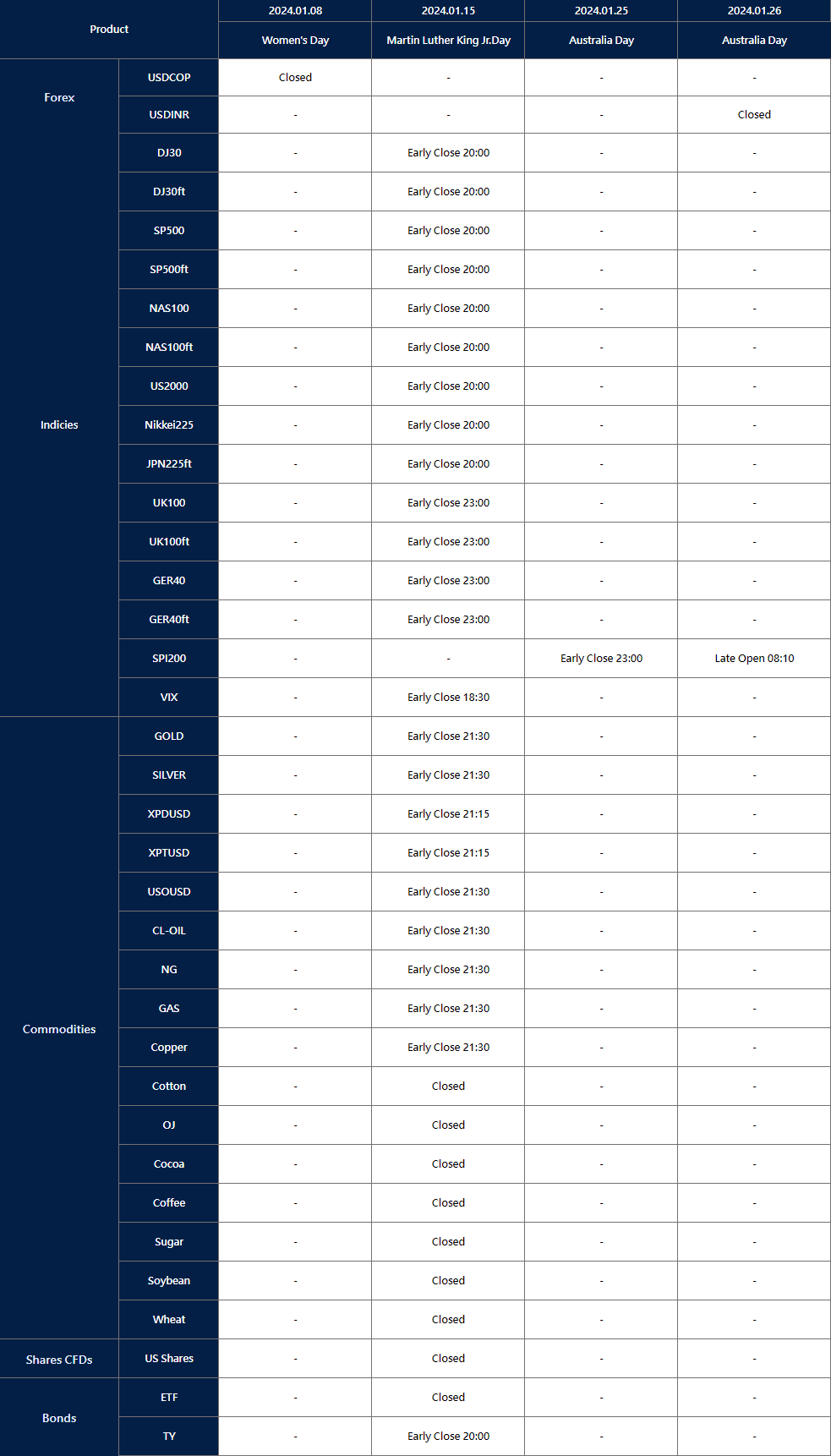

Affected by international holidays, the trading hours of some VT Markets products will be adjusted. Please check the following link for the remaining affected products:

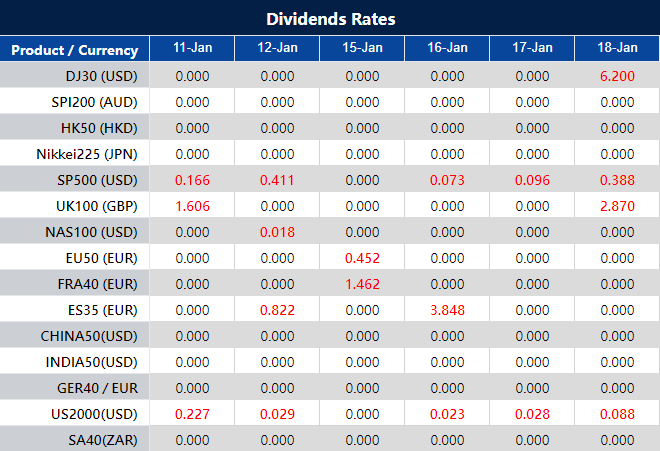

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

In a bullish session, stocks closed higher with the S&P 500, Dow Jones, and Nasdaq posting gains fueled by positive earnings reports, particularly from Intuitive Surgical and Lennar. Investor attention is now focused on the eagerly awaited consumer price index (CPI) report and producer price index, with expectations influencing speculation about potential shifts in Federal Reserve interest rate policies. The dollar index declined slightly due to gains against the yen and losses versus the euro, influenced by yield spreads and economic indicators. Meanwhile, the Bank of Japan maintains caution in unwinding monetary policies, while the eurozone faces economic concerns. Sterling rose, supported by higher gilts-Treasury yield spreads, despite BoE rate cuts pricing lower than the Fed’s.

