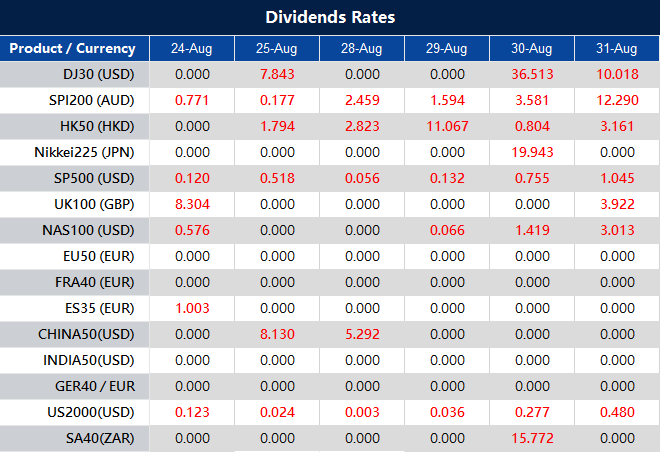

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

In a dramatic turn of events, the stock market experienced a sharp decline following a brief surge triggered by Nvidia’s impressive quarterly results. As the tech rally faded, investors also braced themselves for a significant address from Federal Reserve Chairman Jerome Powell. The Dow Jones Industrial Average closed with a hefty loss of 373.56 points, marking a 1.08% drop to settle at 34,099.42. Similarly, the S&P 500 witnessed a substantial decline of 1.35%, concluding the day at 4,376.31, while the Nasdaq Composite, renowned for its tech-heavy constituents, plunged by 1.87% to reach 13,463.97.

This Thursday brought forth the Dow’s most challenging day since March, while the S&P 500 and Nasdaq encountered their most significant single-day losses since August 2nd. Nvidia, a prominent tech player, reported better-than-expected earnings and revenue, propelling its shares to an all-time high. Although the company’s leadership projected a remarkable third-quarter revenue increase of 170% year-over-year, the stock only managed a meager 0.1% gain by the closing bell. Meanwhile, the tech sector faced a notable setback, causing the S&P 500’s largest loss of 2.15%. Renowned tech giants like Amazon, Apple, and Netflix saw their shares decrease during the session, with losses ranging from 2.6% to 4.8%. As the market awaits Powell’s speech, U.S. Treasury yields climbed, touching 4.241% for the benchmark 10-year Treasury note.

On Thursday, all sectors of the stock market experienced a decline of 1.35%. Among the various sectors, technology and communication services were hit the hardest, both dropping by 2.15% and 2.04% respectively. Consumer discretionary also faced a substantial decrease of 2.01%. Industrials followed with a decline of 1.22%. Health care, energy, and utilities sectors recorded losses of 0.76%, 0.74%, and 0.63% respectively. Financials, real estate, and materials sectors had more modest declines, each decreasing by 0.24%, 0.41%, and 0.43%. The consumer staples sector also saw a decrease of 0.77% in its value.

Major Pair Movement

The US Dollar Index rebounded and surged above 104.00, marking its highest point since early June after a brief correction. This resurgence was fueled by fundamental factors, risk aversion, and higher US Treasury yields, all of which contributed to the strengthening of the Greenback. All eyes are on the Jackson Hole event, with European Central Bank President Christine Lagarde and Federal Reserve Chair Jerome Powell scheduled to speak. Their speeches are anticipated to induce volatility and potentially lead to significant movements in financial markets. Despite mixed data from the US on Thursday, including a 5.2% decline in July’s Durable Goods Orders (versus an expected -4%) and a lower than expected initial Jobless Claims of 230K (versus 240K expected), the US Dollar remained resilient. The University of Michigan’s Consumer Sentiment report is expected to be released on Friday. Additionally, Federal Reserve officials’ comments varied, with some suggesting that policy actions may have been sufficient, while others warned of the possibility of further rate hikes.

