming interest rate decision is highly anticipated. Despite previous indications of potential rate cuts in 2024, analysts expect the Fed to hold the rate steady. This decision is critical for the US Dollar and could significantly influence the equity and bond markets.

Bank of England Interest Rate Decision (1 February 2024)

Having maintained its benchmark interest rate at a 15-year high of 5.25% since December 2023, the Bank of England’s anticipated decision to hold steady will be crucial for the GBP. Given the divided vote in the previous meeting, any shifts in the voting pattern could offer insights into the central bank’s future policy direction.

US Jobs Report (2 February 2024)

The US jobs market, a focal point of attention, witnessed the addition of 216,000 jobs in December 2023, but with the unemployment rate holding steady at 3.7%. The January 2024 report, forecasted to show an addition of 173,000 jobs and a stable unemployment rate, will serve as a key indicator of the US economic health. This data holds substantial influence over the US Dollar and overall market sentiment, especially in light of the Federal Reserve’s monetary policy considerations.

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

In a week marked by mixed market performance, the S&P 500 soared to a new closing record, while the Nasdaq faced challenges due to Tesla’s post-earnings decline. Positive economic indicators, including robust U.S. GDP growth and encouraging inflation data, influenced market optimism. Despite the Federal Reserve’s interest rate hikes, a healthy balance of non-inflationary growth was observed. Notably, IBM’s stellar performance offset Tesla’s impact. In the currency market, the dollar index strengthened amid evidence of the U.S. outperforming Europe economically.

Stock Market Updates

The stock market exhibited mixed performance as the S&P 500 rose for the sixth consecutive day, setting another all-time closing record at 4,894.16. The Dow Jones Industrial Average also climbed by 0.64%, reaching 38,049.13 points. However, the Nasdaq Composite only increased by 0.18%, hindered by a post-earnings decline in Tesla shares. Despite the overall positive trend, Tesla’s disappointing fourth-quarter results led to a more than 12% drop in its stock, impacting the broader market. The technology-heavy Nasdaq, nevertheless, outperformed with a 1.3% weekly gain, while the S&P 500 and Dow posted increases of 1.1% and 0.5%, respectively.

The market was influenced by positive economic indicators, including the U.S. economy’s robust 3.3% growth rate in the fourth quarter, surpassing economists’ expectations of 2%. Additionally, encouraging data on inflation, with a 2% gain in the personal consumption expenditures price index (excluding food and energy), contributed to market optimism. Despite the Federal Reserve’s interest rate hikes, the data reflected a healthy mix of non-inflationary growth. Notably, IBM’s strong performance, with a more than 9% jump in its stock after beating analysts’ predictions for adjusted earnings and revenue, counterbalanced the negative impact of Tesla’s decline on the overall market. With over one-fifth of S&P 500 companies reporting financials this earnings season, nearly 74% have surpassed Wall Street expectations, according to FactSet.

