US equities face pressure from tech earnings and the Fed amid Microsoft’s decline and decreasing enthusiasm for AI.

US stocks faced pressure on Thursday. The S&P 500 declined by 0.7%, the Nasdaq dropped 1.6%, and the Dow fell 0.2%. Cryptocurrencies also took a hit, falling over 4% and hitting near two-month lows. Microsoft’s shares fell 11%, their lowest since early 2020, due to slower cloud growth.

The tech sector struggled, raising concerns over increasing costs in artificial intelligence (AI) that could alter existing business models. ServiceNow’s stock fell even though it exceeded earnings expectations, and both Oracle and Salesforce experienced declines. The IGV ETF, focused on software, entered a bear market, down over 20% from its peak as sentiment shifted away from AI optimism. While AI continues to drive growth, the quality of earnings and diversification matters more now as valuations face pressures.

Microsoft’s earnings drop leads to a $400 billion market loss, impacting other indices negatively.

Microsoft faced a significant drop in its stock price after releasing its earnings report, falling 12% in Thursday’s trading session. This decline wiped out $400 billion in market value, the second-largest one-day loss in U.S. history. Investors are worried about Microsoft’s increasing capital expenses, which are expected to rise by 66% by 2026 for data center expansions.

The NASDAQ 100 index reacted by declining over 1%, while the broader NASDAQ Composite fell by 1.6%. The S&P 500 and Dow Jones dropped 0.6% and 0.2%, respectively. Bitcoin also fell, dropping over 6% to $83,600. Although Microsoft reported strong financial results, including an adjusted EPS of $4.14 and revenue that exceeded expectations, analysts still expressed concerns.

OpenAI Funding Concerns

OpenAI’s funding issues are adding to the worries about Microsoft’s future, as almost half of its Remaining Performance Obligations are connected to OpenAI. This has created unease, despite ongoing discussions about a $60 billion investment from Microsoft, Amazon, and Nvidia into OpenAI. Other software companies like ServiceNow, HubSpot, and SAP also experienced sell-offs amid this market anxiety. The significant drop in Microsoft’s stock has raised fear and volatility in the market. The implied volatility for NASDAQ 100 options, indicated by the VXN index, jumped over 25% yesterday, reaching its highest level since the uncertainty seen in October 2025. This increased volatility may present new opportunities for options traders. For traders expecting further declines, technical analysis suggests that the stock may fill its chart gap from May 2025, targeting a price near $396. A simple bearish strategy could involve buying February or March put options to take advantage of this potential move, providing defined risk while exposing traders to possible further declines due to spending concerns. Consumer Price Index Influence The current market anxiety is also influenced by last week’s Consumer Price Index report, which showed inflation at 3.2%, slightly above expectations. This has led to doubts about the Federal Reserve quickly lowering interest rates. This concern was evident in the options market, where put volume on Microsoft reached over 2.5 million contracts, a 500% increase compared to its recent daily average. Conversely, the stock’s Relative Strength Index is now at 31, suggesting it is nearing oversold territory. Traders who see this as a typical overreaction might consider selling cash-secured puts with a strike price below $390. This approach allows for collecting premium and profiting if the stock stabilizes or rebounds. We’ve seen this trend before, like when Meta Platforms dropped sharply in early 2022 due to worries about its metaverse spending. That situation turned into a long-term buying opportunity, but the stock remained pressured for several months before bouncing back. Microsoft’s drop is already impacting other software companies, indicating that investors are broadly reassessing high-growth tech valuations. In light of the uncertainty, traders expecting continued volatility but unsure of the direction could consider volatility strategies. A long straddle, which involves buying both a call and a put option at the same strike price and expiration, could be beneficial. This strategy profits if the stock makes a significant move—either up or down—larger than the total premium paid. Create your live VT Markets account and start trading now.Markets saw volatility as Trump urged the Fed to quickly cut interest rates on social media.

On Thursday, financial markets were quite volatile during US trading hours, mainly due to comments from President Donald Trump. Trump criticized Federal Reserve Chairman Jerome Powell for not cutting interest rates and argued that the US should have the lowest rates in the world. In response, Powell pointed out that US job gains and unemployment are stable, even with inflation slightly higher than normal.

