In a turbulent market session, the Nasdaq Composite entered correction territory, partly driven by Meta’s underwhelming forecast, and Alphabet’s disappointing results added to the pressure. The S&P 500 briefly touched correction territory, and Wall Street grappled with concerns about the US economy’s outlook. Meanwhile, the US dollar displayed resilience on the back of strong Q3 GDP growth. In the currency market, the dollar saw fluctuations as the Federal Reserve and European Central Bank were expected to make rate decisions. The Japanese yen faced the risk of intervention from the Ministry of Finance. The British pound and Australian dollar saw rebounds. Upcoming economic data releases are poised to continue influencing market dynamics.

Stock Market Updates

The Nasdaq Composite extended its decline into correction territory as Meta, the parent company of Facebook, reported a forecast that fell short of investors’ expectations. The tech-heavy index dropped by 1.76% on Thursday, closing at 12,595.61, falling below its 200-day moving average. The S&P 500 also dipped 1.18% to close at 4,137.23, with the Dow Jones Industrial Average slipping 0.76%, shedding 251.63 points to end at 32,784.30. The S&P 500 briefly entered correction territory during the session, marking a nearly 10% decline from its peak in July. The Nasdaq Composite officially entered correction territory, down more than 10% from its yearly high. Wall Street seemed unimpressed with recent big-tech earnings reports, with concerns about the weakening outlook for the US economy. Meta reported a beat on both top and bottom lines in the third quarter but noted advertising softness and concerns about cost control, leading to a 3.7% drop in Meta’s shares.

This decline in the stock market was influenced by a challenging trading session on Wednesday, driven by a 9.5% decline in Google-parent Alphabet, which had its Class-A shares experience their worst day since March 2020 after disappointing results in the Google cloud unit. The market’s recent correction since the summer has been partly attributed to rising bond yields, with the 10-year Treasury yield crossing 5% earlier in the month. Despite a slight decrease in the 10-year yield to 4.84% on Thursday, it did not halt the market sell-off. The market also didn’t receive a boost from the stronger-than-expected third-quarter gross domestic product (GDP) report, with the US GDP growing at a 4.9% annualized rate from July through September, surpassing the 4.7% forecast by economists. Furthermore, major earnings reports are on the horizon, with Amazon scheduled to release its results after the market’s close.

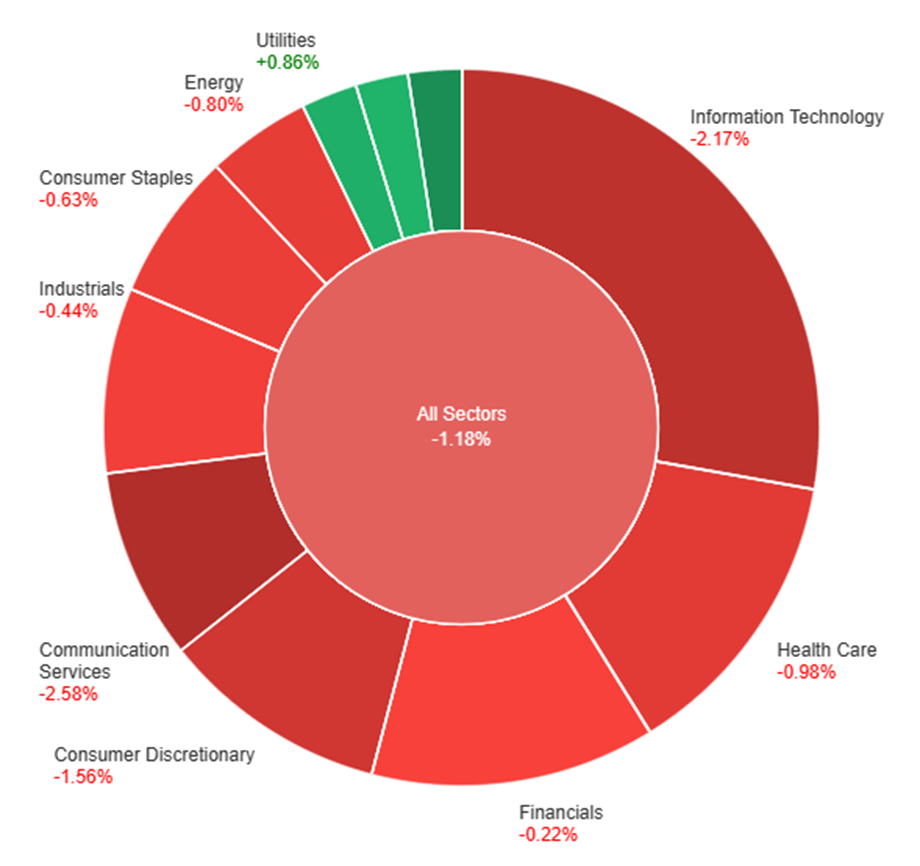

On Thursday, various sectors experienced fluctuating performance in the market. Real Estate and Utilities showed positive gains, with increases of 2.15% and 0.86%, respectively. However, Information Technology and Communication Services had a rough day, with notable declines of 2.17% and 2.58%. Overall, the broader market, represented by “All Sectors,” saw a decrease of 1.18%, while several sectors, including Consumer Discretionary, Health Care, and Consumer Staples, also ended in the red with declines ranging from 0.63% to 1.56%.