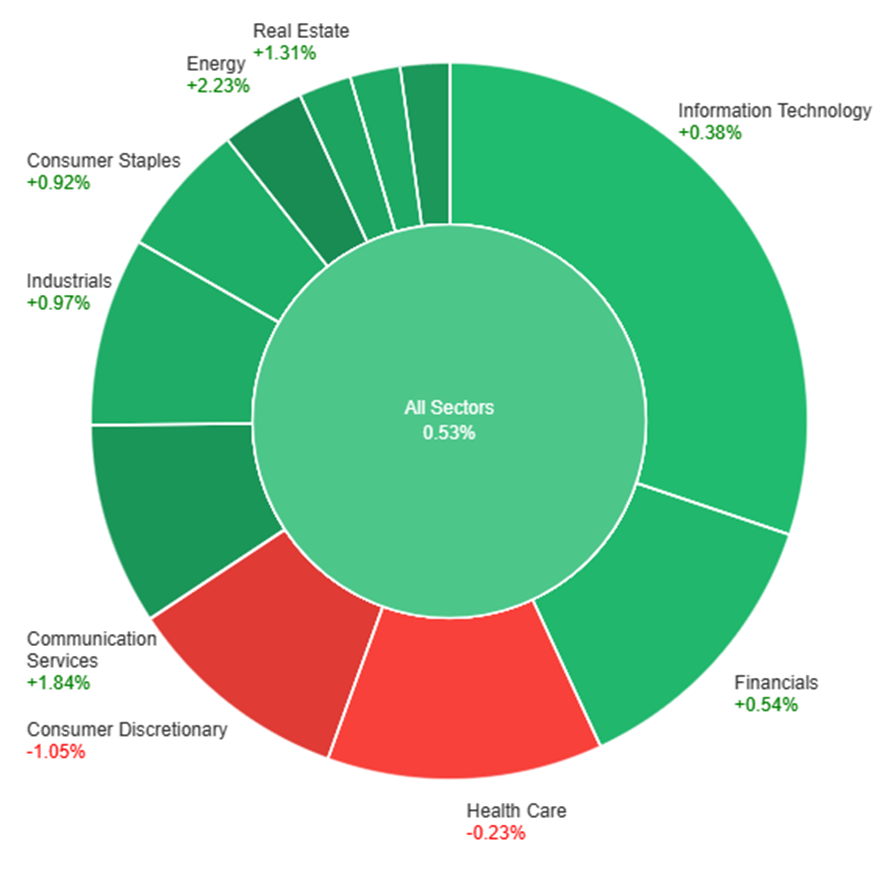

On Thursday, the overall market showed a positive trend with a gain of 0.53%. The Energy sector experienced the highest increase, surging by 2.23%, followed by Communication Services with a rise of 1.84%, and Utilities registering a gain of 1.79%. Real Estate also contributed to the upward movement, advancing by 1.31%, while Materials and Industrials increased by 1.09% and 0.97%, respectively. Consumer Staples and Financials showed modest gains of 0.92% and 0.54%, while Information Technology and Health Care had more conservative increases of 0.38% and a slight decrease of -0.23%, respectively. However, Consumer Discretionary recorded a decline of -1.05% on Thursday.

Currency Market Updates

In the currency market updates, the dollar index demonstrated strength, advancing by 0.3% as fresh evidence emerged showcasing the robust performance of the U.S. economy compared to Europe’s. The U.S. Q4 GDP growth exceeded expectations at 3.3%, while Germany’s Ifo data hinted at a lingering recession, and the UK experienced a significant decline in retail sales. The EUR/USD pair fell by 0.43%, despite the European Central Bank (ECB) opting to delay a rate cut, providing no clear guidance on unwinding its substantial rate-hiking cycle. The lack of clarity on when the eurozone inflation downtrend will prompt a shift in ECB policy raises concerns, especially if the economic situation worsens.

Amidst the data-driven decisions of central banks, the focus on Friday will be on the Federal Reserve’s preferred core Personal Consumption Expenditures (PCE) update. As the ECB, Fed, and Bank of England (BoE) navigate their monetary policies based on economic data, the currency market is witnessing fluctuations. USD/JPY rose by 0.14% as the Bank of Japan (BoJ) meeting on Tuesday left the potential for a rate hike in April. However, the Federal Reserve’s March decision remains uncertain. Other economic indicators, such as Tokyo CPI and U.S. core PCE, are anticipated to influence market dynamics, while geopolitical factors continue to impact oil prices and European natural gas trends.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Stays Steady Amid ECB News and Strong US Economy

The EUR/USD pair held its ground near 1.0900 as important events unfolded. The European Central Bank (ECB) decided not to change interest rates, sticking to its goal of reaching a 2% inflation target. However, the accompanying document didn’t provide new insights, keeping the pair in its usual range. In the US, the economy surprised with a strong 3.3% growth in Q4, beating the expected 2%. While the US Dollar initially got stronger, mixed data and positive stock market trends made its position varied across currencies. The upcoming press conference by ECB President Christine Lagarde might give more clues about the central bank’s plans and impact the direction of EUR/USD.

