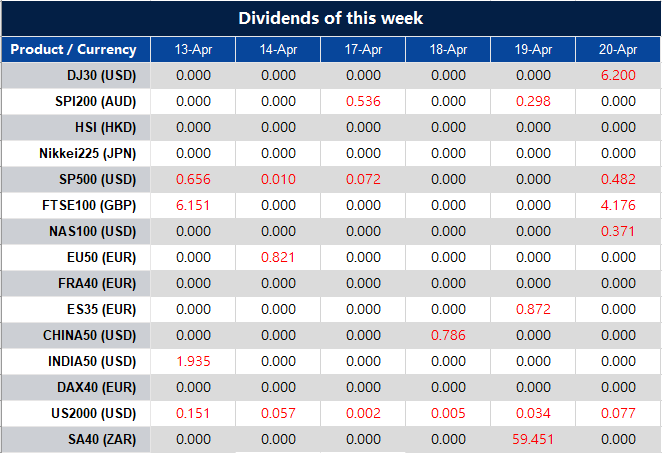

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected]

Stocks on Wall Street declined on Wednesday, despite the release of cooler-than-expected inflation data, due to concerns about a potential recession. The Dow Jones Industrial Average fell by 0.11%, while the S&P 500 and Nasdaq Composite dropped 0.41% and 0.85%, respectively. This came after the Federal Reserve’s March policy meeting minutes showed officials feared a mild recession later this year after the U.S. banking crisis.

Meanwhile, the March consumer price index rose by only 0.1%, compared to the expected 0.2%, suggesting that inflation is beginning to slow. However, the core CPI, which excludes food and energy, rose as anticipated. As companies such as JPMorgan Chase, Wells Fargo, Citigroup, and UnitedHealth begin reporting first-quarter earnings later in the week, the health of the U.S. economy and consumers will be further tested.

data by Bloomberg

On Wednesday, all sectors in the stock market declined by 0.41%, except for Industrials which increased by 0.33%, Energy which increased by 0.11%, and Materials which increased by 0.07%. Health Care increased by only 0.02%, while Utilities decreased by 0.12%, Financials by 0.20%, Real Estate by 0.30%, Consumer Staples by 0.45%, Information Technology by 0.61%, and Communication Services by 0.89%. Consumer Discretionary saw the largest decline, falling by 1.54%.

Major Pair Movement

Data taken from MT4 VT Markets

On Wednesday, the dollar index fell by around 0.6% after the March U.S. CPI came in slightly lower than expected. However, the losses were somewhat contained after Fed speakers reminded the markets that they could still tighten further if core inflation does not proceed sustainably toward their target. The minutes from the Fed’s March meeting showed concern regarding the banking crisis, but inflation remained a top priority.

The EUR/USD rose by 0.74%, nearing February’s one-year highs at 1.1034, as the ECB is expected to hike rates by at least 75bp into year-end, compared to the Fed, which is not fully priced to hike 25bp in May before roughly 50bp of cuts by December. Sterling also rose by 0.5%, nearing April’s 10-month highs at 1.2525, and could continue to climb if upcoming U.S. data favor a more cautious Fed. The USD/JPY fell by 0.42%, but it now needs hawkish U.S. data to get a bullish close above the pivotal 133.77 level.

Technical Analysis

EUR/USD (4 Hours)

The EUR/USD pair reached a psychological resistance level of 1.1000, its highest in more than two months. The US Dollar Index (DXY) dropped to around 101.53 due to market expectations that the Federal Reserve (Fed) will pause its policy tightening. The rise in the major currency pair is due to the US inflation slowing as expected, with headline inflation only increasing by 0.1% and annual inflation easing from 6% to 5%. Core inflation, however, increased from 5.5% to 5.6% due to persistent rent prices.

The Fed believes that US inflation will continue to soften and reach the middle of 3% this year before reaching desired levels in 2024. The market is keenly watching Friday’s US Retail Sales data, which is expected to contract by 0.4%. More rate hikes from the European Central Bank are anticipated due to stubborn inflation caused by a labor shortage and higher oil prices.

