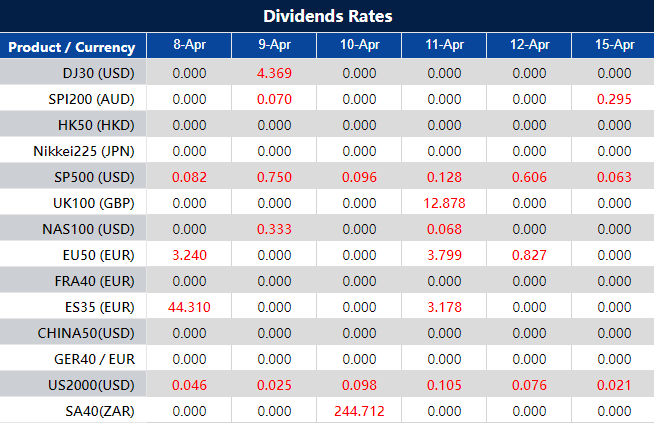

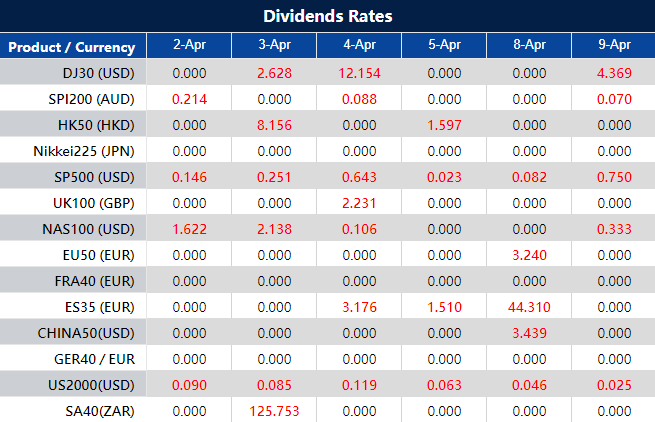

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

As we approach the second week of April 2024, financial markets and policymakers around the globe are bracing for a series of critical economic reports and central bank decisions. These events are expected to offer valuable insights into the ongoing economic recovery efforts, inflationary pressures, and future monetary policy directions. Here’s a day-by-day breakdown of what to anticipate:

Reserve Bank of New Zealand holds firm

On 10 April 2024, the Reserve Bank of New Zealand (RBNZ) made headlines by maintaining its official cash rate (OCR) at 5.5% during its first policy meeting of the year. This decision marked the fifth consecutive meeting without a change in the rate, signalling a cautious stance by the RBNZ amidst economic uncertainties. Analysts are already looking ahead, predicting the OCR to remain at 5.5% following the upcoming meeting, reflecting a steady approach to monetary policy.

U.S. inflation trends upward

In a surprising turn, the annual inflation rate in the United States nudged up to 3.2% in February 2024 from 3.1% in January. This incremental rise, though slight, has caught the attention of market watchers who now forecast a further increase to 3.4% for March. The data, expected to be released on 10 April 2024, will be pivotal for future Federal Reserve decisions.

Bank of Canada’s rate decision

The Bank of Canada, on its part, held its overnight rate target steady at 5% during its March meeting. The bank’s commitment to normalising its balance sheet, despite inflationary concerns, suggests a cautious optimism. Analysts anticipate this trend to continue, with expectations set for the interest rate to remain at 5% in the Bank of Canada’s next meeting.

Federal Reserve and ECB stance

Minutes from the Federal Reserve’s meeting, expected on 11 April 2024, will be closely scrutinised. With the fed funds rate holding steady at a 23-year peak of 5.25%-5.5%, the Federal Reserve’s projections for future rate cuts will be of significant interest. Similarly, the European Central Bank (ECB), which has kept interest rates at historically high levels, faces its own set of challenges balancing recession risks with inflation. Analysts foresee the ECB maintaining its current interest rate levels at 4.5% in its forthcoming meeting.