Stock Market Updates

Stocks closed higher on Wednesday, driven by anticipation surrounding the upcoming release of fresh U.S. inflation data and corporate earnings reports. The S&P 500 rose by 0.57% to close at 4,783.45, the Dow Jones Industrial Average added 170.57 points (0.45%) to reach 37,695.73, and the Nasdaq Composite advanced 0.75% to settle at 14,969.65. Intuitive Surgical and Lennar played pivotal roles in lifting the market, with both companies experiencing notable stock increases of 10.3% and 3.5%, respectively. Intuitive Surgical raised its procedure growth outlook for fiscal year 2024, while Lennar announced an increase in its annual dividend.

Investor focus is now shifting towards the awaited consumer price index (CPI) report scheduled for release on Thursday, with expectations of a 3.2% year-over-year increase in December. Additionally, the producer price index is set for release on Friday. Investors are closely monitoring these reports for insights into potential shifts in the Federal Reserve’s interest rate policies, with current expectations hovering around a 64% likelihood of rate cuts, according to the CME Group FedWatch tool. The upcoming earnings season adds to the market’s dynamics, with major financial heavyweights like JPMorgan Chase, Bank of America, UnitedHealth, and Delta Air Lines set to reveal their results on Friday. Despite a mixed session on Tuesday, stocks exhibited positive momentum on Wednesday.

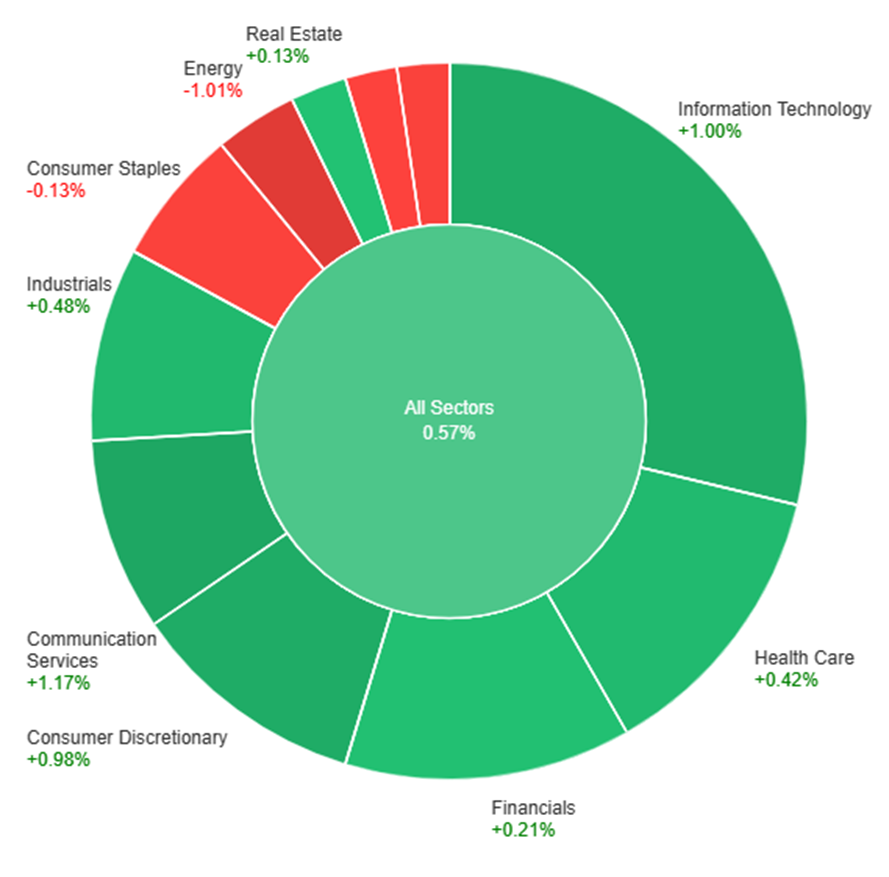

On Wednesday, the overall market exhibited a positive trend with a gain of 0.57%. Notable sector performances include Communication Services and Information Technology, both experiencing substantial increases at +1.17% and +1.00%, respectively. Consumer Discretionary and Industrials also contributed to the positive momentum with gains of +0.98% and +0.48%. Health Care and Financials showed more modest increases at +0.42% and +0.21%. On the flip side, Energy suffered a notable decline of -1.01%, dragging down the overall performance. Utilities and Consumer Staples experienced marginal losses at -0.06% and -0.13%, while Real Estate and Materials also showed slight decreases at +0.13% and -0.17%.

