Consumer Price Index for September expected to show a rise in US inflation

The US Consumer Price Index (CPI) is expected to increase by 3.1% year-on-year (YoY) in September, up from August’s 2.9% rise. The Federal Reserve is likely to lower the monetary policy rate by 25 basis points next week.

The Bureau of Labor Statistics will publish the CPI data for September on Friday at 12:30 GMT, which could affect the US Dollar’s value. The CPI and core CPI are projected to increase monthly by 0.4% and 0.3%, respectively.

HSBC Manufacturing PMI in India increases to 58.4 from 57.7

Germany’s Composite PMI

Germany’s Composite PMI for October is 53.8, reflecting steady progress. Meanwhile, the Indian Rupee remains stable against the USD, with the USD/INR rate holding firm. Several market forecasts highlight that USD/CAD is expected to rise above 1.4000 and GBP/JPY is nearing 204.00. Additionally, Eurozone PMIs are on the horizon, with EUR/USD hovering close to recent lows. Looking ahead, various brokers are pitching valuable insights for trading in 2025, especially focusing on trading the EUR/USD for cost-conscious traders. FXStreet offers helpful resources for traders, including tools, broker comparisons, and market analysis. They caution that market investments come with risks, emphasizing that each trader is responsible for their investment decisions. India’s manufacturing sector is thriving, as the HSBC Manufacturing PMI for October increased to 58.4. This is a notable jump from 57.7 last month. Recent government data from September also shows industrial production grew by 6.2%, reinforcing the positive trend in the economy.Federal Reserve’s Stance

This trend suggests continuing strength for the Indian rupee. We should explore strategies that benefit from a stable or appreciating INR against the US dollar. Options include selling USD/INR futures or buying rupee call options. The Reserve Bank of India maintains healthy forex reserves above $650 billion, which cushions against volatility. The good news isn’t limited to India. Germany’s composite PMI rose sharply to 53.8, surpassing expectations. This unexpected strength might indicate a turning point for the Eurozone economy, which had shown signs of slowing. Derivative traders should watch for a potential euro rally, possibly positioning through long EUR/USD call spreads to take advantage of this momentum. However, we need to remain cautious with upcoming US inflation data. September’s core CPI was unexpectedly high at 3.9%, making the market nervous about another high reading that could push the Federal Reserve to take a more aggressive stance. This raises the risk of holding long positions in other currencies against the dollar until we have more clarity on US inflation. We can compare this situation to market dynamics in 2022, when strong global growth signs were often overshadowed by persistent US inflation worries. While there are plenty of opportunities in emerging markets and Europe, managing risk around major US data releases will be crucial. We can use VIX options to hedge against potential market volatility spikes following the CPI announcement. Create your live VT Markets account and start trading now.In August, Japan’s Coincident Index fell from 113.4 to 112.8.

US CPI is expected to increase by 3.1% in September, with data released on Friday at 12:30 GMT. Markets are closely watching for any effects of President Donald Trump’s tariffs on prices, which could affect the US Dollar and the Federal Reserve’s interest rate choices for the year.

Japan’s coincident index dropped from 113.4 to 112.8 in August. In contrast, Germany’s HCOB Composite PMI unexpectedly rose to 53.8 in October, suggesting a positive outlook for the Eurozone economy.

Currency and Commodity Movements

The GBP/USD pair climbed above 1.3300 after a strong UK Retail Sales report, while the USD/CAD traded above 1.4000, indicating possible buying opportunities. In commodities, Gold prices are under pressure as trade discussions and CPI data approach, currently hovering around $4,100 after rebounding from $4,160. The financial environment is closely monitoring economic indicators like inflation and trade, which significantly affect market sentiment and currency movements in the short term. We are paying close attention to the upcoming US Consumer Price Index data, reminiscent of past concerns over trade tariffs. The market is currently expecting a September year-over-year inflation rate of 2.8%, a slight drop from August’s 2.9%, but still above the Federal Reserve’s goal. This means that options related to the US Dollar are sensitive to any surprises in the data, directly affecting the Fed’s “higher for longer” interest rate stance.Market and Economic Divergence