Upcoming economic data

Additionally, the release of the U.S. Producer Price Index (PPI) on 11 April will offer insights into wholesale price movements, having risen by 0.6% in February. Expectations for March are set at a more modest 0.3% increase. The UK’s GDP data, expected on 12 April, will also be pivotal. After a modest expansion of 0.2% in January, forecasts for February suggest a slight increase of 0.1%, indicating a cautious yet positive economic trajectory.

In summary, the coming week promises a wealth of information for economists, investors, and policymakers alike. With each announcement, the global economic picture for 2024 will become clearer, highlighting the delicate balance central banks are striking between fostering economic growth and managing inflationary pressures.

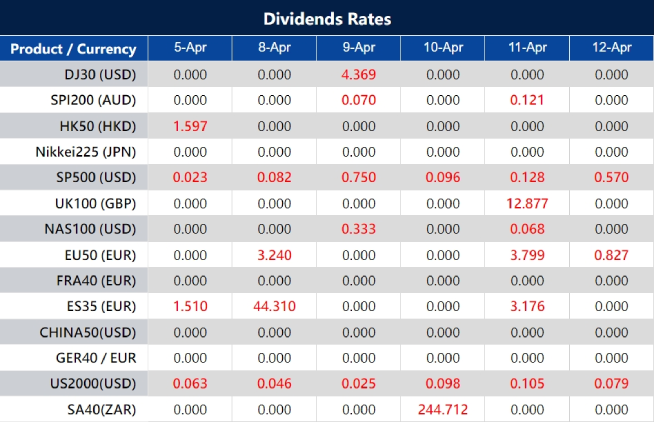

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

Stocks plummeted amid rising oil prices and concerns over the Federal Reserve’s interest rate policies, with major indices like the Dow Jones, S&P 500, and Nasdaq experiencing significant drops. The spike in oil prices to over $86 a barrel fueled inflation fears, while remarks from Fed officials suggested a cautious approach to rate cuts, contributing to market volatility. Meanwhile, in currency markets, the USD Index fell, the euro and pound gained, and gold prices briefly touched all-time highs, reflecting a complex interplay of economic indicators and central bank signals affecting investor sentiment.

Stock market updates

Stock markets experienced a significant downturn on Thursday, fueled by a combination of rising oil prices, mounting fears that the Federal Reserve may delay interest rate cuts, and apprehension about the upcoming March jobs report. This cocktail of concerns led to a sharp sell-off, marking the Dow Jones Industrial Average’s worst performance since March 2023, as it plunged by 530.16 points or 1.35%, settling at 38,596.98. The S&P 500 and Nasdaq Composite weren’t spared either, recording declines of 1.23% and 1.40% to close at 5,147.21 and 16,049.08, respectively, highlighting a broader market apprehension.

Amidst the trading day, a sudden spike in crude oil prices exacerbated the market’s woes, with West Texas Intermediate (WTI) crude breaching the $86 per barrel mark, a peak not seen since October. This surge sparked additional inflationary fears among investors, contributing to the market’s downturn. Complicating matters, Minneapolis Fed President Neel Kashkari’s comments added to the uncertainty, hinting at a potential reconsideration of rate cuts if inflation persists. These factors, combined with a rise in the 10-year Treasury yield to 4.305%, underscored the growing caution among investors, reflected in the day’s volatile trading patterns.

Analysts and investors alike are adopting a cautious stance, closely monitoring the 10-year Treasury yield as a key indicator of future Federal Reserve actions. The overarching sentiment is one of caution, with a focus on how the Fed’s interest rate policies and inflationary pressures will shape market dynamics moving forward.

Currency market updates

The currency markets saw varied movements as the USD Index (DXY) experienced a further decline, dipping into the sub-104.00 region. Anticipation is building for April 5, with market participants keenly awaiting the Non-farm Payrolls, Unemployment Rate, and speeches from several FOMC members. The euro maintained a positive trajectory, reaching new multi-day highs near 1.0880, while the British pound edged close to the significant 1.2700 mark, marking its third consecutive session of gains. Meanwhile, the USD/JPY pair fluctuated within a narrow range, signaling a period of consolidation.

