Sydney, Australia, 1 November 2023 – Online brokerage VT Markets has announced the return of its flagship trading competition, the King of the Hill trading contest. Scheduled to take place from 1 November 2023 to 31 January 2024, this latest edition of the contest promises a bigger, better experience across the board.

For the first time ever, VT Markets will be offering an amplified prize pool of USD 200,000 and increasing the number of potential winners from 25 to 60. Additionally, all participants will also receive complimentary points for VT Markets’ ClubBleu loyalty programme—the latest mark of VT Markets’ ongoing commitment towards its community.

Aside from these enhanced rewards, VT Markets is also expanding other aspects of the contest in unprecedented fashion. Setting the stage for a truly global spectacle, the upcoming King of the Hill trading contest will be open to multiple new regions, including India, Indonesia, and countries from the Middle East.

Commenting on these changes, a VT Markets spokesperson stated: “The evolution of our King of the Hill trading contest has been breathtaking to behold, and that has been due in no small part to our fantastic community. Given the overwhelmingly positive responses we’ve seen in every previous iteration of the contest, we’re now elevating the stakes and inviting a wider array of traders to showcase their trading prowess. With a significantly larger prize pool and up to 500:1 leverage at every trader’s disposal, this contest will no doubt be the most exciting one yet.”

More information will be made available closer to the launch of the contest. For all the latest news and updates, visit the relevant King of the Hill page below:

VT Markets is a regulated multi-asset broker with a presence in over 160 countries. To date, it has won numerous international accolades including Best Customer Service and Fastest Growing Broker.

In line with its mission to make trading accessible to all, VT Markets currently offers unfettered access to over 1,000 financial instruments and a seamless trading experience via its award-winning mobile app.

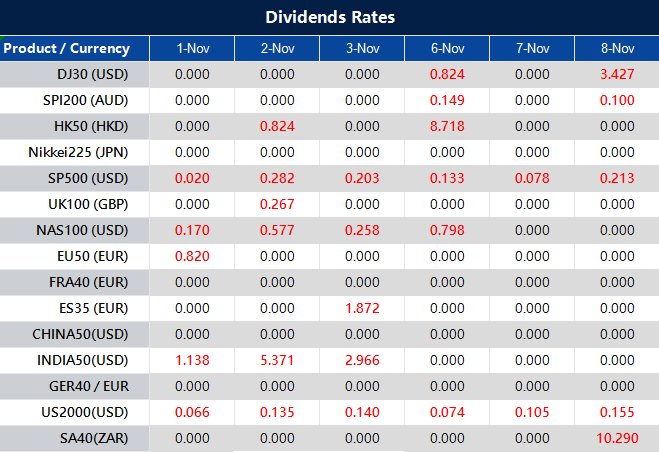

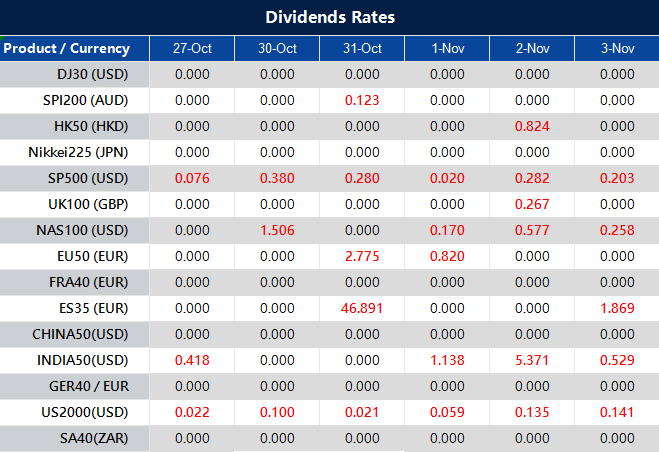

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

In the stock market, October witnessed surging interest rates, leading to a challenging month for investors, but there was a modest recovery on Tuesday as major indices rebounded. Real estate and financial sectors outperformed, while some tech giants faced declines. Despite recent gains, it marked the third consecutive losing month for major stock indices, driven by rising Treasury yields. The currency market saw the US dollar strengthen, particularly against the yen, influenced by central bank policies and economic data. As the markets watch for signals from the Federal Reserve and other central banks, investors remain cautious yet hopeful for a year-end rally, with an eye on currency pairs, such as USD/JPY and EUR/USD.

Stock Market Updates

In the stock market, October was marked by surging interest rates, leading to a challenging month for investors. However, on Tuesday, there was a modest recovery as the major indices rebounded. The S&P 500 climbed 0.65% to 4,193.80, and the Nasdaq Composite added 0.48% to 12,851.24, while the Dow Jones Industrial Average advanced 0.38% to 33,052.87. Notably, real estate and financial sectors outperformed, with gains of 2% and 1.1%, respectively, while some mega-cap tech stocks, such as Alphabet and Meta Platforms, faced declines. The Cboe Volatility Index (VIX) dropped below its long-term average, indicating reduced market uncertainty. Earnings reports also played a role in market movements, with Caterpillar’s stock sliding more than 6% due to a modest fourth-quarter revenue outlook, and JetBlue shares dropping over 10% as the airline’s third-quarter results fell short of expectations.