The economic gap between Europe and the US seems more apparent now than it was in the late 2010s. In the past, we saw German PMIs rising, but recent data showed the HCOB Composite PMI for Germany at a contractionary 49.5, pointing to ongoing energy and industrial challenges. This situation supports strategies favoring the dollar over the euro, with traders looking to sell during any short-term rallies in the EUR/USD pair. Previously, the GBP/USD traded above 1.3300 due to strong data, but now the situation has reversed, with the pair struggling to maintain 1.2200. Recent reports indicate UK retail sales fell by 1.5% year-over-year, negatively impacting the pound. Meanwhile, USD/CAD is steadier around 1.3700, showing less volatility compared to the previous 1.4000 levels, thanks to stable oil prices supporting the Canadian dollar. Gold continues to be a focal point, though its trading range has shifted significantly higher over the years. Once consolidating around $4,100, gold recently achieved an all-time high of $4,250 last month but has settled near $4,210. Traders should consider using derivatives to guard against downside risk if the upcoming CPI data is cooler than expected, as this may decrease gold’s appeal as a hedge against inflation. Create your live VT Markets account and start trading now.In September, Singapore’s industrial output increased by 26.3%, exceeding the expected 8.6% rise.

In September, Singapore’s industrial production soared by 26.3% compared to the previous month, far surpassing the expected 8.6%. This indicates strong growth in the manufacturing sector during this time.

In the UK, retail sales surprisingly increased by 0.5% in September, while a decline of 0.2% was anticipated. This positive news has boosted the Pound Sterling, leading investors to shift their attention to upcoming PMI and US CPI reports.

Currency Trends

The USD/INR dropped, as the Indian Rupee remained strong despite a slowdown in India’s flash PMI growth. On the other hand, USD/CAD rose above 1.4000, driven by a positive market trend. Gold prices experienced fluctuations, hovering around $4,100 early on Friday, influenced by geopolitical tensions. The rising US Dollar and Treasury yields played a role in this volatility. Chainlink’s price stayed above $17 after a 2% recovery, helped by the buyback of 63,481 LINK tokens. However, retail interest in Chainlink remains low, affecting its position in the market. In Japan, the appointment of Sanae Takaichi as Prime Minister has also shaped perceptions of the Yen.Singapore’s Economic Surge

Last month, Singapore’s industrial production report for September was a significant surprise, showing 26.3% growth. This figure far exceeded the forecast of 8.6%, indicating a remarkable boost in the manufacturing sector. It suggests that the regional economy is performing better than expected. This strong performance is not an isolated incident. Advance GDP estimates for Q3 revealed a growth rate of 3.5%, which was also above forecasts. The Monetary Authority of Singapore (MAS) recognized this in its October policy review, keeping a tightening stance on currency, which is beneficial for the Singapore Dollar. The Singapore Dollar has strengthened recently, moving from around 1.38 to 1.35 against the US Dollar. Traders might want to consider buying call options on the SGD to benefit from further gains while limiting potential losses if the trend changes. This economic strength is also a positive sign for Singaporean stocks, particularly in the electronics and manufacturing sectors. Investing in Straits Times Index (STI) futures or call options could be an effective way to take advantage of this economic performance. Strong domestic data, along with a recovering global semiconductor cycle as seen in 2024, typically leads to a rally in the index. The impacts extend to commodities, as Singapore’s status as a major trading hub implies higher demand for energy and industrial metals. Still, the main concern lies with global factors, particularly the upcoming US inflation data. If the US CPI is higher than expected, it could strengthen the US Dollar globally and reduce the regional economic strength. Create your live VT Markets account and start trading now.Japan’s Leading Economic Index falls to 107 in August, missing expectations of 107.4

Japan’s leading economic index for August is at 107, which is below the expected 107.4. This indicates a drop in the country’s economic outlook.

The Indian Rupee is holding steady despite slower growth in India’s flash PMI. Meanwhile, the USD/CAD has gone over 1.4000, signaling a possible bullish trend.