In the commodity currency space, the Australian dollar showcased notable strength, surpassing the 0.6600 threshold, amid expectations for the upcoming Balance of Trade results. This movement reflects broader currency market dynamics, where specific data releases and economic indicators are keenly anticipated for their potential impact on currency valuations. Additionally, the trading session for WTI crude remained relatively flat, yet close to its yearly highs, indicating a sustained interest in energy markets.

Precious metals witnessed a mixed session; gold prices paused after reaching an all-time high above $2,300 per troy ounce, while silver prices ended the session with minimal changes, despite hitting new highs earlier. These movements underscore the volatility and diverse influences at play within the currency and commodity markets, as investors navigate through economic data releases, central bank communications, and broader geopolitical factors impacting market sentiment and currency valuations.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USDrises amid divergent central bank policies and economic outlooks

Despite a significant drop in the US Dollar, leading to a robust increase in EUR/USD to the 1.0870-1.0880 range, the currency pair’s movement reflects broader economic trends, including fluctuating US yields and a steady rise in German bund yields. Central bank policies are in the spotlight, with both the Fed and ECB expected to begin easing cycles possibly by June, although their approaches may diverge. The Fed faces challenges in curbing housing sector inflation, while the ECB grows confident about reaching its inflation target, hinting at upcoming rate cuts. However, the long-term outlook suggests a potential strengthening of the Dollar against the Euro, especially if the ECB and Fed initiate simultaneous easing, potentially driving EUR/USD down to new lows.

On Thursday, the EUR/USD moved lower after reaching the upper band of the Bollinger Bands. Currently, the price is moving in the middle between the middle and upper band, suggesting a potential slight downward movement to reach the lower band before going back higher. Notably, the Relative Strength Index (RSI) maintains its position at 59, signaling a neutral but bullish outlook for this currency pair.

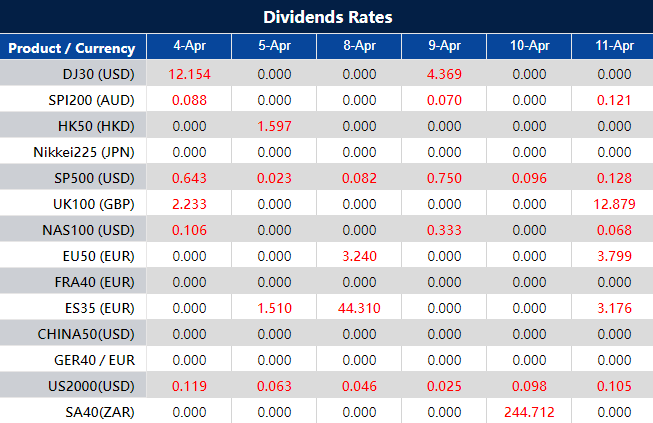

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

On Wednesday, the Dow Jones experienced a slight decline, continuing its downward trend for the third consecutive day, while the S&P 500 and Nasdaq saw modest gains. Market fluctuations were influenced by individual stock performances, such as Intel’s significant drop, and broader economic indicators pointing towards a resilient economy, which in turn affected investor sentiments regarding the Federal Reserve’s interest rate policies. In currency markets, the US dollar faced pressure, with notable movements against the Euro, British pound, and Australian dollar amidst geopolitical tensions and commodity price rallies. Investors remain cautiously optimistic, balancing between the best first quarter since 2019 and the potential for a volatile period ahead as markets adjust to recent gains and anticipate the Federal Reserve’s next moves.

