As November draws to a close, U.S. stock futures indicate a favorable end to the month for major indexes, propelled by surges in Salesforce and Snowflake following stellar earnings. Despite marginal movements in the Dow and S&P 500, both remain near their year-to-date highs, while the Nasdaq holds close to its 2023 peak. November promises to break the three-month losing streak, with the S&P 500 up 8.5% and Nasdaq near 11%, marking their strongest performance since July 2022. Positive market sentiments contrast declines in Asia-Pacific markets, with the focus shifting to potential Federal Reserve rate cuts in 2024. In the currency market, the dollar rebounded on speculations of faster rate cuts, impacting forex pairs and stirring market uncertainties amidst varying economic indicators and central bank remarks.

Stock Market Updates

In November’s final stretch, U.S. stock futures edged up, signaling a positive closure for the month across the major indexes. Wednesday’s after-hours trading saw Salesforce and Snowflake soaring due to better-than-expected earnings, with Salesforce marking an 8% surge and Snowflake climbing over 7%. Despite a marginal day for the Dow and S&P 500, both indexes hover just around 0.5% and 0.8%, respectively, from their year-to-date closing highs. Similarly, the Nasdaq Composite, though slipping 0.16% during the day, remains close to its 2023 closing high by about 0.7%.

November appears poised to end the three-month losing streak for the major indexes, with the S&P 500 marking an 8.5% gain and the Nasdaq nearly reaching an 11% increase. These figures represent their most robust monthly performance since July 2022. The Dow, up by 7.2% in November, is also on track for its best month since October 2022. Amidst higher interest rates, strategist Jay Woods remains optimistic about stocks holding onto their gains, citing positive price action and supportive economic data for the Fed’s stance on rates.

European stocks closed higher, reclaiming positive momentum as markets assessed Federal Reserve board members’ statements. The Stoxx 600 index closed 0.43% higher, with Germany’s DAX index maintaining gains above 1% following a report indicating a slowdown in German inflation for November, surpassing earlier forecasts. Meanwhile, Federal Reserve Governor Christopher Waller expressed growing confidence in the Fed’s policies to rein in inflation, hinting at potential rate reductions if inflation continues to ease in the next few months. However, despite a slight retreat in Wall Street’s earlier gains, the major U.S. indexes remained on course for significant gains in November, contrasting the overnight declines in Asia-Pacific markets, primarily led by losses in Hong Kong.

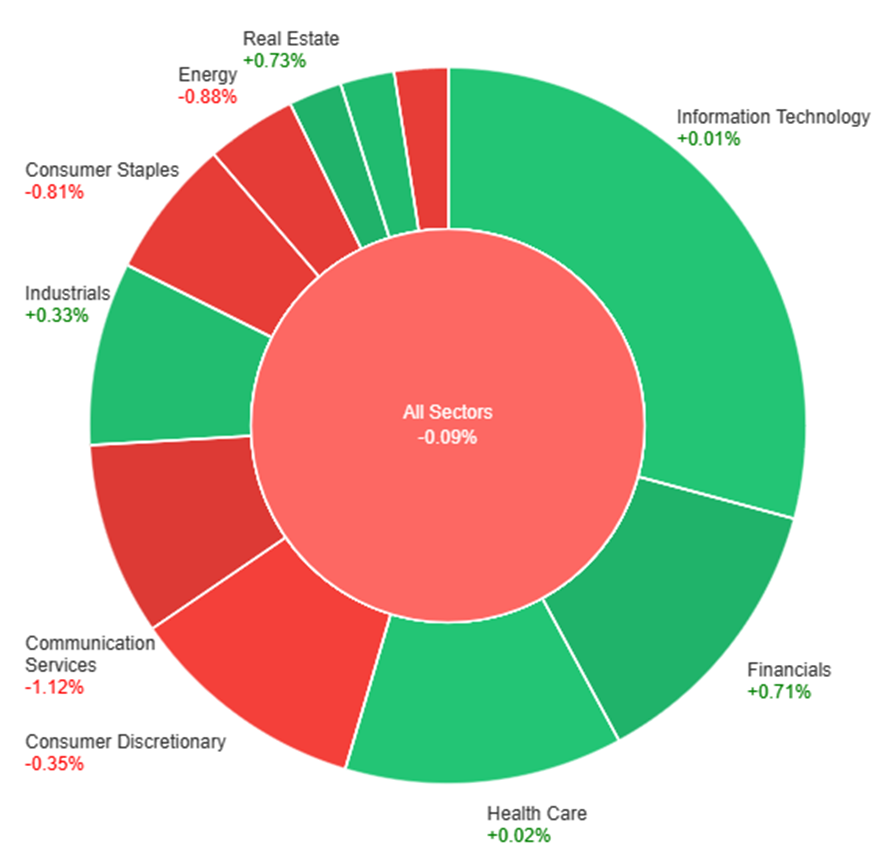

On Wednesday, the overall market experienced a slight decline of 0.09%. However, several sectors showed positive movements, with Real Estate leading the gains at +0.73%, followed closely by Financials at +0.71% and Materials at +0.38%. Industrials and Health Care also saw modest increases of +0.33% and +0.02%, respectively. Conversely, there were notable decreases in certain sectors, with Communication Services taking the biggest hit at -1.12%, followed by Energy at -0.88%, and Consumer Staples at -0.81%. Utilities and Consumer Discretionary also faced declines of -0.79% and -0.35%, respectively. Overall, while some sectors thrived, others encountered notable downturns during the trading day.

Currency Market Updates

In the currency market, the dollar index experienced a rebound of 0.14% after reaching oversold levels, largely influenced by speculation surrounding faster Federal Reserve rate cuts in 2024. This sentiment emerged following comments from Fed’s Waller, leading to expectations of a rate cut as early as May, with futures indicating a potential 114 basis points of cuts by 2024. Concurrently, the Euro saw a decline against the dollar, notably influenced by below-forecast German CPI, fostering a 42% probability of an ECB rate cut in March with an estimated 110 basis points of cuts by the end of 2024. The EUR/USD pair retraced to 1.0960, marking a critical level in its July-October slide.

While the dollar’s trajectory was influenced by expectations around Fed rate cuts, the market remained attentive to upcoming data releases and central bank remarks. The discrepancy among Fed speakers regarding progress in the inflation fight juxtaposed against economic indicators like Q3 GDP revisions, softer Q4 data, and core PCE adjustments to 2.3% contributed to the uncertainty. The movement of key pairs like USD/JPY, impacted by tumbling Treasury yields and contrasting JGB yields, indicated potential challenges for hefty speculative dollar longs. Amidst these fluctuations, sterling rose as it retraced a significant portion of its previous decline, echoing the broader market sentiment awaiting U.S. data releases and Fed Chair Jerome Powell’s commentary. Additionally, the Aussie and Chinese yuan pairs experienced declines and rebounds, respectively, influenced by below-forecast inflation and fluctuations in Fibonacci retracement levels indicative of market sentiment shifts.