From a technical perspective, the EUR/USD price is continuing to rise and create a strong push to the upper band in the Bollinger band. We have adjusted our support level to 1.0962 as the market is expected to break higher today with the release of PPI data which is also an indicator for the US inflation data. The RSI has risen above 50 (at 69), indicating a potential for further upward movement.

Resistance: 1.1026, 1.1052

Support: 1.0962, 1.0921

XAU/USD (4 Hours)

Gold prices initially surged to a high of $2,028.31 per troy ounce after the release of the US Consumer Price Index, which indicated that price pressures continued to recede in March, easing concerns about inflation. However, prices retraced gains and are now hovering around $2,007. The weaker US dollar across the FX market and positive stock market sentiment fueled by modest inflation figures are increasing expectations that the Federal Reserve will hike rates one more time before pausing.

The central bank has adopted a more dovish stance amid a banking crisis that ended up with the collapse of two local banks and dragged alongside Swiss giant Credit Suisse. The inflation figures have somehow let the Fed stay comfortable with a more conservative stance, diminishing the risk of a recession. Investors are not expecting any surprises from the upcoming release of the Federal Open Market Committee Meeting Minutes, which should repeat the dovish tone from Chair Jerome Powell and, if anything, trigger another round of dollar sell-off.

From a technical perspective, the price of XAU/USD continues to rise and reach the upper band of the Bollinger band. The market is currently waiting for the release of the PPI which is also an indicator of the US inflation data. We adjusted our key support level to $2,010. As long as this level is maintained, the XAU/USD uptrend will remain intact. The RSI keeps moving above the 50 levels, indicating that there is potential for gold to continue to rise.

Stock futures were flat in overnight trading on Tuesday as investors turned their attention to the highly anticipated inflation report for March. Dow Jones futures remained unchanged, while S&P 500 and Nasdaq 100 futures slightly increased by 0.04% and 0.07%, respectively.

On Tuesday, the S&P 500 closed with little change, while the Dow Jones Industrial Average gained 0.29% and the Nasdaq Composite lost 0.43%. With Wall Street looking ahead to March’s consumer price index, economists predict that CPI rose by 0.2% in March, which could influence the Federal Reserve’s rate decision in May and result in the cessation of the central bank’s rate-hiking regime.

Investors and traders are keeping an eye on the CPI number, which could cause significant changes in the stock market. Additionally, minutes from the Federal Reserve’s March policy meeting are expected to be released on Wednesday, providing further insight into the central bank’s decision to raise interest rates amid the collapse of Silicon Valley Bank and the turmoil that shook the banking industry. As the first-quarter earnings season begins, investors await reports from JPMorgan Chase, Wells Fargo, Citigroup, and UnitedHealth, which will test the health of the U.S. economy and consumers.

Data by Bloomberg

In the stock market on Tuesday, most sectors remained stable without significant changes. However, the energy sector was the top gainer with an increase of 0.89%, while financials, materials, and industrials followed with gains ranging between 0.59% and 0.85%.

Conversely, the information technology sector experienced the biggest loss with a decline of 1.03%, and communication services also decreased by 0.43%. Consumer discretionary and utilities sectors showed little change, while real estate, health care, and consumer staples sectors had small but positive gains.

Data taken from MT4 VT Markets

Major Pair Movement

The US dollar index fell 0.3%, driven by gains in the EUR/USD and GBP/USD pairs, as the early risk-off sentiment that led to dollar buying retreated despite a rise in Treasury yields. The USD/JPY also rebounded after dropping to 132.97 lows, driven by a rise in Treasury yields earlier in the day. However, a call for policy prudence and patience by Chicago Fed President Austan Goolsbee and IMF’s warning about a “perilous combination of vulnerabilities” in financial markets tempered the Treasury yield rise.

The concerns about the impact of credit tightening on top of monetary tightening remain, as emergency bank borrowing from the Fed remains quite high and bank deposits have only expanded marginally following March’s sharp drop. Wednesday’s US core CPI data will be most relevant, as the expected plunge in the overall year-on-year inflation rate is a function of last March’s post-Ukraine invasion peak in oil versus March’s post-invasion trough. Additionally, the minutes from the Fed’s last meeting will also be released. The ECB and BoE are expected to hike rates at their upcoming meetings, with the BoE having roughly 50bp of hikes by September’s 4.66% implied peak, which still seems weak given the UK’s inflation at 10.4%.