Currency Market Updates

The dollar index experienced a 0.1% decline, driven by notable gains against the vulnerable yen and losses versus the euro. This shift was influenced by the widening 2-year bund-Treasury yield spreads, reaching their highest point since July. The euro’s strength was partly attributed to comments made by ECB hawk Isabel Schnabel. Meanwhile, the Japanese yen faced broad selling pressure as Japanese data revealed a mere 1.2% rise in regular wages and a 3.0% year-on-year decline in real wages for November. This decline underscores persistent inflation concerns and a lack of domestic demand-driven wage growth, aligning with the Bank of Japan’s reluctance to end negative rates.

As the Japanese household spending continued to plummet, acting as a drag on growth and reinforcing disinflation in the December Tokyo CPI report, the BoJ governor expressed a cautious approach towards unwinding ultra-loose monetary policies. In contrast, the U.S. market anticipates the CPI report, assessing the likelihood of a soft landing and potential cuts to the Fed’s 5.5% policy rate compared to the BoJ’s -0.1% rate. The accommodative BoJ policies contributed to the Nikkei 225 reaching its highest point since the 1990s bubble, fostering risk-on sentiment and positively correlating with the rise of USD/JPY towards the key resistance. Meanwhile, EUR/USD showed a 0.34% increase, approaching the 10-day moving average but staying within the range set by Friday’s U.S. jobs data. ECB policymakers highlighted a tepid economic recovery outlook in the eurozone, anticipating a recession in late 2023, driven by concerns about the German property market and supply chain risks. Sterling saw a 0.24% rise, supported by higher gilts-Treasury yield spreads, despite remaining below the November and December highs, as the BoE’s 2024 rate cuts priced roughly 30bp less than those for the Fed.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Gains Ground Amidst Greenback’s Downside Pressure and Market Optimism

In response to a renewed downside bias in the greenback, EUR/USD rebounded, reaching two-day highs in the 1.0965/70 range. The firm optimism in the risk space on Wednesday contributed to the climb, as the USD Index (DXY) faced pressure, retreating to the 102.30 region. Factors such as the absence of clear direction in US yields, an uptick in Germany’s 10-year bund yields, and prevailing risk-on sentiment influenced the pair’s daily movement. Despite a lack of clarity in US yields and rising 10-year bund yields, the focus now shifts to the upcoming US inflation readings, set to be a crucial driver for the dollar’s price action, considering the Federal Reserve’s potential interest rate reductions in the second quarter. Conversely, comments from ECB’s De Guindos and Schnabel regarding a soft landing in the Eurozone’s economy and a reachable inflation target in 2025 had limited impact on the pair. Suggestions of premature interest rate cuts by the ECB, despite speculations of potential reductions, did not significantly sway the market.

On Wednesday, the EUR/USD moved slightly higher and reached the upper band of the Bollinger Bands. Currently, the price moving just around the upper band, suggesting another potential upward movement. Notably, the Relative Strength Index (RSI) maintains its position at 59, signaling a neutral but bullish outlook for this currency pair.

Resistance: 1.1000, 1.1068

Support: 1.0950, 1.0892

XAU/USD (4 Hours)

XAU/USD Hovers as Investors Await Key CPI Data Amidst Lethargic Trading

Gold (XAU/USD) continues to tread familiar levels, showing limited movement amid a cautious market environment marked by a sparse macroeconomic calendar. The precious metal recently touched a weekly low at $2,016.61 and faces support at various levels. As Wall Street maintains a positive but uneventful stance, anticipation builds for the upcoming release of the December Consumer Price Index (CPI) in the United States. Analysts predict a 3.2% annualized increase, with a potential impact on the US Federal Reserve’s rate-cutting decisions. The gold market remains on edge, awaiting CPI readings that could influence sentiment and guide the trajectory of the US Dollar in the coming days.

On Wednesday, XAU/USD moved lower and was able to reach the lower band of the Bollinger Bands. Currently, the price moving higher and trying to reach the middle band. The Relative Strength Index (RSI) stands at 45, signaling a neutral outlook for this pair.

