Crude oil prices are on the rise as traders consider potential sanctions and possible rate cuts from the Federal Reserve. Last week, oil seemed ready to climb to the $70.00 level after breaking key technical levels, but it dropped to around $61.45. This decline was driven by expectations that OPEC+ would raise output and concerns over weak economic data from the U.S.

OPEC+ has decided to increase output by 137,000 barrels per day, with more increases depending on market conditions. This could potentially reverse the previous cut of 1.66 million barrels. This cautious strategy positively influenced oil prices. New sanctions against Russia might raise prices further, although historically, sanctions have had limited effects because of shadow markets.

Technical Analysis And Market Drivers

From a technical perspective, the daily chart indicates that oil tested the trendline near the $64.00 mark before dropping and rebounding at $61.45. On the 4-hour chart, prices are nearing the crucial $64.00 area. Sellers anticipate a decline, while buyers hope for a rise to $66.00. The 1-hour chart shows a small upward trend, suggesting bullish momentum, with buyers aiming for new highs and sellers expecting a drop.

We are looking for important data in the coming days, including the U.S. PPI report on Wednesday, the CPI data and jobless claims on Thursday, and the University of Michigan Consumer Sentiment report on Friday.

We are closely monitoring crude oil after its bounce from the $61.45 level last week. The market is now testing the important $64.00 zone, responding to the cautious outlook from the early September OPEC+ meeting. This movement indicates traders are considering supply stability against potential economic challenges.

The case for immediate rate cuts by the Fed, which would typically boost demand, has weakened. Last week’s data showed the U.S. Consumer Price Index for August 2025 was unexpectedly high at 3.4%, complicating the Fed’s decisions. This shifts attention to supply-side factors for price support.

Options And Trading Strategies

On the supply front, conditions remain tight, supporting the recent price rebound. A Reuters survey on August 2025 production revealed that OPEC+ compliance with cuts is over 95%. Additionally, G7 leaders recently threatened to tighten enforcement of the price cap on Russian oil, adding to the geopolitical risk.

Given the clash between persistent inflation and tight supply, we should expect ongoing volatility. Derivative traders might explore strategies like straddles around the $64 level, preparing for significant price movements in either direction. This method avoids the need to predict the market’s ultimate direction in the near future.

For traders with a specific view, options can offer clear, risk-defined strategies. Those who believe in supply concerns might consider call options with strike prices above $66. In contrast, traders betting that fears of an economic slowdown will prevail could opt for put options targeting a decline below the recent $61.45 low.

This pattern of volatility is not new; we observed similar sharp reactions to OPEC+ headlines throughout late 2023 and 2024. Often, initial sell-offs on production hike rumors were later reversed once the market absorbed the conditional nature of supply increases. This historical perspective suggests the recent bounce from lows could persist, but economic data will remain a critical factor.

Create your live VT Markets account and start trading now.

here to set up a live account on VT Markets now

Written on September 8, 2025 at 12:35 pm, by davin

The American labour market has stumbled, and investors are already bracing for the Federal Reserve to hit the brakes.

August’s non-farm payrolls showed just 22,000 jobs added, a steep slowdown from July’s 79,000. Unemployment edged up to 4.3 per cent, its highest in years. Hardly a surprise, given the earlier warnings.

On 3 September, the JOLTS report revealed job openings had slipped to 7.18 million, the lowest since late 2024. The signs were there; the NFP merely confirmed them.

There are more Americans out of work than there are jobs open for the first time since April 2021.

Wednesday's JOLTS report showed that the ratio of job vacancies to unemployed workers fell below 1 to 0.99 in July. https://t.co/eIMzmwIT8k

With manufacturing and trade shedding jobs and overall demand softening, the Fed is finding itself in a tight spot. Markets have reacted swiftly.

According to the CME FedWatch Tool, traders now price in a full 100 per cent chance of a rate cut at the 17 September meeting. That’s taken as a given. What has shifted is the outlook beyond: a 79.5 per cent probability of another move in October, with December’s odds climbing to 73.3 per cent.

Only weeks ago, investors were still debating whether the Fed would cut again at all this year. That conversation is over. The question now is how many times.

Much of this change stems from Powell’s comments at Jackson Hole. The Fed Chair didn’t just reference jobs. He made them the centrepiece. After two years of focusing squarely on inflation, he acknowledged that the balance of risk has tilted toward employment.