Despite the recent gains, October marked the third consecutive losing month for major stock indices. The Dow and S&P 500 fell 1.4% and 2.2%, respectively, while the tech-heavy Nasdaq declined by 2.8%. These losses were driven by a rapid increase in Treasury yields, with the 10-year U.S. Treasury yield reaching a significant 5% level, last seen in 2007. Market participants attribute this rise to concerns that the Federal Reserve may maintain higher interest rates for an extended period. The Fed’s upcoming decision on interest rates is eagerly anticipated, with expectations that the central bank will likely keep rates unchanged. Investors are looking for signals of a more dovish stance from the Fed to relieve downward pressure on rates and support a sustainable stock market rebound. Additionally, traders are hopeful for seasonal tailwinds in November, historically a strong month for markets, but they believe that a peak in bond yields will be necessary for a year-end rally.

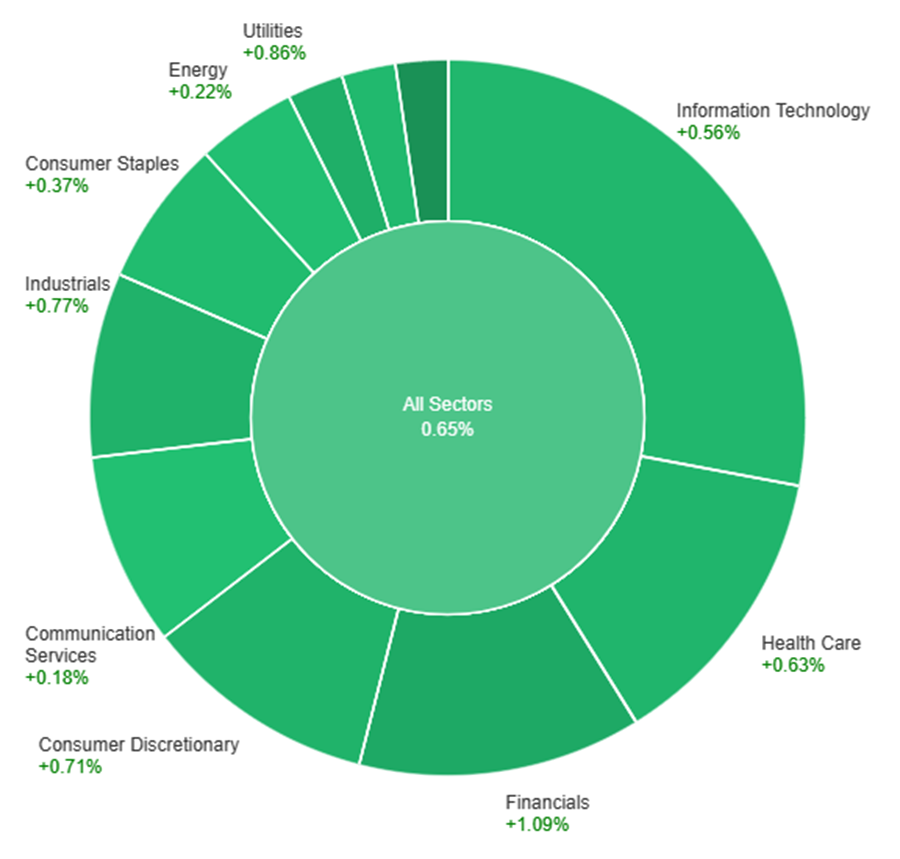

On Tuesday, the overall market showed a positive trend, with all sectors collectively gaining 0.65%. Among the sectors, Real Estate led the way with an impressive increase of 2.04%, followed by Financials at 1.09% and Utilities at 0.86%. Other sectors, such as Industrials, Consumer Discretionary, and Health Care, also experienced gains ranging from 0.63% to 0.77%. However, Information Technology, Materials, Consumer Staples, Energy, and Communication Services had more modest increases, ranging from 0.18% to 0.56%.

Currency Market Updates

In recent currency market developments, the US dollar demonstrated strength as the dollar index saw a 0.6% increase, primarily driven by a remarkable 1.6% surge in USD/JPY, nearing its 2022 peak. This surge was attributed to the Bank of Japan’s (BoJ) shift away from ultra-easy monetary policies, perceived by many as too little and too late in comparison to substantial rate hikes by other major central banks worldwide. Additionally, the US dollar gained broader traction following positive economic data from the United States. The U.S. employment cost index, home prices, and consumer confidence all exceeded expectations, leading to a 7-basis-point rise in 2-year Treasury yields, a 4-basis-point increase on the day. Conversely, the euro lost ground against the US dollar, falling 0.4%, as euro zone inflation and GDP figures came in slightly weaker than forecasts. This decline was further exacerbated by a narrowing of 2-year bund-Treasury yield spreads. Looking ahead, the currency market is keeping a watchful eye on developments like the ECB’s potential rate cuts, as well as any hints of changes in the Federal Reserve’s stance, which could impact the future direction of the EUR/USD pair.

