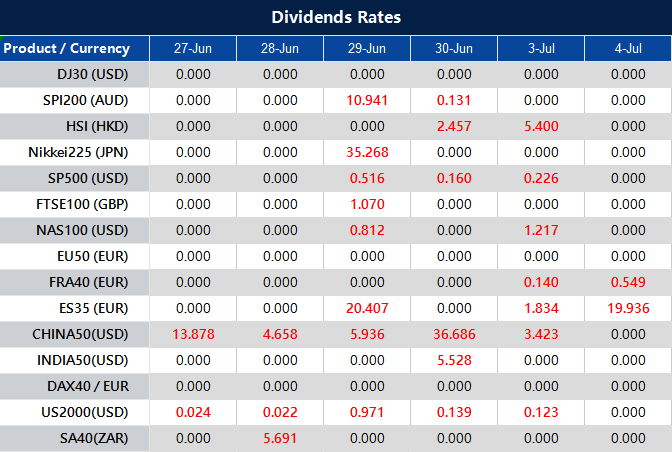

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

In the final week of the first half of the year, the Nasdaq Composite experienced a significant decline as investors sold off shares of technology companies that had performed well so far in 2023. The Nasdaq dropped by 1.16%, while the S&P 500 also saw a loss of 0.45%, and the Dow Jones Industrial Average dipped slightly by 0.04%.

This pullback was primarily driven by a sharp decline in technology giants such as Nvidia, Alphabet, Meta Platforms, and Tesla. Despite the setback, the Nasdaq has still seen a substantial rebound this year, fueled by renewed investor optimism in artificial intelligence and expectations of a slowdown in the Federal Reserve’s interest rate hikes.

While the technology sector experienced a decline, other segments of the market performed well in the first half of the year. The S&P 500 has gained 12.7% and the Dow is up approximately 1.7%. Although the market rally stalled last week, overall, it has been a successful first half for investors.

Traders will keep an eye on the situation in Russia following a brief rebellion by a private military group, which could potentially introduce uncertainty into the markets. Additionally, economic reports for the week are relatively light, with the focus on the personal consumption expenditures index for May and corporate earnings reports from Walgreens Boots Alliance and Nike.

On Monday, the overall market experienced a slight decline of 0.45%. However, some sectors managed to perform well, with the Real Estate sector showing the highest gain at 2.21%, followed by Energy at 1.71% and Materials at 1.00%. Utilities and Industrials also saw positive growth with increases of 0.98% and 0.79% respectively.

On the other hand, several sectors faced declines, including Information Technology leading the losses with a decrease of 1.03%, followed by Consumer Discretionary and Communication Services both experiencing declines of 1.25% and 1.88% respectively. Financials, Health Care, and Consumer Staples also saw slight declines, with decreases of 0.20%, 0.60%, and 0.03% respectively.

Major Pair Movement

GBP/USD remained steady after a day of little change, with the USD weakening slightly. The market anticipates that the Bank of England (BoE) will implement aggressive interest rate hikes, potentially raising rates by 50 basis points. However, relying solely on interest rates to control inflation may not be effective, raising concerns of a looming recession. In June, shop price inflation in the UK slowed down as retailers reduced prices.

The AUD/USD currency pair showed minimal reaction to the turmoil in Russia and remained on the sidelines. The AUD/USD rally was limited by the strengthening of USD/CNH (Chinese yuan) and supported by softer US yields.

EUR/USD initially declined near the 55-day moving average but later turned positive on Monday. The currency pair demonstrated resilience in the face of Russia-related geopolitical risks and disappointing Ifo data, which could strengthen positive technical indicators and contribute to further gains.

Despite potential instability in Europe’s eastern region due to a weekend mutiny, EUR/USD traded higher as investors focused more on a potential pause in the US Federal Reserve’s rate hikes and favourable positioning for long positions.