Governor Waller reinforced that urgency, insisting cuts should begin straightaway. It is now clear that the Fed views a weakening labour market as the more pressing danger, even while inflation holds above three per cent.

That makes the September FOMC meeting pivotal not only for the rate call but also for the dot plot. In June, projections pointed to two cuts in 2025. That stance already looks dated.

Following this NFP, policymakers may shift their dots lower, signalling three cuts rather than two. They will tread carefully, though. Inflation hasn’t convincingly broken lower, but softening the dot plot allows flexibility without over-committing.

Market reactions have been uneven. The S&P 500 initially jumped on hopes of easier policy, but the rally quickly fizzled and the index closed near 6,480.

The failed breakout suggests investors are wary: they like rate cuts aimed at supporting growth, but cuts triggered by economic weakness tell a different story.

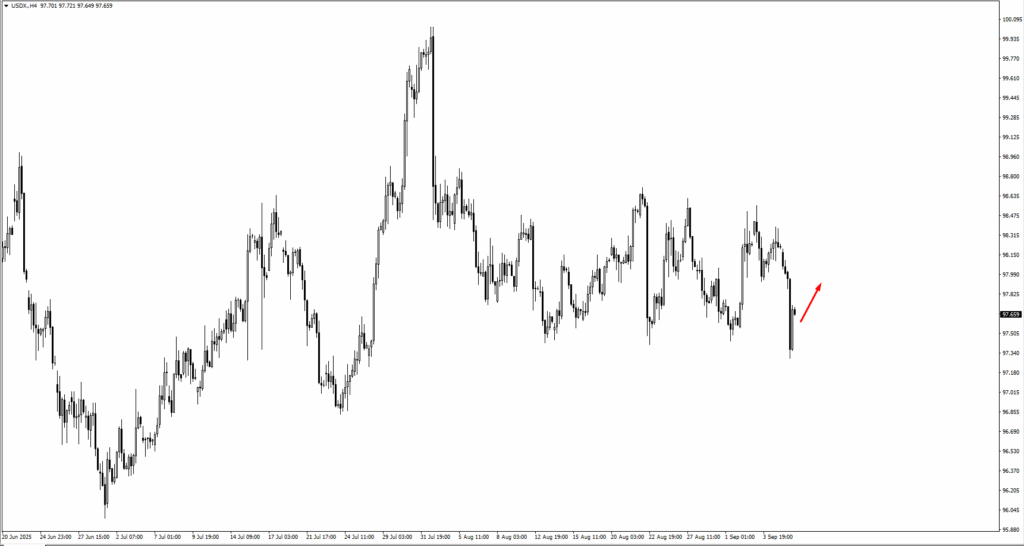

The dollar slipped too. The US Dollar Index fell beneath 97.40 before rebounding slightly to around 97.65. The move reflects collapsing yield expectations but stops short of a breakdown. A sustained move below 97.30 would tilt momentum more decisively lower.

Bitcoin has acted like a classic risk proxy. It spiked to 113,000 USDT after the NFP before giving back gains, consolidating around 110,900.

With equities unsteady, BTC looks set to trade in a narrow band between 109,500 and 111,500. Sentiment is cautious, and without a lead from stocks, crypto may remain choppy.

Looking forward, the 11 September CPI report and the 17 September FOMC meeting are the real catalysts. A sub-3 per cent inflation print would harden expectations for October and December cuts.

If inflation proves sticky, especially in the core measures, the Fed may be forced to hold fire into year-end, keeping scope for easing in early 2026 instead.

Until then, markets sit between two narratives: confidence in a soft landing versus anxiety that the runway is running out.

Market Movements Of The Week

The US Dollar Index moved as expected post-NFP, slipping lower after breaking 97.409, then bouncing near 97.35 as it attempted to reclaim higher ground. Price action is now hovering just below 97.90, a key area where bulls will want to see a decisive close.

EURUSD pushed higher in response to the softer dollar backdrop. After forming a new swing high, the pair found resistance near 1.1755. The rejection at that level halted further upside for now.

GBPUSD also followed the directional bias, making a new swing high before rolling over. As the pair trades lower into the week, the 1.3475 level becomes the next important price zone to monitor for signs of renewed interest from buyers.