The 10-year US Treasury yield rebounded to 4.2%, though it remained below recent peaks, while the 2-year yield climbed back above 5%. These rising yields exerted pressure on the Japanese Yen, causing USD/JPY to rise from 144.65 to 145.85, poised for Jerome Powell’s speech. Meanwhile, EUR/USD retreated to 1.0800, trading with a bearish bias just above the 200-day Simple Moving Average (SMA). ECB President Christine Lagarde’s speech at Jackson Hole and upcoming data on German Q2 GDP and the IFO Survey are awaited. USD/CHF consolidated above 0.8800, achieving its highest daily close in a month around 0.8850, as Switzerland prepared to release Q2 employment data. Conversely, GBP/USD resumed its downtrend, slipping below 1.2600 after failing to hold above the 20-day SMA at 1.2740. In the Antipodean region, AUD/USD reversed its gains from Wednesday and neared the 0.6400 mark, while NZD/USD struggled to regain 0.6000 and dropped to 0.5920, both currencies facing pressure amidst cautious market sentiment.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Nears Crucial Levels Amidst Dollar’s Resurgence Ahead of Powell’s Jackson Hole Speech

The EUR/USD currency pair has edged back towards significant technical thresholds following a brief rebound that faltered near 1.0870. This pullback occurred as the US Dollar regained strength in anticipation of Federal Reserve Chair Jerome Powell’s imminent address at Jackson Hole on Friday. Despite mixed data from the US and no definitive cues from Fed officials, the Greenback managed to strengthen. US stocks saw declines, while US Treasury yields rebounded, contributing to the Dollar’s resurgence. US economic indicators revealed a notable 5.2% drop in Durable Goods Orders for July, exceeding the anticipated 4% decrease. Furthermore, Initial Jobless Claims declined to 230,000, surpassing the projected 240,000 figure.

European Central Bank (ECB) Governing Council member Mario Centeno delivered a cautionary stance on Thursday, expressing the need for prudence in upcoming meetings. He highlighted the realization of downside risks to the economy, aligning with the prevailing downtrend in expectations for additional monetary policy tightening from the ECB. These dovish remarks have potentially contributed to the EUR/USD’s weakness. As the week progresses, Germany is set to release updated data on Q2 GDP and the ZEW Survey, while the University of Michigan’s Consumer Sentiment Survey will be a focal point in the US. However, all eyes remain fixed on Jackson Hole, where ECB President Christine Lagarde will speak at 11:00 GMT, followed by Fed Chair Jerome Powell at 14:00 GMT. These speeches have the potential to trigger substantial market movements across various sectors.

In line with technical analysis, the EUR/USD declined on Thursday, reaching the lower boundary of the Bollinger Bands. At present, the price is hovering close to this lower boundary. The Relative Strength Index (RSI) is currently at 34, signaling a return to bearish sentiment for the EUR/USD.

Resistance: 1.0874, 1.0935

Support: 1.0789, 1.0740

XAU/USD (4 Hours)

XAU/USD Maintains Rally Near $1,923 Amid Dollar’s Volatile Performance

Spot Gold continued its weekly ascent, reaching $1,923.34 per troy ounce and sustaining modest intraday progress, just below this mark during the mid-American session. The US Dollar experienced selling pressure throughout the first half of the day, influenced by a decline in government bond yields and favorable stock market performance.

The USD briefly garnered demand following the release of mixed US data. Durable Goods Orders endured a substantial 5.2% plunge in July, significantly worse than anticipated. Conversely, Initial Jobless Claims for the week concluding on August 18 displayed improvement at 230K, surpassing the expected 240K. The July Chicago Fed National Activity Index also signaled a shift, rising to 0.12 from the previous month’s -0.33.

Macro figures triggered a decline in stock markets, causing Wall Street to further retreat after the opening bell. Despite optimistic remarks from Federal Reserve (Fed) officials, including Boston Federal Reserve President Susan Collins mentioning a possible steadying of the policy rate and Federal Reserve Bank of Philadelphia President Patrick Harker suggesting the Fed might have “done enough” with monetary policy, the market mood dampened. The USD found strength amid this sentiment, further supported by improved Treasury yields, which in turn curbed the extension of gains for XAU/USD (the Gold/US Dollar pair).