Market expectations indicate that the Federal Reserve may implement two more rate hikes, but current US rates are factoring in only one additional increase, potentially followed by cuts later in the year. Despite a decrease in euro positions and an increase in dollar positions, EUR/USD managed to rally as investors reduced their overall exposure, suggesting a positive sign for the currency pair.

In the US, the focus is on the forthcoming weekly claims data and May’s Personal Consumption Expenditures (PCE) figures, which will likely influence market dynamics.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Rises as Markets Await Inflation Data and Central Bank Speeches

The EUR/USD pair saw a modest increase on a quiet Monday, with investors eagerly anticipating the release of key inflation data and speeches from central bank officials. The US dollar weakened slightly due to declining yields and a rebound in commodity prices. Germany’s Ifo data showed a decline, raising concerns about the country’s economic health. The European Central Bank’s forum on central banking in Sintra has begun, where ECB President Lagarde and other policymakers will address the audience. Monetary policy expectations will be influenced by the discussions and upcoming inflation data from the Eurozone and the US.

According to technical analysis, the EUR/USD pair exhibited low volatility on Monday, but the Bollinger Bands still have wide bands. Currently, the price is approaching the middle band of the Bollinger Bands from the lower band. The Relative Strength Index (RSI) is currently at 51, suggesting that the EUR/USD has returned to a neutral position.

Resistance: 1.0932, 1.0965

Support: 1.0890, 1.0863

XAU/USD (4 Hours)

XAU/USD Eases from Highs as Investors Await Central Bank Clues and Inflation Updates

Spot gold (XAU/USD) initially surged at the weekly opening but later retraced its gains during the European session. XAU/USD reached a high of $1,933.31 before settling around $1,925 per troy ounce. The US Dollar traded within narrow ranges as investors remained cautious amid central banks’ ongoing battle against inflation. Market participants are closely watching the European Central Bank (ECB) Forum on Central Banking, where ECB President Christine Lagarde is expected to provide opening remarks.

Additionally, upcoming discussions featuring central bank chiefs, including the Federal Reserve’s Jerome Powell, Bank of England’s Andrew Bailey, and Bank of Japan’s Kazuo Ueda, could provide insights into future monetary policy decisions. Inflation updates from Europe and the US are also anticipated, adding to speculations regarding central banks’ actions and their impact on the global economy. While risk sentiment is currently low and global indexes are trading negatively, market movements are limited due to the absence of significant data releases at present.

According to technical analysis, the XAU/USD pair is experiencing low volatility and a tight range on Monday, resulting in narrower movements for the upper and lower bands of the Bollinger Bands. The price is currently moving above the middle band of the Bollinger Bands, indicating the potential for a slight upward movement with the aim of reaching the upper band and our resistance levels. Currently, the Relative Strength Index (RSI) stands at 50, indicating that the XAU/USD is in a neutral position.

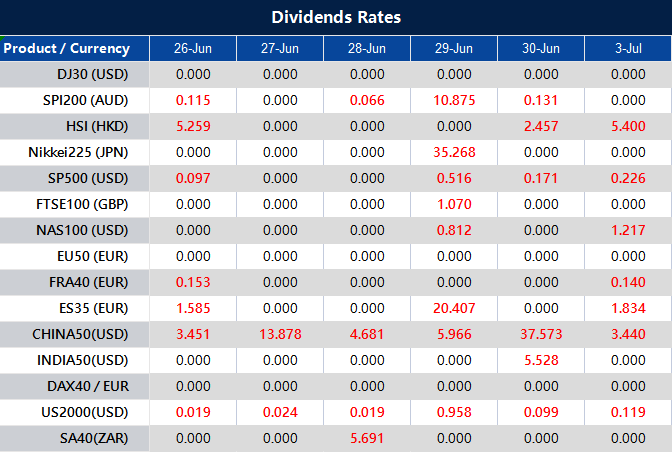

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

This week, market participants prepare for important economic events such as the release of Canada’s Gross Domestic Product (GDP) and Consumer Price Index (CPI), in addition to Australia’s CPI.