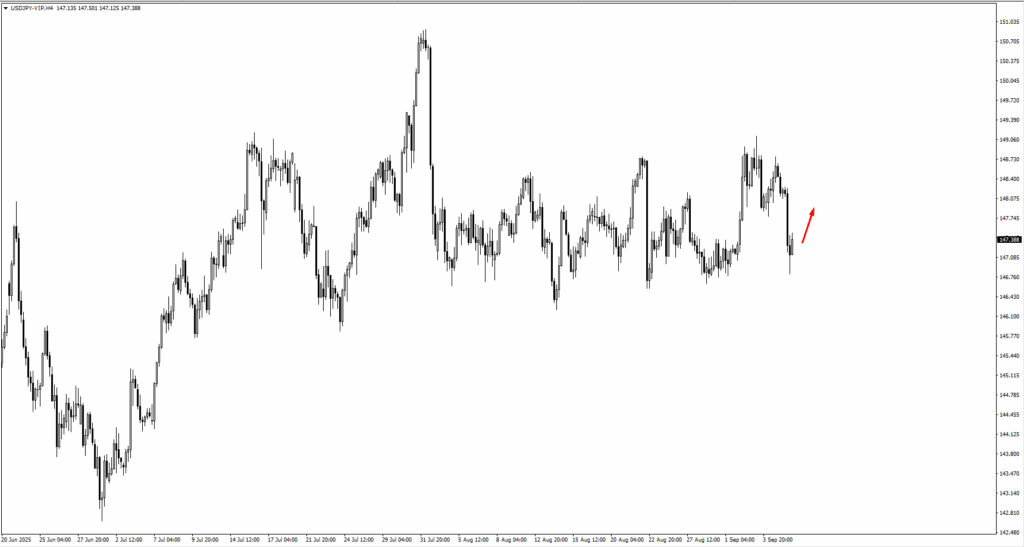

USDJPY remains in its consolidation phase, with price flirting above the recent 148.939 high before pulling back. With the pair still range-bound, eyes are now on the 148.00 handle as a possible re-entry point for buyers.

USDCHF followed the playbook almost perfectly. After hitting a weekly high from the monitored 0.8090 zone, price retraced and found support at 0.7960. The rebound from there has set up a new area of interest near 0.8015.

AUDUSD and NZDUSD both caught downside momentum. Aussie dropped from the 0.6590 resistance area and now eyes 0.6515 for potential support. Kiwi followed suit, falling from the 0.5930 zone and tracking toward 0.5850.

USDCAD bucked the dollar weakness trend and moved higher after the NFP release, breaking cleanly through local resistance. Traders are watching for follow-through above 1.3880.

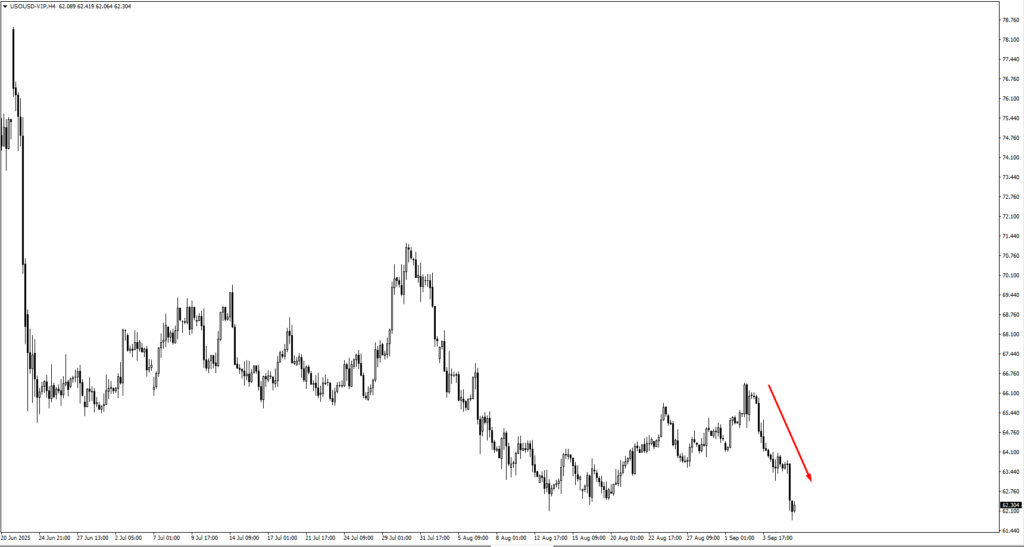

Oil struggled last week, pulling back from the 66.45 zone and now tracking toward 61.15. With demand expectations softening alongside global growth concerns, traders are starting to question whether crude can hold its recent uptrend.