Wall Street saw a decline, especially in the tech sector. Microsoft Corp. shares hit a six-year low after reporting high spending in the last quarter of 2025. As a result, the US Dollar Index (DXY) is trading around 96.20, recovering from four-year lows, while the Australian Dollar increased with Gold reaching record highs.

Major Currency Updates

The major currency pairs show differing trends. The AUD/USD pair stays near 0.7020, supported by a strong Australian Dollar. Meanwhile, USD/JPY is around 153.00, influenced by the Bank of Japan’s views on inflation and wages. The EUR/USD pair is near 1.1950, steady after a recent peak, and GBP/USD is stable above its lower US counterpart at 1.3790. Gold, after hitting a new record, is now trading around $5,330. Upcoming economic reports include Flash GDP and CPI data for Germany and the Eurozone, along with the US Producer Price Index. The tension between the White House and the Federal Reserve is causing considerable market uncertainty. This political pressure on monetary policy suggests we should brace for sharp and unpredictable market movements in the coming weeks. Notably, the VIX, a measure of market fear, spiked over 30% in January, trading above 18. Considering options to capitalise on this rising volatility might be wise. The US Dollar Index is at a crucial point, recovering from a four-year low around 96.00. With the upcoming US Producer Price Index expected to show persistent inflation at about 3.5%, this supports Powell’s firm stance and could lead to a continued dollar rally. We might look at buying short-term call options on the dollar, anticipating a move towards the 97.50 resistance level seen in mid-2025.Gold Market Opportunity

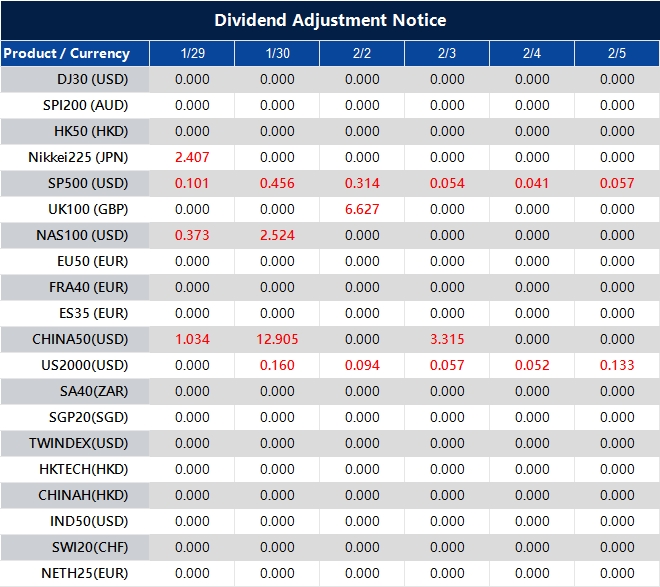

Gold’s recent drop from its all-time high above $5,500 presents an opportunity for bullish traders. This decline is supported by strong central bank buying, which saw an increase of over 1,000 tonnes in global reserves throughout 2025. Buying call options during this dip could position traders for another increase, especially if inflation worries continue. The significant drop in Microsoft shares serves as a warning for the entire tech sector, which has been a market leader for years. Concerns over rising AI spending, now up over 40% year-over-year for major tech companies, are impacting short-term profitability. We might consider buying put options on the Nasdaq 100 as protection against a broader tech correction in the first quarter. The Australian Dollar remains strong around 0.7020 but could reverse if the US dollar gains strength. Meanwhile, hints of further tightening from the Bank of Japan could enhance the Yen’s value, making long JPY positions an appealing option. We are monitoring for a possible downturn in AUD/JPY if risk sentiment weakens. Create your live VT Markets account and start trading now.Dividend Adjustment Notice – Jan 29 ,2026

Dear Client,

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

Monthly Analyst Scope: The Hidden Crypto Signal In Q4 Earnings

As the Quarter 4 2025 earnings season kicks off, investors’ eyes are fixed on the scoreboard to see if corporate America can justify the record valuations seen at the end of last year. Heading into Quarter 3, analysts expected S&P 500 earnings to grow by 7.9%.

Corporate America crushed expectations and delivered earnings growth of approximately 13.3%.

While that marked the ninth consecutive quarter of growth, it revealed a crack in the foundation regarding the consumer. Tech giants thrived, but companies exposed to everyday borrowers flashed warning signs.