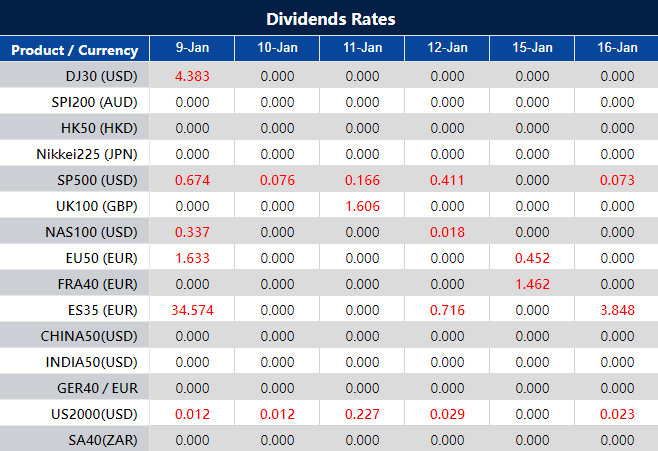

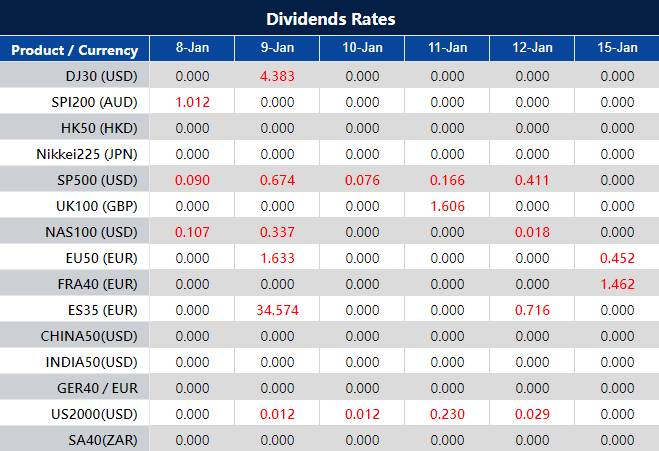

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

Tuesday witnessed a rollercoaster ride in the stock market as the S&P 500 and Dow Jones ended with declines while the Nasdaq managed a slight gain, primarily propelled by tech stocks’ resurgence. Despite the market’s recovery, with notable companies like Nvidia and Amazon showing gains, uncertainties loom as investors brace for crucial inflation data and upcoming earnings reports from major corporations. Simultaneously, the currency market saw the US Dollar Index surge, impacting major pairs such as EUR/USD, GBP/USD, USD/JPY, AUD/USD, and USD/CAD, while precious metals faced headwinds amidst dollar demand and market uncertainties.

Stock Market Updates

The stock market on Tuesday experienced a fluctuating day, with the S&P 500 initially dropping but later recuperating slightly thanks to a surge in tech stocks. Despite this rebound, the S&P 500 closed with a 0.15% decrease at 4,756.50, following a volatile day where it had plunged by 0.7% at its lowest point. Similarly, the Dow Jones Industrial Average ended down by 0.42%, recovering from a 310-point deficit earlier in the session. Conversely, the Nasdaq Composite managed to reverse a 0.9% decline, finishing with a marginal gain of 0.09% at 14,857.71. Notably, Nvidia and Amazon both saw gains of over 1.5%, with Juniper Networks surging by almost 22% due to potential acquisition news by Hewlett Packard Enterprise.

Tech stocks, which had been performing strongly in 2023, faced challenges at the beginning of 2024, impacting the broader market. Despite this setback, healthcare emerged as one of the day’s winners, marking a 3% increase for the year and ranking as the top-performing sector. The recent market movements followed a positive session on Monday, where both the S&P 500 and Nasdaq Composite rebounded, particularly driven by the recovery of mega-cap tech stocks after previous declines. Looking ahead, investors await crucial inflation data later in the week, expecting insight into potential Federal Reserve rate adjustments. Additionally, significant companies like Infosys, JPMorgan Chase, UnitedHealth, Bank of America, and Delta Air Lines are scheduled to report earnings, contributing to market sentiment and direction.

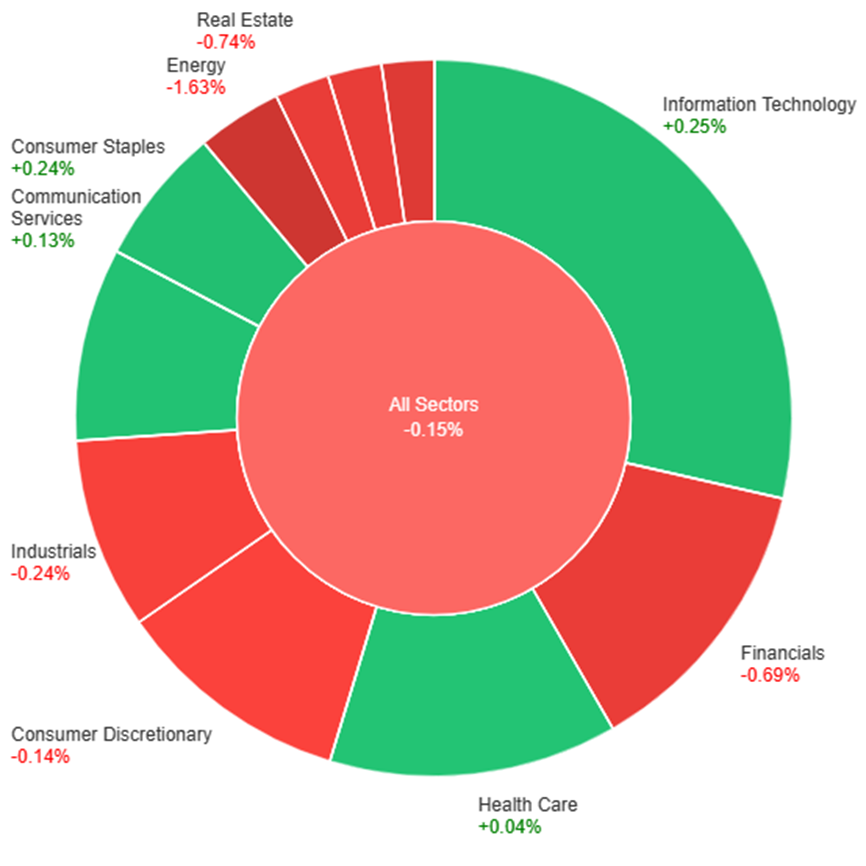

On Tuesday, the overall market experienced a slight decrease of 0.15%. However, there were sectoral variations, with Information Technology (+0.25%), Consumer Staples (+0.24%), and Communication Services (+0.13%) showing modest gains. Health Care (+0.04%) also saw a marginal increase. Conversely, Consumer Discretionary (-0.14%), Industrials (-0.24%), Financials (-0.69%), Real Estate (-0.74%), Utilities (-0.76%), Materials (-1.10%), and Energy (-1.63%) sectors faced declines, with Energy and Materials exhibiting the most significant decreases among the sectors.