Gold is waiting. After reacting to the post-NFP drop in yields, the metal is now consolidating. Price action at 3530 will be critical. A strong bullish setup there could open a path toward 3650, especially if CPI prints softer and the dollar stalls.

The S&P 500 mirrored the broader risk tone. The index made a new swing high but failed to extend, pulling back and closing below 6,500. A retest of that level now becomes the line in the sand for bulls.

Bitcoin continues to behave more like a sentiment barometer than a safe haven. It dropped toward the lower edge of the 114,400 zone and has yet to show decisive direction. Price is hovering near 112,350, where bulls may attempt to defend again.

Natural gas has slipped lower once more after failing to break out above the 3.04 zone. Price is now eyeing 2.91 and potentially 2.87 next. With cooling demand and no clear catalyst, nat gas remains in a technical downtrend for now.

Across the board, markets are recalibrating. The weak jobs print changed the tone, but this week’s CPI and the FOMC next week will decide whether traders double down on the dovish pivot or rein in expectations.

Key Events Of The Week

On Wednesday, 10 Sep, US Producer Price Index (PPI) month-over-month is forecast to rise 0.3 percent, cooling from July’s 0.9 percent. The drop would support the case for weakening inflation momentum, especially if it aligns with soft labour conditions.

If the US Dollar Index has indeed finished its upward consolidation, this number could nudge it lower again. That said, any upside surprise may revive short-term dollar bids.

Thursday, 11 Sep, brings two big prints. The Eurozone’s Main Refinancing Rate is expected to remain flat at 2.15 percent. That’s no change from the prior reading, but with inflation still sticky and growth slowing, the tone of the accompanying press conference will matter more than the number itself.

Traders will likely treat the policy language as a signal of whether the European Central Bank will hold the line or join the global dovish pivot.

Meanwhile, US CPI year-over-year is forecast to accelerate to 2.9 percent from 2.7 percent. If the data comes in below expectations or stays flat, markets may take it as a green light for the Fed to proceed with a full rate-cut cycle.

On Friday, 12 Sep, the UK takes the spotlight with GDP month-over-month expected to stall at 0.0 percent, down from 0.4 percent. That’s a weak signal, and if confirmed, it could increase pressure on the Bank of England ahead of its upcoming policy decision.

Weak GDP might reduce the odds of further hikes or even accelerate discussion around rate stability. Sterling could come under pressure if paired with soft CPI the week after.

Rounding out Friday’s session is the University of Michigan Prelim Consumer Sentiment Index, forecast at 58.0 versus 58.2 previously.

While not a market mover on its own, a surprise drop could reinforce recession worries. With consumers driving the bulk of US GDP, any sharp swing here may contribute to risk-off trading heading into the weekend.

A confidence vote for French Prime Minister Bayrou is happening today, with results expected around 1500 GMT. The euro has mostly ignored potential risks, even though Bayrou may be removed from office. Societe Generale warns that the market might not have fully considered the possible reactions.

There are a few possible outcomes. Bayrou could lose the vote, leading to the appointment of a caretaker prime minister or the dissolution of the National Assembly. This might result in elections, which could lead to a hung parliament. If the elections create a hung parliament or a National Rally victory, it may introduce political and financial risks that could hurt the euro.

Even if results are positive, the impacts on the euro could still be limited and potentially negative. Societe Generale indicates that markets currently seem relaxed, with the forecast for EUR/USD suggesting a target of 1.1570.

With the French confidence vote approaching, the markets appear unconcerned. The one-month EUR/USD implied volatility is a low 5.8%, suggesting that traders might be underestimating the chaos that could follow if Prime Minister Bayrou is removed today. This complacency creates an opportunity since the risk leans toward a negative surprise for the euro.

The most likely outcomes are either a caretaker government or the dissolution of the National Assembly for new elections. Looking back at the snap election in summer 2024 shows how situations like this can impact markets. A new election brings the risk of another hung parliament or a National Rally win, which recent polls show leading with 34% of the intended vote.