Technical Analysis

EUR/USD (4 Hours)

The EUR/USD bounced back from its weekly low as Europe returned from the Easter holiday, with the pair rising above 1.0900 due to a weaker US Dollar and expectations of another rate hike from the ECB. However, Eurozone Retail Sales data released on Tuesday showed a drop of 0.8% in March, with an annual rate decline of -3%, better than expected. The next crucial report for the region will be Industrial Production on Thursday, with expectations of a 25-basis points rate hike at the May 4 ECB meeting.

Meanwhile, the Federal Reserve is evaluating the potential impact of financial stress on the real economy, and if inflation decreases, interest rates will have to be lowered. The attention is now focused on the release of March’s US Consumer Price Index on Wednesday, with the CPI expected to rise by 0.3% and the Core by 0.4%, followed by the publication of the minutes of the latest FOMC meeting later that day. Despite the rise in US yields, the US Dollar was affected by an improvement in risk sentiment.

From a technical perspective, the EUR/USD price is continuing to rise and has moved above the middle band of the Bollinger band. We have adjusted our support level to 1.0881 as the market is expected to break today with the release of US inflation data. The RSI has risen above 50 (at 57), indicating a potential for further upward movement.

Resistance levels: 1.0935, 1.0968

Support levels: 1.0881, 1.0835

XAU/USD (4 Hours)

Gold is currently struggling to extend its gains beyond the $2,000 threshold after having fallen to $1,981.66 on Monday. This is happening amidst the broader weakness of the US dollar and the better performance of stock markets while looming US inflation figures continue to be a concern. Currently, XAU/USD is trading near its daily high of $2,007.44, as most global indexes trade in the green. The Dow Jones Industrial Average in the United States is up 146 points to trade at its highest level since early January. However, the Nasdaq Composite is down 0.37%.

Market participants are dropping the Greenback ahead of the United States March Consumer Price Index (CPI) which is expected to signal core inflation has ticked higher yearly. A few weeks ago, such an outcome would have triggered speculation of a potentially aggressive rate hike from the Federal Reserve (Fed). However, that is not the case following the banking crisis that unfolded in mid-March in the United States. Following the collapse of two local banks, the central bank has adopted a more conservative stance on monetary tightening, as draining liquidity to tame inflationary pressures has multiple undesired effects.

Meanwhile, concerns about a recession continue to grow due to sluggish macroeconomic data and the unexpected decision by OPEC+ to cut oil output. These factors have fueled a dismal market mood, which seems to be temporarily on pause. However, risk-averse environments hardly benefit the Greenback these days, with Gold making the most of it.

From a technical perspective, the price of XAU/USD continues to rise and has surpassed the $2,000 level, indicating the possibility of a renewed upward trend. The market is currently waiting for the release of US inflation data, causing the Bollinger bands to tighten as the price approaches the upper band. It is crucial to monitor the key support level at $2,000, as a decline below this level may signal a potential reversal. However, as long as this level is maintained, the XAU/USD uptrend will remain intact. The RSI has increased to 59, above the 50 levels, indicating that there is potential for gold to continue to rise.

US stock futures showed little change on Monday night as investors await the release of economic data later in the week. Dow Jones Industrial Average futures increased by 35 points, or 0.1%, while S&P 500 and Nasdaq 100 futures climbed 0.13% and 0.11%, respectively. The market is anticipating the March readings of the consumer price index on Wednesday and the producer price index on Thursday, which could provide further insight into how the Federal Reserve will proceed on its rate-hiking campaign.

In addition to the economic data releases, the US stock market is preparing for another earnings season. Several major US banks, which have not reported earnings since the bank crises in March, are scheduled to release their reports. Investors are particularly interested in the financial institutions’ perspectives on current threats and whether they will make any adjustments in an environment that seems less optimistic than three months ago. Before the market opens, the National Federation of Independent Business will also release the latest results of its small business index, and a few regional Federal Reserve presidents will be speaking on Tuesday.

by Bloomberg

On Monday, most sectors in the market saw a positive price change, with the All Sectors index increasing by 0.10%. Industrials had the highest gain of 0.90%, followed by Energy and Materials with gains of 0.65% and 0.49%, respectively. Real Estate and Consumer Discretionary also had positive gains of 0.49% and 0.43%, respectively.