In particular, USD/JPY made a remarkable 1.66% jump, reaching new highs for 2023 at 151.715, approaching the 32-year peak from October 21, 2022, at 151.94. This upward momentum raised concerns of potential pullback risks, particularly due to the narrowing of Treasury-JGB yield spreads as USD/JPY hit new highs. Traders may consider taking profits if the currency pair fails to close above the 2022 high. However, an unobstructed breakout could lead to a potential target at 155.19, representing the 161.8% Fibonacci retracement off the base from 2023 and exacerbating Japan’s imported inflation concerns. Meanwhile, USD/CAD rose by 0.4% to reach new highs for 2023, primarily influenced by recessionary GDP data. The Australian dollar fell by 0.6%, partially due to disappointing factory data from China, which also pushed USD/CNH close to October’s highs. Finally, the global market experienced lower prices for oil and copper, reflecting concerns about global economic growth risks. These factors collectively indicate an evolving landscape in the currency market, with central bank policies, economic data, and geopolitical factors playing significant roles in shaping the future direction of major currency pairs.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Retreats as Eurozone Data Misses Expectations, Eyes Turn to FOMC Meeting and US Employment Figures

The EUR/USD pair experienced a shift as it initially reached weekly highs before turning downward, driven by a stronger US Dollar in anticipation of US employment data and the FOMC meeting. Disappointing inflation and growth figures from the Eurozone, along with an impending ECB hold in December, contrasted with mixed US data on Tuesday. The focus now turns to the upcoming FOMC meeting and US employment reports, with the US Dollar’s support stemming from solid fundamentals, while market sentiment helps keep the EUR/USD pair away from recent lows.

According to technical analysis, the EUR/USD moves lower on Tuesday, approaching the middle band of the Bollinger Bands. Currently, the EUR/USD is trading below the middle band, indicating the potential for a slightly lower movement. The Relative Strength Index (RSI) is at 46, signaling that the EUR/USD is in neutral bias.

Resistance: 1.0616, 1.0705

Support: 1.0500, 1.0405

XAU/USD (4 Hours)

XAU/USD Fluctuates Amidst Mixed Economic Data and USD Demand Ahead of Fed Announcement

In the first half of the day, the XAU/USD saw a surge, reaching $2,007.91 per troy ounce, buoyed by optimism in European financial markets due to softer Euro Zone inflation figures. However, the American session witnessed a downturn as dismal US data spurred demand for the US Dollar. The US Consumer Confidence index dipped slightly in October, and Wall Street’s early gains were erased, contributing to USD strength. The Bank of Japan’s conservative stance on yield-curve control also impacted the currency market. Now, market participants await the US Federal Reserve’s November meeting with uncertainties surrounding the end of the tightening cycle.

According to technical analysis, XAU/USD is moving lower on Monday and able to reach the narrow lower band of the Bollinger Bands. Presently, the price of gold is consolidating near the lower band, creating a possibility to push lower and create a wider band. The Relative Strength Index (RSI) is currently at 42, indicating a neutral bias for the XAU/USD pair.

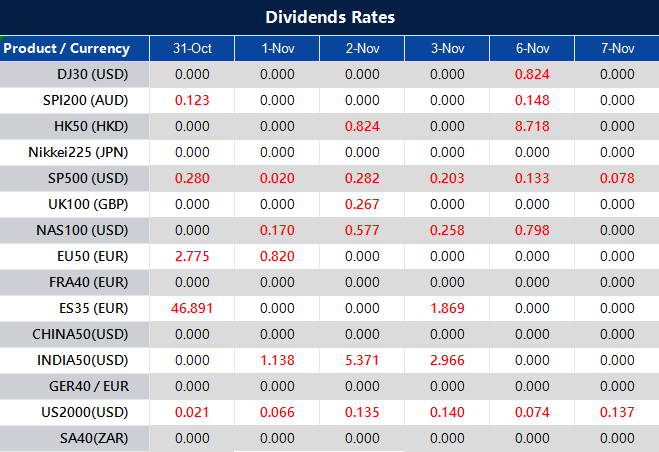

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

On Monday, the stock market experienced a significant rally, with the Dow Jones Industrial Average surging by over 500 points, pulling itself out of correction territory, while the S&P 500 and Nasdaq Composite also made substantial gains. The positive sentiment was attributed to the anticipation of the Federal Reserve’s rate decision and hopes of a pause in rate hikes. The US dollar declined as investors moved away from safe-haven assets. In the currency market, the Euro appreciated, while the British pound remained above recent lows, and the Australian dollar saw a notable rise. Market participants are closely watching central bank meetings and economic data releases that will shape currency market dynamics in the coming days.