The spread between French and German 10-year bonds is an important indicator to follow in the coming weeks. It’s currently around 65 basis points, but it went over 80 basis points during last year’s political uncertainty, showing how quickly sentiment can change. A similar rise could indicate significant stress and put pressure on the euro.

Since options are currently inexpensive, buying downside protection, such as EUR/USD put options, could be a cost-effective way to prepare for turmoil. This strategy would benefit from a drop in the euro’s value along with a potential increase in volatility. The low volatility makes entering such a trade attractive.

Even if Bayrou survives, the upside for the euro looks limited. However, scenarios leaning toward political instability suggest a drop to the 1.1570 area. The risks clearly favor those betting on a weaker euro.

here to set up a live account on VT Markets now

Written on September 8, 2025 at 11:35 am, by davin

The pound’s earlier drop, caused by rising UK long-term yields, changed after a disappointing US Non-Farm Payroll report. This led to a decline in the US dollar as expectations grew for the Federal Reserve to take a softer approach, with projections of rate cuts up to 70 basis points by year-end. If the US Consumer Price Index (CPI) remains weak as the Federal Open Market Committee (FOMC) meeting approaches, it may further weaken the dollar.

Despite these changes, the US dollar stays within a specific range, influenced by potentially overextended bearish positions. If the economy improves after Fed rate cuts, future cuts could be reassessed, which might support the dollar. In contrast, the Bank of England has a hawkish stance backed by solid data, including rising UK CPI and Flash PMIs, despite a recent decline due to the UK 30-year yield hitting a cycle high.

Technical Analysis Of GBP/USD

For GBP/USD, traders watch key resistance and support levels closely, reacting to potential breaks or rebounds. The daily, 4-hour, and 1-hour charts suggest that buyers may aim for higher levels if current momentum continues or if they break through key resistance. Upcoming economic reports, like US PPI and CPI, UK GDP, and consumer sentiment, will influence the market.

The US dollar weakened last Friday after the Non-Farm Payrolls report revealed only 110,000 job gains, missing expectations. This weak data has led to predictions of three Federal Reserve rate cuts by the year’s end. As a result, the derivative markets now show over a 90% chance of a cut at the September 17th FOMC meeting.

All eyes are now on the US CPI report scheduled for this Thursday, with economists expecting a 0.2% month-over-month increase in the core reading. A lower figure could prompt more dollar weakness and signal options traders to buy GBP/USD calls. Conversely, a stronger-than-expected result could quickly shift the market’s view on the pace of Fed cuts.

For the pound, the situation is quite different. The Bank of England is worried about persistent inflation, as last month’s UK CPI printed at 3.1%. This keeps pressure on the central bank to hold off on further cuts. This difference in policy approaches is a key reason for the continued strength in the GBP/USD pair.

Market Positioning Strategies

Currently, the pair is testing the important 1.3590 resistance level after bouncing back from the 1.3368 support area. Traders may consider buying short-dated call options with a strike price above 1.3600 in anticipation of a breakout from a weak US CPI report. Alternatively, put options below the current upward trendline could offer protection if US data turns out strong.

This situation reminds us of market behavior in spring 2024, when weak US data led to a significant dollar decline. While we acknowledge that bearish dollar positions may be getting crowded, it seems that the easiest path for the dollar is down. A strong upside surprise in the data would be needed to change this outlook.

Create your live VT Markets account and start trading now.

here to set up a live account on VT Markets now

Written on September 8, 2025 at 10:36 am, by davin

Recent data shows that Bitcoin holdings by companies are decreasing. Even though Bitcoin is still popular, companies labeled as “Bitcoin treasury companies” are buying less, taking a more cautious stance. Reports reveal these companies currently hold a record 840,000 Bitcoin but are buying less with each transaction. For example, Strategy’s purchases have plummeted by 86% from earlier this year, indicating possible financial strain or increased caution.

El Salvador has bought gold for the first time since 1990, moving away from Bitcoin, hinting at a bearish outlook for Bitcoin. Japan is also considering tightening crypto regulations, which may calm speculative investments. However, institutional adoption of Bitcoin is still growing, even though it doesn’t clarify the market’s direction. The current Bitcoin price is at $112,035, showing a positive outlook when above $112,000. A drop below $111,520 would signal a downward trend.