GBP and Euro Market Trends

The GBP/JPY pair is rising and nearing 204.00, boosted by strong UK retail sales data. In contrast, EUR/USD is lingering near recent lows as the market waits for Eurozone PMI updates. Gold prices have dropped and are now around $4,100, mainly due to a stronger US Dollar. This trend is affected by US Treasury yields and ongoing geopolitical issues. Chainlink is maintaining a price above $17, having recovered by 2% after a token buyback. However, low retail interest indicates a bearish trend for this digital currency. Sanae Takaichi’s appointment as Prime Minister of Japan impacts the stability of the Japanese Yen. The market is considering the potential risks related to Japan’s fiscal and monetary policies.Japanese Economic Indicators

There are ongoing signs of weakness in the Japanese economy. This trend has been evident, especially with last year’s disappointing Leading Economic Index. Recently, Japan’s Q3 2025 GDP data showed a slight contraction, and the latest Tankan survey indicates that manufacturers are feeling negative about future prospects. This struggle for growth puts pressure on the yen, making it attractive to take short positions through JPY futures or currency ETF put options. The US Dollar continues to lead in currency markets, a trend that started during the inflationary period of 2024. Recent US CPI data for September 2025 came in high at 3.5%, increasing expectations for another Federal Reserve rate hike this year. Consequently, US 10-year Treasury yields are around 4.8%, attracting investment toward dollar-denominated assets. This situation suggests that trading volatility could be the best strategy in the upcoming weeks. Sharp movements are expected around the upcoming US inflation and job reports, creating opportunities for those positioned well. Consider using options straddles on major pairs like EUR/USD or buying VIX call options to benefit from a surge in market uncertainty. Across the ocean, the Eurozone appears delicate, with Germany’s latest October 2025 flash manufacturing PMI remaining below 50 at 44.2. Although the UK faces its own issues, the Bank of England’s tougher approach to inflation is providing some support for the Pound Sterling. This divergence makes long GBP/JPY or long GBP/EUR positions attractive through currency options or futures. Gold is particularly affected by the strong dollar and the high-interest rate environment. While we recall when prices were peaking, the high yields now make holding non-yielding assets like gold costly. Additional signs of persistent US inflation could push gold prices down further, making put options or short futures feasible strategies in the weeks ahead. Create your live VT Markets account and start trading now.Gold prices in the Philippines have decreased today according to compiled market data.

History and Importance of Gold

Gold has a long history as a store of value and a way to exchange goods. It is often seen as a safe haven, especially during tough times, and it protects against inflation and currency loss. Central banks are the biggest holders of gold. In 2022, they bought 1,136 tonnes, worth about $70 billion. This was the highest amount ever purchased in a single year. Countries like China, India, and Turkey are boosting their gold reserves. Gold prices usually move in the opposite direction of the US Dollar and Treasury yields. When the Dollar weakens, gold prices typically go up. Instability in global politics and fears of a recession can also drive gold prices higher since many view it as a safe investment. Additionally, interest rates affect gold’s value; higher rates generally lead to lower prices. Recent dips in local gold prices are minor compared to the bigger global picture. We consider this a short-term pause. Gold’s importance as a hedge against currency loss and market instability is becoming even more significant, especially given the geopolitical challenges we face in late 2025.Impact of Economic Factors

Increased tensions in the South China Sea over the last month have boosted demand for safe-haven assets like gold. Historically, such geopolitical instability results in more investment in gold. We are preparing for the potential of further escalation, which would likely push prices higher. The most significant factor for us right now is the recent change in US economic data. A weak jobs report from early October 2025, along with new inflation figures showing a drop to 2.8%, has led the Federal Reserve to indicate a halt on further rate increases. This shift towards a more cautious approach is positive for a non-yielding asset like gold. Create your live VT Markets account and start trading now.Singapore’s industrial production exceeds expectations with 16.1% growth compared to 0.5%

US headline inflation is expected to increase by 3.1% year-on-year in September. Meanwhile, Singapore’s industrial production surged by 16.1% in the same month, far exceeding the forecast of 0.5%.