Traders are anticipated to keep a close watch on these critical updates to tailor their strategies and acquire valuable knowledge about the financial markets.

Remember to stay updated with a summary of noteworthy developments.

Canada Consumer Price Index (27 June)

Canada’s CPI rose 0.7% in April 2023 compared to March 2023 figures.

Analysts anticipate a 0.5% increase for May data, set to be released on 27 June.

Australia Consumer Price Index (28 June)

Australia’s CPI saw a 6.8% increase in the year leading up to April 2023, a rise from the 6.3% gain observed in the year ending in March 2023 – the lowest in 10 months.

Analysts predict a slower growth of 6.4% for the data covering the year to May 2023, set for release on 28 June.

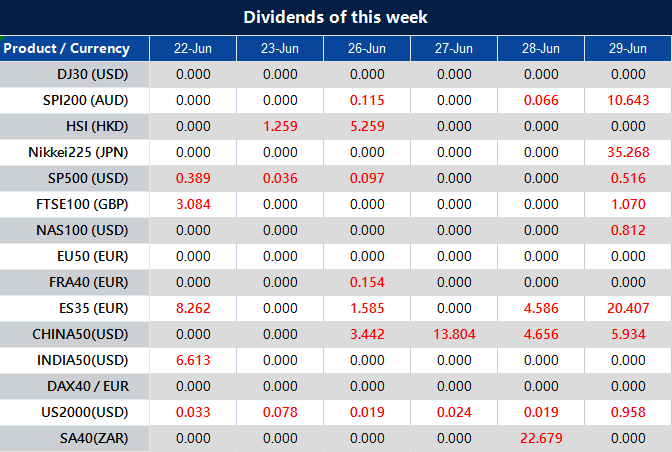

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

The Nasdaq Composite and the S&P 500 ended their three-day losing streaks on Thursday, propelled by renewed investor interest in tech stocks. The Nasdaq, a tech-heavy index, surged by 0.95% to 13,630.61, while the S&P 500 rose 0.37% to 4,381.89, with both indices closing near session highs.

In contrast, the Dow Jones Industrial Average dipped slightly by 0.01% to 33,946.71. The market appeared to be in a state of pause, noted the balance between the bull and bear market sentiments, implying increased volatility and uncertainty ahead.

Investors seized the opportunity to buy major tech stocks that experienced declines earlier in the week. Tesla’s shares, despite being downgraded by a second Wall Street bank, rebounded and closed higher. Amazon’s shares surged by over 4%, Microsoft climbed 1.8%, and Apple reached a new all-time high.

However, concerns loomed in other sectors, as Boeing supplier Spirit AeroSystems saw a significant drop of over 9% due to a halt in production caused by an upcoming worker strike. Additionally, Boeing’s shares fell by over 3%, impacting the Dow’s performance.

Wednesday’s decline in the S&P 500, which marked its worst daily performance in June, was attributed to Federal Reserve Chair Jerome Powell’s statement indicating the likelihood of further interest rate hikes to combat inflation. Powell’s remarks disappointed investors who had hoped the central bank was nearing the end of its tightening cycle.

The Bank of England also raised interest rates by 50 basis points, continuing its streak of consecutive increases. The persistence of central banks worldwide in their inflation-fighting stance, even at the expense of economic growth, contributed to the overall market weakness.

On Thursday, across all sectors, the market experienced a slight increase of 0.37%. Among the specific sectors, Consumer Discretionary showed the highest gain with a growth of 1.53%, followed by Communication Services with a rise of 1.15%, and Information Technology with an increase of 0.92%. Health Care and Consumer Staples also saw modest gains of 0.65% and 0.51%, respectively.

However, Materials and Industrials sectors both suffered declines, with Materials showing a decrease of 0.29% and Industrials experiencing a larger decline of 0.71%. Financials, Utilities, and Energy sectors all had negative performance as well, with declines of 0.74%, 0.76%, and 1.30% respectively. Real Estate had the largest decline among the sectors, with a decrease of 1.44%.

