Stocks experienced a notable upswing on Wednesday as investors found hope in newly released data indicating the Federal Reserve’s potential to manage inflation without triggering a recession in the U.S. economy.

The S&P 500 reached its highest level of the year 2023, reflecting the overall positive sentiment in the market. Bank stocks, including Citigroup and Goldman Sachs, saw significant gains, contributing to the upward momentum.

Although the consumer price index for June rose 3% year-over-year, it fell slightly below economists’ expectations, while the core CPI, which excludes volatile food and energy prices, also rose less than anticipated.

While this was viewed as a positive sign, analysts emphasized that the Federal Reserve remains vigilant about areas such as service inflation, wage inflation, and housing inflation, which still persist at uncomfortably high levels.

Investors are closely watching both the consumer price index and the producer price index for insights into future interest rate adjustments by the Federal Reserve. The market currently indicates a strong probability of approximately 92% for a Fed interest rate increase during the July meeting.

As the economy continues to navigate the path of inflation, analysts remain cautiously optimistic, acknowledging that despite positive developments, the Federal Reserve’s decision to cut rates is not yet certain.

The market eagerly awaits the release of the upcoming producer price index data for June, which will provide further clarity on inflation trends and potentially impact the central bank’s future moves regarding interest rates.

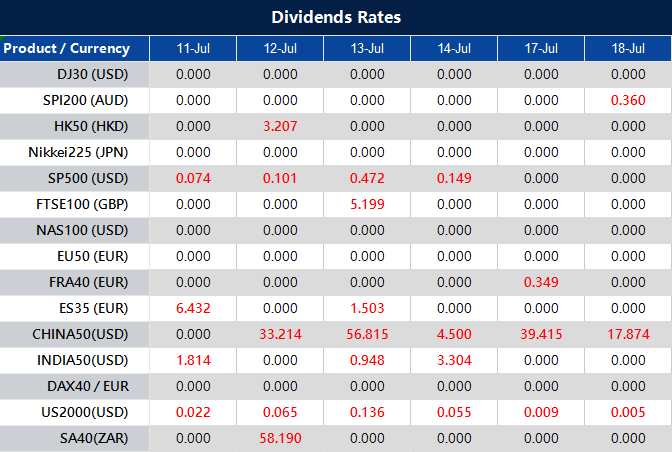

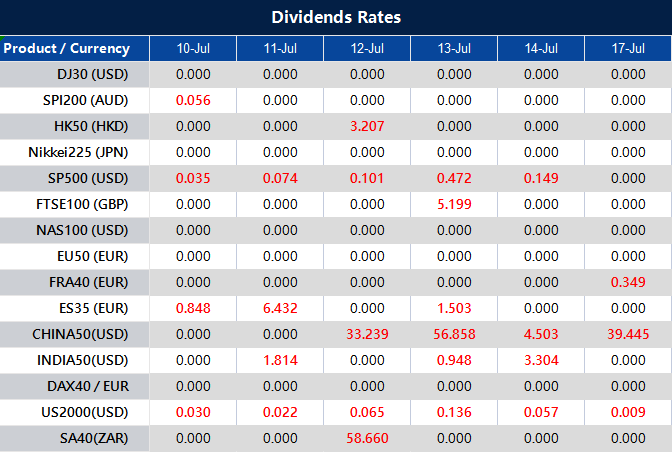

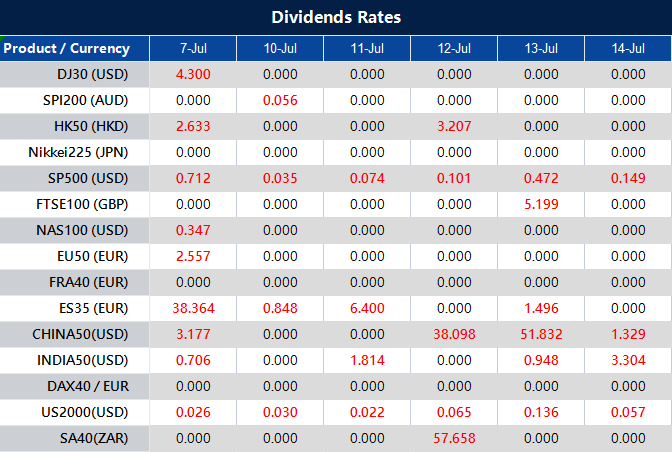

Data by Bloomberg

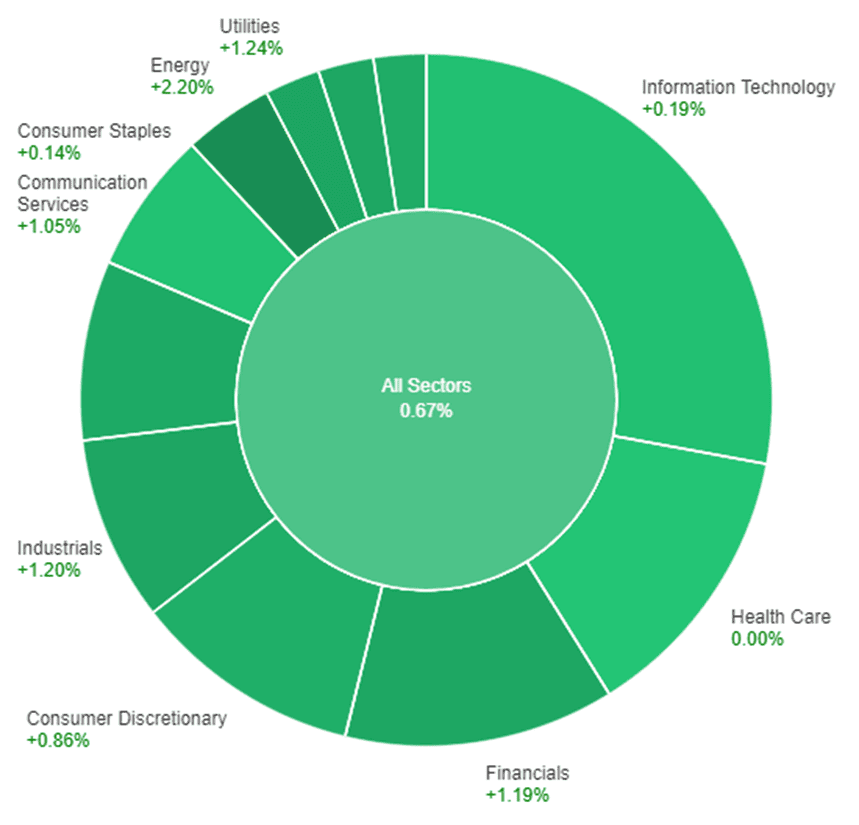

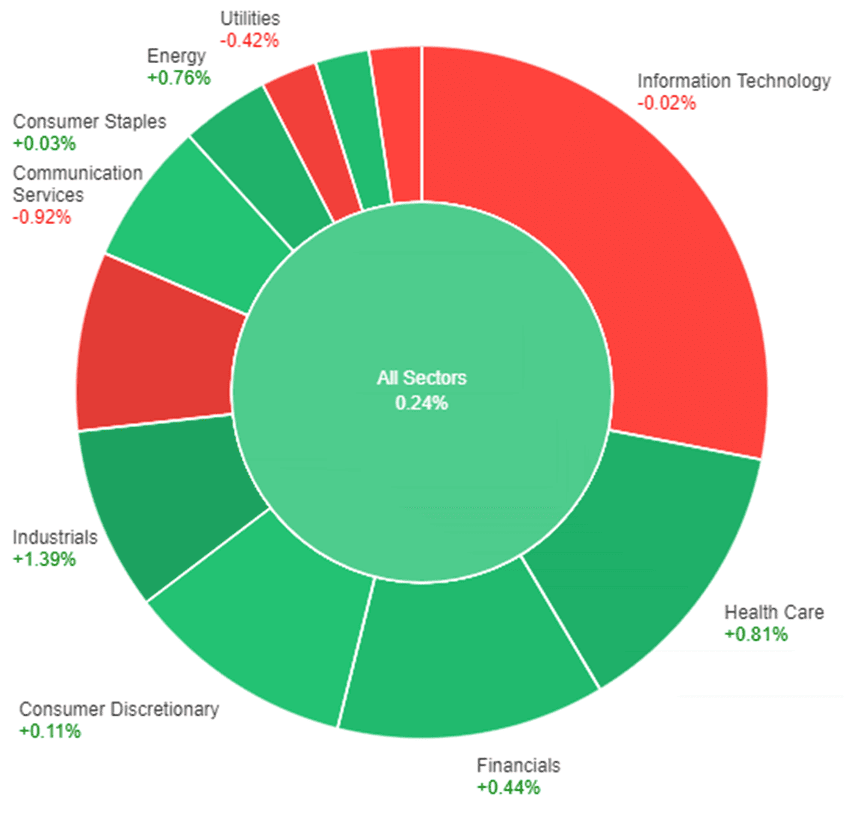

On Wednesday, the stock market showed positive performance across various sectors. The Communication Services sector saw the highest gain, rising by 1.51%, followed closely by Utilities with a 1.47% increase. Materials and Information Technology sectors also performed well, both gaining 1.29% and 1.25% respectively.