Using technical analysis, the XAU/USD didn’t change much on Thursday and stayed between the higher and middle bands of the Bollinger Bands. Right now, the price is still in that same zone between the middle and upper bands. The Relative Strength Index (RSI) is at 61 currently, showing that the XAU/USD pair is still in a positive mode.

Resistance: $1,926, $1,945

Support: $1,910, $1,896

Economic Data

Currency

Data

Time (GMT + 8)

Forecast

EUR

German ifo Business Climate

16:00

86.8

USD

Revised UoM Consumer Sentiment

22:00

71.2

USD

Fed Chair Powell Speaks (Jackson Hole Symposium)

22:05

EUR

ECB President Lagarde Speaks (Jackson Hole Symposium)

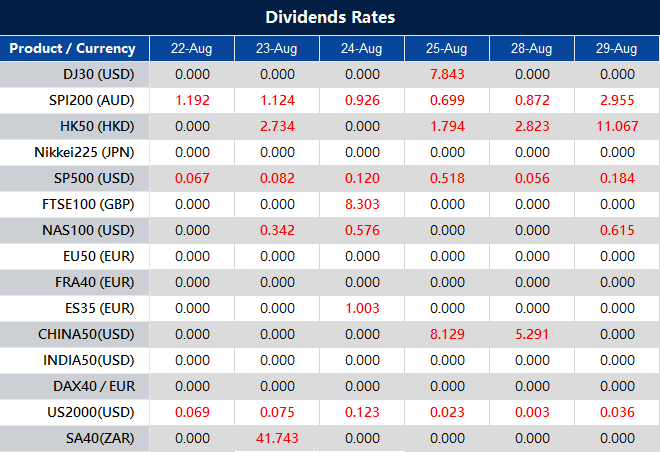

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

Stocks closed higher on Wednesday as investors awaited Nvidia’s latest quarterly earnings report, with the company being a top performer in the S&P 500 due to its association with the artificial intelligence trend. The Dow Jones Industrial Average rose by 0.5%, the S&P 500 had its best daily performance since June 30 with a 1.1% gain, and the Nasdaq Composite climbed 1.6% for a third consecutive day of gains. Nvidia’s report was anticipated to show substantial year-over-year increases in profit and revenue. Investors are keen on the results to gauge the continued momentum of the AI trend, which has propelled Nvidia’s significant stock gains. The benchmark 10-year Treasury yield’s decline by over 11 basis points to 4.21% was also well-received by traders, while concerns over inflation and slowing demand negatively affected athletic apparel stocks like Nike and Foot Locker.

Investors are keeping an eye on Nvidia’s earnings report as the company’s stock has surged over 200% in 2023, largely due to its AI-related prospects. The positive sentiment on Wall Street was further boosted by a decline in the 10-year Treasury yield, which fell by more than 11 basis points to 4.21%. However, athletic apparel stocks faced challenges amidst worries about inflation and decreasing demand, with Nike experiencing its longest losing streak on record and Foot Locker reporting shrinking sales and reducing its forecast. The anticipation of the Federal Reserve symposium in Jackson Hole, Wyoming, and Fed Chair Jerome Powell’s upcoming remarks also drew attention from investors. The market’s short-term direction is seen to hinge significantly on Nvidia’s earnings and how it reflects the AI trend’s momentum, with cautionary notes about stretched valuations and potential market implications in the face of changing economic conditions.

On Wednesday, across all sectors, the market witnessed a positive movement with a gain of 1.10%. The Information Technology sector showed strong growth, leading with a substantial increase of 1.92%, closely followed by the Communication Services sector, which also surged by 1.90%. The Real Estate sector experienced a notable rise of 1.46%, while the Industrials sector saw a more moderate gain of 0.99%. Financial and Consumer Discretionary sectors exhibited growth of 0.93% and 0.83% respectively. The consumer Staples and Utilities sectors showed smaller yet positive increases of 0.63% and 0.45% respectively. The Health Care and Materials sectors saw minor gains of 0.29% and 0.18% respectively. However, the Energy sector faced a decline of -0.30% on the same day.