The EUR/USD surged to a three-month high at 1.1016 but retreated below 1.1000 despite burgeoning risk appetite. Europe witnessed a slowdown in inflation, notably in Germany and Spain, raising concerns about potential ECB rate cuts. Yet, this might not prompt immediate dovish action, as analysts anticipate a rebound in inflation over the next months. Meanwhile, the US economy revealed robust growth of 5.2% in Q3, lifting the US Dollar on confidence in its performance. However, recent indications of a slowdown before November 18 from the Beige Book compounded with upcoming critical US data—Core PCE Price Index and Jobless Claims—could exert further pressure on the Greenback if they reflect softening inflation and labor market conditions. Bond yields fell on both sides, especially in Germany, adding to the volatility gripping the EUR/USD pair.

On Wednesday, the EUR/USD experienced a downward movement, settling around the middle range of the Bollinger Bands. Presently, the price exhibits a marginal increase above this midpoint, suggesting a potential upward trajectory, potentially reaching the upper band. Notably, the Relative Strength Index (RSI) maintains its position at 55, signaling a neutral outlook for this currency pair.

Resistance: 1.1041, 1.1087

Support: 1.0968, 1.0930

XAU/USD (4 Hours)

XAU/USD Dips Amid Dollar’s Recovery and Fed’s Inflation Sentiments

Spot Gold slid to $2,040 an ounce, pulled down by a resurgent US Dollar amidst profit-taking before pivotal data releases. Despite the Dollar’s bounce, its weakness persists on hopeful sentiments that the Federal Reserve might halt tightening measures. Conflicting views within the Fed add to the uncertainty: while Atlanta Fed President Bostic signals confidence in declining inflation, Richmond Fed President Barkin remains cautious, keeping the possibility of rate hikes alive. With US bond yields retreating to multi-week lows and market focus shifting to the upcoming inflation data, Gold’s trajectory hinges on signs of easing price pressures, poised to either bolster optimism or dampen USD demand.

On Wednesday, XAU/USD underwent a period of consolidation, presently oscillating between the middle and upper bands within the Bollinger Bands. This current movement suggests a potential upward trend, potentially reaching the upper band once again. The Relative Strength Index (RSI) stands at a level below 69, indicating that the bullish sentiment for this pair remains robust.

Resistance: $2,052, $2,079

Support: $2,038, $2,012

Economic Data

Currency

Data

Time (GMT + 8)

Forecast

ALL

OPEC-JMMC Meetings

All Day

CAD

GDP m/m

21:30

0.0%

USD

Core PCE Price Index m/m

21:30

0.2%

USD

Unemployment Claims

21:30

219K

Written on November 30, 2023 at 2:35 am, by anakin

Amidst optimistic Federal Reserve comments signaling a possible pause in interest rate hikes, the stock market continued its climb, with the Dow Jones, S&P 500, and Nasdaq closing at record highs. Notable contributors included Boeing, Nike, and Walmart, while Newmont Corporation and Synchrony Financial surged in the S&P 500. Concurrently, currency markets responded to a more dovish Fed sentiment, leading to fluctuations in the dollar, euro, pound sterling, and USD/JPY. Speculations around potential rate cuts and pivotal economic data releases like U.S. GDP revisions and eurozone inflation figures maintain market focus as expectations lean towards a more accommodative stance from the Fed.

Stock Market Updates

On Tuesday, the stock market continued its upward trend from November, buoyed by optimistic remarks from a Federal Reserve official suggesting a possible halt in interest rate hikes. The Dow Jones Industrial Average closed at 35,416.98, up 0.24%, while the S&P 500 edged up by 0.10% to 4,554.89, and the Nasdaq Composite gained 0.29% to reach 14,281.76. Fed Governor Christopher Waller’s affirmation that current policy is well positioned to manage economic growth and inflation helped reassure markets ahead of the Federal Open Market Committee’s upcoming meeting.

Key contributors to the market’s rise included Boeing, lifting the Dow by 1.4%, alongside retailers like Nike and Walmart, which gained 0.7% and 1.2%, respectively. The S&P 500 saw boosts from Newmont Corporation and Synchrony Financial, surging by 6.3% and 5.1%. November showcased a robust rally, with the Dow and S&P 500 tracking towards gains of approximately 7.2% and 8.6%, while the Nasdaq surged by 11.1%. Meanwhile, U.S. Treasury yields experienced a decline, notably with the 10-year note slipping nearly 6 basis points to 4.33%.

Additionally, positive consumer confidence data released indicated an increase in November, with The Conference Board’s index rising to 102, surpassing both the downwardly revised October figure of 99.1 and the Dow Jones estimate of 101. Looking ahead, CrowdStrike was anticipated to report earnings after the market close, adding to the ongoing market dynamics and investor sentiment.

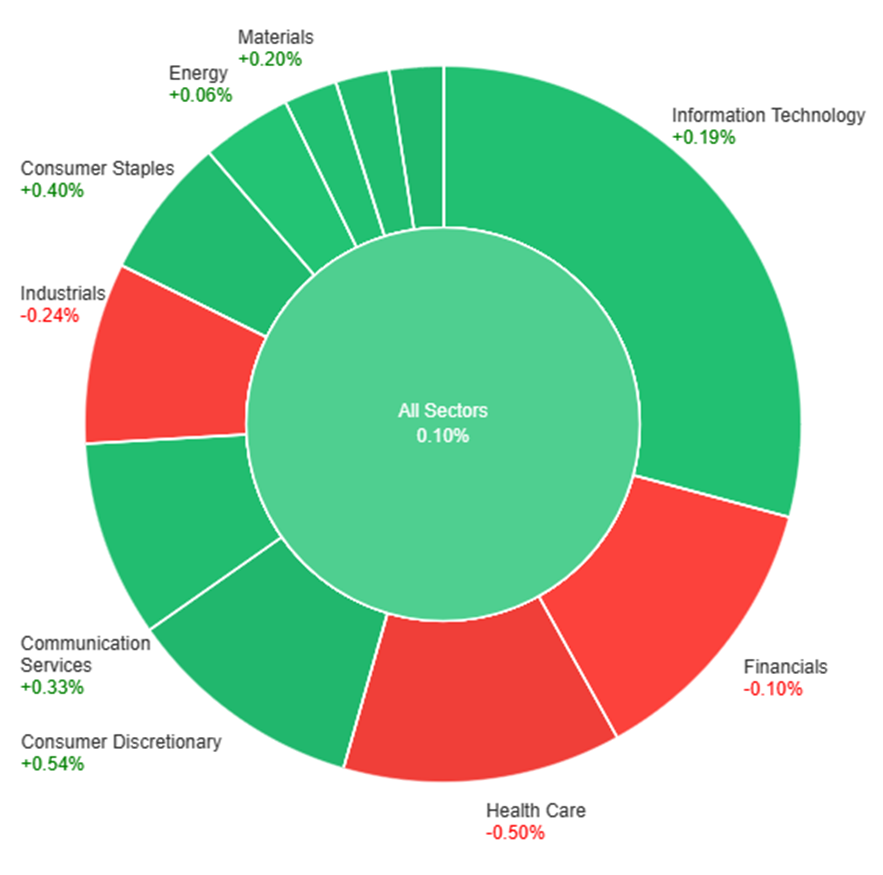

On Tuesday, the market showed a mixed performance across sectors. Consumer Discretionary and Real Estate sectors led the gains with increases of 0.54% and 0.52%, respectively, followed closely by Consumer Staples and Communication Services with gains around 0.40% to 0.33%. Utilities and Materials also saw modest upticks of 0.31% and 0.20%. Conversely, Financials and Industrials experienced declines of -0.10% and -0.24%, respectively, while Health Care faced the most significant downturn, dropping by 0.50%. Energy and Information Technology sectors had more moderate gains, with increases of 0.06% and 0.19% respectively.