Plans for Bitcoin futures suggest bullish targets above $112,000, with key levels identified at $112,465 and $113,945. On the bearish side, targets below $111,520 start at $111,250. Strategies recommend careful trading and focus on risk management.

The technical outlook is bullish as long as prices remain above $112,000. Still, caution is warranted since large corporate buyers are significantly slowing their purchases. This indicates that although prices are stable for now, the institutional momentum that helped boost them may be dwindling.

In the derivatives market, we see signs of this uncertainty. Data from early September 2025 shows that open interest in futures has stayed flat, even with high prices. Additionally, the 30-day options skew has increased slightly, revealing a higher demand for put options that investors might use to hedge their long positions.

For traders with a positive outlook, this environment favors risk-defined strategies instead of straightforward long futures. Call spreads can help in aiming for targets like $112,895 while limiting losses if support at $112,000 fails. Selling cash-secured puts below the bearish trigger of $111,520 can also offer market exposure or generate premium if the market stays steady.

However, a clear break below $111,520 should signal a shift in sentiment. This would invalidate the current bullish setup and open targets for a decline, especially around the major support cluster near $110,755. Aggressive traders might seize this opportunity to start short futures positions or purchase puts.

The mixed signals imply that volatility could rise in the upcoming weeks. The current hold above the 2021 all-time highs is a significant test, suggesting the market is ready for a larger movement. This makes strategies like long straddles or strangles appealing, particularly before any important political or regulatory announcements.

Bitcoin Price Movement

here to set up a live account on VT Markets now

Written on September 8, 2025 at 10:35 am, by davin

**HSBC Predicts Bank of England Will Hold Rates**

HSBC believes the Bank of England (BOE) will keep its rates unchanged until April 2026. Previously, they expected cuts to start in November and continue in February.

Market views on the BOE have stayed steady, as traders do not predict any cuts in the remaining months of this year. The next expected rate cut is in February 2026, while a significant rate change may happen in March 2024.

Inflation risks continue to be a key factor in understanding the UK economy’s financial situation. The upcoming November budget will also be crucial in this analysis.

The forecast for UK interest rates has changed. The BOE is now likely to hold rates steady until at least April 2026, pushing back earlier expectations for cuts this year. This means we need to adjust our positions that were betting on reductions soon.

This decision is influenced by inflation, which remains above the 2% target. In August 2025, the Consumer Price Index (CPI) was recorded at 2.8%. Furthermore, wage growth is concerning, at an annual rate of 4.5%. This leads us to believe the BOE will remain cautious, unlike in late 2023 when markets anticipated quick rate cuts.

**Impact on Sterling and Interest Rate Futures**

For those involved in trading sterling interest rate futures, contracts for December 2025 and March 2026 are likely to maintain or increase their implied yields. Therefore, it may be wise to consider paying fixed rates on short-term swaps to align with the “higher-for-longer” reality. The UK’s slow economic growth, which only grew by 0.1% in the second quarter of 2025, does not seem strong enough to push the BOE to act just yet.

This situation is different from other central banks that have already started easing, which should help support the pound. A stronger sterling, especially against the euro and dollar, is expected in the medium term. With the November budget approaching, we should prepare for increased volatility, making options strategies appealing to guard against any unexpected fiscal changes.

Create your live VT Markets account and start trading now.

here to set up a live account on VT Markets now

Written on September 8, 2025 at 10:35 am, by davin

The Federal Reserve’s outlook has shifted to a more cautious stance after the latest jobs report. Some traders now think there might be a 50 basis point rate cut in September. By the end of the year, there’s a 91% chance of a 70 basis point cut in the next meeting. In Europe, the European Central Bank expects only an 8 basis point cut, but there’s a 99% chance rates will stay the same next time.

The Bank of England anticipates a 12 basis point cut, with a 98% likelihood of no change at its upcoming meeting. Canada is expecting a larger cut of 42 basis points, with an 89% chance of that happening soon. The Reserve Bank of Australia forecasts a 30 basis point reduction and has an 81% chance of keeping rates steady.

Expectations for the Reserve Bank of New Zealand

The Reserve Bank of New Zealand is set to cut rates by 38 basis points, with a 91% chance of this happening at the next meeting. The Swiss National Bank anticipates a small 7 basis point cut but has a 91% chance of keeping rates the same. The Bank of Japan is not expected to change, with a 12 basis point hike possible, but there’s a 97% chance rates will stay unchanged.