Major Pair Movement

On Thursday, the oversold dollar index initially declined but later rebounded as Treasury yields rose and the Federal Reserve expressed a more hawkish stance, leading to risk-off flows. Despite the Bank of England’s aggressive 50bp rate hike and signs of high UK inflation, the pound struggled to surpass June’s highs, causing traders to take profits. A similar setback occurred in the EUR/USD pair, which failed to make significant progress above 1.10.

Concerns arose that the BoE and ECB were lagging behind in addressing inflation, potentially causing more widespread damage to the UK and eurozone economies compared to the United States. The dollar experienced a brief decline following higher-than-expected initial jobless claims, but this reversed as continued claims came in below forecast and the Fed Chair emphasized gradual rate hikes to manage inflation without severe economic consequences.

EUR/USD ended with a 0.28% loss, and GBP/USD was down 0.25% despite expectations of a 25bp rate hike. The market is monitoring the 10-day moving average as a potential support level for GBP/USD. If the spread between 2-year gilts and Treasury yields remains positive, there may be a pullback in the pound, enticing new buyers. USD/JPY and other yen crosses reached new highs as the yen weakened due to the contrast between the Bank of Japan’s negative rates and the rising rates of other major central banks.

Technical analysis suggests a bullish close above a certain level is imminent. On Friday, market participants will pay attention to Japanese core CPI, UK retail sales, and flash PMI readings as key event risks.

In summary, the dollar index initially declined but later recovered, driven by rising Treasury yields and a hawkish Federal Reserve. The pound and EUR/USD faced setbacks despite aggressive rate hikes, raising concerns about the central banks’ ability to address inflation effectively.

The dollar experienced a temporary dip after initial jobless claims exceeded expectations but rebounded as continued claims were lower than forecasted. The yen weakened against the dollar and other currencies due to the divergence in interest rate policies among major central banks.

Technical indicators point to potential support and bullish momentum in certain currency pairs. Notable event risks on Friday include Japanese core CPI, UK retail sales, and flash PMI readings.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Hits Multi-Month High but Retreats as US Dollar Recovers

The EUR/USD pair reached its highest level in months at 1.1011, but failed to sustain above the 1.1000 mark and corrected to around 1.0950. The US Dollar regained strength, causing the pair to decline. Expectations surrounding the European Central Bank (ECB) were overshadowed by Federal Reserve Chair Powell’s testimony, which hinted at the likelihood of more rate hikes.

Analysts are currently discussing the ECB’s final interest rate decision. Some predict a single hike in July to 3.75%, while others suggest an additional hike in September, raising the rate to 4%. These actions will depend on various factors, primarily the Consumer Price Index.

The upcoming release of the flash Purchasing Managers’ Index (PMI) for June on Friday will hold significance. Projections indicate a potential increase in German Manufacturing PMI to 43.5, while the Service PMI is expected to decline from 57.2 to 56.2. The Eurozone Manufacturing PMI is anticipated to remain at 44.8, with the Service PMI predicted to decrease from 55.1 to 54.5.

On Thursday, US yields rose, providing support to the US Dollar. After three days of decline, the US Dollar Index climbed back above the 102.00 level. Chair Powell reiterated that interest rates are likely to rise in the coming months, with the Federal Reserve’s decision relying on a balance between economic performance and inflation indicators.

Thursday’s data revealed that Initial Jobless Claims reached their highest level since October 2021, but there was a positive note with an increase in Existing Home Sales. The June PMI figures, to be released on Friday, will be closely monitored.

According to technical analysis, theEUR/USD pair experienced a correction move on Thursday and was able to break inside the support and resistance levels and move back to the middle band of the Bollinger Bands. The Relative Strength Index (RSI) is currently at 53, indicating that the EUR/USD is back in a neutral stance for the last day of the week.