Currency Market Updates

In the latest currency market updates, the US dollar displayed resilience as it strengthened by 0.1%, despite a minor retreat in Treasury yields. This rally was prompted by robust US economic data, as Q3 GDP grew impressively at a 4.9% rate. However, the sales and core PCE figures fell short of expectations, with core PCE at 2.4% compared to 3.7% in the previous quarter. While September core capital goods orders exceeded forecasts, initial and continued jobless claims saw an increase, signaling potential challenges in finding new employment. Additionally, pending home sales surpassed expectations but remained notably weak. The EUR/USD pair experienced a 0.05% decline, with the dollar gaining momentum as both the Federal Reserve and the European Central Bank (ECB) were expected to cease their rate hikes and potentially cut rates by mid-year. The USD/JPY pair rose by 0.1%, although it had retreated from its 2023 highs at 150.78 due to a decline in Treasury yields and market concerns about the Bank of Japan’s future policy decisions. Despite these fluctuations, the main perceived risk in the currency market is the possibility of the Ministry of Finance (MoF) resuming yen buying to prevent a breakout above 2022’s 32-year high at 151.94.

Meanwhile, the British pound saw a 0.2% increase in value after hitting its lowest level since October’s 1.2038 trend lows. This rebound came in the wake of a pullback in Treasury yields, despite concerning reports of CBI sales and reduced UK public inflation expectations. The Australian dollar also displayed resilience with a 0.3% increase, recovering from its lows in 2023. This recovery was attributed to a potential change in the Reserve Bank of Australia’s policy outlook.

Looking ahead, upcoming economic data releases include Tokyo core CPI for October, expected to remain steady at 2.5%, as well as German GDP and retail sales figures. Additionally, the US market will be closely monitoring data on personal income, spending, core PCE, and Michigan sentiment. These indicators will likely continue to influence the dynamics of the currency market in the days to come.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Finds Support Despite Dovish ECB Stance and Robust US Growth Data

The EUR/USD pair hit a bottom at 1.0521, aligning with the previous week’s lows. This drop came as the European Central Bank (ECB) adopted a more dovish stance, hinting at a possible terminal interest rate amidst economic concerns. Meanwhile, the US Dollar failed to capitalize on better-than-expected US GDP figures, as the Core PCE remained slightly below expectations and employment data raised concerns. Despite these dynamics, the fundamental factors suggest a mixed outlook for EUR/USD, with potential influences from upcoming US Core PCE data.

According to technical analysis, the EUR/USD consolidated on Thursday, approaching the middle band of the Bollinger Bands. Currently, the EUR/USD is trading between the middle and lower bands, indicating the potential for further downward movement. The Relative Strength Index (RSI) is at 43, signaling that the EUR/USD is adopting a bearish bias.

Resistance: 1.0616, 1.0705

Support: 1.0500, 1.0405

XAU/USD (4 Hours)

XAU/USD Resilient as Economic Uncertainties Persist Amid ECB and US GDP Reports

Spot Gold initially surged to $1,993.44 an ounce before receding, influenced by key developments in global economics. The European Central Bank opted to keep rates unchanged due to the Euro Zone’s economic struggles, while the US Dollar strengthened following a robust Q3 GDP report. The uncertain economic outlook drove investors to seek safety in Gold, contributing to its rebound as stock markets faced headwinds.

According to technical analysis, XAU/USD is consolidating on Thursday and has the potential to reach the upper band of the Bollinger Bands, which is currently squeezing. Presently, the price of gold is consolidating near the upper band, implying a possible downward consolidation. The Relative Strength Index (RSI) is currently at 57, indicating a neutral bias for the XAU/USD pair.

On Wednesday, the S&P 500 closed at 4,186.77, dipping below the critical 4,200 level, spurred by Alphabet’s disappointing earnings, tech stock declines, and rising bond yields. Microsoft bucked the trend with a 3% share price increase after strong earnings. Meanwhile, in the currency market, the US dollar gained ground due to higher Treasury yields, while major currencies like the euro and pound struggled. The yen faced a make-or-break moment against the dollar, and the Canadian dollar hit mid-March highs following the Bank of Canada’s cautious stance. Upcoming economic data releases and the ECB meeting are poised to impact the financial landscape further.