Forward guidance was cautious, hinting that while the corporate engine is running hot, the fuel of consumer spending might be running low.

However, for the crypto market, the specific earnings-per-share numbers are almost irrelevant. The real signal lies in the macroeconomic ripples these reports create, specifically how they influence the one metric that matters most for digital assets, which is the US Dollar Index (USDX).

The Expectations For A Market Priced For Perfection

According to the latest data from FactSet, the consensus estimate for Q4 2025 earnings growth sits at 8.3%. If realised, this would secure a tenth straight quarter of expansion. Analysts are currently optimistic and project that this momentum will carry into 2026 with double-digit growth expectations of roughly 15%.

However, good news for the stock market is not necessarily good news for crypto. This is where the logic requires a shift away from simple correlations and toward the mechanics of global liquidity.

How The Dollar Controls Crypto Prices

To understand the link between earnings and crypto, we must look at the Federal Reserve’s reaction function.

The primary driver of Bitcoin’s price action over the last cycle has been global liquidity, which is essentially how much cheap money is moving around the system. The gatekeeper of this liquidity is the US Dollar.

If this earnings season delivers a blowout performance where companies report soaring profits and raise their guidance for 2026, it signals that the US economy is accelerating. In this situation, the Federal Reserve loses the incentive to cut interest rates.

Consequently, bond yields would likely rise and make the US Dollar more attractive to global investors. A surging Dollar acts like a vacuum that sucks liquidity out of risk assets. For Bitcoin, which is priced in USD, a strong Dollar often acts as a price cap.

Conversely, the scenario that traditionally ignites a crypto rally is a soft earnings season.

If we see a slight miss in earnings, particularly in the retail and consumer discretionary sectors, it suggests the economy is cooling. This forces the bond market to price in aggressive rate cuts from the Fed to support the economy. When the market anticipates rate cuts, the Dollar typically weakens as yields fall.

A falling Dollar increases the M2 money supply and creates the Goldilocks zone for crypto, which is an economy weak enough to demand liquidity injections but not so weak that it triggers panic.

However, traders must be careful because this logic has a breaking point.

We are currently facing a market with a split personality where stocks rely on growth to go up, while crypto often relies on liquidity to go up.

If earnings soften just enough to worry stock investors, the Fed typically steps in with the medicine of rate cuts. In that specific scenario, stocks might still feel sick from the lack of growth, but crypto rallies on the medicine of new liquidity.

The danger arises if the news becomes too bad. The argument that bad news is good news only holds if the economy is bending rather than breaking. If earnings are disastrous with massive layoffs or collapsing revenue, we are no longer looking at a slowdown but a potential recession.

In a true panic, the promise of future liquidity matters less than immediate safety. Investors will sell everything, including stocks, bonds, gold, and crypto, in a desperate dash for cash. Therefore, crypto bulls should be rooting for a soft landing in earnings, not a crash.

The Verdict

Ultimately, crypto traders should view this earnings season not as a report card on corporate health, but as a barometer for liquidity.

The key is to watch the reaction of the US Dollar immediately after major earnings prints. If the Dollar spikes, the economy is likely too hot, and crypto volatility may remain suppressed.

If the Dollar falls, the liquidity gates are opening, signalling a potential run for Bitcoin. However, if the Dollar spikes while stocks crash simultaneously, it indicates a recession scare where cash becomes the only safe haven.

The export price index for Australia increased by 3.2% in the fourth quarter, rebounding from a decline of 0.9%

Australia’s export price index has increased by 3.2% in the fourth quarter, reversing a previous drop of 0.9%. This change reflects a positive shift in export prices compared to the prior quarter.

The rise in the export price index signals changes in global demand and market conditions. Analysts note that such shifts can affect the country’s trade balance and economic forecasts.