Major Pair Movement

The US Dollar saw a significant decline, marking its weakest performance since early August, with the Dollar Index (DXY) falling below 103.50 from its recent high around 104.00. This correction was driven by weaker-than-expected US PMI figures and a pullback in US Treasury yields, notably the 10-year yield dropping below 4.20%. The risk-on sentiment was boosted, leading to gains in major indices like the Dow Jones and Nasdaq. The anticipation of Fed Chair Powell’s speech at the Jackson Hole Symposium is notable, as it could shape upcoming policy directions. The Eurozone experienced a drop in the Composite PMI, indicating a contraction, likely impacting ECB projections and hinting at potential policy adjustments. Similarly, the UK’s Composite index fell below 50, weakening GBP/USD and boosting EUR/GBP. The Japanese yen gained ground against the US dollar due to lowered expectations of tightening by central banks, and the Australian dollar rebounded despite disappointing PMI data. Precious metals like gold and silver surged, while cryptocurrencies, including Bitcoin and Ethereum, enjoyed gains due to improved risk sentiment.

Despite its recent highs, the US Dollar weakened notably due to disappointing US PMI data and a decrease in US Treasury yields. The risk-on sentiment was evident in the positive performance of stock indices, and market participants are looking forward to Fed Chair Powell’s speech. The Eurozone and the UK both showed signs of economic contraction, influencing currency dynamics. The Japanese yen benefited from reduced tightening expectations, while the Australian dollar rebounded despite weak data. Precious metals and cryptocurrencies also experienced positive shifts in line with the risk sentiment.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Rebounds on Weaker Dollar, Eurozone PMI Impact, and Upcoming Central Bank Speeches

The EUR/USD exhibited a rebound, finding support above the 200-day Simple Moving Average and driven by a weakened US Dollar. The recovery from the 1.0800 level has brought the pair to test the 1.0870 area, although the overarching trend remains downwards. The Euro’s decline was initially triggered by the Eurozone’s preliminary August PMI figures, with the Composite dropping from 48.6 to 47, indicating contraction. Surprisingly, Services PMI dipped to 48.3 while Manufacturing PMI rose to 43.7. This data has dampened expectations for a September rate hike from the European Central Bank (ECB), influencing the Euro’s performance.

In the US, Wednesday’s data revealed a drop in the S&P Global Composite PMI from 52 to 50.4, with Manufacturing PMI falling to 47, contrary to expectations. The Services PMI also slipped from 52.3 to 51. These figures led to losses in the US Dollar, prompting a corrective movement. Additionally, US Treasury yields retreated, contributing to a weakened Dollar and aiding the EUR/USD pair’s rebound. Looking ahead, attention remains on the Jackson Hole Symposium, particularly speeches by Fed Chair Powell and ECB President Lagarde on Friday, even as Thursday’s data includes weekly Jobless Claims and Durable Goods Orders.

According to technical analysis, the EUR/USD moved higher on Wednesday and managed to reach the middle band of the Bollinger Bands. Currently, the price is slightly below the middle band of the Bollinger Bands. The Relative Strength Index (RSI) currently stands at 47, indicating that the EUR/USD is currently back in a neutral mode.

Resistance: 1.0935, 1.1038

Support: 1.0837, 1.0789

XAU/USD (4 Hours)

XAU/USD Surges as Dollar Softens Amidst Retreat in Yields and Positive Asian Markets

On Wednesday, spot gold experienced a notable shift, surging towards the $1,920 price range. The US Dollar exhibited a weakened stance through the first half of the day, influenced by declining government bond yields. Despite negative cues from American stock markets, Asian markets demonstrated resilience and moved higher.

European indices maintained an optimistic outlook despite unfavorable news for the Euro Zone. S&P Global’s preliminary August PMI estimates indicated a much worse situation than anticipated, revealing the region’s fastest contraction in business activity in over two years. The USD’s decline continued after the release of US figures, where the Manufacturing PMI reached a two-month low of 47.0, and services output dropped to a six-month low of 51.0. American stocks held their ground in positive territory, while Treasury yields retreated further, with the 10-year Treasury note now offering 4.20%, down by 12 basis points (bps).