On the other hand, some sectors saw a decline in prices, with Communication Services having the largest decrease of 0.69%. Information Technology and Utilities also saw a decrease in prices with declines of 0.15% and 0.20%, respectively. Health Care and Consumer Staples had the smallest price changes with a decline of only 0.04% and a decrease of 0.01%, respectively.

Major Pair Movement

Data taken from MT4 VT Markets

The US dollar saw gains on Monday as there was a renewed expectation of a Fed hike following Friday’s solid US jobs report, leading to a flight to safety. Meanwhile, the Japanese yen saw a decline as new BoJ governor Ueda dimmed near-term normalization hopes. Treasury yields and the dollar were supported by Friday’s Fed data showing bank deposits rising for the first time in roughly a month and a New York Fed survey on Monday showing higher inflation expectations and harder credit access.

The market is closely watching the upcoming CPI data on Wednesday and retail sales on Friday as they will be important for the Fed’s May 3 policy announcements. Additionally, the quarterly Senior Loan Officer Opinion Survey, presented to the Fed at that meeting but not publicly released until the following week, will be crucial in understanding the tightening of credit conditions and the impact of monetary tightening. Sterling fell 0.3% while the EUR/USD saw a recovery from Monday’s low but remained down 0.37%. The USD/JPY surged 1.1% as haven dollar gains were augmented by widespread yen selling on dimmed BoJ normalization expectations.

Technical Analysis

EUR/USD (4 Hours)

EUR/USD fell on Monday due to a stronger US dollar following Friday’s NFP report, hitting a week low of 1.0830 before rebounding to 1.0850. Investors are now focusing on Wednesday’s US Consumer Price Index data. US yields climbed, with the 2-year yield back above 4% and the 10-year yield above 3.40%, after the upbeat March jobs report. The European bond market will reopen on Tuesday, and on the same day, the Eurozone will report Retail Sales, which are predicted to decline by 0.8% in March. Market participants are still looking for the ECB to raise interest rates at their next meeting.

From a technical standpoint, the price of EUR/USD has rebounded after reaching the support level at 1.0835 and is now targeting the middle band of the Bollinger bands. The key support level to watch is at 1.0791, as a break below this level could indicate a potential reversal. As long as this level holds, the trend for EUR/USD remains in an uptrend. The RSI has risen to 45 from a lower level, indicating the potential for further upward movement.

Resistance levels: 1.0891, 1.0935

Support levels: 1.0835, 1.0791

XAU/USD (4 Hours)

Gold prices started the week lower, falling to around $1,990 per troy ounce, amid concerns over economic growth and a potential recession in the US after the Nonfarm Payrolls report on Friday. The US dollar benefited from a sour mood and thin market conditions due to the Easter Monday holiday in Europe, while investors await the release of the US Consumer Price Index (CPI) on Wednesday, which is expected to show a YoY inflation rate of 5.2% for March.

From a technical standpoint, the price of XAU/USD has rebounded from Monday’s low of $1,988 and is currently trading at $1,992. This indicates a strong attempt to reach the middle bands of the Bollinger bands from a technical perspective. It is important to keep an eye on the key support level at $1,988, as a break below this level could signal a potential reversal. However, as long as this level holds, the uptrend for XAU/USD remains intact. The RSI has risen to 45 from a lower level, suggesting a potential for further upward movement.

Investors are eyeing key inflation data and the start of the first-quarter earnings season as U.S. equity futures edge up slightly on Sunday evening. Let’s take a closer look at the latest market developments and economic data reports to determine their potential impact on the market.

Futures tied to the S&P 500 rose 0.2%, and Dow Jones Industrial Average futures edged up 62 points or 0.2%, while Nasdaq 100 futures remained flat. The market’s performance last week was volatile, with the Dow being the only index to post a weekly gain of 0.6%. On the other hand, the S&P 500 and Nasdaq Composite ended lower by 0.1% and 1.1%, respectively.

