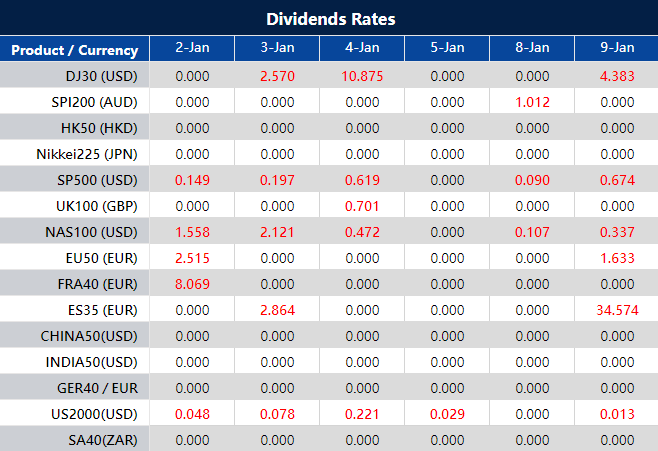

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

The inaugural week of 2024 is poised to be a dynamic period for traders and investors, with a spotlight on critical economic indicators that are expected to shape market sentiments. Among the pivotal data releases are the ISM Manufacturing and Services PMI from the US, the German Preliminary CPI from the EU, and the highly anticipated US and Canada Employment Change figures. This overview aims to guide you through the key developments and predictions, with a specific emphasis on the potential impact on major currencies, particularly the US Dollar.

It’s crucial for traders to be cautious and stay on top of the latest developments for a successful week of trading.

ISM Manufacturing PMI (3 January 2024)

The ISM Manufacturing PMI, holding steady at 46.7 in November 2023, is expected to modestly increase to 47.1 in the upcoming release on 3 January 2024.

FOMC Meeting Minutes (4 January 2024)

The Federal Reserve maintained the fed funds rate at 5.25%-5.5% for a third consecutive meeting in December 2023. However, they have hinted at a potential 75 basis points cut in 2024. Therefore the meeting minutes on 4 January 2024 will provide insights into the Fed’s latest monetary policy stance, reflecting the current economic indicators, including slowed growth, moderated job gains, and persistent but slightly eased inflation.

German Prelim CPI (4 January 2024)

After a 0.4% decline in November 2023, Germany’s Preliminary CPI, anticipated on 4 January 2024, is expected to rebound with a projected increase of 0.2%.

Canada Employment Change (5 January 2024)

Following positive employment numbers in October and November of 2023, Canada is poised to release its December 2023 employment data on 5 January 2024. Forecasts suggest an increase of 12K jobs, but with a marginal uptick in the unemployment rate to 5.9%.

US Non-Farm Employment Change (5 January 2024)

November 2023 saw a robust addition of 199k jobs in the US, surpassing October figures. The upcoming release on 5 January 2024 is anticipated to reveal a positive trend with an estimated increase of 163,000 jobs, while the unemployment rate is expected to inch up to 3.8%.

US ISM Services PMI (5 January 2024)

Closing the week, the US ISM Services PMI, reflecting growth in the services sector, is projected to experience a marginal decline from 52.7 to 52.6 in the December figures, set for release on 5 January 2024.

As traders embark on the first week of 2024, vigilance and adaptability will be key. Stay informed, monitor the latest developments, and be prepared for potential market shifts in response to these critical economic indicators.

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

In the penultimate trading session of the year, the S&P 500 approached an all-time high, indicating a robust finish to an exceptionally bullish year for stocks. The Dow Jones Industrial Average secured a new record, while the Nasdaq Composite saw a slight dip. With major indices poised to end 2023 on gains, projected around 13.8% for the Dow and 24.6% for the S&P, the Nasdaq’s remarkable 44.2% rise stands out, buoyed by tech giants and fervor over AI. As the market anticipates the traditional “Santa Claus rally,” the late 2023 surge sets an optimistic tone for 2024, backed by positive technical indicators and expectations of rate cuts and reduced inflation. In the currency market, the US Dollar Index fluctuated significantly, buoyed by rising Treasury yields, impacting major pairs like EUR/USD and GBP/USD. Additionally, USD/JPY and AUD/USD experienced noteworthy volatility, while gold faced a pullback amidst the USD resurgence and climbing yields, reflecting the complex interplay of economic factors and geopolitical events shaping currency movements.

Stock Market Updates

In the penultimate trading day of the year, the S&P 500 edged slightly higher, nearing an all-time high at 4,783.35, signaling a robust end to a bullish year for stocks. The Dow Jones Industrial Average also achieved a new record, closing at 37,710.10, while the Nasdaq Composite experienced a minor dip to 15,095.14. Notably, all major indices are set to conclude 2023 with gains, with the Dow and S&P projected to finish up nearly 13.8% and 24.6%, respectively. The Nasdaq stands out with a remarkable 44.2% climb, its most substantial increase since 2003, primarily fueled by the resurgence of mega-cap tech companies and the fervor surrounding artificial intelligence.

Amidst this year-end rally, the market looks forward to the “Santa Claus rally,” historically observed in the final days of a year and the early days of the subsequent one. The market’s impressive late-2023 surge, rebounding from a sluggish third quarter, positions the S&P with an 11.6% quarterly increase, marking its strongest quarterly performance in three years. As 2023 concludes, the optimistic sentiment continues, with a positive technical outlook and expanding market breadth anticipated to set the stage for a promising 2024. Forecasts pivot on expectations of forthcoming rate cuts and sustained alleviation in inflation, creating what’s termed a “perfect storm” for stocks in the coming year.