Stock Market Updates

On Wednesday, the S&P 500 experienced a significant decline, closing at 4,186.77, which was below a key level of 4,200. This drop of 1.43% marked the first time the S&P 500 had closed below this level since May, a development closely monitored by chart analysts. The downward trend was attributed to disappointing quarterly results from Alphabet, the parent company of Google, which saw its shares plummet more than 9% due to a miss in its cloud business performance, overshadowing otherwise strong revenue growth and earnings. The S&P 500’s communication services sector also took a hit, losing 5.9%. Other major tech giants, such as Apple and Amazon, saw their shares decline by 1.3% and 5.6%, respectively. Concerns also revolved around rising bond yields, with the 10-year Treasury yield spiking nearly 11 basis points to approximately 4.95%, causing jitters in the market and negatively impacting tech stocks.

Amid this turbulence, Microsoft stood out as an exception among tech stocks, experiencing a 3% increase in share prices after it posted fiscal first-quarter results that exceeded Wall Street expectations. Additionally, other tech firms like IBM and Meta were set to announce their quarterly results in the afternoon. So far, approximately 29% of S&P 500 companies have reported their third-quarter earnings and an impressive 78% of these companies have surpassed analysts’ expectations. While corporate earnings remained a focal point for investors, the bond market’s rapid rise in yields, not witnessed since 1982, raised concerns about the future of the stock market.

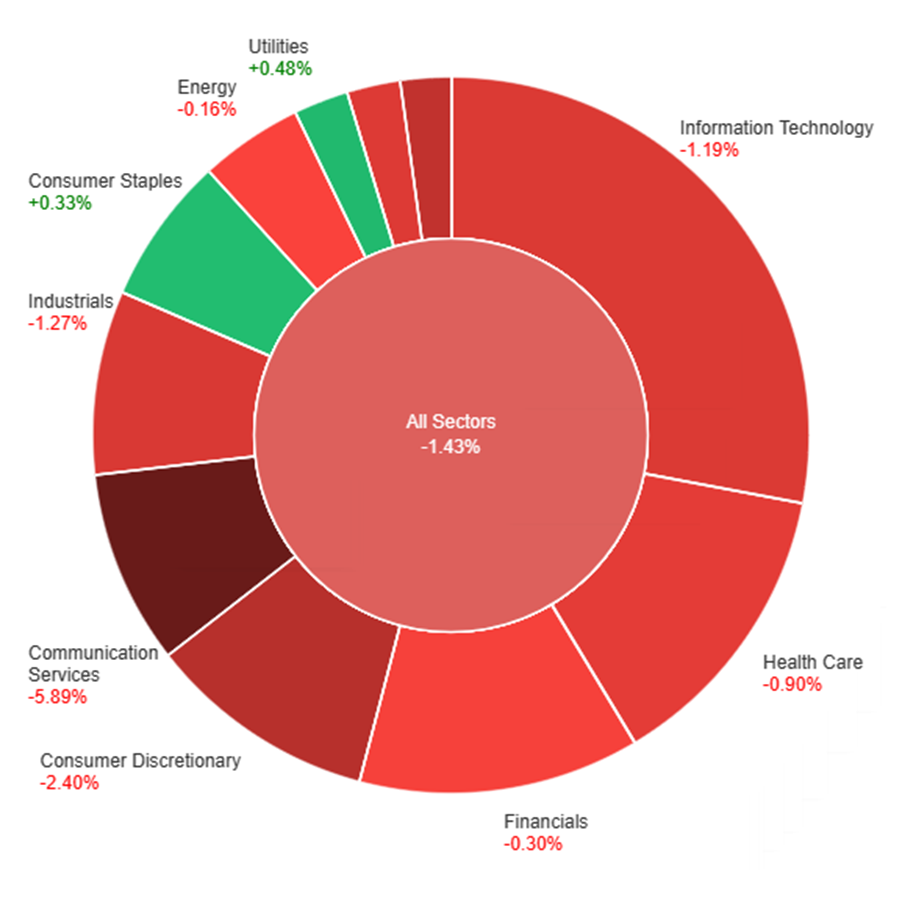

On Wednesday, various sectors experienced different changes in their stock market performance. Overall, the All Sectors index decreased by 1.43%. The sectors of Utilities and Consumer Staples showed modest gains, with increases of 0.48% and 0.33%, respectively. On the other hand, several sectors saw declines: Energy (-0.16%), Financials (-0.30%), Health Care (-0.90%), Materials (-1.14%), Information Technology (-1.19%), Industrials (-1.27%), Real Estate (-2.07%), Consumer Discretionary (-2.40%), and Communication Services (-5.89%) all faced negative returns.

Currency Market Updates

In the latest currency market updates, the US dollar saw a 0.2% rise, primarily driven by risk-off sentiment and higher Treasury yields when compared to the yields of bunds, gilts, and JGBs, which favored the safety of the US currency. Notably, the EUR/USD pair struggled to gain momentum despite better-than-expected German Ifo data and the lowest MBA mortgage purchase reading in the US since 1995. Weak lending data in the eurozone raised concerns of a looming recession, while the US exhibited a strong rebound. Additionally, falling US stocks, a return of 10-year Treasury yields towards the 5% mark, and increasing oil prices all contributed to the dollar’s strength, particularly against currencies sensitive to market risks. The pair, EUR/USD, dropped by 0.2%, reaching its lowest level since the previous Friday. This decline followed a significant bearish rejection from the 50% Fibonacci retracement level and the 55-day moving average resistance.