The March jobs report released on Friday showed that the nonfarm payrolls grew by 236,000 for the month, slightly lower than the Dow Jones estimate of 238,000. The unemployment rate also fell to 3.5%, as expected. However, the data revealed a weakening labor market and the potential of a slow-moving recession unfolding in the U.S. The latest economic data has not resolved the inflation concerns. As such, the odds of another quarter-point rate hike in May should increase as the data does not appear to justify a Fed pause.

Investors can expect a busy week ahead with a flurry of economic data and the start of the first-quarter earnings season. The latest consumer price index and producer price index data will be key in determining if or when the Fed will pause or put an end to its rate-hiking campaign. The first batch of companies reporting their first-quarter financial results will also be released, with Tilray Brands kicking things off on Monday, followed by the major banks – JPMorgan Chase, Wells Fargo, and Citigroup – reporting on Friday.

Today’s Early Market Pair Movement

The US dollar index remained stable at 102.06 on Monday morning.

The EUR/USD currency pair was unchanged at 1.0917.

The GBP/USD currency pair stabilized at 1.2439 after experiencing a three-session fall.

USD/JPY remained at elevated levels above 132.00.

AUD/USD continued to lack upward momentum, trading at 0.6672.

USD/CHF remained subdued at 0.9043.

USD/CAD continued its recent rebound and traded at 1.3505 after Canada’s jobless rate remained steady at 5.0% in March, versus the expected 5.2%.

Bitcoin rebounded and traded above $28,300.

Technical Analysis

EUR/USD (4 Hours)

The EUR/USD pair retreats from its intraday high to 1.0900, although the bulls remain defensive as they look for fresh clues to continue the four-week uptrend in early Monday trading. The pair is reflecting the holiday mood of Easter Monday, as well as anxiety ahead of the top-tier data/events this week. The optimism in the options market for the EUR/USD prices is due to fears surrounding the reserve currency status of the US dollar and relatively more hawkish comments from the European Central Bank (ECB) compared to the Federal Reserve (Fed).

Although the Easter Monday holiday may limit the movements of EUR/USD, the US Consumer Price Index (CPI) data, and the latest Federal Open Market Committee (FOMC) Monetary Policy Meeting Minutes will be crucial in providing clear directions for the pair.

From a technical perspective, the current movement of EUR/USD is at 1.0901, which is below the middle band in the Bollinger Band. This suggests there is still a possibility of the EUR/USD moving lower. Additionally, the RSI indicator is at 49, just below the mid-level, which also supports the potential for a lower movement. However, since there is a bank holiday in the EU today, we can expect that there won’t be much movement in the EUR/USD.

XAU/USD (4 Hours)

The price of gold (XAU/USD) initially saw a sharp decline at the opening but managed to recover due to responsive buyers at lower levels. It fell below the psychological support level of $2,000.00 as the chances for another 25-basis point rate hike increased significantly. However, it managed to climb back above the $2,000.00 resistance level. The CME Fedwatch tool shows a sudden increase in the likelihood of a 25-basis point rate hike by more than 65%.

The rock-bottom unemployment rate in the US economy has raised expectations of a consecutive 25 basis point rate hike by the Federal Reserve (Fed). The jobless rate was reported at 3.5% on Friday, which was lower than expected than the previous release of 3.6%. The US Nonfarm Payrolls (NFP) data remained subdued, with the US economy adding slightly fewer jobs in March at 236k than the consensus of 240k.

From a technical perspective, Gold experienced a decline after a strong US jobs report on Friday, which is a typical reaction. Currently, Gold is trading at $1,998, breaking below the $2,000 barrier. Today, some bank holidays may affect the movement of Gold. However, it is expected that Gold will rise today as investors may turn to Gold while waiting for tomorrow’s US inflation data.

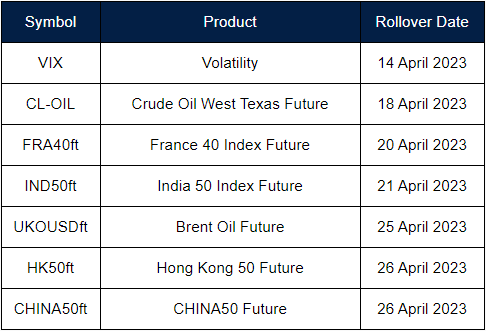

New contracts will automatically be rolled over as follows:

Please note:

• The rollover will be automatic, and any existing open positions will remain open.