Stock Market Updates

Stocks rallied on Monday, with the S&P 500 making significant gains and ending the day out of corrected territory. The Dow Jones Industrial Average surged by 511.37 points, or 1.58%, to reach 32,928.96, marking its best day since June 2. The S&P 500 also performed well, jumping 1.2% to 4,166.82, its best performance since late August. The Nasdaq Composite rose by 1.16% to 12,789.48. Communication services were the top-performing S&P 500 sector, gaining over 2%, with mega-cap tech stocks like Amazon and Meta Platforms rising by 3.9% and 2%, respectively. These gains followed a recent dip in the S&P 500 into correction territory, shedding 2.5% for the week, and it was down more than 10% from its 2023 closing high. The positive market sentiment on Monday was attributed to a lack of new negative developments over the weekend and a perception that bad news might have already been priced into the market.

Investors were eagerly anticipating the upcoming Federal Reserve rate decision, set for Wednesday, where it was widely expected that the central bank would maintain its benchmark interest rate at the current level. With surging interest rates being a key factor behind the recent market correction, investors hoped that the Fed would signal a pause in its rate-hiking cycle. This pause could provide some relief and potentially halt the rapid rise in Treasury yields. The 10-year Treasury yield, which had previously spiked above 5%, traded around 4.89% on Monday. Additionally, investors were looking forward to the October jobs report on Friday, with hopes that any signs of a slowing labor market could persuade the Fed to keep interest rates on hold for the remainder of the year. Furthermore, Apple was set to report its earnings on Thursday, and the stock was in correction territory, down 14% from its 52-week high. Overall, the market appeared to be responding positively to the potential for stability and improved economic conditions.

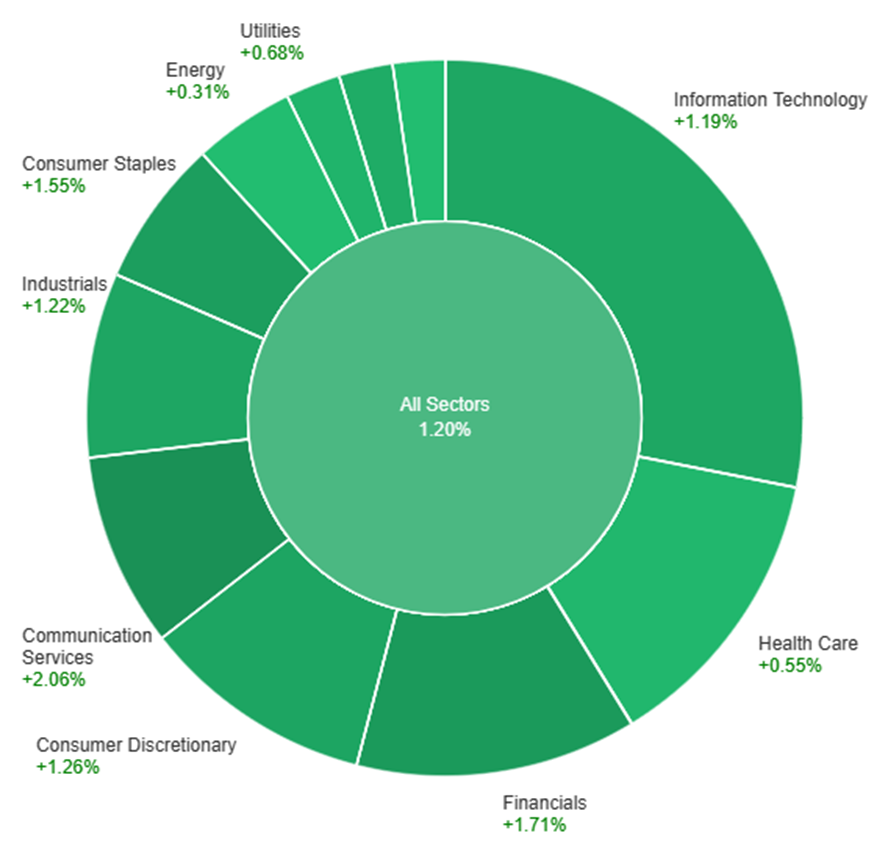

On Monday, the overall market showed a positive trend with a gain of 1.20%. Among the sectors, Communication Services saw the highest increase at 2.06%, followed by Financials at 1.71%, and Consumer Staples at 1.55%. The sectors of Energy and Real Estate had the lowest gains at 0.31%, while Health Care and Utilities also saw relatively modest increases at 0.55% and 0.68%, respectively.