Furthermore, other major currencies were also impacted by the dollar’s resurgence. The British pound fell by 0.32%, with investors eagerly awaiting further UK inflation data that might confirm the Bank of England’s expectations of a significant year-end drop, potentially leading to interest rate cuts. USD/JPY briefly touched above the 150 mark for the third time in the current month, driven by the widening yield spreads between US Treasuries and Japanese government bonds (JGBs). The relatively shallow pullbacks observed in the market have placed the dollar in a critical make-or-break position, one that could challenge the Japanese Ministry of Finance’s tolerance for further yen depreciation towards the 32-year peak seen in 2022 at 151.94. Meanwhile, the Bank of Japan’s readiness to continue quantitative easing to defend its current 1% 10-year yield cap also remains a crucial factor. In contrast, the Australian dollar experienced a brief rally following unexpectedly strong Q3 inflation figures but subsequently dropped by 0.72% due to risk-off market flows. Lastly, the Chinese yuan depreciated by 0.24% as concerns about local and central government limitations on risk-taking activities overshadowed the effects of modest fiscal stimulus announcements. The USD/CAD pair rose by 0.4% to reach its highest level since mid-March, following the Bank of Canada’s decision to maintain its interest rates and express concerns about the narrowing path to avoid a recession, raising questions about the comparative hawkishness of the Bank of Canada versus the Federal Reserve’s policy pricing. This week’s agenda includes the ECB meeting, which is widely expected to maintain the status quo, followed by significant US economic data releases, such as durable goods, Q3 GDP figures, core PCE data, jobless claims, and pending home sales.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Slides Below 1.0600 as Strong US Dollar Dominates, Eyes on ECB and US Economic Data

The EUR/USD currency pair faced a second consecutive day of declines, dropping below the 1.0600 mark, driven by the strength of the US Dollar. Market attention now shifts to the European Central Bank’s (ECB) upcoming meeting and significant US economic data releases. Notably, the German IFO Business Survey displayed positive results, while the ECB is expected to maintain unchanged interest rates amid concerns about slowing inflation and subdued economic activity. Additionally, robust US economic data could further bolster the US Dollar, while any negative surprises may trigger a correction in the currency pair.

According to technical analysis, the EUR/USD moved lower on Wednesday, approaching the middle band of the Bollinger Bands. Currently, the EUR/USD is trading between the middle and lower bands, indicating the potential for further downward movement. The Relative Strength Index (RSI) is at 39, signaling that the EUR/USD is adopting a bearish bias.

Resistance: 1.0616, 1.0705

Support: 1.0500, 1.0405

XAU/USD (4 Hours)

XAU/USD Climbs to $1,982 as Markets Weigh Economic Outlook Amidst Earnings Season and Central Bank Decisions

In Wednesday’s trading, XAU/USD made gains, reaching approximately $1,982 per troy ounce. As financial markets closely observe Wall Street’s earnings reports, the focus is on the economic outlook leading up to pivotal events on Thursday. Anticipations of robust U.S. economic growth, potentially at an annualized rate of 4.2% for the third quarter, are raising questions about interest rates and the Federal Reserve’s stance. Simultaneously, the European Central Bank (ECB) is expected to maintain rates and adopt a cautious approach to future monetary policy. Earnings season is further impacting sentiment, with mixed results from major tech companies affecting stock indices, and rising government bond yields adding to market dynamics.

According to technical analysis, XAU/USD is consolidating on Wednesday and has the potential to reach the upper band of the Bollinger Bands, which is currently squeezing. Presently, the price of gold is consolidating near the upper band, implying a possible downward consolidation. The Relative Strength Index (RSI) is currently at 60, indicating a neutral bias for the XAU/USD pair.

Learn from the expert on most 6 crucial factors for successful Forex trading. Our expert will guide you how to analyze market factors to idenify trading opportunity and earn profit from those factors.

In a positive turn for the stock markets, Tuesday saw a surge driven by robust earnings reports, yet concerns linger over lofty tech valuations. Major companies like Coca-Cola and Spotify exceeded expectations, while General Motors faced challenges. David Bahnsen of Bahnsen Group emphasized worries about high-tech valuations. Meanwhile, the US dollar gained strength with a rebound in Treasury yields and strong US PMI data, impacting currency markets. The article highlights the potential impact of upcoming economic data and central bank meetings on the currency market.