Currency Market Updates

In the currency market, the US Dollar Index (DXY) surged to two-day highs, hitting the 102.70 zone, buoyed by increased demand for the greenback despite the lack of clear direction in US yields. This propelled EUR/USD downwards, nearly touching the critical support level of 1.0900 as the dollar gained traction alongside safe-haven assets. GBP/USD also faced downward pressure, slipping below 1.2700 and reversing gains from earlier in the week. Conversely, USD/JPY saw a notable recovery, surpassing the key barrier at 144.00 after consecutive sessions of losses, driven by inconclusive movements in US yields and a dip in JGB 10-year yields. Meanwhile, AUD/USD experienced a sharp decline to the 0.6680/75 region following two days of slight gains, ahead of the release of pivotal inflation data in Australia.

Additionally, the robust performance of the greenback pushed USD/CAD to fresh four-week highs beyond 1.3400 amid weak results in Canadian trade balance and building permits, sustaining selling pressure on the Canadian dollar. Precious metals faced headwinds as gold closed around $2030 per troy ounce due to heightened demand for the dollar and uncertain sentiments in US money markets. Silver prices echoed this trend, grappling with the significant $23.00 mark as they continued a negative trend from the beginning of the week. The currency market witnessed a shift in dynamics driven by the dollar’s resurgence, impacting major pairs and commodities alike as traders closely monitored key economic data releases and fluctuations in yields.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Reversal and Dollar Strength Amidst Economic Indicators

The EUR/USD pair retreated from early-week gains, hovering near 1.0900 amidst a stronger USD Index reaching 102.70. Market caution ahead of US inflation data and consumer sentiment reports contributed to the dollar’s uptick. The pair’s movement was influenced by mixed US yield trends and divergent central bank policies, with the ECB possibly eyeing rate cuts while the Fed leans toward reductions. Germany’s disappointing industrial production and an unexpected jobless rate improvement in the broader Eurozone added to the euro’s bearish sentiment, shaping the currency pair’s recent downturn.

On Tuesday, the EUR/USD moved slightly lower and reached the lower band of the Bollinger Bands. Currently, the price moving just below the middle band, suggesting a potential upward movement. Notably, the Relative Strength Index (RSI) maintains its position at 44, signaling a neutral outlook for this currency pair.

Resistance: 1.0980, 1.1068

Support: 1.0892, 1.0814

XAU/USD (4 Hours)

XAU/USD Treads Cautiously Amidst Economic Uncertainty and Fed Rate Expectations

Spot gold, reflected by XAU/USD, remains within familiar ranges, lingering at the lower end of Monday’s spectrum. The US Dollar gains momentum amid a gloomy market sentiment as stocks dip, while anticipation builds for key macroeconomic indicators. Market optimism regarding a potential Fed interest rate trim awaits validation from forthcoming Consumer Price Index (CPI) figures. Recent employment data signaling a tight labor market raises concerns about potential inflationary pressures, posing a dilemma for the Fed’s tightening policy. With rates at multi-year highs, there’s a looming risk of an economic setback, prompting speculation on potential rate cuts as early as March. Amidst this backdrop, the surge in US Treasury yields further bolsters the USD, creating a cautious atmosphere for gold traders.

On Tuesday, XAU/USD moved lower and moving between the middle and lower bands of the Bollinger Bands. Currently, the price moving higher and trying to reach the middle band. The Relative Strength Index (RSI) stands at 42, signaling a neutral outlook for this pair.

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

The stock market rallied strongly, particularly in the tech sector, with the S&P 500 rising by 1.41% and the Nasdaq Composite surging 2.2%, rebounding from a challenging prior week. Notable tech giants like Nvidia, Amazon, Alphabet, and Apple experienced gains, fueling investor confidence. However, Boeing’s 8% stumble due to 737 Max 9 inspections impacted the Dow Jones Industrial Average. As traders anticipate crucial data releases, including CPI and PPI, this week, the focus shifts to the Fed’s inflation control measures and their influence on market sentiment. The currency market saw varied movements, with the USD index declining slightly, affecting currency pairs differently, as the EUR/USD and GBP/USD surged, while USD/JPY and USD/CAD faced challenges. Precious metals like Gold dipped amid a reassessment of Fed policies, contrasting with Silver’s rebound.