Based on technical analysis, the XAU/USD moved higher on Wednesday and was able to reach the upper band of the Bollinger Bands. Currently, the price is moving just around the upper band of the Bollinger Bands. The Relative Strength Index (RSI) is currently at 67, indicating that the XAU/USD pair is now in bullish mode.

VT Markets is a global, multi-asset brokerage company specializing in Contract for Differences (CFD) and Foreign Exchange Market (Forex) trading. The Australia-based company has spent almost a decade building an innovative and trusted brand for retail traders, with over 200,000 active clients from more than 160 countries, and an average daily trade volume of over 4 million trades every month — traders can open an account with VT Markets in as little as five minutes.

Forex trading has reached new highs, with a daily turnover of $7.5 trillion in 2022, up from $6.6 trillion in 2019. There are approximately 10 million Forex traders globally.

Brokerage firms like VT Markets can often help traders with everything from the mechanics of the trade to providing advice on how to make smart investment decisions. For traders, it is important to find a brokerage firm that they can trust and which has the financial instruments and the platform to support them in their trading.

VT Markets’ Mission Of Accessible Trading

VT Market is setting out to build a reliable, accessible platform that can serve all traders. Mobile app trading has been growing in popularity, with over $22 billion in revenue generated by app trading in 2022. Additionally, over half of all Forex traders prefer trading using a mobile device or app. VT Markets gives its traders a variety of platforms to choose from, including the popular MetaTrader 4 and 5 platforms, as well as WebTrader, WebTrader+ and the VT Markets app.

The level of accessibility the platform offers is one of its key differentiating factors, with many competitors carrying far more restrictions on instruments and requirements. VT Markets provides its users with access to over a thousand financial instruments that allow them to trade almost every asset class — including Commodities, Gold and ETFs.

The brokerage is the recipient of numerous brokerage awards, including Best Forex Broker Europe 2023 Awarded by Forex Awards, Fastest Growing Broker Europe 2023 Awarded by Global Business Review Magazine, Best Multi-Asset Broker MENA 2023 Awarded by International Business Magazine and more.

The company believes all these awards are a recognition of its stated mission “to make trading easy and accessible for everyone.” VT Markets is looking to become one of the easiest-to-use trading solutions that provides retail traders with a comprehensive set of tools within a safe, regulated environment. This includes up to 500:1 trading leverage, a robust account management portal, and even potential extra trading bonuses.

This post contains sponsored content. This content is for informational purposes only and not intended to be investing advice.

About VT Markets:

VT Markets is a global multi-asset broker, providing access to a wide range of financial markets for traders and investors worldwide. With a strong commitment to innovation, technology, and client satisfaction, VT Markets offers competitive trading conditions, advanced trading platforms, and a comprehensive suite of educational resources. As a responsible corporate citizen, VT Markets is dedicated to making a positive impact on society through its corporate social responsibility initiatives.

For more information, please visit the official VT Markets website. Alternatively, follow VT Markets on Meta, Instagram, or LinkedIn.

For media enquiries and sponsorship opportunities, please email [email protected]

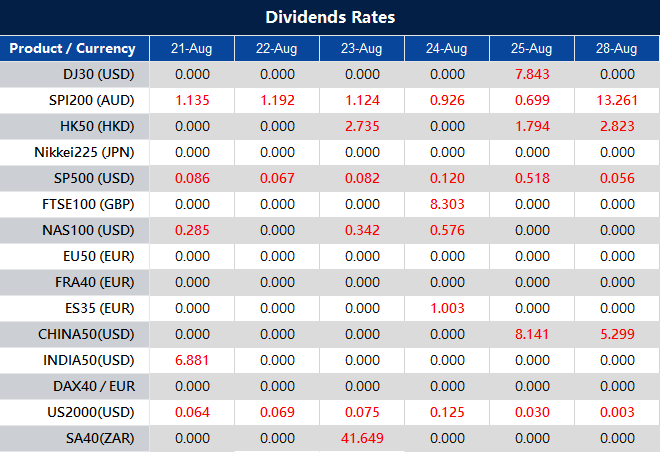

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

The S&P 500 experienced a 0.3% decline driven by concerns over rising Treasury yields and upcoming remarks from Federal Reserve Chairman Jerome Powell. The decline was also impacted by a drop in banking and retail shares. The Dow Jones Industrial Average followed suit, slipping by 0.5% to 34,288.83, while the Nasdaq Composite managed a small gain at 13,505.87. Notably, Nvidia’s stock dipped 2.9%, offsetting an earlier increase.