Last Friday, the US jobs report revealed only 125,000 new jobs, far below the expected 180,000. This disappointing data has led to increased speculation about major rate cuts. The market is now nearly certain a rate cut will occur at the Federal Reserve’s meeting on September 17. Weaker wage growth, which was only 0.2%, also influenced this shift.

Traders are now expecting a total of 70 basis points in cuts by the end of the year, suggesting three 25 basis point reductions. Some are hoping for a larger “insurance cut” of 50 basis points this month, similar to what happened in 2024. The chances of such a significant cut have risen to about 9% in futures markets.

Key Focus on US CPI Inflation Report

This week, all eyes are on the US CPI inflation report due on Thursday, September 11. A weak inflation update could encourage the Federal Reserve to implement that larger 50 basis point cut. Consequently, interest rate futures are buzzing with activity as traders prepare for market shifts.

It’s not only about the Fed; Canada’s job market also took a hit, losing 10,000 jobs unexpectedly. This has solidified expectations for a second rate cut from the Bank of Canada, which now includes 42 basis points of cuts anticipated by year-end. Such policy differences may create chances for trading currency pairs like USD/CAD.

With the discussion around whether to cut by 25 or 50 basis points, we can expect short-term volatility in bond and currency markets to rise. Traders can take advantage of this with options strategies, such as straddles on treasury futures, which are looking more appealing ahead of Thursday’s data. The VIX is around 17 and likely to face upward pressure this week.

Create your live VT Markets account and start trading now.

Investor confidence in the Euro area has dropped in September, hitting its lowest point since April. According to Sentix, the latest reading is -9.2, whereas analysts had expected it to be -2.0.

Concerns about the economy are rising sharply, as Sentix notes. There’s little sign of a recovery this autumn, and industries focused on exports may face tougher times due to tariffs from the US.

The significant decline in confidence to -9.2 shows that people are becoming more pessimistic about the Eurozone’s economy. This marks the lowest level since spring and indicates increasing fears of a recession. We should prepare for more bearish investments in the coming weeks.

This negative outlook suggests that investors might want to buy put options on key European indices like the Euro Stoxx 50 and Germany’s DAX. Supporting this, Germany’s final manufacturing PMI for August 2025 was confirmed at a contractionary 43.5, highlighting real industrial weakness. Such poor sentiment is likely to put additional pressure on stock prices.

The euro may weaken, especially against the US dollar. With the US economy appearing stronger and tariffs on the horizon, the EUR/USD exchange rate could fall to levels not seen since earlier this year. This situation resembles the dollar strengthening we experienced during the energy crisis in 2022, when uncertainty loomed over Europe.

This troubling data complicates matters for the European Central Bank (ECB). While growth is clearly slowing, the latest Eurostat flash estimate for August inflation stands at 2.7%, still too high for the ECB’s target. This environment of stagnation and inflation makes it hard for the ECB to cut interest rates, which could have provided some market support.

Increased economic anxiety often leads to higher market volatility. Therefore, we should think about long volatility positions, like buying calls on the VSTOXX index, to protect against or benefit from anticipated price fluctuations. The current anxieties resemble those from early 2023 when global recession risks were reassessed.

The mention of US tariffs directly affects export-heavy sectors such as German car manufacturers and French luxury brands. With Washington scheduled to review these tariffs in October 2025, traders are likely to factor in this risk more aggressively. Options strategies that target these sectors could be effective.

Gold prices have soared past $3,600, reaching new highs despite the usual sluggishness of September. Several favorable factors are driving this increase.

Gold’s upward trend began last year and continues strongly. While September typically sees lower prices, current developments around U.S. Federal Reserve policy and data changes are boosting gold’s appeal. This week’s upcoming Consumer Price Index report may influence gold prices even further.

Global and Domestic Influences on Gold Prices

Both global and local factors support gold prices, making major market shifts unlikely. Important elements include expected Federal Reserve easing, central bank gold purchases, ETF activity, a weak dollar, and threats of stagflation. Together, these factors offer strong support for gold.

As we approach December and January—historically strong months for gold—traders are paying close attention to how these months might influence current trends. Many traders buy gold when prices dip. Currently, the main focus remains on benefiting from gold’s upward momentum.