Consumer Discretionary and Energy sectors saw moderate gains of 0.96% and 0.90% respectively. Financials and Real Estate sectors experienced smaller increases of 0.63% and 0.44% respectively. Consumer Staples sector had a modest gain of 0.23%. However, Industrials and Health Care sectors faced slight declines, dropping by 0.20% and 0.28% respectively.

Major Pair Movement

On Wednesday, the U.S. dollar index dropped by 1% as the U.S. CPI data came in below expectations. This led to a significant decrease in Treasury yields and pushed the dollar below its prior lows for 2023. Two-year Treasury yields fell by 15 basis points, outpacing the 12 basis point drop in 10-year yields. This shift in yields suggests a potential signal that the Federal Reserve’s hiking cycle may be coming to an end.

The CPI data, along with a relatively positive beige book report, did not change the market’s expectation of a 25 basis point rate hike in July, which has been priced in since the Fed’s pause in June. However, it did reduce the likelihood of further tightening and increased expectations of rate cuts in 2024 by at least 150 basis points.

The euro to U.S. dollar exchange rate (EUR/USD) increased by 1.1% following a breakout above its prior peak for 2023. EUR/USD is approaching its pivotal 200-week moving average at 1.1183, but further disinflationary U.S. data and the Fed’s stance on 2024 rate cuts may impact its future movements.

The U.S. dollar to Japanese yen exchange rate (USD/JPY) fell by 1.47%, trading below June’s low. It briefly dipped below the 38.2% retracement level of its uptrend for 2023. While USD/JPY is oversold on daily studies, there is a possibility of a corrective bounce if it fails to indicate further decline and closes above 138.25.

The significant recovery of the yen could reduce the need for the Bank of Japan (BoJ) to raise its cap on 10-year JGB yields. As a result, pricing by the Fed and Treasury yields remain crucial factors. Sterling (GBP) rose by 0.44%, but its boost was smaller compared to EUR/USD, as it had already broken out above its prior peak for 2023 earlier in the week.

Picks of the Day Analysis

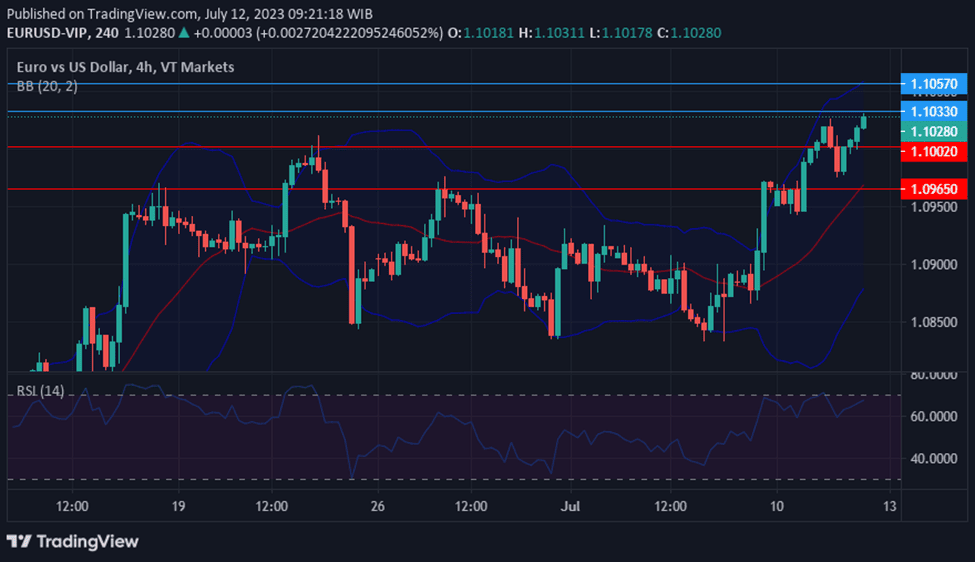

EUR/USD (4 Hours)

EUR/USD Surges on Weakening US Dollar Amidst Inflation Data, Awaited Economic Reports and Central Bank Minutes

The EUR/USD extended its upward momentum, driven by a sharp decline in the US Dollar following disappointing US inflation data. The pair reached monthly highs as Treasury yields dropped and stocks rallied on Wall Street, boosting risk sentiment.