Bank ratings adjustments and challenging operating conditions caused several banks, both regional and larger, to witness declines. Consequently, the financial sector saw a 0.9% drop, making it the day’s poorest-performing sector within the S&P 500. Major banks like KeyCorp, Comerica, and JPMorgan Chase faced declines of 4.1% and 2.1% respectively. Meanwhile, Dick’s Sporting Goods and Macy’s tumbled by 24% and 14%, leading to a downward trajectory for the SPDR S&P Retail ETF. Nike also recorded over a 1% slide, marking its ninth successive daily loss. Wall Street’s attention has been on the bond market, particularly the 10-year Treasury yield, which reached its highest point since 2007 during the week. The yield dipped slightly to 4.33% on Tuesday.

Market analysts anticipate a continued market pullback. They point to the influence of climbing yields and a cautious consumer sentiment as drivers of this trend. Investors are eagerly awaiting Federal Reserve Chairman Jerome Powell’s speech at the Jackson Hole economic symposium on Friday, which is expected to provide insights into the central bank’s future monetary policy decisions.

On Tuesday, most sectors experienced a slight decline, with the overall market slipping by 0.28%. The Real Estate sector managed a 0.28% gain, while Utilities and Communication Services saw increases of 0.26% and 0.18% respectively. On the positive side, Consumer Discretionary showed a marginal uptick of 0.09%. However, several sectors faced losses, including Energy and Financials, which saw declines of 0.77% and 0.88% respectively. The Consumer Staples sector had the largest drop at 0.53%, followed by Health Care at 0.37%, Information Technology at 0.24%, and Industrials at 0.20%.

Major Pair Movement

The dollar index exhibited a 0.24% increase, led by a 0.36% decline in EUR/USD, pushing the euro close to breaking its pivotal lows from July. The possibility of this break is tied to Federal Reserve Chair Jerome Powell’s upcoming speech at Jackson Hole and the potential for its content to align with statements from Richmond Fed President Barkin. Despite a temporary alleviation from recent events that might have contributed to the Treasury yield’s retreat from post-GFC highs, the 2-year bund-Treasury yield spreads hit new lows for 2023. This shift coincided with the Treasury curve inverting further due to the attraction of high 10-year yields and short-covering. Barkin’s comments, which deviated from his generally dovish stance, introduced the risk that Powell could emphasize relative U.S. economic strength and the importance of achieving the Fed’s 2% inflation mandate.

The uncertainty centers on the potential length of elevated interest rates by the Fed and the implications for inflation. The conversation also includes evaluating the impact of China’s economic challenges. Jens Eskelund, President of [unspecified institution], weighed in on these matters. Despite the Fed’s stance based on strong economic growth and a tight labor market, both S&P and Moody’s have expressed concerns, leading to a market prediction of almost 100 basis points of Fed rate cuts next year, coinciding with one of the most rapid rate increases in decades. The USD/JPY pair dropped by 0.25%, reflecting a retreat in Treasury yields, while sterling faced a 0.13% decline due to factors including the dollar’s broader rebound from Barkin’s comments and an equities pullback. USD/CNH saw a 0.22% rise, in contrast to USD/CNY’s 0.09% gain. The focus now shifts to the global PMIs scheduled for Wednesday and Powell’s upcoming presentation on Friday.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Hits Mid-June Lows Amidst Dollar’s Strength and Economic Concerns

The EUR/USD currency pair experienced a significant drop, marking its lowest daily close since mid-June. The decline came after a brief two-day recovery, highlighting the persistent pressure on the pair driven by a strong US Dollar. The Eurozone’s current account surplus of €35.8 billion in June, attributed to reduced imports due to lower energy prices, is juxtaposed against expectations of a slight dip in the August PMI composite index. The Eurozone’s economic concerns are further fueled by a cautious market atmosphere, contrasting the robustness of the US economy. As the US Dollar Index (DXY) surged above 103.50 and US Treasury yields rose, data from the US housing market added to the narrative. Attention now turns to the forthcoming Jackson Hole Symposium, where addresses by Federal Reserve Chair Powell and European Central Bank President Lagarde are eagerly anticipated.