Stock Market Updates

On Tuesday, stock markets saw positive gains driven by a fresh wave of earnings reports and cautious monitoring of Treasury yields. The Dow Jones Industrial Average rose by 204.97 points, a 0.62% increase, closing at 33,141.38. The S&P 500 followed suit, climbing by 0.73% to finish at 4,247.68, and the Nasdaq Composite experienced a significant 0.93% uptick, reaching a level of 13,139.87. Earnings reports from major companies were a key focus for investors, with Coca-Cola reporting earnings and revenue that surpassed estimates, leading to a 2.9% increase in its stock price. Similarly, Spotify experienced a notable 10% surge after surpassing expectations with its third-quarter results. On the other hand, General Motors’ shares declined by 2.3% as the company withdrew its full-year outlook due to increased costs attributed to strikes by the United Auto Workers union. Despite this setback, the automaker did manage to post better-than-expected third-quarter results. Several tech giants, including Alphabet and Microsoft, were scheduled to release their results after the market closed, with Amazon and Meta also set to report later in the week. Despite strong earnings, some experts like David Bahnsen, the chief investment officer at Bahnsen Group, cautioned that the lofty valuations of big tech companies remain a cause for concern, suggesting that the market may be pricing them for perfection.

The ongoing earnings season has been generally positive, with around 23% of S&P 500 companies already reporting their earnings, and a significant 77% of them surpassing analysts’ expectations, according to FactSet. Despite this favorable start, concerns persist about the high valuations of many tech companies. Bahnsen Group’s David Bahnsen emphasized that the current valuations of big tech firms are excessively high, even considering the recent stock price declines observed over the past few months. He expressed skepticism about the sustainability of such valuations, suggesting that this dynamic may not end well. A significant number of S&P 500 companies are yet to report their earnings for the week, totaling around 150, making it a pivotal period for investors as they continue to assess the overall health of the market.

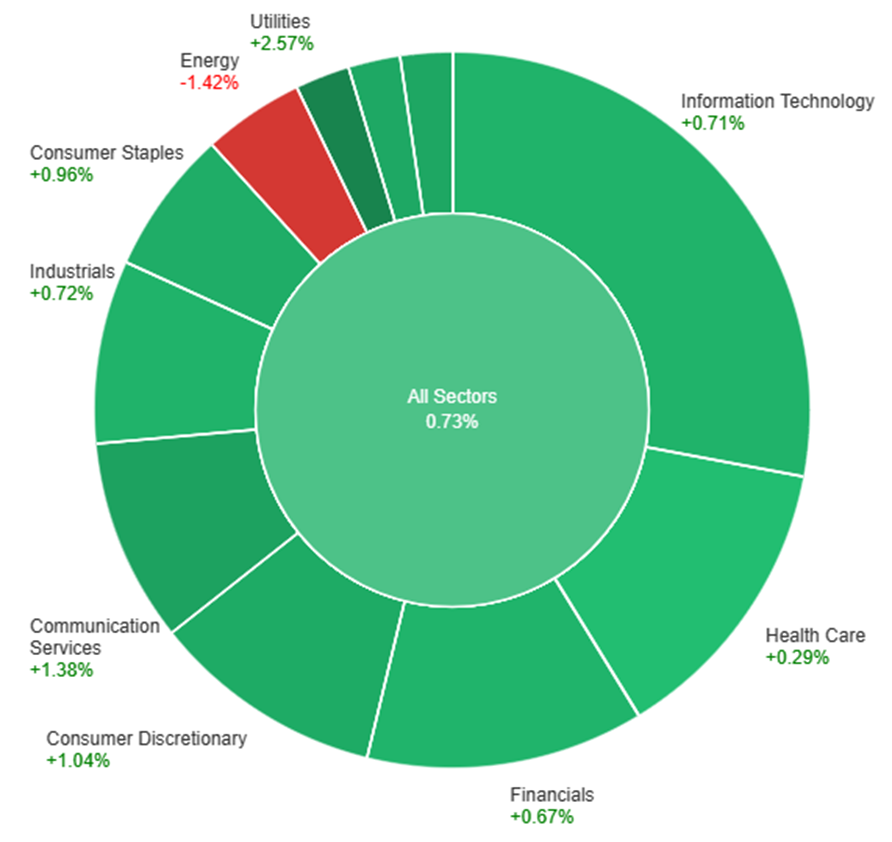

On Tuesday, across all sectors, the market saw a 0.73% increase in value. The top-performing sectors were Utilities, with a significant gain of 2.57%, followed by Communication Services at 1.38%, Real Estate at 1.19%, and Materials at 1.13%. Other sectors also showed positive performance, including Consumer Discretionary (1.04%), Consumer Staples (0.96%), Industrials (0.72%), Information Technology (0.71%), and Financials (0.67%). However, Health Care had a more modest increase at 0.29%, while Energy experienced a decline of -1.42% on that day.

Currency Market Updates

In the latest currency market updates, the US dollar exhibited strength, with the dollar index rising by 0.7%. This uptick was driven by a rebound in Treasury yields, following a setback on Monday, and positive flash US October PMI figures that exceeded expectations. In contrast, European and Japanese PMIs showed signs of deterioration, which put pressure on the euro. The EUR/USD pair fell by 0.74% as bund-Treasury yield spreads narrowed due to the divergence in PMIs. The potential reinforcement of this trend is anticipated with the release of US Q3 GDP data on Thursday, which is forecasted to be 4.3%. The article notes that the US dollar’s performance is also influenced by key economic data, with a focus on the European Central Bank (ECB) meeting on Thursday.