Market participants anticipate the Federal Reserve’s rate hike in July, but the lower-than-expected inflation figures have sparked optimism that this could be the final increase. Traders are now eagerly awaiting the US Producer Price Index report and the European Commission’s economic forecast, Industrial Production data, and the release of the European Central Bank’s latest meeting minutes.

With ongoing volatility, the pair faces the potential for both continued gains and significant corrections.

According to technical analysis, the EUR/USD pair is experiencing an upward movement on Wednesday, pushing towards the upper band of the Bollinger Bands. Presently, the price is still near the upper bands of the Bollinger Bands, and the bands themselves indicate the potential for further upward movement.

This suggests that the price has the potential to reach the upper band of the Bollinger Bands. Additionally, the Relative Strength Index (RSI) is currently at 78, which is within the overbought area, indicating a bullish trend for the EUR/USD.

Resistance: 1.1185, 1.1271

Support: 1.1086, 1.0990

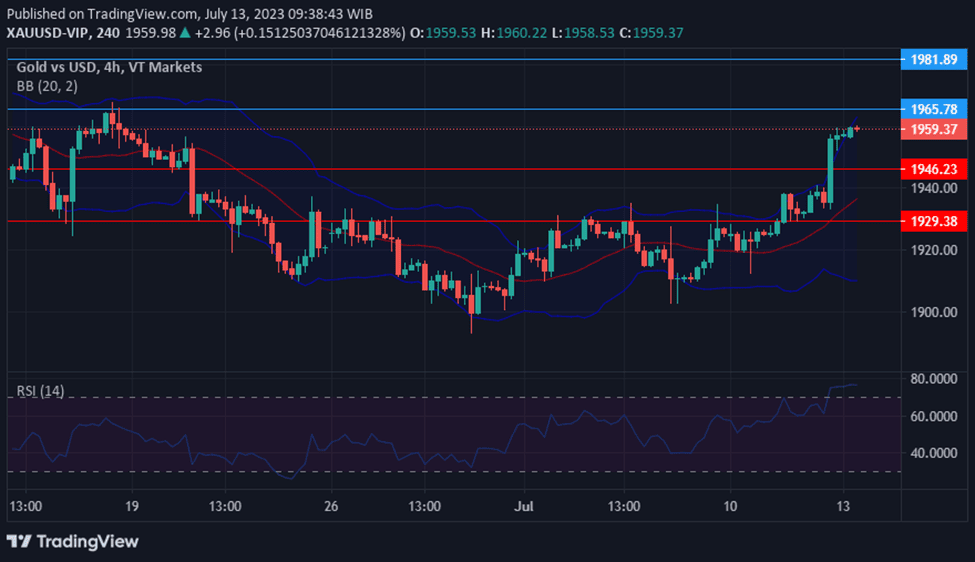

XAU/USD (4 Hours)

Gold (XAU/USD) Surges as Disappointing US Inflation Data Weighs on Dollar

XAU/USD experienced a strong rally, hitting an intraday high of $1,959.30 per troy ounce during the American session, as the US Dollar faltered due to lower-than-anticipated inflation figures. The Consumer Price Index (CPI) for June rose by a modest 0.2% month-on-month, falling short of the expected 0.3%, while the year-on-year CPI increase was 3%.

Additionally, the core annual reading came in at 4.8%, both below forecasts, indicating a continued easing of price pressures. This development bolstered risk appetite, leading to a surge in global stocks and further weakening of the US Dollar across foreign exchange markets.

The prospect of a potential shift in the Federal Reserve’s tightening cycle gained traction, suggesting a potential easing or conclusion of rate hikes, which could potentially mitigate the risk of a severe recession in the United States.

According to technical analysis, the XAU/USD pair underwent an upward movement on Wednesday, pushing towards the upper band of the Bollinger Bands. Currently, the price is close to the upper bands of the Bollinger Bands, and the bands themselves suggest the possibility of further upward movement.

This indicates the potential for the price to reach the upper band of the Bollinger Bands. Furthermore, the Relative Strength Index (RSI) is currently at 76, within the overbought area, indicating a bullish trend for the XAU/USD.

Resistance: $1,965, $1,981

Support: $1,946, $1,929

Economic Data

| Currency | Data | Time (GMT + 8) | Forecast |

|---|---|---|---|

| GBP | Gross Domestic Product m/m | 14:00 | -0.3% |

| USD | Unemployment Claims | 20:30 | 251K |

| USD | Producer Price Index m/m | 20:30 | 0.2% |

| USD | Core Producer Price Index m/m | 20:30 | 0.2% |

Start trading now — click here to create your live VT Markets account.