Currency Market Updates

In the currency market, the US dollar experienced a 0.4% decline, driven by a resurgence in risk sentiment that prompted investors to move away from the safe-haven US currency. This decrease in the dollar index occurred as market participants prepared for upcoming central bank meetings, including those of the Bank of Japan (BoJ), the Federal Reserve (Fed), and the Bank of England (BoE). Additionally, traders were bracing for a barrage of critical economic data releases, with the eagerly awaited US employment report scheduled for Friday. The most intriguing event in this lineup is the BoJ’s announcement, particularly if it entails an increase in the current 1% yield cap on 10-year Japanese Government Bonds (JGBs) and a potential shift away from aggressive JGB purchases. Such a move, if implemented, could reduce the need for aggressive quantitative easing (QE) and provide support to the Japanese yen. If the USD/JPY exchange rate breaches a key support level at 149.04, it could test the lows observed during the flash-crash on October 3, ranging from 150.165 to 147.30. Market participants are also keenly watching for the Ministry of Finance (MoF) intervention report on Tuesday to ascertain if the MoF was responsible for the sudden dive in the yen on October 3. It’s noteworthy that, among major central banks like the Fed, European Central Bank (ECB), and BoE, the BoJ is currently considered the most likely to raise interest rates next year, as it does not face expectations of cutting rates in 2024.

Meanwhile, in other currency movements, the Euro (EUR) appreciated by 0.47% against the US dollar, reaching a high of 1.0625. This upward correction followed a period of oversold conditions in October and will need to overcome the 55-day moving average at 1.0675, which had previously capped the highs in the last week of October. The German economy, however, faced a setback with a 0.1% contraction in Q3 compared to Q2, defying expectations of a 0.3% drop. Moreover, October’s inflation rate in the Eurozone came in at 3.0% year-on-year, slightly below the anticipated 3.3% and a decrease from the 4.3% rate recorded in September.

In the British pound (GBP) market, the sterling appreciated by 0.3%, remaining above the lows observed in October but staying below the downtrend line from July. This movement occurred against the backdrop of a mostly discouraging streak of economic data. The Australian dollar (AUD) also witnessed a notable 0.67% rise, benefiting from strong retail sales and a broader reduction in US dollar long positions amid decreasing risk aversion.

Looking ahead, the market’s attention is focused on key data releases, including euro zone inflation and GDP figures, followed by US data on the Employment Cost Index (ECI), home prices, and consumer confidence. Additionally, the schedule includes reports on Mortgage Bankers Association (MBA) data, the ADP employment report, ISM manufacturing data, and the JOLTS report, leading up to the post-meeting press conference by Federal Reserve Chair Jerome Powell on Wednesday. These developments are expected to further shape the dynamics in the currency market in the coming days.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Climbs Above 1.0600 as Dollar Weakens Ahead of FOMC Meeting and Key Data

The EUR/USD pair surged above 1.0600 during the American session, driven by a weakened US Dollar in anticipation of the upcoming FOMC meeting and crucial jobs data. The Euro received additional support from positive Eurozone economic data. Notably, Germany’s economic contraction in the third quarter was less severe than anticipated, and inflation rates in October eased below expectations. These factors support the expectation that the European Central Bank (ECB) will maintain its current stance. While the Federal Reserve (Fed) is set to keep rates unchanged, strong economic performance in the US allows for potential rate hikes in the future. Key US data releases throughout the week will influence the US Dollar’s momentum.

According to technical analysis, the EUR/USD moved higher on Monday, approaching the upper band of the Bollinger Bands. Currently, the EUR/USD is trading around the upper band, indicating the potential for a slightly lower movement. The Relative Strength Index (RSI) is at 58, signaling that the EUR/USD is in neutral bias.

Resistance: 1.0616, 1.0705

Support: 1.0500, 1.0405

XAU/USD (4 Hours)

XAU/USD Dips Below $2,000 Amidst Global Uncertainty and Central Bank Speculation

Gold (XAU/USD) is struggling to maintain the $2,000 mark after reaching a high of $2,009.34 last Friday, the highest level since mid-May. The demand for safe-haven assets has waned at the start of the week, impacting both Gold and the US Dollar. Global attention is focused on Middle East developments, including Israel’s ground offensive in the Gaza Strip, and anticipation is building for key central bank decisions, with the Federal Reserve, Bank of Japan, and Bank of England set to announce their monetary policies this week. Additionally, the US employment situation and upcoming economic reports are expected to influence Gold’s performance, while stock markets remain positive and Treasury yields rise, albeit not providing strong support for the US Dollar.

According to technical analysis, XAU/USD is consolidating on Monday and has the potential to reach the middle band of the Bollinger Bands, which is currently squeezing. Presently, the price of gold is consolidating near the middle band, implying a possible downward consolidation. The Relative Strength Index (RSI) is currently at 58, indicating a neutral bias for the XAU/USD pair.