Currency Market Updates

The recent movements in the currency market have been influenced by a shift in Fed sentiment towards a more dovish stance. The dollar index dipped by 0.3% as Treasury yields slid following comments from Fed speakers indicating a willingness to consider rate cuts if disinflation persists. This sentiment contrasts with the Fed’s prior messaging, prompting the futures market to anticipate a rate cut in May as twice as likely as a hold, with potential cuts of up to 100 basis points by December 2024. Consequently, the euro gained against the dollar, reaching levels above its 61.8% retracement for the year, driven by a rise in 2-year bund-Treasury yield spreads and risk-on flows due to lower U.S. and European yields.

In tandem with these developments, the pound sterling rose but halted before reaching its 61.8% Fibo of its July-October slide, with expectations that the Bank of England might delay rate cuts compared to the Fed, potentially reducing rates by 67 basis points in the coming year. Conversely, USD/JPY experienced a decline of 0.75%, continuing its reversal from 2023’s uptrend, driven by falling 2-year JGB yields and potential bearish signals if certain technical levels, like a close below the daily cloud base and last month’s low, are breached. The Bank of Japan faces pressure to reconsider negative rates and the efforts to cap JGB yields due to concerns about the weak yen’s impact on Japan’s economy and persistent low inflation.

Looking ahead, key events like German CPI, U.S. GDP revisions, and the beige book are expected to offer further insights. The market’s focus also centers around Thursday’s session with pivotal data releases including euro zone inflation figures and U.S. core PCE, income, consumption, savings rate data, jobless claims, and pending home sales. Forecasts lean towards a more dovish Fed stance and potentially weaker dollar amidst these upcoming releases.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Hovers Within Familiar Territory Amid Cautious Investor Sentiment

The EUR/USD pair remained steady within established ranges as investors exercised caution ahead of pivotal data releases and central bank speeches scheduled in the coming days. While reaching a high of 1.0962, the pair saw a dip to 1.0934 during European trading hours. The US Dollar’s declining appeal for the fourth consecutive day amid speculation around the Fed’s potential halt to rate hikes by May 2024 has lent support, but concerns about inflation updates in the US and Eurozone have curbed the EUR/USD rally. Key data releases, including Germany’s November HICP and the US October PCE Price Index, are anticipated, alongside speeches from Fed officials, heightening the market’s vigilance.

On Tuesday, the EUR/USD moved higher, attempting to reach the upper band of the Bollinger Bands. Currently, the price is hovering just around the upper band, showing potential for consolidation and a possible move toward the middle band. The Relative Strength Index (RSI) remains at 74, indicating a bullish stance for the currency pair.

Resistance: 1.1041, 1.1087

Support: 1.0968, 1.0930

XAU/USD (4 Hours)

XAU/USD Surge as Fed Signals Dovish Tone Amidst Inflation Debate

Gold prices soared, reaching $2,038.45 against the USD following a shift in sentiment from Federal Reserve officials. Governor Waller’s dovish remarks on the recent economic slowdown, suggesting an adequate monetary policy stance against inflation, set the tone. Chicago Fed President Goolsbee echoed progress on inflation, hinting at a potential substantial drop in rates. Meanwhile, Governor Bowman maintained a hawkish stance, leaving room for a rate hike if inflation stagnates. This shift toward dovish sentiments weakened the US Dollar, driving Treasury yields down—10-year government notes now offer 4.36%, while 2-year notes yield 4.80%, signaling market reactions to the Fed’s evolving stance.

On Tuesday, the XAU/USD moved higher and managed to create a push to the upper band of the Bollinger Bands. Currently, the price is just below the upper band, indicating potential consolidation and a possible move downward toward the middle band. The Relative Strength Index (RSI) remains at 83, reflecting a bullish stance for the pair.

Resistance: $2,052, $2,079

Support: $2,038, $2,012

Economic Data

Currency

Data

Time (GMT + 8)

Forecast

AUD

CPI y/y

08:30

4.9% (Actual)

NZD

Official Cash Rate

09:00

5.50% (Actual)

NZD

RBNZ Rate Statement

09:00

NZD

RBNZ Press Conference

10:00

EUR

German Prelim CPI m/m

All Day

-0.1%

EUR

Spanish Flash CPI y/y

16:00

3.6%

USD

Prelim GDP q/q

21:30

5.0%

GBP

BOE Gov Bailey Speaks

23:05

Written on November 29, 2023 at 2:16 am, by anakin

Margin trading can be a double-edged sword, offering the potential for significant gains but also carrying substantial risks. In the realm of Forex trading, this dynamic becomes even more pronounced.

Traders, regardless of their experience level, must understand the intricacies of margin calls in this context. This article is dedicated to demystifying margin calls in the Forex market, clarifying a complex yet crucial part of trading.

Forex trading often involves using a high leverage, which means using borrowed money to increase potential profits. This makes margin trading a strong but risky approach. To use it effectively, traders need to be smart and careful. They should learn as much as they can and have a good plan for managing risks.

Basics of Margin Trading in Forex

Margin trading in the Forex market is a method where traders borrow funds from a broker to control larger positions in currency pairs than they could with just their own capital. This approach enhances their trading potential, allowing for significant market exposure.

When traders begin margin trading in Forex, they start by depositing an initial margin. This deposit acts as a base for their leveraged currency trades. It’s not just about starting out; traders must also maintain a minimum balance in their account, known as the maintenance margin. This is crucial in the Forex market, known for its volatility, to cover potential losses and keep positions open.

Leverage in Forex can significantly increase profit potential. However, it’s a double-edged sword – the same leverage that can amplify profits can also magnify losses, especially given the frequent, sometimes sharp, fluctuations in currency values.

What is a Margin Call?

In Forex trading, a margin call is a crucial event, occurring when a trader’s account equity drops below the broker’s required maintenance margin. This call for action requires the trader to add funds or securities to meet the margin level.

It’s typically triggered by a market value decrease of margin-purchased securities or currencies, reducing account equity. The maintenance margin, a broker’s safety measure, is a fixed percentage of the account’s total value. Falling below this due to market downturns triggers a margin call.

The processfollowing a margin call typically unfolds in several key steps:

1. Notification of Margin Call: The first step is the trader receiving a notification from their broker. This usually happens through email, phone, or a direct message on the trading platform. The notification informs the trader of the deficit in their account and the amount needed to resolve the margin call.