On Thursday, the EUR/USD moved lower, reaching the lower band of the Bollinger Bands. Currently, the price is moving just above the lower band, suggesting a potential upward movement to reach the middle band. Notably, the Relative Strength Index (RSI) maintains its position at 41, signaling a neutral but bearish outlook for this currency pair.

Resistance: 1.0890, 1.0954

Support: 1.0814, 1.0745

XAU/USD (4 Hours)

XAU/USD Steady Amid Economic Boost and Dovish Signals

Gold prices stayed steady even as the US Dollar got stronger due to the US economy growing by a better-than-expected 3.3%. This positive news made stocks rise, but interest rates stayed low. In Europe, the central bank didn’t change key interest rates, and its president, Christine Lagarde, shared a cautious message, making the US Dollar even stronger. People are now thinking that interest rates might go down soon. We’re waiting for the release of the December inflation numbers to see what might happen next.

On Thursday, XAU/USD moved lower and was able to reach the lower band of the Bollinger Bands. Currently, the price is moving higher near the middle band suggesting a potential upward movement to reach above the middle band. The Relative Strength Index (RSI) stands at 48, signaling a neutral outlook for this pair.

As part of our commitment to provide the most reliable service to our clients, there will be server maintenance this weekend.

Maintenance Hours :

27th of January 2024 (Saturday) 01:30-03:30 (GMT+2)

Please note that the following aspects might be affected during the maintenance:

1. Client portal and VT Markets App will be unavailable. In addition, all their functions will be limited.

2. The price quote and trading management on MT4 and MT5 will be temporarily disabled during the maintenance. You will not be able to open new positions, close open positions, or make any adjustments to the trades.

3. There might be a gap between the original price and the price after maintenance. The gaps between Pending Orders, Stop Loss and Take Profit will be filled at the market price once the maintenance is completed. If you don’t want to hold any open positions during the maintenance, it is suggested to close the position in advance.

4. Please refer to MT4/MT5 for the latest update on the completion and market opening time. Our services will be back online once the maintenance is completed.

Thank you for your patience and understanding about this important initiative.

If you’d like more information, please don’t hesitate to contact [email protected]

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

On Wednesday, the stock market exhibited a blend of movements as the S&P 500 set a new record high, driven by a technology stock rally led by Netflix. While the S&P 500 and Nasdaq Composite saw positive gains, the Dow Jones Industrial Average faced a slight decline due to notable drops in Verizon and 3M following earnings reports. Netflix’s remarkable 10% surge, supported by an all-time high subscriber count, contributed to the broader tech sector’s strength in 2024. Microsoft and Meta also made significant gains, pushing the S&P 500 to record levels and confirming a new bull market. However, not all companies shared in the positive momentum, with AT&T and DuPont De Nemours facing setbacks. In the currency market, the dollar index declined, influenced by China’s stimulus measures, impacting pairs like USD/JPY and EUR/USD. The article concludes with a look ahead at upcoming economic data releases, central bank meetings, and geopolitical factors influencing the dynamic currency market.

Stock Market Updates

The stock market experienced mixed movements on Wednesday, with the S&P 500 reaching a new record high, driven by a rally in technology stocks led by Netflix. The S&P 500 edged up 0.08% to close at 4,868.55, establishing a fresh all-time closing record, while the Nasdaq Composite gained 0.36%, marking the fifth consecutive day of positive performance for both indices. However, the Dow Jones Industrial Average slipped 0.26% to 37,806.39, impacted by notable declines in Verizon and 3M following their earnings reports. Netflix saw a significant surge of over 10% after announcing an all-time high subscriber count of 260.8 million and surpassing analysts’ revenue estimates, contributing to the broader tech sector’s strong performance in 2024.