Stock market update

The Dow Jones Industrial Average experienced a slight decline on Wednesday, continuing its struggle to break free from the slump that has characterized the second quarter. The Dow fell by 43.10 points, a 0.11% drop, closing at 39,127.14, marking its third consecutive day of losses. In contrast, the S&P 500 managed a slight increase of 0.11%, closing at 5,211.49, its first gain of the week, while the Nasdaq Composite saw a 0.23% rise, ending the day at 16,277.46. The downturn for the Dow was primarily due to a significant over 8% drop in Intel shares following the announcement of operating losses in its semiconductor manufacturing sector. Despite a positive trend for most of the day, artificial intelligence leader Nvidia ended in the red, hampering the overall market gains. However, substantial increases in major technology stocks like Netflix, up by 2.6%, and Meta Platforms, with a 1.9% gain, provided some support to the market.

Interest rates have continued to place pressure on the stock market. The release of ADP data on Wednesday indicated a higher-than-expected increase in private payrolls for March, signaling a resilient economy but also heightening investor anxiety over the Federal Reserve’s interest rate policies. Comments from Federal Reserve officials dampened hopes for early rate cuts, with Atlanta Fed President Raphael Bostic suggesting a potential rate decrease not occurring until the fourth quarter. Fed Chair Jerome Powell emphasized the need for more evidence of inflation easing before any reduction in borrowing costs. Market predictions now lean heavily towards unchanged rates at the Fed’s May policy meeting, with a diminishing likelihood of a cut by June, as reflected in the shifting odds according to the CME FedWatch Tool and Fed funds futures data.

Despite the challenging start to the quarter, some market analysts remain optimistic, viewing the recent downturn as a period of consolidation after a strong first quarter, the best since 2019 for the S&P 500.

Currency market update

The US dollar experienced additional downward pressure, challenging the 104.00 level as measured by the USD Index (DXY). Upcoming economic data includes February’s Balance of Trade results and weekly Initial Jobless Claims on April 4, alongside speeches from Fed members Barkin, Goolsbee, and Mester. The Euro gained momentum against the dollar, pushing towards the significant 200-day SMA at the 1.0830 region, with market participants looking forward to the final HCOB Services PMIs from Germany and the euro area, as well as the release of the ECB Accounts on the same day. Meanwhile, the British pound surged to new multi-day highs beyond the 1.2600 mark, aligning with the 100-day SMA, ahead of the final S&P Global Services PMI announcement for the UK.

The Japanese yen maintained a steady position against the dollar, staying below the 152.00 mark, with investors eyeing the upcoming release of weekly Foreign Bond Investment figures in Japan. The Australian dollar saw increased buying interest, surpassing the crucial 200-day SMA around 0.6545, with the final Judo Bank Services PMI report due on April 4. In the commodities market, ongoing geopolitical tensions drove West Texas Intermediate (WTI) oil prices to new 2024 highs, exceeding the $86.00 per barrel mark. Safe-haven demand, coupled with anticipations of Federal Reserve rate cuts in June, propelled gold prices to a record peak near the $2,300 per troy ounce, while silver prices continued their rally, reaching new highs just above the $27.00 level per ounce for the first time since June 2021.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD surges amid diverging central bank policies and mixed economic signals

The EUR/USD pair experienced a significant upswing, breaking past the 1.0800 mark and nearing the 200-day SMA, driven by a noticeable decline in the US Dollar amidst contrasting movements in US and German bond yields. Despite the Federal Reserve and the European Central Bank both indicating the onset of easing cycles potentially beginning in June, divergences in their approach could lead to varied strategies. This period saw mixed messages from Fed officials on interest rate adjustments, amidst indicators suggesting a softer economic landscape in the eurozone but expectations of a resilient US economy. These dynamics, coupled with inflation data below expectations in the euro area, hint at a complex interplay of economic factors influencing the EUR/USD trajectory, with a potential shift towards a stronger Dollar in the medium term as both central banks embark on easing measures, potentially driving the pair to revisit its recent lows.

On Wednesday, the EUR/USD moved higher, able to reach the upper band of the Bollinger Bands. Currently, the price is moving slightly below widen the upper band, suggesting a potential another upward movement to reach the resistance level. Notably, the Relative Strength Index (RSI) maintains its position at 67, signaling a bullish outlook for this currency pair.