Stock Market Updates

The stock market witnessed a significant rebound on Monday as major indices surged, led by a robust performance in the technology sector. The S&P 500 rallied by 1.41% to close at 4,763.54, and the Nasdaq Composite surged by 2.2%, reaching 14,843.77, marking its most impressive day since mid-November. Investors displayed renewed confidence in tech companies after a challenging prior week that saw a 4% decline in the sector, primarily driven by falling yields. Notable tech giants like Nvidia, Amazon, Alphabet, and Apple experienced notable gains, with Nvidia hitting an all-time high, Amazon climbing nearly 2.7%, Alphabet advancing 2.3%, and Apple rising by 2.4% post an Evercore ISI recommendation to buy the recent dip. The VanEck Semiconductor ETF (SMH) also surged by 3.5%, its most robust performance since November, further indicating a broader tech resurgence. However, Boeing’s shares tumbled by 8% due to the temporary grounding of Boeing 737 Max 9 planes for inspections after an Alaska Airlines fuselage incident, impacting the Dow Jones Industrial Average, which managed a 0.58% increase at the close.

Last week marked the market’s first downturn in ten weeks, primarily influenced by underperforming mega-cap tech stocks like Apple and rising Treasury yields, resulting in a 0.59% slide in the Dow, a 1.52% drop in the S&P 500, and the Nasdaq Composite witnessing its worst weekly performance since September with a 3.25% decline. As the new week progresses, traders are eagerly anticipating upcoming data releases, particularly the December consumer price index and the producer price index scheduled for Thursday and Friday, respectively. These crucial figures are expected to shed light on the Federal Reserve’s potential moves regarding interest rates, offering insights into the efficacy of their measures in reining in inflation towards the 2% target. This information could significantly influence market sentiment and trading strategies in the days ahead.

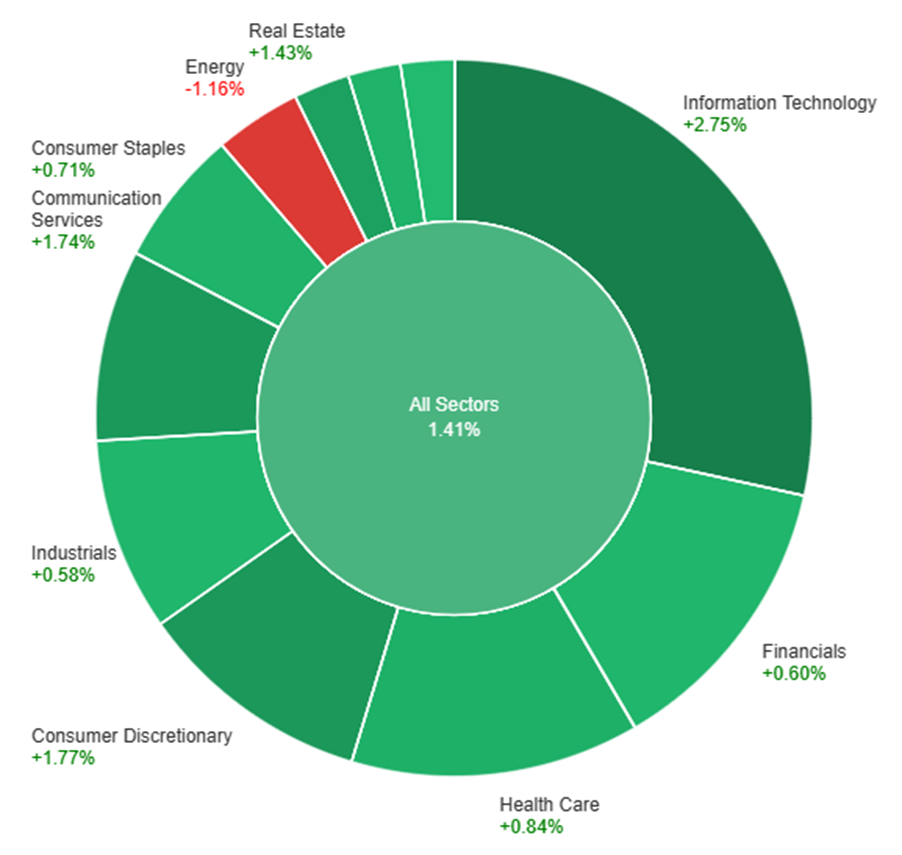

On Monday, the market saw an overall positive trend across various sectors, with a 1.41% increase across all sectors. Information Technology experienced the most significant surge at 2.75%, followed by Consumer Discretionary and Communication Services with gains of 1.77% and 1.74%, respectively. Real Estate and Health Care also showed notable growth, rising by 1.43% and 0.84%, respectively. However, Energy exhibited a decline of 1.16%, while Utilities, Consumer Staples, Financials, Industrials, and Materials sectors saw more modest increases ranging from 0.41% to 0.72%.

Currency Market Updates

The currency market exhibited varied movements amidst a shifting landscape of global economic sentiments. The US Dollar Index (DXY) saw a modest decline, hovering just above the 102.00 threshold as investors favored riskier assets and US yields underwent a corrective downturn. This decline in the dollar bolstered the performance of several currency pairs, notably the EUR/USD, which made significant gains reaching around 1.0980. Factors contributing to this uptick included a marginal increase in Investor Confidence tracked by the Sentix Index and better-than-expected Retail Sales figures in the eurozone. Similarly, GBP/USD continued its bullish trajectory for the fourth consecutive session, surging past the 1.2700 mark, largely supported by positive risk sentiment.