In currency markets, NZD/USD is stabilizing at around 0.5750 as traders remain cautious before the US CPI data release. The AUD/JPY is performing well above 99.50, though the Australian dollar is under pressure. Gold prices are falling ahead of trade talks and the US inflation data. The EUR/GBP is steady at about 0.8700 as UK retail sales updates come in, while crude oil prices are showing a bearish trend in Europe.

Market Dynamics and Sentiments

The EUR/USD is feeling the pressure close to 1.1600 due to a stronger US Dollar. The GBP/USD has risen above 1.3300 after a 0.5% increase in UK retail sales for September. Gold is hovering near $4,100, affected by geopolitical tensions influencing oil prices. Chainlink is holding steady above $17 after a 2% recovery, but it faces bearish sentiment due to low retail interest. Looking ahead to 2025, several brokers stand out for their low spreads and Islamic accounts. Please remember this information is for informational purposes only and may involve risks. Readers are encouraged to review FXStreet’s terms and conditions for more details. With US inflation for September projected at 3.1%, we expect the US dollar to stay strong. This figure is still significantly above the Federal Reserve’s target of 2%, so we don’t anticipate any interest rate cuts soon. Futures markets support this view, showing no cuts until at least mid-2026. Traders should be careful about betting against the dollar, as a higher-than-expected inflation figure could lead to a swift rally. The market is tense ahead of this data, often signaling that volatility is underestimated. We see this cautiousness in the New Zealand dollar, which is nervously lingering around 0.5750 against the US dollar. Using options strategies, like straddles on major currency pairs, might be a profitable way to take advantage of potential price swings once the inflation results are out.Gold and Currency Trends