2. Response Time: Traders are given a limited period to respond to a margin call. This timeframe varies depending on the broker’s policy but usually ranges from a few hours to a couple of days.

3. Depositing Additional Funds: To meet the margin call, traders can deposit additional cash into their margin account. This helps in bringing the account’s equity back up to the required maintenance margin.

4. Selling Securities or Currencies: If depositing additional funds is not feasible, traders have the option to sell some of their securities or currencies. The sale should be sufficient to cover the shortfall and restore the account to the required margin level.

5. Broker’s Forced Liquidation: If the trader is unable to meet the margin call within the stipulated timeframe, the broker may proceed to liquidate the trader’s positions. This is done to bring the account back in line with the maintenance requirements. The liquidation often occurs at current market prices, which may not be favorable.

6. Account Adjustment and Strategy Reassessment: After resolving the margin call, either through depositing funds or selling assets, the trader’s account is adjusted to reflect the new balance. Traders often need to reassess and modify their trading strategies post a margin call to prevent future occurrences.

The Mechanics of a Margin Call

Understanding the mechanics of a margin call is key in Forex trading.

Equity in a margin account is the value of your securities minus any borrowed funds. It varies with market values: if your securities’ value goes up, so does your equity; if it falls, your equity decreases.

The maintenance margin is the minimum equity percentage you must keep in your margin account, set by your broker. It’s a safety measure to ensure there’s enough equity to cover potential losses. If your equity falls below this level due to market declines, you’ll face a margin call.

To illustrate, consider a simple example:

A trader opens a margin account and purchases $10,000 worth of currency, using $5,000 of their own money and $5,000 borrowed from the broker. The initial equity in the account is $5,000 (the trader’s own funds).

The maintenance margin requirement set by the broker is 25%.

If the value of the currency falls to $6,000, the equity in the account would now be $1,000 ($6,000 market value minus the $5,000 borrowed).

However, 25% of the current market value ($6,000) is $1,500, which means the trader’s equity of $1,000 is now below the maintenance margin requirement.

This deficit triggers a margin call, requiring the trader to deposit additional funds or sell a portion of the securities to bring the equity back up to or above the maintenance margin level.

This example shows how market changes can lead to a margin call and underscores the importance of understanding and managing your margin account.

Responding to a Margin Call

When a trader in the Forex market receives a margin call, immediate and decisive action is required. This section outlines the crucial steps to take, the options available for meeting a margin call, and the potential consequences of failing to do so.

Immediate Actions

Upon receiving a margin call, a trader should first review their account to understand the shortfall. Quick assessment of the situation is vital to decide the next course of action. It’s important to act swiftly, as delays can lead to more severe financial implications.

Options for Meeting a Margin Call

Traders have several options to satisfy a margin call:

Adding Funds: The most straightforward approach is depositing additional cash into the margin account to cover the shortfall. This action immediately increases the account’s equity back to the required level.

Selling Assets: If adding funds isn’t feasible, traders can sell some of their assets, such as securities or currencies. The proceeds from the sale can then be used to restore the margin balance. This option, however, might involve selling assets at less-than-ideal market prices.

Consequences of Not Meeting a Margin Call

Failure to meet a margin call can have significant consequences:

Forced Liquidation: If a trader cannot satisfy the margin call, the broker may forcibly sell the trader’s securities or currencies. This liquidation is done at current market prices, which might result in substantial losses.

Account Closure: In severe cases, continued failure to meet margin requirements can lead to the closure of the margin account.

Credit Impact: Not addressing a margin call can also negatively impact the trader’s credit status with the broker and potentially affect their ability to trade on margin in the future.

In summary, effectively handling a margin call in Forex trading demands quick decisions, understanding of resolution options, and awareness of the consequences. Prompt action is key to financial stability and ongoing trading.

Best Practices for Margin Traders

In Forex margin trading, effectively managing risk is key. These are essential strategies for more secure trading:

Stop-Loss Orders: Implementing stop-loss orders is crucial to limit potential losses. These orders automatically close out trading positions once they reach a predetermined price level, helping to prevent larger losses.

Judicious Use of Leverage: Leverage can significantly amplify both gains and losses. It’s important to use leverage carefully, understanding its impact on your trading portfolio.

Clear Exit Strategy: Develop a predefined strategy for exiting trades. This helps in reducing impulsive decision-making driven by emotions.

Diversification: Diversify your investments across various currency pairs and other asset classes. This strategy helps in spreading and mitigating risk.

Continuous Monitoring: Regularly review your margin account to ensure it meets maintenance requirements. Additionally, stay informed about market news and events that could impact your trading positions.

By following these practices, traders can better navigate the complexities of Forex margin trading, balancing the potential risks and rewards. To develop your trading skills and test your strategies use VT Markets’ risk-free demo account.

In conclusion, margin calls are an integral aspect of margin trading, representing a significant risk factor that traders must be prepared to manage. While the potential for higher returns exists, the risks are equally amplified. Aspiring margin traders should continue educating themselves about these risks and seek advice from financial experts. Remember, informed trading is responsible trading.

Written on November 28, 2023 at 10:44 am, by anakin

Stocks took a breather after a robust four-week surge as major indices, including the Dow Jones Industrial Average, S&P 500, and Nasdaq Composite, dipped slightly. Cyber Monday witnessed rises in e-commerce stocks like Amazon and Shopify while “buy now, pay later” options surged, propelling Affirm’s stock. However, concerns over weakening consumer spending raised Fed rate hike impact worries. The currency market saw the US Dollar Index dip, reflecting vulnerability amidst declining Treasury yields. Economic indicators, including new home sales, shaped concerns, while currency movements, especially the EUR/USD climb, GBP/USD trajectory, and AUD/USD surge, drew attention. Gold and silver rallied, breaching significant resistance levels.

Stock Market Updates

Stocks took a breather on Monday following a robust four-week surge across major averages. The Dow Jones Industrial Average dipped by 0.16%, closing at 35,333.47, while the S&P 500 shed 0.20% to settle at 4,550.43, and the Nasdaq Composite edged down 0.07% to 14,241.02. The recent bullish trend stemmed from a retreat in the 10-year Treasury yield from briefly surpassing the 5% mark in late October. Despite concerns over weakening consumer spending from some retailers, the market maintained momentum, evidenced by a significant month-to-date increase in the S&P 500 by 8.5%, the Dow by 6.9%, and the Nasdaq by 10.8%.

Amidst the market fluctuation, Cyber Monday saw notable rises in certain e-commerce stocks, with Amazon and Shopify marking increases of 0.7% and 4.9%, respectively. The surge in interest in “buy now, pay later” options on Cyber Monday saw Affirm’s stock soar by nearly 12%. However, weaker spending data is seen as a potential indication that the Federal Reserve’s rate hikes might be impacting the broader economy, raising questions about consumer confidence. Looking ahead, key reports like the consumer confidence report and the personal consumption expenditures price index are expected to provide further insights into the market’s trajectory. Additionally, recent data from the Commerce Department revealed a slower-than-expected pace of new home sales in October, although there was an improvement from the previous year.