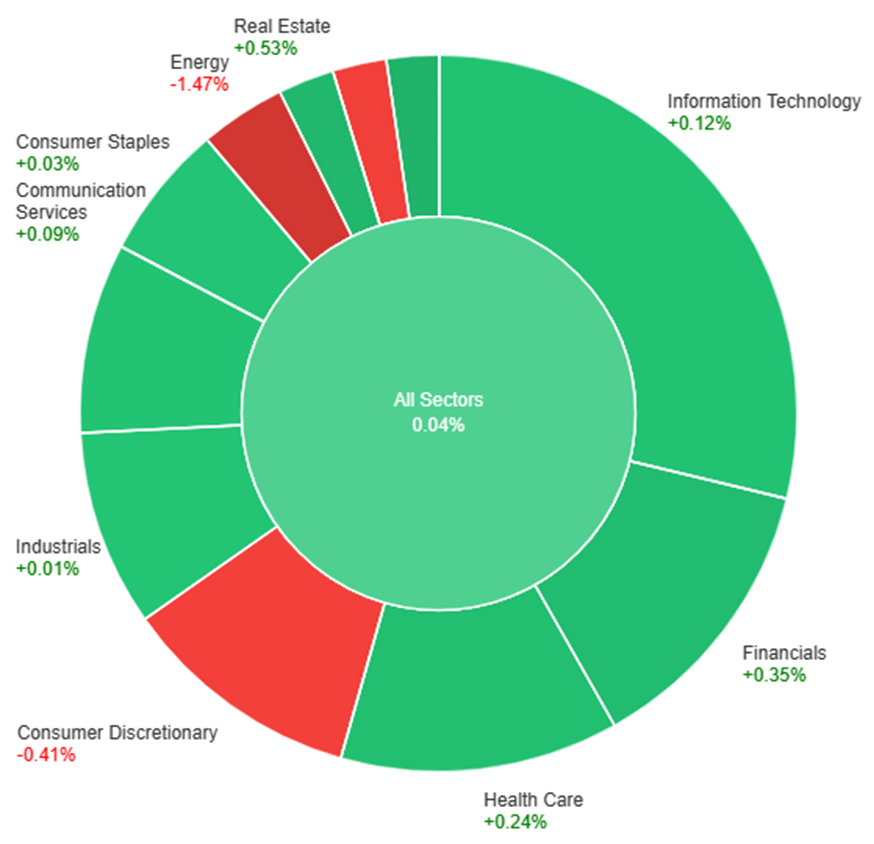

On Thursday, most sectors experienced modest gains, with Utilities leading at +0.70%, followed closely by Real Estate at +0.53% and Financials at +0.35%. Health Care, Information Technology, and Communication Services saw smaller increases ranging from +0.12% to +0.24%. However, Consumer Discretionary and Materials faced declines of -0.41% and -0.46% respectively. Energy witnessed a significant drop of -1.47%, marking the most substantial decrease among all sectors for the day.

Currency Market Updates

In the currency market update, the US Dollar Index (DXY) demonstrated significant volatility, bottoming out at 100.86 before sharply rebounding to 101.25. The Greenback’s resurgence was propelled by a surge in US Treasury yields, reaching 3.85% following a successful auction of the 7-year note. Despite the correction, with higher yields contributing to its recovery, the overall trend for the USD remains downward, albeit with potential for further correction.

EUR/USD faced its steepest decline in two weeks, sliding from a monthly high of 1.1139 to the 1.1055 area. The pair’s movement was influenced by Spain’s impending inflation figures and Eurostat’s scheduled release of Eurozone figures, both expected to provide significant insights into the euro’s trajectory. Similarly, GBP/USD retreated from above 1.2800 to around 1.2700, with the UK’s final economic report for 2023 focusing on Nationwide Housing Prices for December.

USD/JPY experienced notable volatility, plunging to 140.23—the lowest level since July—before recovering to 141.40, supported by rising yields. AUD/USD reached a peak at 0.6871 but failed to maintain momentum, slipping to 0.6835. The Australian Dollar faces immediate support at 0.6825, while a potential upswing could occur if it surpasses 0.6850.

Gold faced a pullback from $2,088 to $2,065 due to the rebounding US Dollar and rising yields. Despite the overarching upward trend, current conditions hint at a potential downside bias ahead of the Asian session for the precious metal. These fluctuations across currency pairs and gold prices reflect the intricate interplay between economic indicators, market sentiments, and geopolitical events driving currency market movements.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Falters Despite US Economic Data; Eyes on Eurozone Inflation

The EUR/USD faced setbacks as it slipped below 1.1100, driven by a surge in US Treasury yields despite mixed American economic reports. The US Dollar remained resilient, largely unaffected by the jobless claims uptick and stagnant pending home sales. Amidst Wall Street’s festive rally, the greenback found strength with a rebound in yields post a 7-year note auction, sidelining the impact of economic data. Attention turns to Spain’s preliminary CPI figures for December, crucial for insight into Eurozone inflation, likely to shape the pair’s trajectory.

On Thursday, the EUR/USD moved lower and reached the middle band of the Bollinger Bands. Currently, the price moving slightly above the middle band, suggesting a potential upward movement. Notably, the Relative Strength Index (RSI) maintains its position at 55, signaling a neutral outlook for this currency pair.

Resistance: 1.1138, 1.1222

Support: 1.1043, 1.0946

XAU/USD (4 Hours)

XAU/USD Continues Surge Amid Dollar Weakness and Investor Optimism

Gold prices are on the rise as the US Dollar faces pressure amidst a buoyant Asian stock market. Investor enthusiasm for anticipated aggressive interest rate cuts by the Fed, coupled with China’s commitment to bolster domestic demand and liquidity injections by the PBOC, fuels risk appetite, edging the Dollar lower. Despite a slight rebound in US Treasury bond yields, Gold maintains its upward momentum, nearing the $2,100 mark in Asian trade. The Dollar Index hovers near five-month lows, while US Treasury bond yields, after bouncing off multi-month lows, stand at 3.81%, up 0.50% on the day. Wednesday’s market return saw Gold hit a record close above $2,070, propelled by a Dollar sell-off post-positive US auctions. Anticipation of Fed rate cuts continues to drive demand for stocks and bonds, influencing Treasury yields. With the focus shifting to mid-tier US Jobless Claims and a seven-year bond auction, Gold traders remain vigilant amid pre-New Year thin liquidity conditions, expecting potential upside boosts.

On Thursday, XAU/USD moved lower and reached the middle band of the Bollinger Bands. Currently, the price moving at the upper band, suggesting a potential upward movement. The Relative Strength Index (RSI) stands at 53, signaling a neutral outlook for this pair.

Resistance: $2,088, $2,103

Support: $2,065, $2,048

Written on December 29, 2023 at 3:10 am, by anakin

Stocks closed higher as the S&P 500 edged up 0.14%, nearing its all-time high from January 2022. The Dow Jones Industrial Average also hit a new closing high, while the Nasdaq Composite rose 0.16%, marking an eight-week winning streak. Analysts anticipate a potential ‘Santa Claus rally’ despite concerns over market over-optimism, cautioning investors about unexpected shifts as the Federal Reserve’s rate decisions loom. Additionally, the US Dollar weakened against major currencies, influenced by lower Treasury yields and economic data releases, while the commodity market saw Gold nearing record highs and Silver stabilizing.