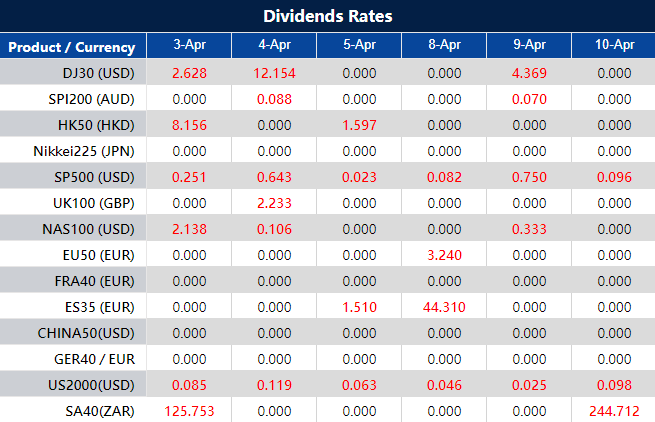

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

The stock market’s continued downturn, driven by concerns over interest rates and persistent inflation, contrasts with a slight recovery in the currency market despite the dollar’s fluctuation. While the stock market’s early 2024 gains face challenges from economic indicators and Federal Reserve officials’ cautious outlooks, currency markets adjust to new data and geopolitical tensions, with notable movements in the Euro, Pound, and Australian Dollar. As investors navigate these turbulent waters, the focus turns to upcoming economic reports and Fed communications, which could further shape market trajectories in both stocks and currencies.

Stock market updates

The stock market experienced another day of declines, marking a continuation of its sluggish start to the quarter. The Dow Jones Industrial Average dropped by 1%, losing 396.61 points to close at 39,170.24, with a session low dipping over 500 points. Similarly, the S&P 500 and Nasdaq Composite fell by 0.72% and 0.95%, respectively, with the Dow and S&P 500 seeing their worst day since March 5. This downturn reflects growing concerns over bond yields and a dampening of expectations for a Federal Reserve interest rate cut in June, further exacerbated by rising oil prices and persistent inflation.

Despite the recent market setbacks, some experts view this as a normal market correction after significant gains in the first quarter. Greg Bassuk of AXS Investments highlighted the market’s reaction to continuous inflation concerns paired with profit-taking activities, while Sarat Sethi from Douglas C. Lane & Associates saw the sell-off as a “natural digestion” of the rapid equity gains. The first quarter saw the S&P 500 enjoying a 10% increase, its best start since 2019, buoyed by hopes of easing inflation and continued economic growth, alongside a strong performance in tech stocks driven by the AI sector. Yet, recent economic indicators and cautious statements from Federal Reserve officials suggest that immediate rate cuts are unlikely, casting doubts on the market’s ability to sustain its early 2024 momentum.

Currency markets updates

In the currency markets, the USD Index (DXY) faced downward pressure, dropping to 104.70 after recent peaks, indicating renewed selling interest. Upcoming economic indicators such as the ADP Employment Change, S&P Global Services PMI, and statements from Federal Reserve officials could further influence the dollar’s trajectory. Meanwhile, the Euro and the British Pound both recovered against the dollar, thanks to its recent weakness, with the Euro area’s inflation rate and unemployment data eagerly anticipated. The Australian Dollar also saw an uplift, moving past the 0.6500 mark, amidst a backdrop of rising WTI oil prices and gold reaching new highs, reflecting increased market volatility and safe-haven demand.

Pick of the day

EURUSD

EUR/USD moved slightly higher on Tuesday and reach our resistance level. Currently, EUR/USD is trading at 1.0768.

At the time of writing, the four-hour Stochastic indicator is moving higher targeting the overbought area, and the price is moving at the 20-period moving average. We expect that EUR/USD might move lower today and reach our support level at 1.0741.

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].