With gold now solidly above $3,600, we see a clear signal to stay bullish. The momentum since the breakout in late August suggests that buying call options or call spreads is a great way to ride this trend. This current surge is overcoming the usual September decline, hinting at stronger forces at work.

The rally is mainly driven by expectations of Federal Reserve easing, which have become even stronger since last week’s disappointing non-farm payrolls report of just 95,000 jobs added. Following this news, the odds for a rate cut in November have risen to over 70%. Continued pressure on the U.S. dollar, now testing its yearly lows, further supports gold.

Market Strategies and Upcoming Data Releases

Strong physical demand is also seen as central banks added 55 tonnes to their gold reserves in August. Additionally, gold-backed ETFs experienced their biggest weekly inflow since the second quarter, bringing in over $2.5 billion. Traders should closely monitor this Thursday’s CPI report; a surprise rise in inflation could lead to a price correction.

Given the market’s “buy the dip” mentality, any decline in prices is expected to attract strong buying interest. Selling out-of-the-money puts could be a worthwhile strategy, allowing traders to benefit from premiums if gold prices keep rising or to enter a long position at a reduced price. This is particularly relevant after the lengthy consolidation period from May to August 2025, which laid a solid foundation for the current price surge.

The current strength is significant as we approach the traditionally positive seasonal period for gold in December and January. For now, we should capitalize on the upward momentum while being cautious around key data releases.

Create your live VT Markets account and start trading now.

The US dollar dropped significantly after a weaker-than-expected Non-Farm Payrolls (NFP) report. This has led to higher expectations for Federal Reserve interest rate cuts. The market now predicts three cuts by the end of the year, totaling 70 basis points. If the Consumer Price Index (CPI) report is also soft, we could see a 50 basis point cut in September. Overall, the dollar is trending downward unless strong economic data emerges to change this.

For the euro, recent attention has shifted to the French political landscape, with a confidence vote expected to cause some market changes. The European Central Bank (ECB) members are currently neutral on rate cuts, waiting for significantly negative data to consider any further easing. By year-end, only 8 basis points are anticipated, reaching 19 basis points by the end of 2026. This suggests we might be nearing the end of the easing cycle.

Technical Analysis

From a technical perspective, the EURUSD is testing a breakout from its monthly range on the 4-hour chart, with a potential rally if it breaks upwards. On the 1-hour chart, a recent surge was followed by a pullback. Buyers are looking at support at 1.1680, while sellers are targeting support at 1.16. Key upcoming reports include the US Producer Price Index (PPI) on Wednesday, the ECB rate decision and the US CPI report on Thursday, and the University of Michigan Consumer Sentiment report on Friday.

The US dollar is under pressure after last Friday’s NFP report showed only 145,000 jobs were added in August, falling short of expectations. This led to a full pricing of three Federal Reserve rate cuts by year-end. Futures markets now indicate over an 80% chance of the first cut happening at the September Federal Open Markets Committee (FOMC) meeting.

All attention is on this Thursday’s US Consumer Price Index (CPI) report, which will be crucial. A weak inflation figure, especially if the core year-over-year rate drops below 3.0%, would likely lead to a dovish Fed. This could push the EURUSD above its month-long resistance, starting a new upward trend.

In Europe, the situation is different, which creates a clear policy divergence that supports the euro. The ECB has indicated it may not cut rates any further for now, with recent Eurozone inflation data being stickier than expected. This difference between a dovish Fed and a neutral ECB is driving the potential EURUSD breakout.

Options and Strategies

For traders expecting an upward breakout, buying EURUSD call options just above the current range seems wise. This allows for leveraged betting on a rally following weak US data, with risk limited to the premium paid for the option. The goal would be to capture a quick move towards new cycle highs.

If we feel the market is ahead of itself, selling a call credit spread with a ceiling above the range offers another option. This strategy benefits from time decay and a failure of the EURUSD to break out, which might happen if the CPI report is stronger than expected. This is a bet that the pair will stay within the range or fall back to the 1.1600 support level.

Caution is necessary, as we recall a similar situation from early 2024 when the market priced in Fed cuts that did not materialize quickly. A surprisingly strong CPI number this week could lead to a sharp reversal, impacting bearish dollar positions. Therefore, managing risk around this week’s data releases is essential.

Create your live VT Markets account and start trading now.