According to technical analysis, the EUR/USD moved lower on Tuesday and managed to reach the lower band of the Bollinger Bands. Currently, the price is slightly above the lower band of the Bollinger Bands. The Relative Strength Index (RSI) currently stands at 39, indicating that the EUR/USD is currently back in a bearish mode.

Resistance: 1.0935, 1.1038

Support: 1.0837, 1.0789

XAU/USD (4 Hours)

XAU/USD‘s Volatile Rally Amidst Dollar’s Rebound and Market Uncertainty

The XAU/USD currency pair experienced a fluctuating rally, surging to $1,904.44 in London trading before reversing due to renewed US Dollar demand, prompted by S&P Global Ratings’ downgrade of US bank ratings following a similar move by Moody’s. Equities maintained a bullish tone as Wall Street and European indexes held onto gains despite retracements from intraday highs, and XAU/USD recovered from its low of $1,889.12. The Dollar’s performance was influenced by rising government bond yields, with the 10-year Treasury note hitting 4.366% and the 2-year note reaching 5.01%. Market unease prevailed ahead of the Jackson Hole Symposium, where speeches by US Federal Reserve Chair Jerome Powell and European Central Bank President Christine Lagarde are anticipated.

Based on technical analysis, the XAU/USD moved higher on Tuesday and was able to reach the upper band of the Bollinger Bands. Currently, the price is moving just below the upper band of the Bollinger Bands. The Relative Strength Index (RSI) is currently at 55, indicating that the XAU/USD pair is now in a neutral stance with a slight bull mode.

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

U.S. stock futures held steady after a month marked by losses across major indices, as the Nasdaq Composite and S&P 500 finally halted their four-day negative streak. Futures tied to the Dow Jones Industrial Average dipped slightly by 0.1%, while S&P 500 and Nasdaq 100 futures also saw marginal declines of the same magnitude. During the main trading session, the Nasdaq Composite posted its most significant gain of the month, surging by 1.6%, and the S&P 500 recorded a nearly 0.7% increase. Impressively, these advances occurred even as the 10-year Treasury yield reached its highest level since November 2007, climbing by around 9 basis points to 4.34%. This simultaneous rise of tech-heavy stocks and yields drew attention in Wall Street, where the historically challenging relationship between tech shares and higher interest rates was defied. Despite the current optimism, analysts remain cautious, highlighting potential vulnerabilities associated with the recent Treasury yield surge, including impacts on refinancing and concerns for tech and growth stocks with high price-to-earnings ratios.

Looking ahead, market watchers await crucial corporate earnings releases from prominent retail giants Lowe’s and Macy’s, as well as Nvidia, a significant tech gainer that plays a pivotal role in gauging sentiment within the AI sector. Economic data releases, such as the Philadelphia Fed’s nonmanufacturing survey, Richmond Fed’s manufacturing survey results, and July’s existing home sales data, will also be scrutinized for insights into the health of the economy. Additionally, all eyes are on Fed Chairman Jerome Powell’s forthcoming remarks at Jackson Hole, expected to provide further clarity on the central bank’s perspective regarding inflation trends. This context underscores the delicate balancing act investors face as they assess the interplay between market performance, interest rates, and economic indicators in the months ahead.

On Monday, the overall market displayed a positive trend with all sectors collectively gaining 0.69%. The Information Technology sector led the way with an impressive surge of 2.26%, followed by Consumer Discretionary at 1.15% and Communication Services at 0.80%. Health Care experienced a marginal uptick of 0.09%, while Materials and Financials saw minimal gains of 0.02% and -0.09% respectively. On the other hand, Industrials and Utilities witnessed slight declines of -0.14% and -0.60%, while Energy, Consumer Staples, and Real Estate faced more substantial decreases, sliding by -0.62%, -0.64%, and -0.88% respectively.