Stock Market Updates

Stocks closed higher, with the S&P 500 edging up 0.14% to nearly reach its all-time high from January 2022, ending at 4,781.58. The Dow Jones Industrial Average also hit a new closing high, while the Nasdaq Composite rose 0.16%. This climb marks an eight-week winning streak for the S&P, Dow, and Nasdaq, with the S&P nearing its record. Analysts anticipate a ‘Santa Claus rally,’ a period noted for market upswings at the end of one year and the start of the next, which historically sees an average increase of about 1.3% for the S&P 500.

Despite the overall positive market sentiment, concerns loom regarding potential over-optimism. Some experts worry that the market’s enthusiasm might lead to disappointment if the Federal Reserve delays rate cuts. While Fed funds futures indicate possible rate cuts as early as March, experts caution that the current bullish sentiment might expose investors to unexpected market shifts, especially with 90% of S&P 500 stocks trading above their 50-day moving average, suggesting a level of market “frothiness.” Analysts advise caution amidst this optimistic climate to guard against unforeseen market volatility.

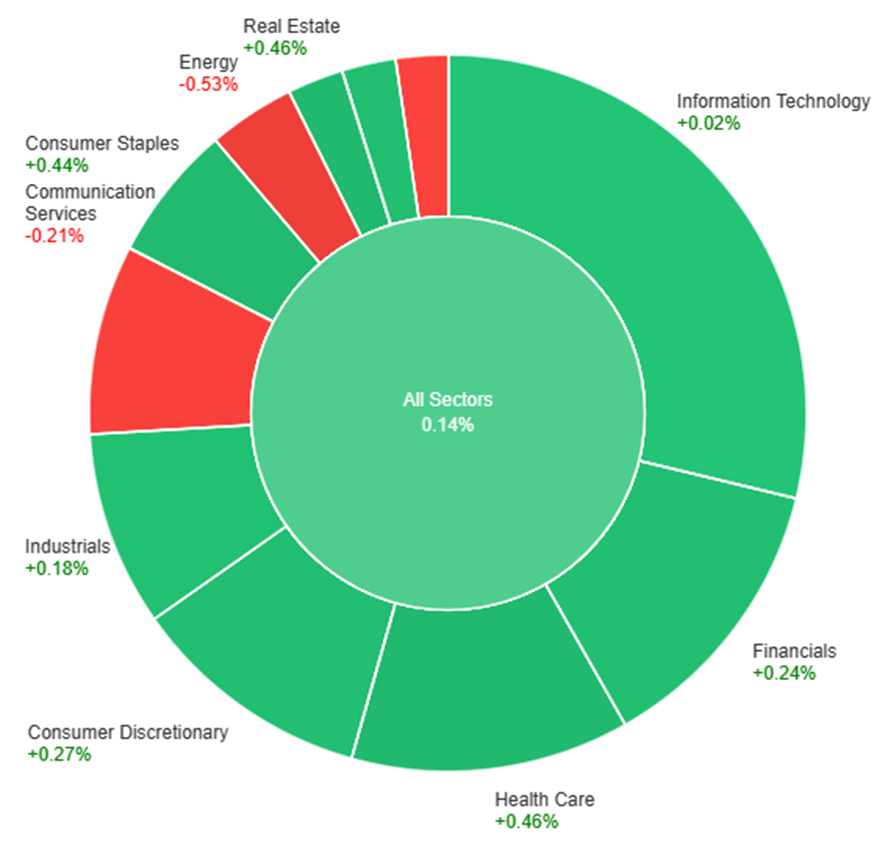

On Wednesday, across various sectors, the market showed a modest overall increase of 0.14%. Health care and real estate sectors led the gains, both surging by 0.46%, followed closely by consumer staples at 0.44%. Sectors like consumer discretionary and materials experienced moderate gains at 0.27% and 0.25%, respectively. However, there were declines in certain sectors, with energy facing the most significant drop of 0.53%, followed by communication services at -0.21% and utilities at -0.12%. Information technology saw the smallest change, with a marginal increase of 0.02%.

Currency Market Updates

The currency markets saw a notable weakening of the US Dollar as the US Dollar Index (DXY) dropped below 101.00, marking its lowest point since July. This decline was attributed to a combination of factors, including the 10-year Treasury yield hitting a five-month low at 3.78%, coupled with the 2-year settling at 4.24%, the lowest since May. Amidst this, US stocks hovered near recent highs, especially the Dow Jones, which edged closer to an all-time high. However, the Dollar’s decline persisted due to increased risk appetite and the sustained pressure of lower Treasury yields. The release of economic data further exacerbated the situation, with the Richmond Fed Manufacturing Index dropping to -11 in December, reflecting worse-than-expected figures across shipments, new orders, and employment. The upcoming release of the weekly Jobless Claims report, trade figures, and November’s Pending Home Sales report could add to the market’s sentiment.

Meanwhile, the Euro (EUR/USD) surged past 1.1100 for the first time in five months, driven by the broad-based weakness of the Dollar. The Pound (GBP/USD) also witnessed a strengthening trend, reaching 1.2802, its strongest level since August, although it subsequently retreated slightly. The Japanese Yen outperformed amidst the Dollar’s decline, pushing USD/JPY below 142.00 and approaching December lows. Australian (AUD/USD) and New Zealand (NZD/USD) currencies remained in upward trajectories, facing resistance levels around 0.6850 and reaching the 0.6350 area, respectively, backed by a combination of risk appetite and lower yields. Conversely, the Canadian Dollar (USD/CAD) experienced a lag despite bottoming at 1.3175, its lowest since August, as it climbed back above 1.3200 by the end of the trading day. In the commodity market, Gold continued its upward trajectory, nearing a record close above $2,070, while Silver stagnated around $24.25, failing to follow Gold’s upward trend.