Conversely, the USD/JPY pair experienced a daily pullback to the 143.60 region due to declining US yields and a temporary weakening of the greenback, yet it managed to recover and surpass the 144.00 hurdle by the end of the North American session. AUD/USD showcased resilience by regaining the 0.6700 level, despite the broader bearish performance in the commodity market. However, USD/CAD faced challenges to maintain momentum beyond 1.3400, eventually retreating to the mid-1.3300s amidst a consolidative market environment. Amidst these currency fluctuations, precious metals like Gold saw a retreat to three-week lows, approximately $2015 per troy ounce, influenced by traders reassessing the potential for a prolonged restrictive stance by the Fed, especially in light of December’s Non-Farm Payrolls (NFP) data. In a similar vein, Silver rebounded from two consecutive sessions of losses, yet remained below the $23.00 mark.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Gains Ground Amidst USD Index Decline and Fed Rate Cut Speculation

EUR/USD saw a promising rise early in the week, reaching around 1.0975/80 against a weakening USD Index (DXY), sparked by uncertainties despite strong December Payrolls. Investor demand for bonds drove yields down on both sides of the Atlantic, slightly dimming the optimistic start to the trading year. The market’s focus remains on the Federal Reserve’s potential rate cuts versus the more restrained stance of the ECB, with consensus leaning towards a later rate cut by the ECB. Factors contributing to the euro’s strength included an uptick in Investor Confidence and stable Consumer Confidence, while Retail Sales in the bloc showed a slight contraction.

On Monday, the EUR/USD moved slightly higher and reached the upper band of the Bollinger Bands. Currently, the price moving just below the upper band, suggesting a potential downward movement. Notably, the Relative Strength Index (RSI) maintains its position at 51, signaling a neutral outlook for this currency pair.

Resistance: 1.0980, 1.1068

Support: 1.0892, 1.0814

XAU/USD (4 Hours)

XAU/USD Finds Support Amid Dollar Weakness and Fed Speculation

During American trading, XAU/USD managed to recover from early losses, hovering around $2,030 per ounce after hitting a mid-December low of $2,016.61. The weakening US Dollar spurred this turnaround, fueled by market optimism driven by expectations of a potential Federal Reserve rate cut in March. Additionally, Bank of America analysts’ predictions of a tapering in Treasury holdings by the Fed further influenced the market sentiment. As government bond yields dipped and stock indexes fluctuated, attention turned to the upcoming US inflation update, with the December Consumer Price Index anticipated to show a 3.2% YoY increase, potentially impacting the future trajectory of gold prices.

On Monday, XAU/USD moved lower and reached the lower band of the Bollinger Bands. Currently, the price moving higher and trying to reach the middle band. The Relative Strength Index (RSI) stands at 42, signaling a neutral but bearish outlook for this pair.

Renowned investor Warren Buffett, ranked as the fourth wealthiest person globally, boasts a net worth of approximately $120 billion.

His strategic prowess lies in his distinctive position sizing approach, emphasising concentration within a margin of safety.

Unlike conventional diversification, Buffett’s strategy involves substantial investments in a select few stocks with robust fundamentals—a testament to his confidence in their quality.

While this approach thrives in stable markets, the dynamics shift when engaging in faster-moving arenas like day trading or currency trading. For investors navigating these volatile markets, the question becomes: What position sizing strategy best aligns with the rapid pace and unpredictability of dynamic trading?

In this article, we’ll unravel the intricacies of position sizing tailored for such scenarios, offering practical insights to empower traders in the dynamic world of Forex.

What is Position Sizing?

Think of position sizing as deciding how much of your money to put into a single trade. It’s like choosing the right portion size for your meal – not too much that it overwhelms you, but enough to satisfy your appetite. In trading, it’s about finding the sweet spot that balances making gains and avoiding big losses, all based on your comfort level with risk.

Now, let’s clear up a common mix-up between position sizing and leverage. Position sizing is about determining how much of a particular asset you’re buying or selling, usually as a percentage of your total funds.

On the other hand, leverage involves borrowing money to increase the size of your trade. They’re related but different – it’s like deciding how much dessert (position sizing) you want, versus sharing it with a friend (leverage).

How position sizing shapes your strategy?

1. Risk Control: Position sizing helps you control how much you’re willing to risk on each trade. It’s like setting a limit on your spending to avoid blowing your budget.

2. Portfolio Management: Just like you diversify your meals for a balanced diet, position sizing lets you spread your money across different trades, reducing the impact of a bad outcome on your overall portfolio.

3. Psychological Impact: Imagine if your plate is too full – overwhelming, right? Well-sized positions relieve stress, helping you stay cool-headed and stick to your plan, avoiding impulsive decisions.

In a nutshell, understanding position sizing is like being a smart eater in the trading world. It’s about choosing your portions wisely, avoiding unnecessary risks, and making sure your overall trading strategy stays healthy and satisfying.

Calculating Position Size

Understanding how to calculate the right position size involves a straightforward formula that considers two crucial factors:

Risk per Trade: This is like deciding how much you’re willing to spend on a single item during your shopping spree. It sets a limit on how much you’re willing to lose in a single trade.