Additionally, the sterling weakened by 0.75%, primarily due to the drop in gilt-treasury yield spreads, which was accentuated by soft UK PMI data and reinforced by the view that the Bank of England’s rate hike cycle may be coming to an end. Meanwhile, the USD/JPY pair rose by 0.1%, but its upward momentum remained stalled near the 150 level. Despite a decline in 2-year Treasury-JGB yields, which was significant relative to last week’s peak, buyers are still attracted to the pair due to the substantial yield spread. However, the market remains cautious beyond the 150 level, fearing potential intervention by the Ministry of Finance (MoF) to support the yen. The article highlights that the currency market is keeping a close eye on these developments.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Surges to One-Month High as Weaker US Dollar Drives Momentum

The EUR/USD pair rallied significantly on Monday, breaking a downtrend line and reaching 1.0676, its highest level in a month, primarily due to a sharp decline in the US Dollar and improved market sentiment. As the Eurozone and the US prepare to release key PMI data and important monetary policy meetings are on the horizon, the Euro’s outlook remains favorable, though some consolidation may follow the 100-pip rally.

Based on technical analysis, the EUR/USD moved lower on Tuesday, pushing towards the middle band of the Bollinger Bands. Currently, the EUR/USD is trading just below the middle band, suggesting the potential for another push lower movement. The Relative Strength Index (RSI) stands at 49, indicating that the EUR/USD is back in neutral bias.

Resistance: 1.0616, 1.0705

Support: 1.0561, 1.0500

XAU/USD (4 Hours)

XAU/USD Slips as Resurgent US Dollar Overshadows Global Tensions

Gold prices faced downward pressure, with XAU/USD hitting an intraday low of $1,953.53 per troy ounce during London trading hours due to a resurgence in demand for the US Dollar. While global tensions simmered with delays in a ground incursion into the Gaza Strip and calls for a peaceful resolution, the Greenback gained strength, benefiting from positive US data and concerns about a steeper economic contraction in Europe, leading to a modest recovery after mid-day trading.

Based on technical analysis, XAU/USD is moving in consolidation on Tuesday and able to reach the middle band of the Bollinger Bands. Currently, the price of gold is moving just around the middle band, suggesting a possible continuation movement. The Relative Strength Index (RSI) currently registers at 58, indicating a neutral bias for the XAU/USD pair.

On Monday, the stock market witnessed mixed fortunes as the Nasdaq Composite edged higher while the Dow Jones and S&P 500 experienced declines, influenced by fluctuations in Treasury yields. The 10-year Treasury yield breached the 5% mark, sparking worries of further monetary tightening and its potential impact on the economy. As Wall Street endured a challenging week, major tech giants like Alphabet, Amazon, Meta, and Microsoft’s upcoming earnings reports were eagerly anticipated for insights into the market’s trajectory. Meanwhile, the currency market saw the US dollar weaken, the euro showing strength, and the British pound gaining ground, as expectations of central bank policies and upcoming economic data played a pivotal role in shaping market sentiment.

Stock Market Updates

On Monday, the Nasdaq Composite saw a slight increase in value as Treasury yields eased from their recent highs. Investors were eagerly anticipating the release of corporate earnings reports from tech industry giants. The Dow Jones Industrial Average, however, experienced a decline of 190.87 points, amounting to a 0.58% drop, closing at 32,936.41. The S&P 500 also dipped, falling by 0.17% to reach 4,217.04. In contrast, the Nasdaq Composite, known for its tech-heavy components, managed to gain 0.27%, concluding the session at 13,018.33. The benchmark 10-year Treasury note yield briefly exceeded the significant 5% level before slightly receding, ultimately settling at around 4.85%.

Interest rates have surged in recent weeks, with the 10-year Treasury yield surpassing the 5% threshold for the first time since July 2007. Federal Reserve Chair Jerome Powell’s comments suggested further monetary policy tightening, increasing investor concerns and contributing to the rise in Treasury yields. Some analysts predict that the benchmark yield may continue to rise. The rapid increase in yields has raised concerns about its impact on the economy, with Canaccord Genuity chief market strategist Tony Dwyer noting that it could accelerate an already weakening economic situation masked by higher rates. After a challenging week, which saw the S&P 500 ending 2.4% lower, the Dow Jones losing 1.6%, and the Nasdaq experienced its second consecutive weekly decline of 3.2%, Wall Street now awaits a series of major tech companies’ earnings reports, including Alphabet, Amazon, Meta, and Microsoft, which are expected to provide crucial insights for the stock market.