Changes for Exporters

Exporters could see revenue changes due to these price shifts. The new data may influence their strategies regarding export volumes and target markets. Overall, these quarterly figures offer valuable insights into Australia’s economic landscape. They provide a glimpse into the trading conditions faced by businesses in the export sector. The notable rise in Australia’s export price index during the fourth quarter of 2025 is a strong positive sign. This data supports the trend noted earlier in the December 2025 trade balance figures, which reported a surplus of A$13.2 billion—the highest surplus in six months. Traders should consider that this strength may continue to bolster the Australian dollar, making long positions in AUD/USD futures or call options appealing. The price increase is driven by commodities, particularly iron ore, which has remained above $135 a tonne throughout January 2026 due to strong demand from Asia. This trend benefits major exporters listed on the ASX, with companies like BHP and Rio Tinto outperforming the broader market since the year began. Traders might consider call options on the XJO index or specific mining and energy stocks to capitalize on this momentum.Economic Data and Inflation Worries

The recent strong economic data raises inflation concerns, especially after last week’s Q4 2025 CPI reading was higher than anticipated at an annual rate of 3.4%. As a result, market expectations for a mid-year interest rate cut by the Reserve Bank of Australia have largely disappeared. Traders should prepare for the RBA to keep rates steady and possibly adopt a more hawkish stance at its upcoming meeting. Given this situation, increased market volatility is likely as expectations are adjusted. While the overall trend looks encouraging, implementing strategies like collars on equity positions can help shield against sudden reversals in commodity prices. Options on the AUD/USD provide a defined-risk way to speculate on currency movements linked to these strong trade conditions. Create your live VT Markets account and start trading now.Major tech firms had mixed earnings: Meta excelled, Microsoft underperformed, and Tesla exceeded expectations.

The tech sector had mixed earnings results, with notable reports from Microsoft, Meta, and Tesla.

**Microsoft** did well by exceeding revenue expectations, but its shares dropped 5% after hours. While the overall numbers looked strong, the company expects declines in earnings and revenue growth by 2025. Critics pointed out that its big investments in AI haven’t significantly boosted earnings, with capital expenditures reaching $37.5 billion.

**Meta**, in contrast, saw its shares jump more than 8% after reporting revenues and forecasts that beat expectations. The company plans to increase capital expenditures on AI to $135 billion, a move investors welcomed thanks to its strong ad revenue. Unlike Microsoft, Meta doesn’t face capacity constraints and is determined to meet ambitious AI objectives, attracting more investor interest.

**Tesla** shares rose by over 3%. Even though car sales decreased, the energy storage division performed well, and a weaker dollar worked in its favor. The company is focusing on expanding its cyber taxi business and investing in AI, aiming to transform from just a car manufacturer into a broader technology player. With lower capital expenditures of $2.39 billion, Tesla positions itself as a contender in the AI space while signaling potential recovery in stock prices.

The Q4 2025 earnings reports show that the market is punishing companies for substantial AI spending that doesn’t quickly improve profitability. Microsoft’s stock decline reflects investor impatience despite strong overall results. This scenario could lead traders to consider buying puts or creating bear call spreads on Microsoft, anticipating continued disappointment.

The stock’s 5% drop to around $425 has increased 30-day implied volatility to about 35%, raising options premiums. Since the company indicated that data center issues may not improve until the latter half of 2026, we could see sideways or downward movement in stock prices. Selling covered calls against long positions might be a wise way to earn income while waiting for the AI investments to pay off.

In sharp contrast, **Meta** is being rewarded for its AI investments because its growing advertising business offsets costs. The stock surged over 8% in after-hours trading to just under $555, indicating strong bullish sentiment. This momentum makes strategies like buying call options or putting together bull put spreads appealing in the coming weeks.

With the significant price rise, implied volatility has increased, making outright call purchases costly. Instead, traders might consider selling cash-secured puts at a strike price where they would be comfortable owning the stock, such as $520. This strategy lets them earn a hefty premium while maintaining a bullish to neutral perspective.

**Tesla** presents a more complex situation. The market responded positively to its earnings beat and shifting narrative. The 3% price increase reflects cautious optimism as it’s increasingly recognized as an AI and energy company, not just a car maker. This shift, combined with lower capital expenditures than competitors, might support the stock price.

After a tough start to 2026, with the stock below $240, this earnings report could serve as a recovery catalyst. Given Tesla’s historically high volatility, selling out-of-the-money puts for February or March 2026 expirations could be an effective way to collect premium, betting that the evolving AI narrative will stop the stock from dropping significantly further.

In January, New Zealand’s ANZ Business Confidence dropped from 73.6 to 64.1.