The EUR/USD rallied past the 1.1100 mark propelled by a weakening US Dollar, sinking below 101.00 in the DXY index for the first time in five months. With US Treasury yields hitting new lows amidst expectations of Federal Reserve rate cuts in the upcoming year, the Dollar faced downward pressure while equity markets remained buoyant. Despite quiet trading, anticipation grows for crucial reports like the US weekly Jobless Claims and Spain’s preliminary inflation figures. As 2023 concludes, the serene market conditions continue to weigh on the Dollar, setting the stage for a pivotal turn with the impending release of US employment data next week.

On Wednesday, the EUR/USD moved higher and reached the upper band of the Bollinger Bands. Currently, the price moving slightly below the upper band, suggesting a potential upward movement. Notably, the Relative Strength Index (RSI) maintains its position at 75, signaling a bullish outlook for this currency pair.

Resistance: 1.1138, 1.1222

Support: 1.1043, 1.0946

XAU/USD (4 Hours)

XAU/USD Navigates Volatility Amidst Cautious Dollar and Fed Watch

Gold (XAU/USD) is experiencing a pause as the US Dollar (USD) stabilizes amidst market caution, despite sluggish US Treasury bond yields. Investors, returning from the Christmas holiday, are refraining from substantial trades, closely monitoring macroeconomic developments. Uncertainty looms as Fed interest rate cut expectations for 2024 remain ambiguous, leaving Gold buyers in suspense. The dovish sentiment surrounding the Fed’s policy shift strengthened following lackluster data on the Core PCE Price Index, propelling the US Dollar Index to a five-month low. With thin liquidity and cautious trading ahead due to the holiday week, Gold’s trajectory remains vulnerable to intense fluctuations amidst this landscape.

On Wednesday, XAU/USD moved higher and reached the upper band of the Bollinger Bands. Currently, the price moving at the upper band, suggesting a potential upward movement. The Relative Strength Index (RSI) stands at 72, signaling a bullish outlook for this pair.

Resistance: $2,088, $2,103

Support: $2,070, $2,048

Written on December 28, 2023 at 2:45 am, by anakin

The markets witnessed a surge as major indices edged closer to historic peaks in the final week of the year. The S&P 500, Nasdaq Composite, and Dow Jones Industrial Average all marked significant gains, with the Nasdaq 100 hitting a new all-time high. Wall Street’s bullish run continued, fueled by optimism stemming from encouraging inflation data aligning with the Federal Reserve’s targets. Meanwhile, the USD/JPY pair saw movement, while the Australian Dollar stood strong against a subdued US Dollar, influenced by potential central bank stances. Furthermore, developments in China’s industrial profits hinted at a slowdown, impacting trade relations and currency movements. In the currency markets, the EUR/USD pair maintained stability, influenced by data-driven decisions by the ECB and prevailing market sentiment, as economic data remained minimal.

Stock Market Updates

Stocks surged at the onset of the final week of the year, propelling major indices closer to historic peaks. The S&P 500 escalated by 0.42% to reach 4,774.75, nearing its all-time high of 4,796.56 from January 2022. Similarly, the Nasdaq Composite surged by 0.54% to settle at 15,074.57, while the Dow Jones Industrial Average gained 159.36 points, closing at 37,545.33, marking a 0.43% increase. The Nasdaq 100 notably climbed by 0.6%, achieving a new all-time high and ending at 16,878.46.

The market’s bullish trajectory persisted as the S&P 500 approached record levels, merely less than 1% away from its previous peak. Wall Street sustained this momentum, with the S&P 500 marking its eighth consecutive weekly advance, the lengthiest streak since 2017, and similar winning streaks observed in the Dow and Nasdaq Composite. Investor optimism soared following encouraging inflation data indicating a closer alignment with the Federal Reserve’s 2% target. Moreover, the anticipation of potential rate cuts in the upcoming year further bolstered equities, contributing to recent weeks’ market upswings.

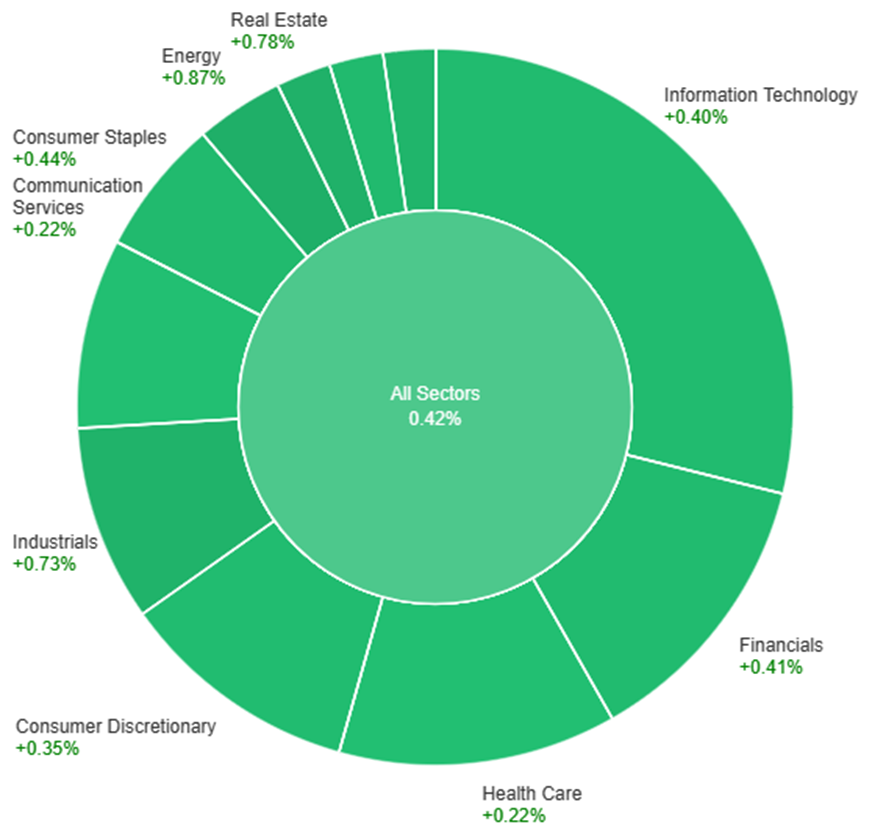

On Tuesday, across various sectors, the market saw a positive trend with a general increase in most sectors. Energy stood out with a notable rise of 0.87%, leading the charge, followed closely by Real Estate at 0.78% and Industrials at 0.73%. Utilities and Materials showed moderate gains at 0.65% and 0.44% respectively, aligning with Consumer Staples also at 0.44%. Financials and Information Technology both saw increases of around 0.4%, while Consumer Discretionary showed a slight uptick of 0.35%. Communication Services and Health Care trailed the pack with a smaller increase of 0.22% each. Overall, the market demonstrated positive momentum, particularly in the Energy and Real Estate sectors on Tuesday.