Resistance: 1.0965, 1.1003

Support: 1.0920, 1.0890

XAU/USD (4 Hours)

US Dollar Appreciates as XAU/USD Hits Lowest Level in Months

The US Dollar strengthened, causing XAU/USD to reach its lowest point since mid-March. The currency pair, currently trading slightly above the $1,912.78 mark, has declined for four consecutive days. Despite some initial struggles, the USD remained robust, especially after Federal Reserve Chairman Jerome Powell’s testimony on the Semi-Annual Monetary Policy Report before the Senate Banking Committee. Powell indicated that the committee largely supports one or two more rate hikes, while rate cuts are not expected. He acknowledged the persistent nature of inflation but expressed the desire for confidence in its downward trajectory.

Simultaneously, disappointing macroeconomic data in the United States added to concerns and exerted additional pressure on high-yield stocks. Initial Jobless Claims for the week ending June 16 exceeded expectations at 264K, while the Q1 Current Account showed a deficit of $219.3 billion. Additionally, the May Chicago Fed National Activity Index unexpectedly declined to -0.15, and May Existing Home Sales saw a modest 0.2% increase, surpassing the projected -0.6% decrease.

According to technical analysis, the XAU/USD pair is moving lower and created a push to the lower band of the Bollinger Bands. There is potential for a slight upward movement, aiming to reach the middle band. Currently, the Relative Strength Index (RSI) is at 26, indicating that the XAU/USD is in an oversold stance.

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

In a temporary halt to the recent market rally, stocks experienced a decline on Wednesday. Investor sentiment was influenced by Federal Reserve Chair Jerome Powell’s remarks on inflation. The Dow Jones Industrial Average dropped 0.30%, the S&P 500 declined by 0.52%, and the Nasdaq Composite slid 1.21%, marking the third consecutive day of losses for all three indexes.

The pullback was particularly evident among major tech stocks that had seen significant gains due to the hype around artificial intelligence. Amazon shares fell by approximately 0.8% following a lawsuit by the Federal Trade Commission, accusing the company of misleading customers and obstructing cancellation attempts. Nvidia, which witnessed an impressive 200% surge this year, saw a 1.7% decrease. Google-parent Alphabet and Netflix also experienced declines of over 2%.

The decline in stocks was further fueled by disappointing earnings reports. FedEx shares fell over 2% after reporting weaker-than-expected revenue for the last quarter, while Winnebago’s shares dropped nearly 1.3% due to the company’s failure to meet third-quarter revenue estimates.

Investor attention was also drawn to Powell’s statements, where he indicated the likelihood of future interest rate hikes in response to combating inflation. Although the central bank refrained from raising rates after 10 consecutive hikes, Powell mentioned the possibility of two more quarter-percentage-point moves this year. This cautious outlook contributed to the pause in the recent market exuberance, as investors reassessed their positions following the S&P 500’s highest level since April 2022 and its five consecutive positive weeks.

On Wednesday, there were varied price changes across different sectors. The energy sector experienced a positive gain of 0.92%, followed by utilities with a gain of 0.84%, and industrials with a gain of 0.57%. Consumer staples and materials sectors also saw modest gains of 0.39% and 0.35% respectively. Health care had a minimal increase of 0.06%.

However, some sectors experienced losses. The largest decline was observed in the information technology sector, which had a decrease of 1.41%. This was followed by communication services with a decline of 1.35%, and consumer discretionary with a decline of 1.17%. The financials sector also experienced a slight decrease of 0.19%. Real estate had the largest loss among the sectors, with a decline of 0.45%.

Major Pair Movement

On Wednesday, the dollar index experienced a 0.45% decline as Fed Chair Jerome Powell’s testimony and comments indicated uncertainty about the extent of future policy tightening by the U.S. central bank. Powell’s comparison of the gradual tightening to slowing down a car as it approaches its destination worried dollar traders, leading to further losses.

Meanwhile, EUR/USD rose by 0.65%, surpassing previous highs after the Fed and ECB meetings, and approaching the significant psychological barrier of 1.10. The market expects two more rate hikes from the ECB before a prolonged plateau, while only one additional hike from the Fed is anticipated before rate cuts begin next year.