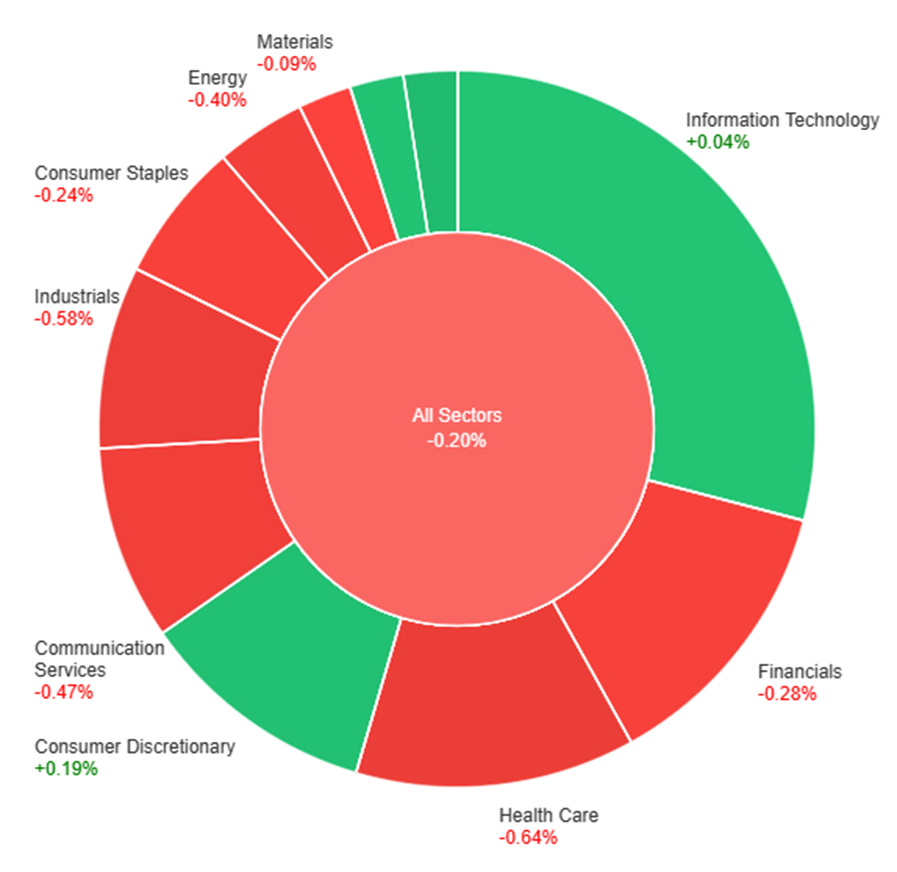

On Monday, the market saw a general decline with the overall sectors showing a negative trend of -0.20%. Real Estate and Consumer Discretionary sectors were the only ones to experience positive growth, gaining +0.38% and +0.19% respectively. Utilities and Information Technology followed with marginal increases of +0.09% and +0.04%. However, the majority of sectors faced losses, notably in Health Care (-0.64%), Industrials (-0.58%), Communication Services (-0.47%), and Energy (-0.40%). Financials and Consumer Staples also experienced declines at -0.28% and -0.24% respectively, while Materials showed a minor dip of -0.09%. Overall, it was a day marked by widespread negative performance across sectors, despite some minor gains in select areas.

Currency Market Updates

In the recent currency market updates, the US Dollar Index experienced a 0.20% dip, marking its lowest daily closure since late August, settling near 103.20. This downward trend persists, indicating the Greenback’s vulnerability, accentuated by declining Treasury yields—specifically, the 2-year fell to 4.89% and the 10-year decreased from 4.50% to 4.38%. The US New Home Sales declined unexpectedly by 5.6%, hitting 679K, below the anticipated 725K mark. This week’s US data focuses on housing metrics, consumer confidence, and manufacturing indices, culminating in the Core Personal Consumption Expenditure Index. Federal Reserve officials are slated to speak, with a blackout period commencing shortly.

Amidst this, the EUR/USD climbed to a three-month high, maintaining the potential for further growth while above 1.0950, eyeing a probable test of 1.1000. Attention in Europe hones in on upcoming inflation figures and the German GfK survey. Meanwhile, GBP/USD continued its upward trajectory, surpassing 1.2600, steering towards establishing a fresh equilibrium level. However, USD/JPY witnessed a decline, descending to around 148.50, impacted by diminished yields after a period of subdued trading.

Elsewhere, AUD/USD surged above 0.6600, marking its peak since early August and surpassing the 200-day Simple Moving Average (SMA). The Reserve Bank of Australia’s Governor Bullock is scheduled for a discussion on economic aspects, coinciding with the release of October Retail Sales data. USD/CAD stayed below the 55-day SMA, potentially aiming for the 1.3600 zone, with a downside bias ahead of the impending employment data.

Complementing these currency movements, gold and silver rallied significantly, breaching significant resistance levels—gold surged past $2,010, while silver recorded its highest daily closure above $24.50 in weeks.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Climbs to Three-Month High Amid Dollar Strain and ECB Caution

The EUR/USD marked a significant upswing, reaching its highest point in three months, propelled by a weakening US Dollar and a persistent bullish trend. With the Greenback facing continued pressure due to subdued Treasury yields, ECB President Christine Lagarde’s warnings about potential inflation upticks and tepid growth added to the Dollar’s woes. Despite disappointing US New Home Sales data and impending housing figures, the Dollar’s strain persisted, allowing the EUR/USD to soar. Nevertheless, market attention is poised to shift toward contrasting growth trajectories between the US and the Eurozone, posing a potential impact on the current bullish momentum.

On Monday, the EUR/USD moved slightly higher, attempting to reach the upper band of the Bollinger Bands. Currently, the price is hovering just below the upper band, showing potential for consolidation and a possible move toward the middle band. The Relative Strength Index (RSI) remains at 63, indicating a neutral position for the currency pair.

Resistance: 1.0965, 1.1004

Support: 1.0925, 1.0885

XAU/USD (4 Hours)

XAU/USD Soars to $2,016 Amid Dollar Weakness: Fed Speculation and Market Mood Swings Drive Precious Metal’s Rally

Gold, represented by XAU/USD, surged to $2,016.38 an ounce propelled by broad US Dollar weakness in the initial half of the day, only to taper to $2,010 as Wall Street’s opening prompted a mild dollar rebound. The Greenback’s recovery stemmed from market sentiment shifts and waning near-term seller interest, fueled by speculation that the Federal Reserve has concluded its tightening cycle. Despite intraday stock market declines, the Dollar struggles to sustain a lasting recovery. In the absence of major economic events, the focus shifts to forthcoming inflation updates from Germany, the Eurozone, and the US, particularly the Fed’s favored inflation gauge, the October Personal Consumption Expenditures (PCE) – Price Index, anticipated next Thursday.