Currency Market Updates

The USD/JPY pair experienced upward movement, reaching 142.84 after the Bank of Japan’s Summary of Opinions release, with the market showing quiet activity amidst the holiday season’s thin trading. The BoJ hinted at potential policy shifts if the wage-price cycle strengthens but has not finalized the timing for such changes. Meanwhile, in the US, the latest Core PCE figures fell slightly below expectations, signaling a 3.2% YoY growth in November, potentially influencing the Federal Reserve’s future interest rate decisions. Amidst these developments, the currency market awaits the US Richmond Fed Manufacturing Index and Initial Jobless Claims for further insights, but their impact might be limited given the prevailing light trading conditions.

Concurrently, the Australian Dollar stood at a five-month high against a subdued US Dollar, backed by the Australian central bank’s potential hawkish stance in early 2024 due to robust inflation. However, China’s reported decline in Industrial Profits for January to November by 4.4% hints at a slowdown, prompting expectations for additional policy support to bolster the second-largest global economy. This slowdown could impact the RBA’s stance, considering the significance of trade relations between Australia and China. The weakening US Dollar Index, influenced by Fed easing speculations and declining Treasury yields, further highlights the prevailing pressure on the Greenback.

On the EUR/USD front, the pair traded near August’s highest level around 1.1040, encountering minimal losses. The Core PCE figures in the US slightly missed expectations, growing 3.2% YoY, while the Eurozone witnessed a consistent ECB policy stance, with no change in interest rates. The ECB’s data-driven decisions, clarified by President Christine Lagarde, and the slightly more hawkish tone from ECB Vice President Luis de Guindos may contribute to lifting the Euro and maintaining stability for the EUR/USD pair. However, with minimal top-tier economic data expected, market sentiment remains a crucial factor influencing the pair’s movement.

The EUR/USD pair hovers near 1.1037, experiencing marginal setbacks amidst subdued trading conditions. The Federal Reserve’s favored inflation metric, the Core PCE, exhibited a 3.2% year-on-year growth, slightly under the anticipated 3.3%, further affecting the US Dollar’s stance. Conversely, ECB statements from President Christine Lagarde emphasized the bank’s data-dependent approach, dismissing market pressures. Eurozone outlook remained cautiously optimistic, with ECB Vice President Luis de Guindos highlighting a reluctance to alter monetary policy prematurely. As economic calendars lack major data releases, the EUR/USD trend hinges on prevailing market sentiment, potentially swayed by upcoming US Richmond Fed Manufacturing Index and Initial Jobless Claims reports, influencing near-term price movements.

On Tuesday, the EUR/USD moved slightly higher and tried to reach the upper band of the Bollinger Bands. Currently, the price moving slightly below the upper band, suggesting a potential upward movement. Notably, the Relative Strength Index (RSI) maintains its position at 64, signaling a neutral but slightly bullish outlook for this currency pair.

Resistance: 1.1042, 1.1138

Support: 1.0946, 1.0852

XAU/USD (4 Hours)

XAU/USD Holds Steady Above $2,060 Amid Dollar Weakness and Easing Speculations

In the early Asian session, Gold (XAU/USD) maintained its position above $2,060 despite a marginal 0.09% dip, set amidst a quiet trading week expected due to light volumes in the final stretch of 2023. The US Dollar weakened against its counterparts, pressing the US Dollar Index (DXY) to its lowest since July near 101.45. As Treasury yields edged lower, resting at 3.89%, expectations of Federal Reserve easing intensified, with the market pricing in potential cuts in January and fully anticipating cuts by March 2024. This dovish stance, alongside recent data showing a softer increase in the Core PCE, has positioned lower interest rates as a potential boon for gold, reducing its opportunity cost as a non-yielding asset. Geopolitical tensions in the Middle East, particularly Yemen’s threat to Red Sea shipping and Iran’s potential actions in the Gibraltar Strait, are adding pressure, potentially elevating gold’s safe-haven appeal. Traders are keenly observing the unfolding geopolitical landscape alongside upcoming economic indicators like the US Richmond Fed Manufacturing Index and Initial Jobless Claims.

On Tuesday, XAU/USD moved slightly higher and tried to reach the upper band of the Bollinger Bands. Currently, the price moving just below the upper band, suggesting a potential upward movement. The Relative Strength Index (RSI) stands at 62, signaling a neutral but slightly bullish outlook for this pair.

Resistance: $2,068, $2,088

Support: $2,048, $2,031

Written on December 27, 2023 at 2:51 am, by anakin

Sydney, Australia, 27 December 2023 – Having reaffirmed its commitment to corporate social responsibility (CSR) earlier in the year, VT Markets is closing the year with 3 major environmental, social, and governance (ESG) milestones under its belt:

Food for good with the UN’s ShareTheMeal programme Through the United Nations’ online ShareTheMeal platform, VT Markets raised 2,000 meals for communities in need between November to December 2023.

A gift of joy with South Africa’s Cotlands Ahead of the holiday season, VT Markets donated 1,240 educational toys—including stacking rings and puzzles—to Cotlands, a Johannesburg organisation seeking to provide early development opportunities to marginalised children.

Youth advocacy at UNESCO’s Jakarta workshop In addition to pledging its support as a key sponsor, VT Markets advocated for equal treatment of young STEM professionals via a keynote address at the UNESCO-led 3rd International Workshop and Training on Youth and Young Professionals in Science, Engineering, Technology, and Innovation for Disaster and Climate Resilience.

Commenting on these initiatives, VT Markets’ Director of Global Marketing, Martin Li, stated: “The work we’ve done with ShareTheMeal, Cotlands, and UNESCO is just the start of much more to come. In a year that has yielded its fair share of challenges for humanity, we’re delighted to have contributed in some way.”