Sterling initially experienced losses but later recovered, returning to a flat position. Concerns about the UK’s inflation, which reached its highest level since 1992 at 7.1% in April, raised worries that the Bank of England (BoE) would need to implement substantial tightening measures, potentially leading to a challenging economic situation.

Market uncertainty regarding the extent of rate hikes by the BoE resulted in a 10-basis point increase in two-year gilts yields. However, expectations remain steady at a total of 150 basis points of hikes and a terminal rate of 6%. The doubts surrounding additional Fed hikes pulled the sterling up from its 10-day moving average support level of 1.2691, edging closer to Tuesday’s highs.

On the other hand, the Bank of Japan (BoJ) maintained its negative policy rate, implemented yield curve control, and engaged in extensive asset purchases. This policy contrast with other central banks, including the Fed, propelled USD/JPY to new highs in 2023 at 142.37.

However, significant resistance at 142.50 prevented further gains. To surpass this resistance, USD/JPY may require support from U.S. jobless claims data on Thursday and Japan’s consumer price index (CPI) release on Friday, reinforcing the bullish divergence between the Fed and BoJ policies.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Surges as Euro Outperforms and US Dollar Weakens amid Fed Chair Powell’s Comments

The EUR/USD pair experienced a surge on Wednesday, reaching its highest level in a month at 1.0989, with the Euro displaying strength while the US Dollar weakened due to lower Treasury yields. Federal Reserve Chair Powell’s comments during his testimony to the House Financial Services Committee provided no surprises.

In contrast, the German IFO Institute warned of a sharper-than-expected German recession, leading to uncertainty about the European Central Bank’s (ECB) future rate hikes. However, ECB members Schnabel and Nagel remained hawkish, suggesting more work needs to be done. Despite UK inflation numbers, the Euro continued to outperform, particularly against the GBP.

Meanwhile, Fed Chair Powell reiterated the FOMC’s message from the recent monetary policy meeting, emphasizing potential rate hikes if the economy performs as anticipated. The US Dollar faced additional pressure as US yields turned negative, pushing the EUR/USD closer to the 1.1000 level. While no significant data from the European Union was expected on Thursday, the US would release Jobless Claims and Existing Home Sales reports. Furthermore, the Bank of England’s decision could potentially impact the markets.

According to technical analysis, theEUR/USD pair experienced a strong movement on Wednesday and able to break our resistance level and create a push to the upper band of the Bollinger Bands. The Relative Strength Index (RSI) is currently at 74, indicating that the EUR/USD is back in a bullish trend which can create another higher movement.

Resistance: 1.1003, 1.1034

Support: 1.0920, 1.0957

XAU/USD (4 Hours)

XAU/USDRecovers from Three-Month Low as US Dollar Loses Momentum on Powell’s Comments

The price of gold (XAU/USD) bounced back from a recent three-month low of $1,919.12 per troy ounce as the US Dollar lost steam following statements made by Federal Reserve Chairman Jerome Powell. Initially, the Greenback had strengthened in anticipation of a hawkish stance from the Fed chief.

However, Powell’s remarks, which echoed the latest Federal Open Market Committee (FOMC) Minutes, indicated that while the US economy was growing at a modest pace and the labour market remained tight, inflation was gradually decreasing, and consumer strength was waning.

This assurance alleviated market concerns, leading to a recovery in stock markets and a decline in the US Dollar against major currencies.

According to technical analysis, the XAU/USD pair is moving lower and has reached the lower band of the Bollinger Bands. There is potential for a slight upward movement, aiming to reach the middle band. Currently, the Relative Strength Index (RSI) is at 38, indicating that the XAU/USD is bearish but still in a neutral stance.

Stocks experienced a decline on Tuesday, marking the first trading day of the week, as the market took a breather after a recent rally that had propelled it to levels not seen in over a year. The Dow Jones Industrial Average fell by 245.25 points (0.72%) to reach 34,053.87, while the S&P 500 and Nasdaq Composite declined by 0.47% and 0.16%, respectively.