In addition to Netflix’s positive impact, Microsoft’s shares rose nearly 1%, briefly pushing its market value above $3 trillion for the first time, while Meta advanced 1.4%, surpassing a $1 trillion market cap. These gains, along with the strong performance of communication services and information technology stocks, propelled the S&P 500 to record highs and confirmed a new bull market. However, not all companies shared in the positive momentum, with AT&T slipping about 3% due to lower-than-expected earnings, and DuPont De Nemours tumbling 14% after preannouncing weak fourth-quarter results and issuing disappointing first-quarter guidance. Traders continued to focus on earnings reports, with Tesla, Las Vegas Sands, and IBM scheduled to release results after the market close. As of the current earnings season, more than 71% of S&P 500 companies that have reported quarterly financials have exceeded Wall Street expectations, according to FactSet.

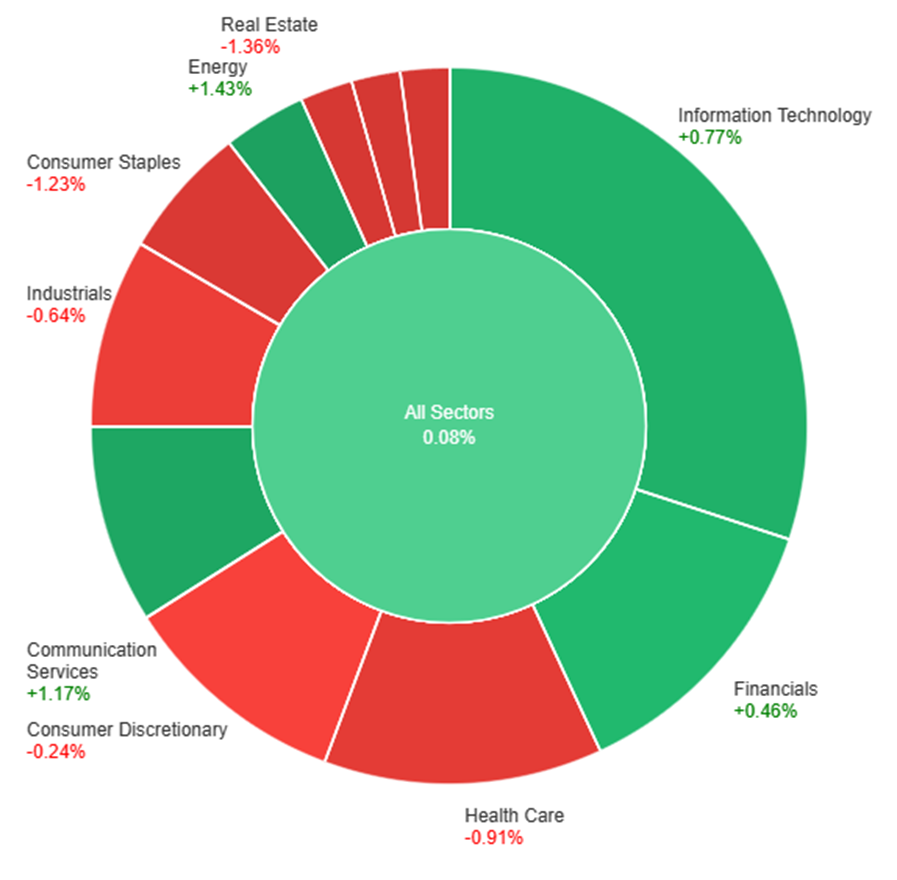

On Wednesday, the overall market saw a marginal increase of 0.08%. Notable positive performances were observed in the Energy sector, which gained 1.43%, followed by Communication Services at 1.17%, and Information Technology at 0.77%. Conversely, the

Consumer Staples, Real Estate, Utilities, and Materials sectors experienced declines of -1.23%, -1.36%, -1.38%, and -1.40%, respectively. The Consumer Discretionary sector also saw a modest decrease of -0.24%. Sectors such as Industrials and Health Care reported larger declines of -0.64% and -0.91%, respectively.