Heading into 2024, VT Markets is poised to build on this success. Off the back of a fresh partnership with the renowned team competing in the formula E world championship Maserati MSG Racing, the company will redouble its ESG efforts with both new and existing collaborators in tow. For news of upcoming initiatives and potential sponsorship opportunities, be sure to follow VT Markets on their official website and social media pages.

About VT Markets:

VT Markets is a regulated multi-asset broker with a presence in over 160 countries. To date, it has won numerous international accolades including Best Customer Service and Fastest Growing Broker.

In line with its mission to make trading accessible to all, VT Markets currently offers unfettered access to over 1,000 financial instruments and a seamless trading experience via its award-winning mobile app.

With no high-impact news expected, the market’s attention will be focused on the holiday season this week. Investor sentiment is likely to be influenced by holiday festivities, resulting in increased shopping activity and the investment of holiday bonuses. Additionally, the end-of-year period typically coincides with institutional investors going on vacation, leaving the market in the hands of comparatively bullish retail investors. This phenomenon, known as the Santa Claus rally, is expected to occur in the last week of December.

Holiday-related factors aside, here are several other medium-impact market indicators to watch for in the last week of 2023:

US unemployment claims (28 December 2023)

The number of Americans filing for unemployment benefits increased by 2,000 to 205,000 in the week ending 16 December, staying close to the 2-month low of 203,000 seen in the previous week.

Analysts expect a further rise to 207,000 in the week ending 28 December.

US pending home sales (28 December 2023)

Following a 1% rise in September 2023, pending home sales in the US dropped 1.5% month-over-month in October, marking the lowest level since records were first kept in 2001.

Analysts expect a 0.5% increase in the figures for November, set to be released on 28 December.

Written on December 26, 2023 at 1:35 am, by anakin

Thursday witnessed a strong comeback for stocks, with the S&P 500, Dow Jones, and Nasdaq rebounding significantly, nearing their record highs. Micron Technology’s stellar performance fueled tech stocks, while companies like Salesforce contributed to the climb. This turnaround followed a recent market dip attributed to profit-taking after a sustained period of gains. Meanwhile, the currency market saw the dollar index decline due to weaker U.S. economic data, impacting Treasury yields, while EUR/USD faced resistance and USD/JPY retreated within a defined range. Attention now turns to pivotal economic releases that could influence market dynamics, including the US core PCE and Japan CPI data.

Stock Market Updates

Stocks rebounded on Thursday after a recent dip, marking a robust resurgence in the year-end rally. The S&P 500 recovered from its recent decline, edging up by 1.03% to 4,746.75, inching within 1% of its closing high and 1.5% of its intraday record. The Dow Jones Industrial Average soared by 0.87% to 37,404.35, and the Nasdaq Composite surged 1.26% to 14,963.87. The market’s upward trajectory was widespread, with over 450 companies in the S&P 500 index witnessing gains. Micron Technology notably stood out, jumping by 8.6% following its quarterly performance surpassing expectations, bolstered further by an optimistic current-quarter guidance. Chip stocks broadly surged, with Intel and Advanced Micro Devices rising by 2.9% and 3.3%, respectively. Salesforce also contributed to the Dow’s climb, rising by 2.7% after receiving an upgrade from Morgan Stanley.

This upward swing followed a recent downtrend where Wall Street faced losses due to profit-taking after a streak of gains. The prior session marked the Dow and Nasdaq’s worst performance since October, breaking nine-day winning streaks, while the S&P 500 experienced its most significant decline since September. Rhys Williams, chief strategist at Spouting Rock Asset Management, attributed this shift to a technical correction following a robust market period. Since late October, the Dow and S&P 500 have surged over 15%, while the Nasdaq Composite saw an impressive 18% surge during the same period, reflecting a substantial upward momentum in the market.

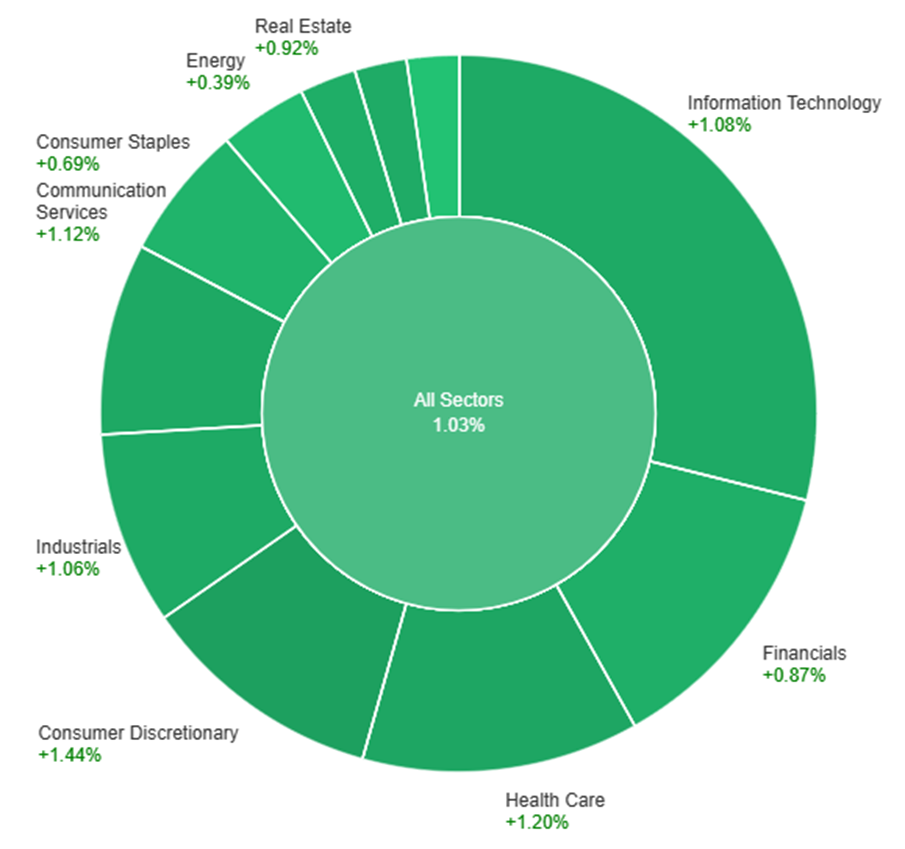

On Thursday, across various sectors, the market showed a general upward trend with an overall increase of 1.03%. Consumer Discretionary saw the highest surge at 1.44%, followed closely by Health Care at 1.20% and Communication Services at 1.12%. Information Technology and Industrials also experienced notable gains at 1.08% and 1.06%, respectively. Meanwhile, Energy and Utilities demonstrated the smallest upticks, with Energy rising by 0.39% and Utilities by 0.13%. Real Estate and Financials fell within the mid-range increases, with Real Estate at 0.92% and Financials at 0.87%. Consumer Staples trailed behind with a rise of 0.69%.