Energy stocks, along with Intel, Nike, and Boeing, weighed on the market with notable drops of more than 3%. Conversely, homebuilders, including PulteGroup, D.R. Horton, and Lennar, outperformed following a robust housing report. Nvidia also defied the downward trend, posting a gain of over 2% amidst the broader market decline.

Investors were coming off a strong week, with the S&P 500 and Nasdaq Composite delivering their best weekly performances since March. The S&P 500 rose 2.6% and the Nasdaq gained 3.25%, while both indexes reached their highest levels since April 2022. The market responded favourably to the Federal Reserve’s decision to skip a rate hike in June, although policymakers are projecting two quarter-point increases later in the year.

Despite uncertainties surrounding future Fed policies, investor bullishness has been on the rise, reaching its highest level since November 2021. As economic data remains limited in the current shortened trading week, traders are closely monitoring market sentiment and its potential impact on stock performance.

On Tuesday, the overall market performance showed a decline of 0.47% across all sectors. However, there were a few sectors that experienced positive movement. Consumer Discretionary had a gain of 0.75%, indicating increased consumer spending on non-essential goods.

In contrast, Health Care saw a slight decrease of 0.15%. Communication Services and Information Technology both experienced declines of 0.29% and 0.44% respectively.

Financials had a larger decline of 0.69%, while Consumer Staples and Industrials experienced decreases of 0.75% and 0.76% respectively. Real Estate and Utilities were among the sectors with the largest declines, with decreases of 1.11% and 1.17% respectively.

Materials and Energy had the most significant declines, with decreases of 1.26% and 2.29% respectively, indicating a negative trend in these sectors.

Major Pair Movement

Last week, the US dollar and Japanese yen experienced declines against major currencies, which were corrected this week. The correction came ahead of Federal Reserve Chair Jerome Powell’s upcoming testimony and was driven by factors such as the Fed’s pause in rate hikes, the ECB’s ongoing rate-hiking efforts, and the Bank of Japan’s commitment to maintaining its easing policies.

The euro faced pressure due to a drop in German PPI and the euro zone’s current account surplus. Additionally, the market responded to a significant increase in US housing starts. Meanwhile, the UK pound fell after a sharp surge, and the yen strengthened against the Australian dollar, pound, and euro, influenced by Treasury yields and safe-haven demand.

This week, all eyes are on Powell’s testimony as the market seeks clarity on the Fed’s future monetary policy direction. Market expectations currently suggest only one more rate hike, contrasting with the Fed’s projection of two additional hikes. Meanwhile, the euro is anticipated to see a slower retreat compared to the US dollar, with the market pricing in two more rate hikes by the ECB.

In the UK, there is anticipation around the BoE meeting and the possibility of a rate hike. The market currently prices in a 25 basis point hike, with a chance of a 50 basis point hike. Overall, market dynamics and central bank actions continue to shape currency movements, with investors closely monitoring economic indicators and policy announcements.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Falls as China’s Rate Cut Fails to Calm Markets, US Dollar Gains Momentum

The EUR/USD pair experienced a decline, reaching 1.0891, as market sentiment turned sour, favouring the US Dollar. Concerns about China’s economic health intensified after the local central bank, the People’s Bank of China (PBoC), lowered key interest rates by 10 bps.

However, financial markets remained skeptical of the effectiveness of the rate cuts and sought refuge in the American currency. European Central Bank (ECB) Governing Council member Olli Rehn’s comments on the gradual easing of underlying inflation did not surprise the market, reinforcing the central bank’s previous message.

In addition, disappointing Eurozone data, including the lower-than-expected April Current Account surplus and a decline in Construction Output, contributed to the Euro’s weakness. The US Dollar received a final boost from positive US economic indicators, with Building Permits rising by 5.2% MoM in May and Housing Starts surging 21.7%, surpassing market expectations.