Currency Market Updates

In the currency market updates, the dollar index experienced a 0.45% decline, driven by risk-on sentiments influenced by China’s stimulus measures. The USD/JPY pair saw a significant drop due to rising Japanese Government Bond (JGB) yields in response to the Bank of Japan’s somewhat hawkish meeting earlier in the week. However, a rebound in U.S. flash Purchasing Managers’ Index (PMI) numbers contributed to lifting Treasury yields and helping the dollar recover from its lows. The EUR/USD pair rose by 0.38%, reaching a high of 1.0930 before the U.S. PMI release. The positive impact of the U.S. manufacturing and service sector readings beating forecasts was tempered by a cooling price received index.

Looking ahead, attention in the currency market is shifting to upcoming hard U.S. data ahead of the Federal Reserve meeting next week. Key events include Q4 GDP and jobless claims on Thursday, followed by core Personal Consumption Expenditures (PCE), income, and spending on Friday. Additionally, post-European Central Bank (ECB) meeting events on Thursday may provide hints regarding the timing of the first rate cut, which is currently favored for April. Tokyo CPI data on Friday will also be closely monitored amid speculation about a Bank of Japan rate hike, with April’s BoJ meeting seen as the earliest potential venue for such a move. The article also notes the market’s modest preference for a March Fed rate cut in futures. Overall, the currency market remains dynamic, responding to a combination of economic data releases, central bank meetings, and geopolitical developments.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Surges as Intense Greenback Sell-Off and Positive Economic Indicators Overpower Rate Cut Speculations

In a surprising turn of events, the intense sell-off in the greenback allowed EUR/USD to overcome recent weaknesses, pushing past the 1.0900 hurdle and reaching new multi-day highs. The USD Index (DXY) faced headwinds in the risk-friendly environment, dropping below 103.00 despite an uptick in US yields. Speculation shifted away from a Fed rate cut in March, favoring a reduction in May. Contributing to the Euro’s strength were robust PMIs in Germany and the eurozone for January, suggesting a potential soft landing for the regional economy. As the ECB event approaches, market participants are weighing in on potential rate cuts, with debates arising on the timing of the central bank’s decision, further fueled by President Lagarde’s hints at a move during the summer.

On Wednesday, the EUR/USD moved higher, able to reach the upper band of the Bollinger Bands. Currently, the price is moving back lower to reach below the middle band, suggesting a potential downward movement to reach the lower band. Notably, the Relative Strength Index (RSI) maintains its position at 47, signaling a neutral outlook for this currency pair.

Resistance: 1.0890, 1.0954

Support: 1.0814, 1.0745

XAU/USD (4 Hours)

US Dollar Strengthens as Upbeat Data Pushes Gold (XAU/USD) to Weekly Low

In the American session, the US Dollar gained momentum, driving Gold (XAU/USD) down to $2,011.72, marking a fresh weekly low. The surge was fueled by optimistic US economic data, particularly the January Producer Manager Indexes (PMIs) released by S&P Global. Manufacturing output improved to 50.3, surpassing the previous 47.9 and reaching the highest reading in over a year. The Services PMI also exceeded expectations at 52.9, indicating the sharpest business activity growth in seven months. While the Bank of Canada (BoC) left its key rate unchanged at 5%, the statement was slightly more hawkish, reducing the likelihood of an April rate cut. Despite this, stock markets maintained a positive tone, with Wall Street resuming its record rally on better-than-anticipated earnings reports, signaling overall economic health.

On Wednesday, XAU/USD moved lower and was able to reach the lower band of the Bollinger Bands. Currently, the price moving around the lower band suggesting a potential upward movement to reach the middle band. The Relative Strength Index (RSI) stands at 43, signaling a neutral outlook for this pair.

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].