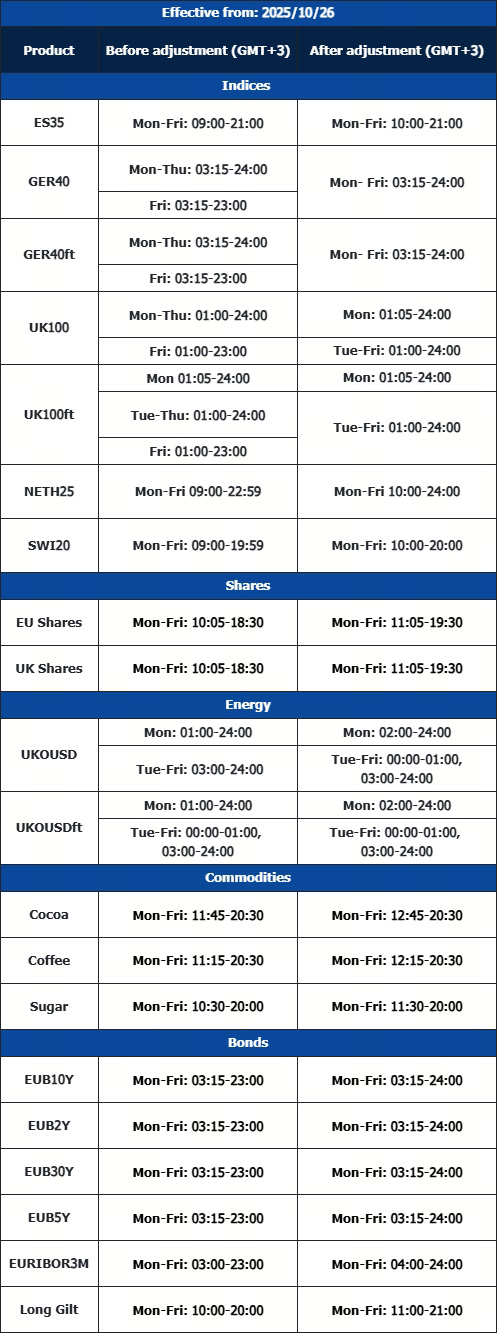

Gold’s price, remaining near $4,100, reflects significant market uncertainty, especially since the geopolitical events of early 2025. This recent drop seems to be a temporary profit-taking move ahead of the inflation data, as higher interest rates generally make non-yielding gold less appealing. However, if the inflation data comes in lower than expected, we could see a strong rebound in gold prices as the dollar weakens. The British pound is showing unexpected strength, rising above 1.3300 against the dollar due to better-than-expected retail sales. This is in stark contrast with the euro, which remains weak near 1.1600, highlighting a clear divide between the UK and Eurozone economies. This trend, observed for much of 2025, could make shorting the EUR/GBP pair an attractive opportunity. While US data is in focus, we must also acknowledge Singapore’s impressive 16.1% increase in industrial production. This signals robust demand in Asia, particularly for electronics and high-tech goods, serving as a counterpoint to the bearish outlook in oil prices. Therefore, while the US dollar might be strong globally, currencies linked to Asian growth, like the Singapore dollar, may perform favorably against commodity-exporting currencies. Create your live VT Markets account and start trading now.Notification of Trading Adjustment – Oct 24 ,2025

Dear Client,

The trading hours of some MT4/MT5 products will change due to the upcoming Daylight-Saving Time change in EU/UK.

Please refer to the table below outlining the affected instruments:

The above information is provided for reference only; please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected]

China’s state planner announces plans for major investment projects and improved government investment structure

China’s National Development and Reform Commission (NDRC) plans to start important investment projects and improve government investment structures. The focus will be on increasing domestic demand and allocating more resources to enhance people’s living conditions, while also reducing local market protectionism.

The AUD/USD pair has fallen by 0.04%, currently trading at 0.6510. The Australian Dollar’s value is influenced by interest rates from the Reserve Bank of Australia (RBA), iron ore prices, and the economic status of China, which is Australia’s largest trading partner.

China’s Demand Impact

The RBA affects the AUD by changing interest rates to keep inflation steady at 2-3%. High interest rates boost the AUD, while low rates usually weaken it. China’s demand for Australian exports plays a significant role in the AUD’s strength. A strong Chinese economy increases demand for Australian currency. Iron ore, worth $118 billion and Australia’s top export, influences the AUD’s value; it rises with higher iron ore prices and falls with lower prices. Australia’s Trade Balance also impacts the AUD. A positive Trade Balance, where exports exceed imports, usually strengthens the currency by increasing foreign demand. China’s plan to enhance government investment sends a strong signal for the upcoming weeks. This indicates a likely increase in demand for industrial commodities, which supports a brighter outlook for the Australian dollar.Iron Ore Prices Impact

This announcement follows recent reports showing China’s Caixin Manufacturing PMI fell to 49.5 in September 2025. The stimulus is a response to this decline and lower-than-expected Q3 GDP growth. The current AUD/USD level of about 0.6510 may not fully reflect the potential effects of this spending. Australia’s economy heavily depends on iron ore, its main export to China. With prices for 62% Fe iron ore around $105 per tonne, the planned infrastructure spending is expected to boost demand. Traders in derivatives might consider taking long positions in iron ore futures, anticipating a price recovery from this renewed demand. We can recall the significant commodity booms that followed China’s major stimulus plans after the 2008 financial crisis and during the 2021 recovery. Both times, there were substantial increases in the prices of iron ore and the AUD. This new announcement suggests a similar, albeit smaller, trend might emerge. With the Reserve Bank of Australia keeping interest rates steady amid ongoing inflation, the AUD is in a strong position. Purchasing AUD/USD call options that expire in the next few months could be a good strategy to capitalize on potential gains, allowing traders to benefit from a price rally while minimizing risk. Create your live VT Markets account and start trading now.WTI oil trades near $61.00 after three days of increases, affected by supply issues

WTI Oil prices have dropped to about $61 per barrel after three days of rising but are still on track for a weekly gain. This decline is happening because the US has imposed sanctions on Russian oil companies Rosneft and Lukoil, which supply nearly half of Russia’s oil exports and over 5% of the world’s oil.

Chinese oil companies have stopped buying Russian oil shipped by sea, and Indian refineries plan to cut back on imports due to the new sanctions. The European Union has also strengthened sanctions aimed at Russia’s energy sector, while Ukrainian forces continue attacks on refineries and pipelines. Despite all of this, Russia remains a significant player in the global oil market.