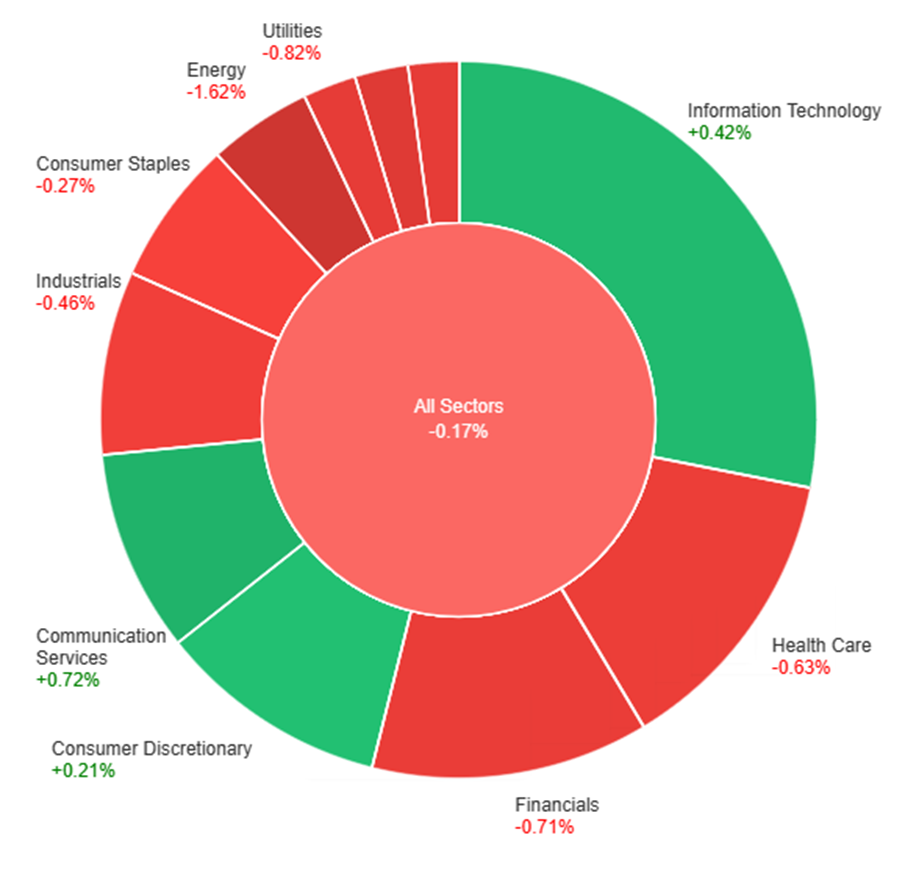

On Monday, the overall market experienced a slight decline, with a decrease of 0.17%. Among the individual sectors, there were variations in performance. Communication Services and Information Technology sectors saw gains of +0.72% and +0.42%, respectively. Consumer Discretionary also showed a modest increase of +0.21%. Conversely, Consumer Staples and Industrials experienced declines of -0.27% and -0.46%, respectively. Health Care and Financials sectors declined by -0.63% and -0.71%, respectively. Utilities and Real Estate sectors had larger declines of -0.82% and -0.84%, respectively. Materials and Energy sectors saw the most significant declines with -1.07% and -1.62%, respectively.

Currency Market Updates

In recent currency market updates, the US dollar experienced a decline of 0.5% as risk aversion sentiment eased, allowing stocks to recover and oil prices to drop, primarily because the worst-case geopolitical scenarios did not materialize. Concurrently, 10-year Treasury yields retreated from their recent peak above 5%. The dollar index fell below a crucial 30-day moving average support level, heading toward October’s lows. Meanwhile, the EUR/USD pair showed strength, rising by 0.7% and surpassing its previous October recovery high at 1.0640, along with other significant resistance levels nearby. A close above 1.0643 would signify a broader correction after a 12-week downtrend, with potential upside targets at 1.0700 and 1.0740.

Furthermore, market sentiment regarding the euro was influenced by the anticipation of upcoming economic data from the eurozone and the United States. Although these data forecasts were not particularly bullish for EUR/USD, the market seemed to signal that the worst of the divergence in yield spreads between the Federal Reserve (Fed) and the European Central Bank (ECB) is over. The ECB was expected to maintain a steady course, with no further rate hikes and the possibility of rate cuts by June, which aligns with the Fed’s timeline. The British pound also gained strength for similar reasons as EUR/USD, with expectations of fewer rate cuts by the Bank of England (BoE) in comparison to the Fed. However, it remained below its downtrend line from July’s highs and October’s rebound highs. Investors were closely watching delayed UK employment data to assess the likelihood of another BoE rate hike. Additionally, USD/JPY experienced a 0.14% decline after nearly reaching a peak close to the pivotal 150 level, primarily due to a drop in 10-year Treasury yields. The market was focused on a significant amount of USD/JPY 150 option expiries on Friday, with limited pricing for substantial moves, especially above 150, before the end of the month and the Bank of Japan (BoJ) meeting. The prospects for dip-buyers would depend on the performance of Treasury-JGB yields following key US data releases later in the week. Tuesday was expected to bring global flash PMI readings for October, with most forecasts indicating continued economic challenges.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Surges to One-Month High as Weaker US Dollar Drives Momentum

The EUR/USD pair rallied significantly on Monday, breaking a downtrend line and reaching 1.0676, its highest level in a month, primarily due to a sharp decline in the US Dollar and improved market sentiment. As the Eurozone and the US prepare to release key PMI data and important monetary policy meetings are on the horizon, the Euro’s outlook remains favorable, though some consolidation may follow the 100-pip rally.