On Monday, the XAU/USD moved slightly higher and managed to reach the upper band of the Bollinger Bands. Currently, the price is just below the upper band, indicating potential consolidation and a possible move downward toward the middle band. The Relative Strength Index (RSI) remains at 69, reflecting a neutral position for the pair.

Resistance: $2,021, $2,038

Support: $2,007, $1,988

Economic Data

Currency

Data

Time (GMT + 8)

Forecast

USD

Consumer Confidence

23:00

101.0

Written on November 28, 2023 at 2:36 am, by anakin

Several key factors are expected to impact the financial markets this week, including the Reserve Bank of New Zealand’s Rate Statement and the US Core Personal Consumption Expenditure (PCE) Price Index. Given the potential for significant market movements, we advise traders to exercise caution when undertaking any trading activity.

Australia’s Consumer Price Index (29 November 2023)

The monthly CPI in Australia increased by 5.6% in the 12 months leading up to September 2023, reaching its highest level in five months.

Analysts forecast a growth rate of 5.2% in the figures for October 2023, which are due to be released on 29 November.

Reserve Bank of New Zealand Rate Statement (29 November 2023)

During its October meeting, the Reserve Bank of New Zealand (RBNZ) held its official cash rate (OCR) steady at 5.5%, marking the third consecutive meeting without a change in the rate.

Analysts anticipate that the RBNZ will maintain its OCR at 5.5% following its upcoming meeting on 29 November.

Canada’s Gross Domestic Product (30 November 2023)

The Canadian economy experienced no change in August 2023, a downward revision from preliminary estimates of a 0.1% growth rate.

The September data for Canada’s GDP is set to be released on 30 November and is expected to reflect no change from August’s figures.

US Core PCE Price Index (30 November 2023)

The US core PCE prices, which exclude food and energy, rose by 0.3% in September 2023, the highest increase in four months.

The next set of data will be released on 30 November, with analysts expecting a growth of 0.2%.

Canada’s Employment Change (1 December 2023)

The Canadian economy added 17,500 jobs in October 2023, marking the third consecutive month of workforce expansion. Meanwhile, the unemployment rate increased to 5.7% in the same period, up from 5.5% in the previous month, reaching its highest level since January 2022.

The figures for November 2023 are scheduled to be released on 1 December, with analysts expecting the creation of 14,000 additional jobs and a rise in the unemployment rate to 5.8%.

Written on November 27, 2023 at 2:46 am, by anakin

European stocks showed a cautious upward trend as the US markets remained closed, with the Stoxx 600 index edging up by 0.3%. Despite oil price falls from the postponed OPEC meeting, oil and gas stocks surged while travel stocks faced a decline. Eurozone’s PMI data revealed worrying employment drops, yet signs of a slowing decline in business activity emerged. Meanwhile, attention shifted to the Dutch election’s potential impact. In the US, the Thanksgiving holiday bolstered positive sentiment despite a modest dollar decline. Wall Street futures mirrored gains in European markets, while attention shifted to S&P Global PMI projections amid a lack of major US releases. Currencies like the Euro and Pound remained steady against the dollar, driven by encouraging PMI data, while others, including the Aussie and Kiwi Dollars, saw mixed movements influenced by domestic indicators and market sentiments.

Stock Market Updates

With the US markets closed, European stocks closed slightly higher on Thursday. The pan-European Stoxx 600 index edged up by 0.3%, showcasing a cautious upward trend amidst investor uncertainty. Despite the ongoing fall in oil prices stemming from OPEC’s postponed meeting, oil and gas stocks surged by 1.4%, countering the downward pressure. However, travel stocks faced a contrasting fate, experiencing a 1% decline. The preliminary purchasing managers’ index data for November in the eurozone painted a worrisome picture, revealing a significant drop in employment for the first time in nearly three years. Even as business activity continued to contract, there were glimmers of hope as the rate of decline in both output and new business showed signs of slowing down. Meanwhile, attention turned to the Dutch election results, particularly an exit poll suggesting the potential for a substantial victory by right-wing populist Geert Wilders and his Freedom Party, the PVV.

In the U.S., stocks saw an increase on Wednesday, buoyed by the benchmark 10-year Treasury yield’s temporary dip to a two-month low. The broadening of the November market rally extended into the Thanksgiving holiday, fostering positive momentum in the market.