Stop-Loss Placement: Think of this as a safety net. Just like placing fragile items securely in your shopping cart, setting a stop-loss helps protect your investment by defining the point at which you’ll exit a trade to limit losses.

Let’s delve into a real-world scenario to bring the position sizing formula to life. Suppose you have $1,000 as your trading capital, and you’ve decided to risk 2% of that on a single trade.

1. Risk per Trade Calculation: 2% of $1,000 is $20. This means you’re willing to risk $20 on this particular trade.

2. Stop-Loss Placement: With your $20 risk in mind, you set a stop-loss order at a level that, if reached, would result in a $20 loss.

3. Optimal Position Size Calculation: Now, considering the risk and your stop-loss, you can calculate the optimal position size. Let’s say your chosen currency pair has a pip value of $0.10. With a $20 risk and a $0.10 pip value, your optimal position size would be $20 / $0.10 = 200 pips.

This practical example demonstrates how the formula translates into actionable steps. By aligning your risk tolerance (2% of your capital) with a well-placed stop-loss, you can precisely determine the position size (200 pips) that ensures your trade aligns with your overall strategy.

Much like adjusting your shopping budget based on your available funds, adapting your position size to your account size is key. As your account balance fluctuates, so should your position size. This dynamic approach ensures that you’re not overcommitting when funds are limited or missing out on opportunities when your account size grows.

Risk Tolerance and Position Sizing

Forex trading requires a clear understanding of your individual comfort level with risk. Similar to gauging the thrill you seek during an adventurous activity, assessing your personal risk tolerance is about evaluating the financial excitement you can comfortably navigate without losing sleep at night.

It involves a thoughtful examination of your willingness to embrace risk, ensuring that your trading endeavours align with your financial and emotional well-being.

Once you’ve gauged your risk tolerance, the next step is to align your position size with it. Well-calibrated position sizes help you maintain composure, make rational decisions, and avoid emotional reactions to market fluctuations.

Utilising the 1-2% Rule

Exploring the dynamics of Forex trading requires implementing robust risk management strategies. Among these strategies, the 1-2% rule stands out as a widely acknowledged approach designed to safeguard your capital amidst market uncertainties. Understanding the 1-2% rule is fundamental for traders seeking stability in their financial endeavours.

Once introduced to the 1-2% rule, the logical next step is applying it to position sizing. Imagine it as incorporating safety protocols into your adventure gear – ensuring your equipment is in sync with the demands of your journey.

In Forex trading, aligning your position size with the 1-2% rule becomes a fundamental practice, allowing you to control risk while positioning yourself for potential growth.

Let’s put theory into practice with real-world examples to illustrate the impact of the 1-2% rule. Consider a scenario where your trading capital is $5,000. Following the rule, you’d limit your risk to 1-2%, translating to a risk of $50 to $100 per trade. These examples provide tangible insights into how the 1-2% rule can be applied, demonstrating its practicality in preserving capital and fostering a disciplined trading approach.

Practical Tips for Effective Position Sizing

Regularly Reassess Your Risk Tolerance: Keep your trading strategy in sync with your risk tolerance by regularly reassessing it. Think of it as checking your financial health before diving into the market – a crucial step to align your positions with your comfort level.

Stay Informed About Market Conditions: Position sizing isn’t static; it adapts to market shifts. Stay informed about market dynamics, just like checking the weather before planning an event. This awareness allows you to adjust your positions, ensuring they match the evolving market landscape.

Harness Risk Management Tools: Trading platforms offer tools for a reason. Use them as your safety net in the unpredictable trading world. These tools provide insights, help control risk, and maintain discipline. Integrating them into your strategy enhances your risk management capabilities, ensuring a resilient and controlled trading experience.

In conclusion, mastering position sizing is essential for success in Forex trading. Understanding its principles, aligning with risk tolerance, and implementing practical strategies empowers investors to confidently navigate the dynamic Forex market. Consider it your indispensable guide to manoeuvring the complexities and achieving success in your trading journey.

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

Following a turbulent start to 2024, the upcoming week is poised for potential high volatility. Key drivers include the release of inflation data, taking in CPI figures from Australia, the US, and alongside PPI data. The UK GDP release also holds considerable significance, contributing to potential market impacts. Traders are advised to focus on monitoring this week’s CPI data, acknowledging its role as a primary market influencer for a successful trading week.

Australia Consumer Price Index (10 January 2024)

Registering a 4.9% increase in October 2023 (slightly down from September’s 5.6%), the Australian CPI is expected to further decrease to 4.4% in November 2023. Watch for the release on January 10, 2024.

US Consumer Price Index (11 January 2024)

In November 2023, US consumer prices edged up by 0.1% compared to the previous month, with an anticipated uptick of 0.2% expected in the December 2023 data. Keep an eye out for the release on January 11, 2024.

UK Gross Domestic Product (12 January 2024)

After contracting by 0.3% in October 2023, the UK GDP is anticipated to show growth of 0.2% in November 2023. Data is scheduled for release on January 12, 2024, following two months of consecutive growth.

US Producer Price Index (12 January 2024)

US producer prices remained unchanged in November 2023 after a 0.4% decline in the prior period. Anticipations for the December 2023 data, set to release on 12 January 2024, suggest a 0.1% increase.

{kind=link}