Based on technical analysis, the EUR/USD moved higher on Monday, pushing towards the upper band of the Bollinger Bands. Currently, the EUR/USD is trading at the upper band, suggesting the potential for another push higher movement. The Relative Strength Index (RSI) stands at 75, indicating that the EUR/USD is entering a bullish bias.

Resistance: 1.0705, 1.0770

Support: 1.0630, 1.0561

XAU/USD (4 Hours)

XAU/USD Retreats from Multi-Month Highs Amid Optimistic Start to the Week”

Spot Gold (XAU/USD) experienced a pullback from recent multi-month highs, briefly dipping to the $1,960 price range before finding support at around $1,977 per troy ounce during the American trading session. This retreat was attributed to easing demand for safe-haven assets, influenced by optimism in the financial markets as the situation in the Middle East, particularly the conflict between Israel and Hamas, showed signs of not escalating. The movement in gold was also influenced by changes in government bond yields and speculation about monetary policies in various countries, including Japan and the United States. As the week progresses, investors are closely watching upcoming events, such as the European Central Bank’s monetary policy decision and the release of key economic indicators in the United States.

Based on technical analysis, XAU/USD is moving in consolidation on Monday and able to reach the middle band of the Bollinger Bands. Currently, the price of gold is moving just above the middle band, suggesting a possible continuation movement. The Relative Strength Index (RSI) currently registers at 63, indicating a bullish bias for the XAU/USD pair.

Several key events are expected to influence the financial markets this week, including interest rate decisions from the Bank of Canada (BOC) and the European Central Bank (ECB). In light of this, we recommend traders to exercise caution in their trading preparations, keeping in mind the potential for increased market volatility.

Here are some key highlights to keep an eye on during the week:

UK Claimant Count Change (24 October 2023)

The number of people claiming unemployment benefits in the UK increased by 900 in August 2023.

Updated figures will be released on 24 October, with analysts expecting an additional increase of 2,300.

Flash Manufacturing PMI for Germany, the UK, and the US (24 October 2023)

Germany’s manufacturing Purchasing Managers’ Index (PMI) climbed from 39.1 in August 2023 to 39.6 in September 2023. Meanwhile, the UK’s manufacturing PMI for the same period increased from 43 to 44.3. Finally, the US’ manufacturing PMI for the same period rose from 47.9 to 49.8.

Updated figures will be released on 24 October, with analysts expecting manufacturing PMIs of 40.1 for Germany, 44.7 for the UK, and 49.5 for the US.

Flash Services PMI for Germany, the UK, and the US (24 October 2023)

Germany’s services PMI rose from 47.3 in August 2023 to 50.3 in September 2023. Conversely, the UK’s services PMI declined from 49.5 to 49.3 during this period, while the US’ services PMI also fell from 50.5 to 50.1 during the same period.

Analysts’ forecasted services PMIs for October 2023 are as follows: 50.1 for Germany, 49.4 for the UK, and 49.9 for the US.

Australia Consumer Price Index (25 October 2023)

The Consumer Price Index (CPI) in Australia increased by 5.2% in August 2023, up from the 4.9% rise recorded in July 2023.

Analysts are expecting a growth rate of 5.4% for September 2023, with updated figures to be released on 25 October.

Bank of Canada Rate Statement (25 October 2023)

The BOC maintained its overnight rate target at 5% during its September 2023 meeting, marking another pause in its tightening cycle. The bank indicated that future rate decisions would hinge on the most recent economic indicators.

The next rate statement is set to be released on 25 October, with analysts expecting rates to remain at 5%.

European Central Bank Main Refinancing Rate (26 October 2023)

During its September 2023 meeting, the ECB increased its main refinancing rate by 25 bps to 4.5%. The decision to hike the interest rate was closely contested among ECB members, with the meeting minutes revealing that they were divided by tactical considerations.

Analysts expect the central bank to maintain a rate of 4.5% following its upcoming meeting on 26 October.

US Advance GDP (26 October 2023)

The US economy expanded at an annualised rate of 2.1% in Q2 2023, down slightly from the 2.2% growth in Q1 2023.

Data for Q3 2023 is scheduled for release on 26 October, with analysts projecting a growth rate of 4.3%.

US Core PCE Price Index (27 October 2023)

The Core Personal Consumption Expenditure (PCE) Price Index for the US, excluding food and energy, rose by 0.1% month-over-month in August 2023. This was the smallest increase since November 2020.

Data for September 2023 is scheduled for release on 27 October, with analysts expecting a growth of 0.3%.

Start trading now — click here to create your live VT Markets account.