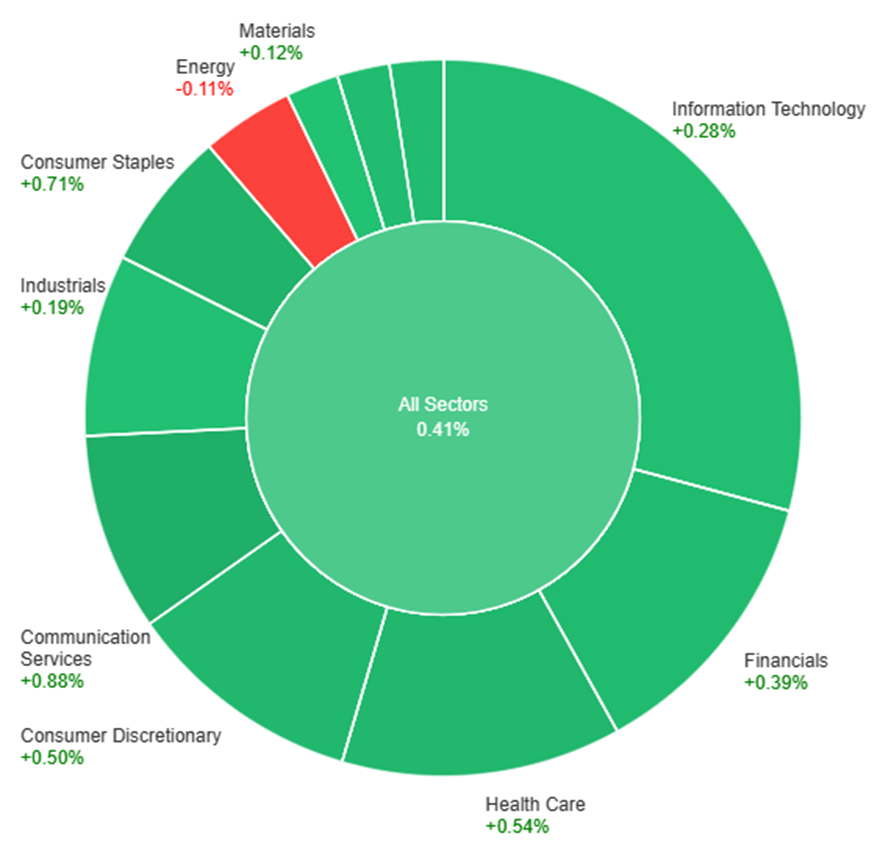

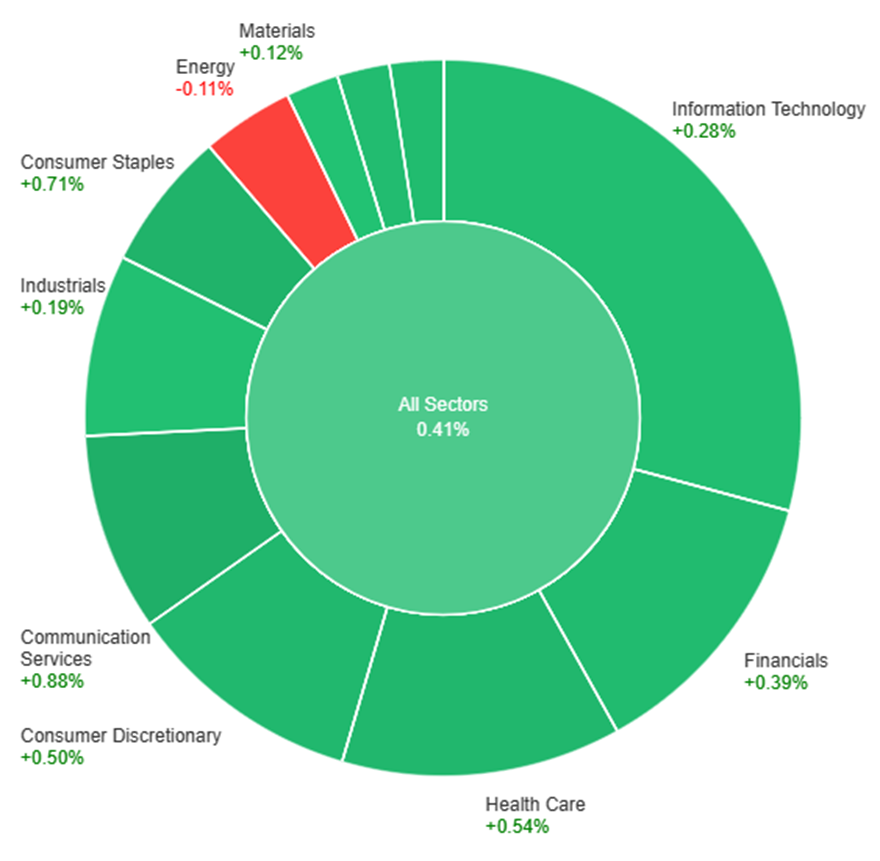

Stock markets were closed on Thursday, here it is the latest updates from Wednesday, across various sectors, the market generally saw positive gains, with the Communication Services sector leading the way with a rise of 0.88%. Following closely were Consumer Staples at 0.71% and Health Care at 0.54%. Sectors such as Financials, Real Estate, and Consumer Discretionary also experienced moderate gains, ranging from 0.37% to 0.50%. However, some sectors did not fare as well, with Energy being the only sector to experience a decrease, falling by 0.11%. Sectors like Information Technology, Industrials, and Materials saw gains ranging from 0.12% to 0.28%, contributing to the overall positive trend in the market for the day.

Currency Market Updates

In a truncated trading session due to the Thanksgiving holiday, the US Dollar experienced a modest decline, settling around 103.75 in the US Dollar Index (DXY), lingering below the 104.00 mark. Despite the closure of US markets, positive sentiment prevailed in Wall Street futures following gains in European markets. With no major US data scheduled for release on Friday and a shortened Wall Street session, attention turned to the S&P Global PMI projection, indicating a slight anticipated downturn in both the Services and Manufacturing sectors.

Meanwhile, the performance of other currencies against the dollar varied. The Euro maintained a relatively stable position around 1.0900 against the dollar, buoyed by encouraging Eurozone PMI figures and an uneventful account of the European Central Bank’s latest meeting. The Pound exhibited strength, reaching a two-month high against the dollar at 1.2530, driven by positive UK PMI data. Other currencies like the Japanese Yen, New Zealand Dollar, Canadian Dollar, and Australian Dollar displayed mixed movements against the US Dollar, influenced by domestic economic indicators and market sentiment. Despite subdued price action, the Australian Dollar managed to rise against the dollar, hovering around 0.6550, while the New Zealand Dollar awaited Q3 Retail Sales data and the Canadian Dollar looked toward the release of September Retail Sales figures.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Inches Up Amidst Low Volume Consolidation: Eurozone Data Insights and ECB Outlook

The EUR/USD saw a modest rise amidst low trading volume, hovering around 1.0900 while the US Dollar Index weakened slightly, fostering support for the pair amid subdued market activity. Eurozone PMI figures showed improvements in both the Manufacturing and Services sectors, yet remaining below the growth threshold. The data initially boosted the Euro but lacked sustained momentum due to minimal trading. The upcoming German GDP report and ZEW survey are anticipated to impact market sentiment. ECB’s recent meeting minutes revealed a consensus on maintaining policy rates and addressing heightened economic uncertainty. Despite ECB President Lagarde and council members slated to speak, clear insights into monetary policy adjustments aren’t expected, especially amid the US market’s closure for Thanksgiving, likely leading to thin trading conditions.

On Thursday, the EUR/USD moved flat as the US market holiday. Currently, the price is moving just below the middle band of the Bollinger Bands with a potential of moving in consolidation as the US market will also close earlier today. The Relative Strength Index (RSI) stays at 54 which reflects a neutral position for the currency pair.

Resistance: 1.0956, 1.1004

Support: 1.0885, 1.0832

XAU/USD (4 Hours)

XAU/USD Struggles to Hold $2,000 Amidst Quiet Trading Session

Gold Spot experienced a fluctuating journey, initially surging towards $2,000 in the Asian session, propelled by a weaker US Dollar, only to retract gains and settle around $1,990 during American hours amid limited trading activity with US markets closed. Despite benefiting from increased risk appetite and a weakening dollar, bolstered by favorable Eurozone PMIs, the precious metal fell short of reclaiming the $2,000 mark. With expectations of continued thin trading and a shortened US market session on Friday, Gold faces a landscape favoring consolidation, although the bullish bias persists for XAU/USD.

On Thursday, the XAU/USD moved flat as the US market holiday. Currently, the price is moving just below the middle band of the Bollinger Bands with a potential of moving in consolidation as the US market will also close earlier today. The Relative Strength Index (RSI) stays at 55 which reflects a neutral position for the pair.

Resistance: $1,996, $2,008

Support: $1,988, $1,973

Economic Data

Currency

Data

Time (GMT + 8)

Forecast

USD

Flash Manufacturing PMI

22:45

49.9

USD

Flash Services PMI

22:45

50.4

Written on November 24, 2023 at 1:06 am, by anakin

The stock market witnessed a surge in major indices, with the Dow Jones, S&P 500, and Nasdaq all marking notable gains, signaling a widening positive trend across the market. However, the energy sector faced a slight decline due to OPEC’s postponed meeting on production cuts. Treasury yields experienced a significant drop, reaching a low not seen since September, influenced by the Federal Reserve’s persistent stance on monetary policy. Despite slight fluctuations and concerns over export restrictions on China impacting Nvidia’s shares, the market remains on track for monthly gains. Meanwhile, in currency markets, the US dollar strengthened against various currencies like the euro, yen, and pound, driven by positive US economic data and global market dynamics. The focus now shifts to upcoming flash PMI releases, which are anticipated to shape currency trajectories and impact key support levels.