Currency Market Updates

The currency market saw notable shifts as the dollar index declined by 0.4% due to weaker-than-expected U.S. economic data, impacting Treasury yields. Despite a solid 4.9% annualized GDP increase in Q3, downward revisions in GDP and core PCE figures influenced market sentiment. Core PCE rose only 2.0% year-on-year, signaling a potential downside miss, which could favor dollar bears. The upcoming release of November’s core PCE, income, and spending figures was highlighted as pivotal for Treasuries, risk, and the dollar, with indications pointing towards a possible downward trend in core PCE, impacting market dynamics.

EUR/USD observed a 0.4% rise, facing resistance near 1.1000 due to ongoing weak economic data and outlooks in the eurozone, particularly in Germany. USD/JPY, on the other hand, experienced a 0.8% fall, retracting all weekly gains but maintaining a recovery pattern within the 140.95-4.95 range following dovish meetings from both the Fed and BoJ. With the upcoming Japan CPI and U.S. core PCE releases, attention is on the 200-day moving average at 142.72, potentially signaling a retest of 140.95. Sterling saw a marginal 0.25% rise amidst a pessimistic UK CBI retail sales survey and below-forecast UK CPI, with further market focus on impending UK retail sales and Q3 GDP announcements.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD USD Gains Ground Amid Dollar Weakness Despite Mixed US Data; Eyes on Inflation Figures

The EUR/USD edged higher, reaching the 1.1000 mark as the Dollar struggled despite increased Treasury yields. US economic indicators presented a mixed picture, with declines in the Philadelphia Fed Index and a revision in Q3 GDP, while Jobless Claims remained steady. Investors await the crucial Core PCE inflation data, anticipating a 0.2% rise for November. Despite the rebound in US yields, the Dollar remains subdued, limiting the EUR/USD upside potential amidst thinner market conditions.

On Thursday, the EUR/USD moved higher and reached the upper band of the Bollinger Bands. Currently, the price moving slightly below the upper band, suggesting a potential upward movement. Notably, the Relative Strength Index (RSI) maintains its position at 66, signaling a neutral outlook for this currency pair.

Resistance: 1.1017, 1.1138

Support: 1.0946, 1.0830

XAU/USD (4 Hours)

XAU/USD Resilient Above $2,040 Despite USD Swings Amidst Mixed US Economic Data

In fluctuating market sentiment driven by a resilient US Dollar and mixed economic indicators, spot Gold managed to maintain its position above $2,040 per troy ounce. The Dollar initially gained traction, favored by Wall Street’s lackluster performance and softer Treasury yields, but a shift in direction followed mixed US data. Despite GDP figures slightly below estimates and declining bond yields, investor confidence bounced back on Wall Street. With attention now turning to upcoming US economic releases, including the Core PCE Price Index and Michigan Consumer Sentiment Index, Gold remains resilient amidst the market’s uncertain landscape.

On Thursday, XAU/USD moved slightly higher and reached the upper band of the Bollinger Bands. Currently, the price moving just below the upper band, suggesting a potential upward movement. The Relative Strength Index (RSI) stands at 63, signaling a neutral outlook for this pair.

Resistance: $2,050, $2,068

Support: $2,031, $2,008

Economic Data

Currency

Data

Time (GMT + 8)

Forecast

GBP

Retail Sales m/m

15:00

0.4%

CAD

GDP m/m

21:30

0.2%

USD

Core PCE Price Index m/m

21:30

0.2%

USD

Revised UoM Consumer Sentiment

23:00

69.4

Written on December 22, 2023 at 1:21 am, by anakin

Stock futures edged higher after a recent market pause, with S&P 500, Nasdaq 100, and Dow Jones futures indicating slight upticks. Micron’s notable postmarket leap of over 4% propelled optimism after surpassing Wall Street’s projections for its first fiscal quarter. However, the prior day marked a downturn as investors seized profit opportunities, reflecting the S&P 500’s worst performance since September. Looking forward, attention is on forthcoming economic indicators like jobless claims and GDP figures, alongside Nike’s imminent earnings release. In currency markets, Sterling declined by 0.5% due to disappointing UK CPI, while the dollar, euro, and yen stabilized. Ongoing central bank comments continue to sway sentiment, impacting the EUR/USD pair and hinting at potential shifts in global monetary policies tied to upcoming data releases like Japan’s core CPI and the U.S. core PCE.

Stock Market Updates

Stock futures indicated a modest upward trend following a pause in the recent market surge. S&P 500 futures rose by 0.16%, Nasdaq 100 futures by 0.24%, and Dow Jones Industrial Average futures climbed 0.15%. Micron experienced a significant postmarket increase, jumping over 4% after surpassing Wall Street’s expectations for its first fiscal quarter and providing a stronger-than-expected outlook for the current quarter. The day prior witnessed a downturn in the markets as investors seized the opportunity to capitalize on recent profits, resulting in the S&P 500’s worst performance since September and the Dow and Nasdaq marking their most significant drops since October. These declines marked a breather from a robust market rally that saw substantial gains in the Dow, S&P 500, and Nasdaq Composite over the past few months.

Looking ahead, investors are eyeing upcoming data releases such as jobless claims and third-quarter gross domestic product figures, along with the closely watched personal consumption expenditures price index, known as an essential measure of inflation. Additionally, market watchers are anticipating Nike’s earnings announcement after the closing bell on Thursday, which is likely to influence market sentiment and direction.