New Zealand’s business confidence index, reported by ANZ, fell from 73.6 in December to 64.1 in January. This drop indicates that businesses are becoming more cautious due to ongoing economic challenges.

While some sectors remain optimistic, overall sentiment is weakening. This change could impact future investment and spending decisions. People will be watching for new economic data and government actions that might affect business conditions and consumer confidence in New Zealand.

Impact of Dropping Business Confidence

The decline in New Zealand’s business confidence, from 73.6 to 64.1, shows that the economy’s outlook is softening. This suggests the New Zealand dollar’s recent strength might be peaking. We should prepare for more price fluctuations and possibly a downward trend for the Kiwi in the coming weeks. The situation looks more significant when we consider the recent inflation rate, which fell to 4.7% in the last quarter of 2025. This decrease in price pressure, along with weakening business sentiment, could lead the Reserve Bank of New Zealand to change its strict approach. Now, the market may start to seriously consider interest rate cuts later this year, which seemed unlikely just a few months ago. Given this, there is an opportunity in the currency markets through derivatives. Buying put options on the NZD/USD is a simple way to prepare for a possible decline while managing risk. A drop in the Kiwi seems likely as interest rate expectations shift against it.Comparisons to Past Economic Trends

This situation is reminiscent of what we saw in 2024, when the effects of the RBNZ’s aggressive rate hikes began to slow business activity. At that time, early signs of a slowdown led to a longer period of economic cooling. We should consider this confidence report as a possible early warning of a similar trend developing now. This outlook also affects the local equity market and interest rate swaps. Hedging long equity positions with NZX 50 index futures could be a wise move against a potential downturn in company profits. At the same time, traders might look to secure fixed rates in the swaps market, taking advantage of the rising expectation of lower official cash rates. Create your live VT Markets account and start trading now.Gold price hits historic high in early Asian trading due to safe-haven demand

Gold prices soared past $5,500, reaching a record $5,579 in the Asian market. This surge was driven by geopolitical tensions and economic uncertainties. A weaker US Dollar also increased demand for gold as a safe investment.

The Federal Reserve kept interest rates between 3.5% and 3.75%. Low rates make holding gold cheaper, which makes it more attractive to buyers.

Geopolitical Tensions Rise

Geopolitical tensions escalated after US President Donald Trump cautioned Iran about its nuclear weapon negotiations. Iran’s threats of retaliation heightened concerns and made gold more appealing. The expectation of a new Fed Chair appointed by Trump added to the uncertainty, further boosting gold demand. Worries about the Fed’s independence and potential interest rate cuts under new leadership shaped market behavior. Despite gold’s rise, some profit-taking could affect its short-term performance, especially after an 80% annual increase. Central bank purchases and interest from trend-following funds were major factors in the market, hinting at potential buying opportunities during price dips. Supportive fundamentals are expected to last until 2026. As gold hits $5,500, we see strong bullish sentiment driven by geopolitical issues and a steady Fed. However, with an 80% increase over the last year, the market may be overextended, and a sharp pullback could occur. This creates challenges but also opportunities for traders in the coming weeks.Trading Strategies and Market Outlook

With strong underlying support from global tensions and steady interest rates from the Fed, traders seeking further gains might consider buying call options. This strategy allows participation in any rally while limiting risk to the premium paid, enabling traders to stay long without full exposure to a sharp downturn. The rapid increase in prices signals caution. A similar situation happened in 2011 when gold peaked above $1,900 an ounce before dropping by over 25% the following year. Buying put options could be a smart way to hedge existing long positions or bet on a near-term correction. The upcoming announcement of a new Fed Chair is a key factor for potential volatility. This uncertainty is reflected in the Cboe Gold Volatility Index (GVZ), which is currently around 25, a level not seen consistently since early 2023’s banking stresses. Strategies like long straddles, which profit from a significant price shift in either direction, might work well until the new Fed leadership is clarified. Create your live VT Markets account and start trading now.Foreign investment in Japanese stocks dropped from ¥874 billion to ¥328.1 billion in January 2023

Foreign investment in Japanese stocks dropped significantly from ¥874 billion to ¥328.1 billion in January. This is a notable decrease compared to earlier totals.

The US Federal Reserve decided to keep interest rates steady during its January meeting, keeping the Fed Funds Target Range at 3.50%-3.75%. This matched what the market expected.