Stock Market Updates

The stock market saw a rise in indices as the Dow Jones Industrial Average gained 184.74 points to reach 35,273.03, marking a 0.53% increase. Similarly, the S&P 500 climbed 0.41% to 4,556.62, and the Nasdaq Composite advanced by 0.46% to 14,265.86. This broadening market rally was reflected in over half of the stocks on the NYSE showing gains, suggesting a widening scope for the positive trend. Notably, smaller cap stocks outperformed with a 0.7% and 0.6% rise for small and mid-cap stocks, respectively. However, the energy sector faced a 0.1% decline due to OPEC’s postponed meeting on production cuts, impacting companies like Marathon Oil, EOG Resources, and Devon Energy.

The Treasury yield for the 10-year briefly dropped to 4.369%, hitting its lowest since September, a significant decrease from October’s milestone of crossing the 5% mark for the first time in 16 years. The Federal Reserve’s notes from its recent meeting suggested a persistent stance on restrictive monetary policy, with no hint of imminent interest rate cuts. Despite this, investor optimism prevailed regarding the December meeting. Nvidia’s quarterly report revealed better-than-expected earnings and revenue but cautioned about the impact of export restrictions on China, leading to a 2.5% drop in its shares. Despite Tuesday’s slight decline, the major indices remain on track for monthly gains, with the Nasdaq rallying 11% in November, the Dow up nearly 7%, and the S&P 500 rising over 8%. The market sentiment leans towards the possibility of continued rally, especially with inflation trends and the likelihood of a “soft landing” from the Fed, as noted by Charlie Ripley, a senior investment strategist at Allianz Investment Management. The New York Stock Exchange closed for Thanksgiving and will have an early closure on Friday.

On Wednesday, across various sectors, the market generally saw positive gains, with the Communication Services sector leading the way with a rise of 0.88%. Following closely were Consumer Staples at 0.71% and Health Care at 0.54%. Sectors such as Financials, Real Estate, and Consumer Discretionary also experienced moderate gains, ranging from 0.37% to 0.50%. However, some sectors did not fare as well, with Energy being the only sector to experience a decrease, falling by 0.11%. Sectors like Information Technology, Industrials, and Materials saw gains ranging from 0.12% to 0.28%, contributing to the overall positive trend in the market for the day.

Currency Market Updates

The recent updates in the currency markets have seen the US dollar gaining strength, primarily driven by positive data on U.S. jobless claims and Michigan sentiment, reinforcing the Federal Reserve’s stance against premature rate cuts. Treasury yields experienced an upsurge following a notable drop in initial claims during the job report survey week and a concurrent decrease in continued claims, supporting the dollar’s ascent. Despite below-forecast October durable goods orders, the upward revision in Michigan sentiment and a rise in 1-year inflation expectations propelled Treasury yields further, benefiting the dollar. Notably, EUR/USD faced a 0.3% decline, largely influenced by the widening gap between 2-year Treasury yields and bund yields.

Meanwhile, USD/JPY exhibited a rebound, erasing a significant portion of its previous dive, driven partly by Japan’s economic view being reduced for the first time in 10 months, following an unexpected drop in Q3 GDP. Sterling experienced a 0.4% decline amid the dollar’s broader resurgence and the announcement of fiscal stimulus plans by British Finance Minister Jeremy Hunt. The pound found support at the 1.2450 200-DMA, with the retreat in risk-sensitive cable partially offset by the rise in U.S. equities. Other currencies like the Aussie faced a 0.24% fall, encountering resistance at the 200-DMA amidst a backdrop of weakened Chinese markets and commodities.

The upcoming focus in the market lies on the November flash PMI releases, which are expected to serve as crucial indicators for major economies, potentially impacting the trajectory of currencies like EUR/USD and influencing key support levels, such as the 100-day moving average around 1.08. Additionally, USD/JPY’s movement is closely tied to the convergence of various DMAs in a specific range, indicative of potential future trends. These developments reflect a dynamic landscape in the currency market, shaped by economic data releases and geopolitical events impacting different currencies differently.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Corrects Amidst US Dollar Strength: Market Anticipation on Eurozone Rates and US Data

The EUR/USD retreated to 1.0850 as the US Dollar surged post-release of robust US economic data, marking a correction from recent highs. Bundesbank President Joachim Nagel’s remarks on Eurozone interest rates nearing their peak spurred speculation, hinting at limited rate hikes without an inflation rebound. Thursday’s focus lies on preliminary November PMI data, expected to show slight improvements below the pivotal 50 mark, potentially amplifying pressure on EUR/USD if outcomes disappoint. Concurrently, the US Dollar strengthened on mixed data, including a larger-than-expected drop in Jobless Claims and a sizable contraction in Durable Goods Orders. With US markets closed Thursday, attention shifts to the ECB’s monetary policy meeting minutes, while Treasury yields bolster the Dollar’s corrective momentum amid anticipations for market consolidation.

On Wednesday, the EUR/USD demonstrated a robust downward trend, hitting the lower band of the Bollinger Bands. Presently, it trades marginally above this point, suggesting a potential upward shift aiming for the middle band. With the Relative Strength Index (RSI) resting at 50, it reflects a neutral position for the currency pair.

Resistance: 1.0956, 1.1004

Support: 1.0885, 1.0832

XAU/USD (4 Hours)

XAU/USD Retreats Amid US Dollar Rebound and Economic Data Surge

In response to a surge earlier in the week, Spot Gold (XAU/USD) experienced a pullback as it approached the critical resistance level of $2,010. The decline continued through the American session, signaling potential further downside, albeit at a gradual pace. Despite this retreat, the yellow metal retains an underlying bullish outlook. Concurrently, the US Dollar Index (DXY) rebounded from monthly lows, spurred by robust US economic data, reaching 104.20 before retracing slightly below 104.00. The climb was supported by an uptick in US Yields following a bounce from 4.37% to 4.40%. Notably, recent US data showcased a drop in Initial and Continuing Claims alongside a larger-than-expected contraction in October Durable Goods Orders. With the US market set to be closed on Thursday, a decline in trading volume is anticipated in the upcoming sessions.

On Wednesday, XAU/USD experienced a downward movement, reaching the middle band of the Bollinger Bands. Presently, the gold price hovers slightly above this level, indicating a potential minor uptick aiming for the upper band. The Relative Strength Index (RSI) sits at 55, indicating a period of consolidation for the XAU/USD pair.

Resistance: $1,996, $2,008

Support: $1,988, $1,973

Economic Data

Currency

Data

Time (GMT + 8)

Forecast

JPY

Bank Holiday

USD

Bank Holiday

EUR

French Flash Manufacturing PMI

16:15

43.2

EUR

French Flash Services PMI

16:15

45.6

EUR

German Flash Manufacturing PMI

16:30

41.1

EUR

German Flash Services PMI

16:30

48.4

GBP

Flash Manufacturing PMI

17:30

45.0

GBP

Flash Services PMI

17:30

49.5

Written on November 23, 2023 at 2:11 am, by anakin