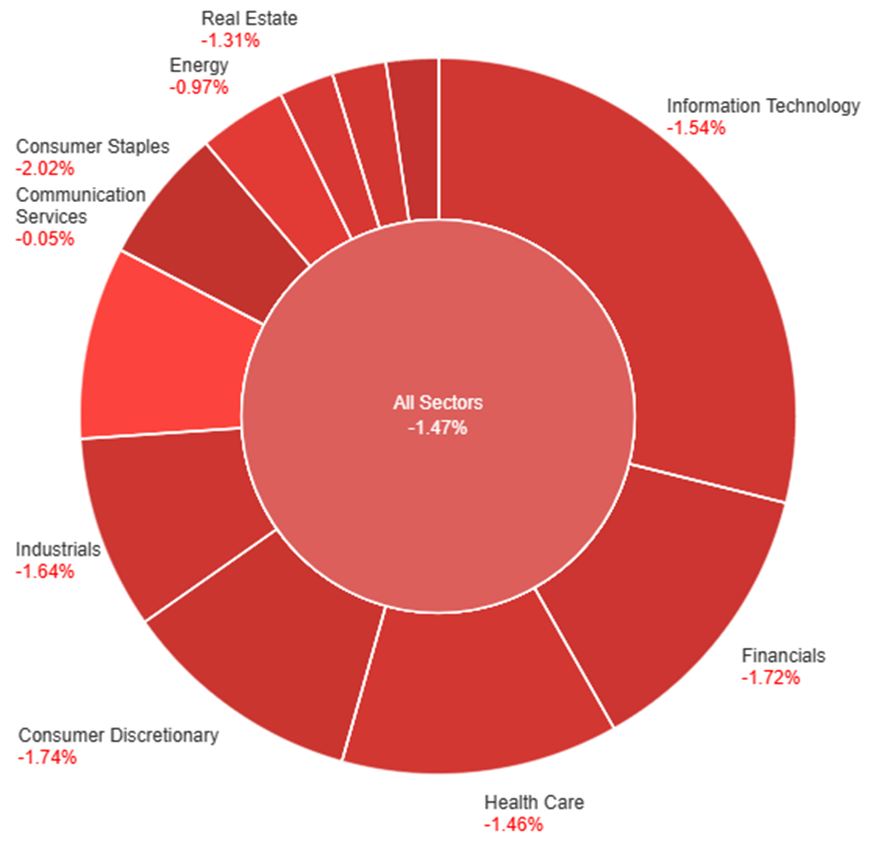

On Wednesday, the overall market experienced a decline of 1.47%. Across sectors, most industries saw negative movements, with Utilities and Consumer Staples facing the steepest drops at -1.98% and -2.02% respectively. The Information Technology sector also fell notably by 1.54%, while Financials and Consumer Discretionary both recorded decreases of 1.72% and 1.74% respectively. Other sectors such as Health Care, Materials, and Industrials followed a similar downward trend, showing declines ranging from 1.46% to 1.64%. Communication Services and Energy sectors were relatively less affected, with marginal decreases of -0.05% and -0.97% respectively. Real Estate experienced a decline of 1.31%. Overall, it was a day of widespread negative performance across various sectors, with Utilities and Consumer Staples bearing the brunt of the losses.

Currency Market Updates

In recent currency market movements, Sterling faced losses as UK CPI fell below expectations, leading to a 0.5% decline. This drop was influenced by a significant 16bp decrease in two-year gilt yields, impacting the market and offsetting risk-on flows. Conversely, the dollar, euro, and yen stabilized within specific ranges following fluctuations post-recent central bank meetings. However, these adjustments were insufficient to extend the EUR/USD’s attempt to surpass November and December highs or bolster USD/JPY after its post-Fed pivot retreat.

The market sentiment remains influenced by ongoing post-meeting comments from the Fed and ECB. Eurozone dynamics saw ECB hawks challenging aggressive rate cut expectations while grappling with declining German producer prices amidst forecasts of increased German inflation in early 2024 due to budget constraints. As a result, the EUR/USD pair experienced a 0.2% decline, nearing 1.0950 from its late 2023 peaks. Additionally, the focus now shifts towards upcoming data releases, including Japan’s core CPI, predicted to drop to 2.5%, potentially influencing the BoJ’s policies. Meanwhile, the U.S. core PCE is expected to decrease to 3.3%, aligning with futures pricing indicating a decline in Fed rates to 3.85% by the next December. These impending reports stand poised to shape future currency movements.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Teeters Amid US Dollar Recovery: Key Data Points Influence Direction

The EUR/USD faced a dip amidst a recovering US Dollar Index, struggling to break the 1.1000 mark as it moved directionlessly. Supported by a weak US Dollar and a hint of risk appetite, the pair showed resilience. Positive US data, including a rise in Existing Home Sales and Consumer Confidence, countered the Eurozone’s moderate uptick in Consumer Confidence and the ECB’s resistance to early rate cuts. While the bias leans towards an upward trajectory, the EUR/USD needs to breach 1.1000 swiftly to mitigate focus on the diverging economic performances of the US and Eurozone. Thursday’s upcoming data, including Jobless Claims and Q3 GDP, followed by Friday’s Core PCE report, will likely steer the pair’s direction.

On Wednesday, the EUR/USD moved slightly lower reaching the middle band of the Bollinger Bands. Currently, the price moving slightly above the upper band, suggesting a potential for another upward movement. Notably, the Relative Strength Index (RSI) maintains its position at 55, signaling a neutral outlook for this currency pair.

Resistance: 1.1017, 1.1138

Support: 1.0946, 1.0830

XAU/USD (4 Hours)

XAU/USD Holds Steady Amidst USD Strength and Inflation Concerns

Spot Gold, represented by XAU/USD, navigated within a tight range as the US Dollar gained momentum earlier in the day, buoyed by upbeat US data like the CB Consumer Confidence report. Despite hitting an intraday high before retracing, Gold settled near its daily low. Market sentiment shifted during the European session on news of easing UK inflation, alleviating some concerns. Eyes now turn to the upcoming US Personal Consumption Expenditures Price Index, anticipated to influence markets significantly and potentially affirm or challenge the Fed’s recent policy stance.

On Wednesday, XAU/USD moved slightly lower and reached the middle band of the Bollinger Bands. Currently, the price moving just above the upper band, suggesting a potential upward movement. The Relative Strength Index (RSI) stands at 56, signaling a neutral outlook for this pair.

Resistance: $2,050, $2,068

Support: $2,031, $2,008

Economic Data

Currency

Data

Time (GMT + 8)

Forecast

USD

Final GDP q/q

21:30

5.2%

USD

Unemployment Claims

21:30

214K

Written on December 21, 2023 at 3:53 am, by anakin