As anticipation builds for Federal Reserve (Fed) Chairman Jerome Powell’s semi-annual testimony before Congress, the US Dollar maintains its strength, with his remarks and subsequent Q&A session expected to influence the markets.

According to technical analysis, theEUR/USD pair experienced a flat movement on Tuesday and created a narrower range for the upper and lower bands of the Bollinger Bands. The Relative Strength Index (RSI) is currently at 56, indicating that the EUR/USD is back in a neutral stance before deciding on the next movement.

Resistance: 1.0963, 1.1034

Support: 1.0892, 1.0803

XAU/USD (4 Hours)

XAU/USDPlummets as US Traders Return Amid Economic Concerns and Positive US Data

The price of gold (XAU/USD) experienced a significant drop as American traders resumed trading after a long weekend, resulting in a decline of approximately $20, reaching a low of $1,929.94 per troy ounce. This decline was influenced by the strengthening US dollar due to worries about China’s economic slowdown. The People’s Bank of China (PBoC) reduced two key lending rates for the first time since August of the previous year, surprising the market with a 10-basis point cut that fell short of expectations.

While the US dollar initially struggled, it gained momentum after the release of optimistic US macroeconomic data, including a remarkable 21.7% surge in Housing Starts and a 5.2% increase in Building Permits for May, as reported by the US Census Bureau.

Although Asian and European stock markets experienced minor losses, Wall Street saw a significant decline, with the three major indexes down by around 1% each. Meanwhile, demand for government bonds kept Treasury yields in check, with the 10-year note currently offering 3.71%, reflecting a 5-basis point decrease on the day.

According to technical analysis, the XAU/USD pair is moving lower and has reached the lower band of the Bollinger Bands. There is potential for a slight upward movement, aiming to reach the middle band. Currently, the Relative Strength Index (RSI) is at 41, indicating that the XAU/USD is still in a neutral stance.

Sydney, Australia, 19 June 2023 – Over a month into the campaign, the King of the Hill Trading Contest, organised by leading online trading platform VT Markets, has been a rousing success thus far. The contest, which began on 1 May 2023, has attracted over 200 participants from 14 countries worldwide, all competing for international recognition and a share of the whopping total prize pool of US$60,000.

Traders across Europe, Southeast Asia, and Greater China are competing to see who can grow the most profits and be the King of the Hill. As of writing, the Southeast Asia competition has the highest profit margins, with the competing traders racking up $7679.51 so far, compared to Europe’s $1249.17 and Greater China’s $3,283.45. Southeast Asia also has the highest profit rates of all the regions. Most profits have been generated through trading XAUUSD, GBPJPY, and BTCUSD, which have been the three most popular trading products at the contest’s halfway mark.

The King of the Hill Trading Contest, which is currently in its second iteration, will run until 31 July 2023, leaving a lot of time left for traders to outwork the competition. VT Markets believes that the competition’s success shows how far the competition has come, and how far it can still go.

“It’s very encouraging to know that this is just the second time we’ve held this contest, and yet, we already have many traders taking on the challenge to be the best,” said a company representative. “At VT Markets, we take a lot of pride in contests like this, which not only offer participants the opportunity to earn substantial rewards but also enable them to showcase their expertise while refining their trading skills on our platform.”

Outside of the cash prize pool, the top performers will also be featured on VT Markets’ Wall of Fame, allowing them to grow their influence and establish themselves among the world’s elite traders. The success of this contest serves as a testament to the growth and potential of the industry, and VT Markets looks forward to witnessing even more exceptional achievements in future competitions.

For more information, visit the relevant King of the Hill Trading Contest page below:

VT Markets is a regulated multi-asset broker with a presence in over 160 countries. Since its inception in 2015, the company has set out to make trading a simple and more accessible experience for everyone. As of today, VT Markets has emerged as one of the world’s top brokers, recently adding a haul of seven awards to its growing list of accolades.

For more information, please visit the official VT Markets website. Alternatively, follow VT Markets on Meta, Instagram, or LinkedIn.

For media enquiries and sponsorship opportunities, please email [email protected]