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

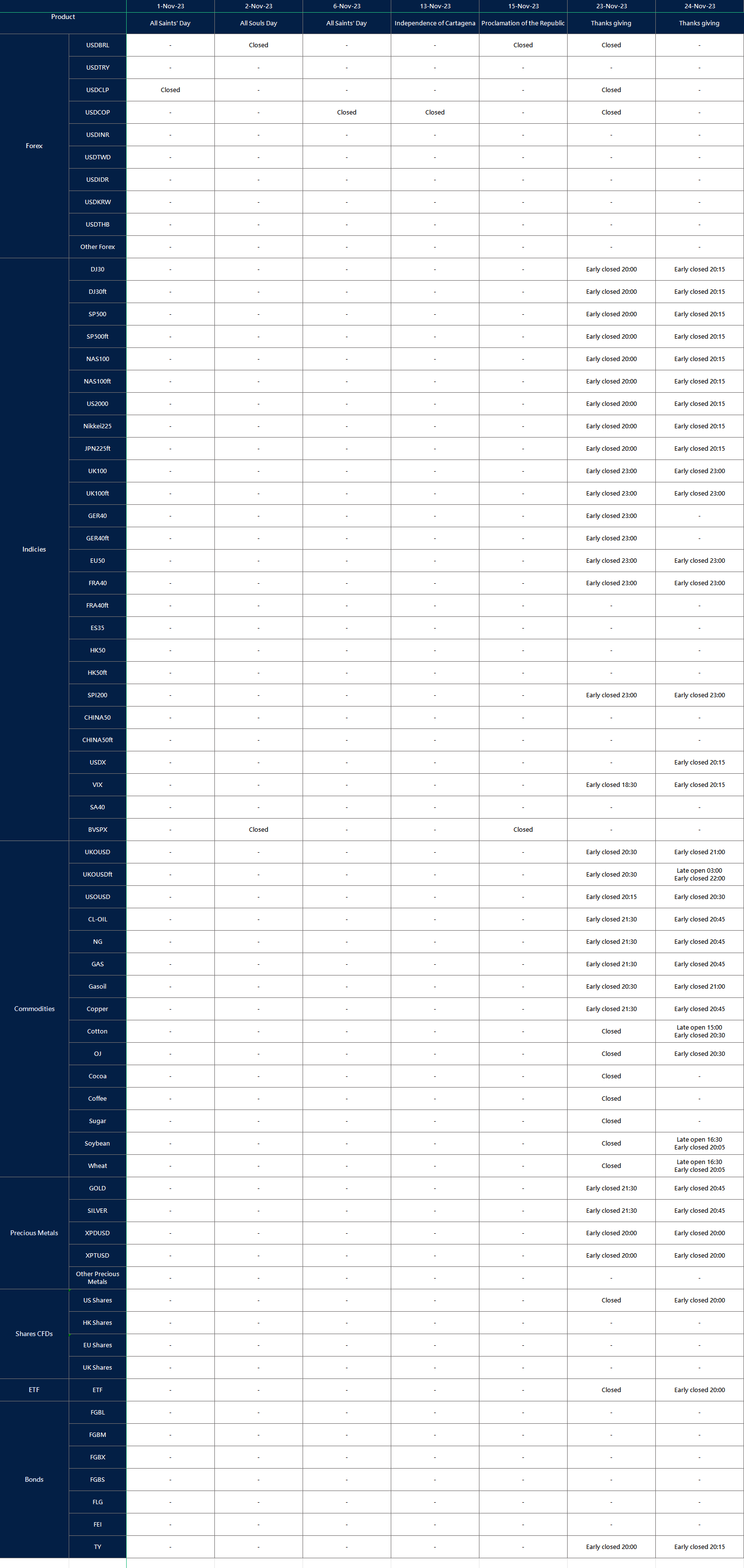

This week, traders are primarily focused on the rate decisions of major central banks, such as the Federal Reserve and Bank of England. Alongside these, the US Jobs Report is slated for release, serving as a critical indicator for the US’ economic health. Traders and investors are advised to be cautious, as these events could drive market fluctuations.

BOJ Rate Statement (31 October 2023)

In its September meeting, the Bank of Japan (BoJ) unanimously voted to keep its key short-term interest rate at -0.1% and the 10-year bond yields at 0%.

Analysts predict that the central bank will keep these interest rate levels in its upcoming meeting on 31 October.

Canada Gross Domestic Product (31 October 2023)

Canada’s economy showed stagnation in July, following a 0.2% decline in June.

Analysts expect a 0.1% growth for Canada’s GDP in August, with the figures set to be released on 31 October.

US FOMC Rate Statement (2 November 2023)

During its meeting in September, the Federal Reserve (Fed) maintained the target range for its funds rate at a 22-year high of 5.5%.

Analysts predict that the Fed will keep interest rates steady at 5.5% in the upcoming meeting on 2 November.

Bank of England Rate Statement (2 November 2023)

In its September meeting, the Bank of England held its policy interest rate at 5.25%, the highest level since 2008. This was influenced by the latest inflation and labour data.

As the next meeting approaches on 2 November, analysts predict that the central bank will maintain the rate at 5.25%.

Canada Employment Change (3 November 2023)

The Canadian economy added 63,800 jobs in September 2023, the highest in eight months. However, the unemployment rate held steady at 5.5% for the third consecutive month.

Looking ahead, analysts forecast an addition of 24,600 jobs for October. These figures, due for release on 3 November, are also expected to show a slight rise in the unemployment rate to 5.6%.

US Jobs Report (3 November 2023)

The US nonfarm payrolls saw a increase of 336,000 in September, while the unemployment rate stayed steady at 3.8%.

For October 2023, the data set to be released on 3 November is anticipated to report an addition of 172,000 jobs, with the unemployment rate projected to remain at 3.8%.

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

In a turbulent market session, the Nasdaq Composite entered correction territory, partly driven by Meta’s underwhelming forecast, and Alphabet’s disappointing results added to the pressure. The S&P 500 briefly touched correction territory, and Wall Street grappled with concerns about the US economy’s outlook. Meanwhile, the US dollar displayed resilience on the back of strong Q3 GDP growth. In the currency market, the dollar saw fluctuations as the Federal Reserve and European Central Bank were expected to make rate decisions. The Japanese yen faced the risk of intervention from the Ministry of Finance. The British pound and Australian dollar saw rebounds. Upcoming economic data releases are poised to continue influencing market dynamics.

Stock Market Updates

The Nasdaq Composite extended its decline into correction territory as Meta, the parent company of Facebook, reported a forecast that fell short of investors’ expectations. The tech-heavy index dropped by 1.76% on Thursday, closing at 12,595.61, falling below its 200-day moving average. The S&P 500 also dipped 1.18% to close at 4,137.23, with the Dow Jones Industrial Average slipping 0.76%, shedding 251.63 points to end at 32,784.30. The S&P 500 briefly entered correction territory during the session, marking a nearly 10% decline from its peak in July. The Nasdaq Composite officially entered correction territory, down more than 10% from its yearly high. Wall Street seemed unimpressed with recent big-tech earnings reports, with concerns about the weakening outlook for the US economy. Meta reported a beat on both top and bottom lines in the third quarter but noted advertising softness and concerns about cost control, leading to a 3.7% drop in Meta’s shares.

This decline in the stock market was influenced by a challenging trading session on Wednesday, driven by a 9.5% decline in Google-parent Alphabet, which had its Class-A shares experience their worst day since March 2020 after disappointing results in the Google cloud unit. The market’s recent correction since the summer has been partly attributed to rising bond yields, with the 10-year Treasury yield crossing 5% earlier in the month. Despite a slight decrease in the 10-year yield to 4.84% on Thursday, it did not halt the market sell-off. The market also didn’t receive a boost from the stronger-than-expected third-quarter gross domestic product (GDP) report, with the US GDP growing at a 4.9% annualized rate from July through September, surpassing the 4.7% forecast by economists. Furthermore, major earnings reports are on the horizon, with Amazon scheduled to release its results after the market’s close.

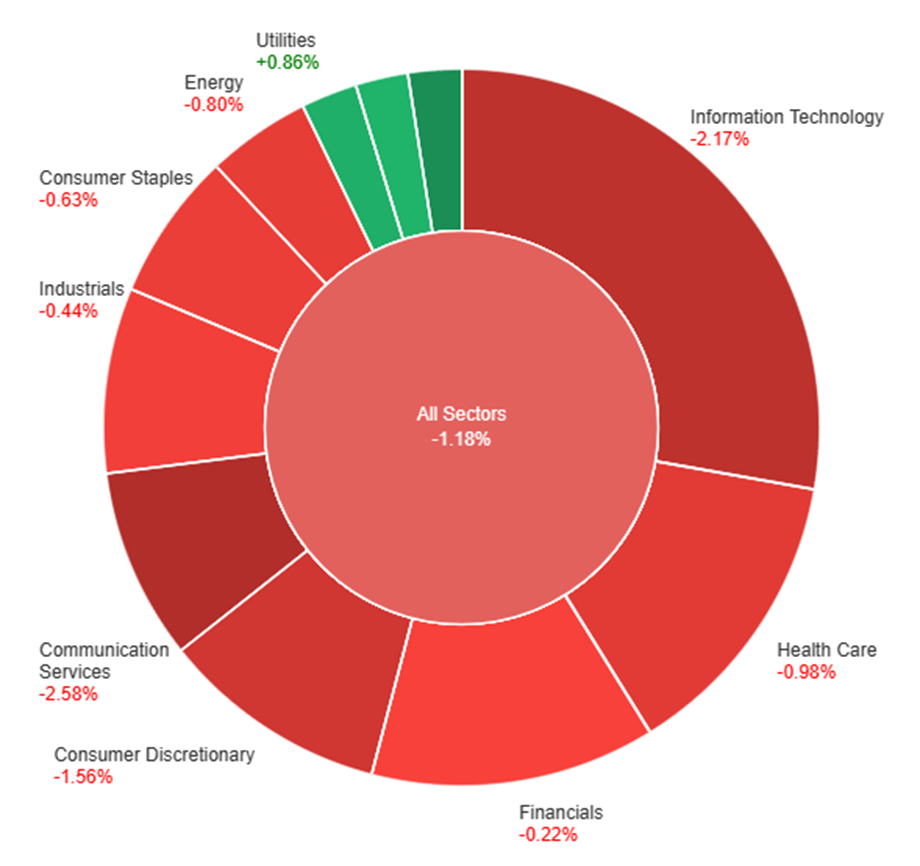

On Thursday, various sectors experienced fluctuating performance in the market. Real Estate and Utilities showed positive gains, with increases of 2.15% and 0.86%, respectively. However, Information Technology and Communication Services had a rough day, with notable declines of 2.17% and 2.58%. Overall, the broader market, represented by “All Sectors,” saw a decrease of 1.18%, while several sectors, including Consumer Discretionary, Health Care, and Consumer Staples, also ended in the red with declines ranging from 0.63% to 1.56%.

Currency Market Updates

In the latest currency market updates, the US dollar displayed resilience as it strengthened by 0.1%, despite a minor retreat in Treasury yields. This rally was prompted by robust US economic data, as Q3 GDP grew impressively at a 4.9% rate. However, the sales and core PCE figures fell short of expectations, with core PCE at 2.4% compared to 3.7% in the previous quarter. While September core capital goods orders exceeded forecasts, initial and continued jobless claims saw an increase, signaling potential challenges in finding new employment. Additionally, pending home sales surpassed expectations but remained notably weak. The EUR/USD pair experienced a 0.05% decline, with the dollar gaining momentum as both the Federal Reserve and the European Central Bank (ECB) were expected to cease their rate hikes and potentially cut rates by mid-year. The USD/JPY pair rose by 0.1%, although it had retreated from its 2023 highs at 150.78 due to a decline in Treasury yields and market concerns about the Bank of Japan’s future policy decisions. Despite these fluctuations, the main perceived risk in the currency market is the possibility of the Ministry of Finance (MoF) resuming yen buying to prevent a breakout above 2022’s 32-year high at 151.94.

Meanwhile, the British pound saw a 0.2% increase in value after hitting its lowest level since October’s 1.2038 trend lows. This rebound came in the wake of a pullback in Treasury yields, despite concerning reports of CBI sales and reduced UK public inflation expectations. The Australian dollar also displayed resilience with a 0.3% increase, recovering from its lows in 2023. This recovery was attributed to a potential change in the Reserve Bank of Australia’s policy outlook.

Looking ahead, upcoming economic data releases include Tokyo core CPI for October, expected to remain steady at 2.5%, as well as German GDP and retail sales figures. Additionally, the US market will be closely monitoring data on personal income, spending, core PCE, and Michigan sentiment. These indicators will likely continue to influence the dynamics of the currency market in the days to come.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Finds Support Despite Dovish ECB Stance and Robust US Growth Data

The EUR/USD pair hit a bottom at 1.0521, aligning with the previous week’s lows. This drop came as the European Central Bank (ECB) adopted a more dovish stance, hinting at a possible terminal interest rate amidst economic concerns. Meanwhile, the US Dollar failed to capitalize on better-than-expected US GDP figures, as the Core PCE remained slightly below expectations and employment data raised concerns. Despite these dynamics, the fundamental factors suggest a mixed outlook for EUR/USD, with potential influences from upcoming US Core PCE data.

According to technical analysis, the EUR/USD consolidated on Thursday, approaching the middle band of the Bollinger Bands. Currently, the EUR/USD is trading between the middle and lower bands, indicating the potential for further downward movement. The Relative Strength Index (RSI) is at 43, signaling that the EUR/USD is adopting a bearish bias.

Resistance: 1.0616, 1.0705

Support: 1.0500, 1.0405

XAU/USD (4 Hours)

XAU/USD Resilient as Economic Uncertainties Persist Amid ECB and US GDP Reports

Spot Gold initially surged to $1,993.44 an ounce before receding, influenced by key developments in global economics. The European Central Bank opted to keep rates unchanged due to the Euro Zone’s economic struggles, while the US Dollar strengthened following a robust Q3 GDP report. The uncertain economic outlook drove investors to seek safety in Gold, contributing to its rebound as stock markets faced headwinds.

According to technical analysis, XAU/USD is consolidating on Thursday and has the potential to reach the upper band of the Bollinger Bands, which is currently squeezing. Presently, the price of gold is consolidating near the upper band, implying a possible downward consolidation. The Relative Strength Index (RSI) is currently at 57, indicating a neutral bias for the XAU/USD pair.