Major Pair Movement

On Monday, the US Dollar faced a slight decline as major currency pairs remained relatively stable due to a lack of significant macroeconomic events. Market sentiment stayed negative, causing government bond yields to rise. The US Treasury yield reached its highest point since 2007, reflecting concerns that global central banks might extend monetary tightening measures to control inflation.

China continued to face challenges, with reports showing a continued decline in government land sales revenue for the 19th consecutive month in July. The People’s Bank of China (PBoC) made a minor expected adjustment by reducing the one-year Loan Prime Rate by 10 basis points to 3.45%. However, this fell short of more aggressive expectations, causing the Yuan to weaken. UBS also lowered China’s 2023 real GDP growth forecast from 5.2% to 4.8%.

The German Bundesbank’s monthly report indicated that inflation might persist above central bank targets for a while, while Q3 growth is predicted to remain largely flat.

Currency pairs displayed varied trends: EUR/USD struggled to surpass 1.0900, GBP/USD appeared better positioned for gains at around 1.2740, the Australian Dollar gained against the US Dollar alongside rising Gold prices, and USD/CAD rose due to decreased oil prices impacting the Canadian Dollar.

USD/JPY traded above 146.00 and near its recent high of 146.53, with growing speculation that the Bank of Japan might need to adjust its ultra-loose monetary policy soon.

The upcoming week’s macroeconomic calendar had limited offerings, with attention turning to the Jackson Hole Symposium starting next Thursday. Federal Reserve Chair Jerome Powell and European Central Bank President Christine Lagarde were scheduled to speak on Friday, raising anticipation for potential hints about future policy decisions.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Holds Near 1.0900 Amid USD Struggles and Chinese Woes

The EUR/USD pair remains steady around 1.0900 as the US Dollar faces challenges despite a sour mood. Asian stocks dip due to ongoing Chinese real estate concerns, while the People’s Bank of China (PBoC) cuts rates as expected, impacting the Yuan. Global bond yields rise, led by the US 10-year Treasury note hitting a 2007 high. Germany sees mixed economic news, with Producer Price Index (PPI) decline but Bundesbank’s caution on inflation. Upcoming data includes Euro Zone’s June Current Account and US July Existing Home Sales and August Richmond Fed Manufacturing Index, alongside insights from Fed officials.

According to technical analysis, the EUR/USD moved higher on Monday and managed to reach the upper band of the Bollinger Bands. Currently, the price is slightly below the upper band of the Bollinger Bands. The Relative Strength Index (RSI) currently stands at 51, indicating that the EUR/USD is currently back in a neutral stance.

Resistance: 1.0935, 1.1038

Support: 1.0865, 1.0789

XAU/USD (4 Hours)

XAU/USDRecovers Briefly as USD Strengthens Amid Economic Uncertainties

Spot Gold hit a low of $1,884.77 on Monday before recovering slightly as XAU/USD responded to reduced US Dollar demand, eventually stabilizing around $1,890. The USD rebounded due to a deteriorating market sentiment, causing US indexes to dip and government bond yields, including the 10-year Treasury note, to surge to their highest levels since 2007, with the 2-year note nearing 5%. Growing concerns about a potential economic setback persist as global central banks remain cautious about ending the ongoing monetary tightening cycle, and worries intensify due to China’s currency struggles and limited action. The macroeconomic calendar offers little this week, heightening anticipation for insights from Federal Reserve Chair Jerome Powell and European Central Bank President Christine Lagarde at the Jackson Hole Symposium on Friday, as investors seek guidance on future directions.

Based on technical analysis, the XAU/USD moved higher on Monday and was able to move near the upper band of the Bollinger Bands. Currently, the price is moving just below the upper band of the Bollinger Bands. The Relative Strength Index (RSI) is currently at 48, indicating that the XAU/USD pair is now in a neutral stance.

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].