• Positions that are open on the expiration date will be adjusted via a rollover charge or credit to reflect the price difference between the expiring and new contracts.

• To avoid CFD rollovers, clients can choose to close any open CFD positions prior to the expiration date.

• Please ensure that all take-profit and stop-loss settings are adjusted before the rollover occurs.

• All internal transfers for accounts under the same name will be prohibited during the first and last 30 minutes of the trading hours on the rollover dates.

If you’d like more information, please don’t hesitate to contact [email protected].

As we begin a new week, the financial world is buzzing with anticipation of some economic reports. All eyes will be on the Bank of Canada Rate Statement and FOMC Meeting Minutes, alongside the eagerly awaited CPI, PPI and Retail Sales data release in the US. These reports are crucial for traders navigating the markets and making informed decisions.

Here are key events to watch out for:

Consumer Price Index (CPI) | US (April 12)

The CPI in the US rose 0.4% month-on-month in February 2023, after rising 0.5% in January.

For March, analysts expect the reading to increase by 0.3%

Bank of Canada Rate Statement | (April 12)

As previously signalled, the Bank of Canada kept its overnight rate target steady at 4.5% during its March 2023 meeting.

The central bank stated that it intends to maintain the current rate if the economic conditions align with the latest Monetary Policy Report’s expectations.

FOMC Meeting Minutes | US (April 13)

The Fed raised the fed funds rate by 25bps to 4.75%-5% in March 2023, matching the February increase, and pushing borrowing costs to new highs since 2007, as inflation remains elevated.

The decision came in line with expectations from most investors, although some believed the central bank should pause the tightening cycle to shore up financial stability.

Employment Change | Australia (April 13)

Employment in Australia created an additional 64,600 jobs to reach 13.83 million in February 2023, surpassing market predictions of 48,500, following a downward revision of 10,900 jobs in the previous month.

Analysts expect employment will add 20,000 jobs in March 2023.

Gross Domestic Product (GDP) | UK (April 13)

The British economy expanded 0.3% month-on-month in January 2023, partially bouncing back from a 0.5% contraction in December when strikes halted business activities.

For February 2023, analysts expect the UK GDP to expand further by 0.2%.

Producer Price Index (PPI) | US (April 13)

Producer prices for final demand in the US fell 0.1% month-on-month in February 2023.

For March, analysts expect the US PPI to go up by 0.1%.

Retail Sales | US (April 14)

Retail sales in the US were down 0.4% month-on-month in February 2023, following an upwardly revised 3.2% surge in January.

For March 2023, analysts expect US Retail Sales to contract by 0.4%.

Prelim University of Michigan Consumer Sentiment (April 14)

The University of Michigan revised the US consumer sentiment downwards to 62 in March 2023 from the preliminary figure of 67. This marks the first decrease in sentiment in four months, as consumers anticipate an upcoming recession.

For April 2023, analysts the data to stand at 62.7.

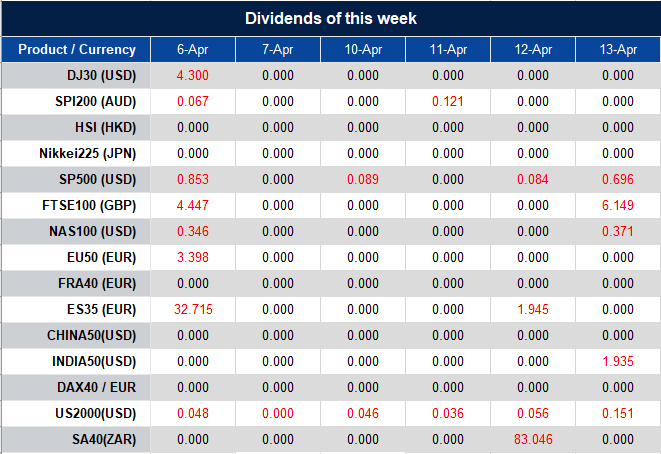

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected]