As the world’s economies continue to navigate the post-pandemic landscape, key indicators from the United States, Switzerland, and Canada offer insights into the ongoing recovery and challenges faced by various sectors. The upcoming weeks are set to deliver pivotal data on services sector performance, inflation rates, and employment changes that will shed light on the economic direction of these countries. Below, we delve into the specifics of each report and what analysts are anticipating.

U.S. ISM Services PMI Takes a Slight Dip

In the United States, the Institute for Supply Management (ISM) Services Purchasing Managers’ Index (PMI) saw a slight decline to 52.6 in February 2024, down from a four-month peak of 53.4 in January. This metric is crucial as it reflects the health of the services sector, which constitutes a significant portion of the U.S. economy. The anticipated PMI for March, set to be unveiled on 2 April 2024, is expected to hold steady at 52.6, signaling continued expansion in the services sector, albeit at a tempered pace.

Switzerland’s Inflation Rate on the Rise

Moving to Europe, Switzerland reported an uptick in its inflation rate to 0.6% in February 2024, a significant jump from the 0.2% recorded in the preceding month. This increase was primarily driven by higher costs for housing rentals and air transport. Analysts are closely watching the Swiss economy and forecast a further inflation rise of 0.3% for March 2024, with the official figures scheduled for release on 4 April 2024. This gradual increase in inflation could signal a strengthening consumer demand and economic activity in the country.

Canadian Employment Figures Show Growth

In Canada, the employment landscape showed positive momentum with the addition of 40.7K jobs in February 2024, an improvement over the 37.3K jobs added in January. However, the unemployment rate edged higher to 5.8% in February, up from 5.7% the month before. The focus now turns to the March 2024 employment report, expected on 5 April 2024. Analysts predict a more modest job growth of 25K, with unemployment anticipated to tick slightly higher to 5.9%. These figures suggest that while the job market remains robust, it faces headwinds that could moderate growth.

U.S. Job Market Shows Resilience Amidst Challenges

Lastly, the U.S. job market continued to demonstrate resilience with the economy adding 275K jobs in February 2024, surpassing the revised figure of 229K in January. Despite this strong job growth, the unemployment rate increased to 3.9%, the highest level since January 2022. Looking ahead to March 2024, analysts are forecasting the addition of 200K jobs, with the unemployment rate expected to remain steady at 3.9%. The upcoming jobs report, due on 5 April 2024, will be crucial in assessing whether the U.S. labor market can sustain its momentum amidst economic uncertainties.

As these economic indicators unfold, they will provide valuable insights into the health and trajectory of the global economy. Stakeholders, from policymakers to investors, will be watching closely to gauge the effectiveness of current economic policies and to strategize for the future amidst a landscape of ongoing challenges and opportunities.

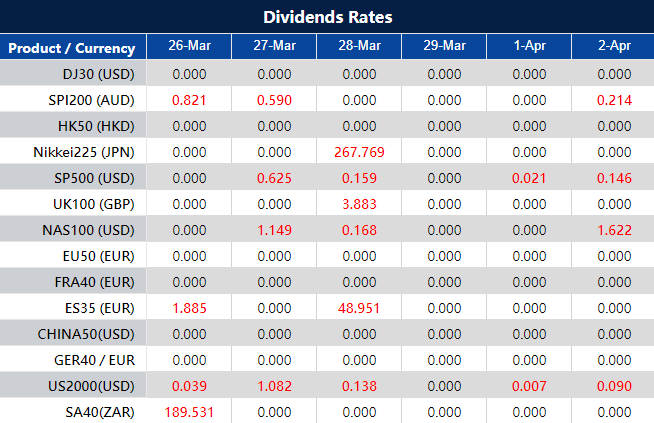

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

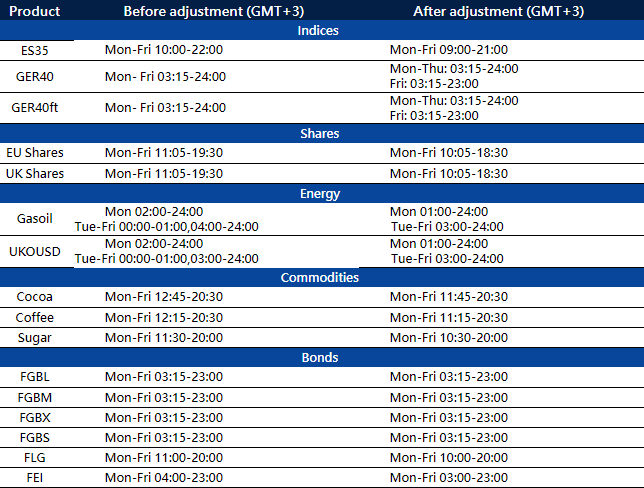

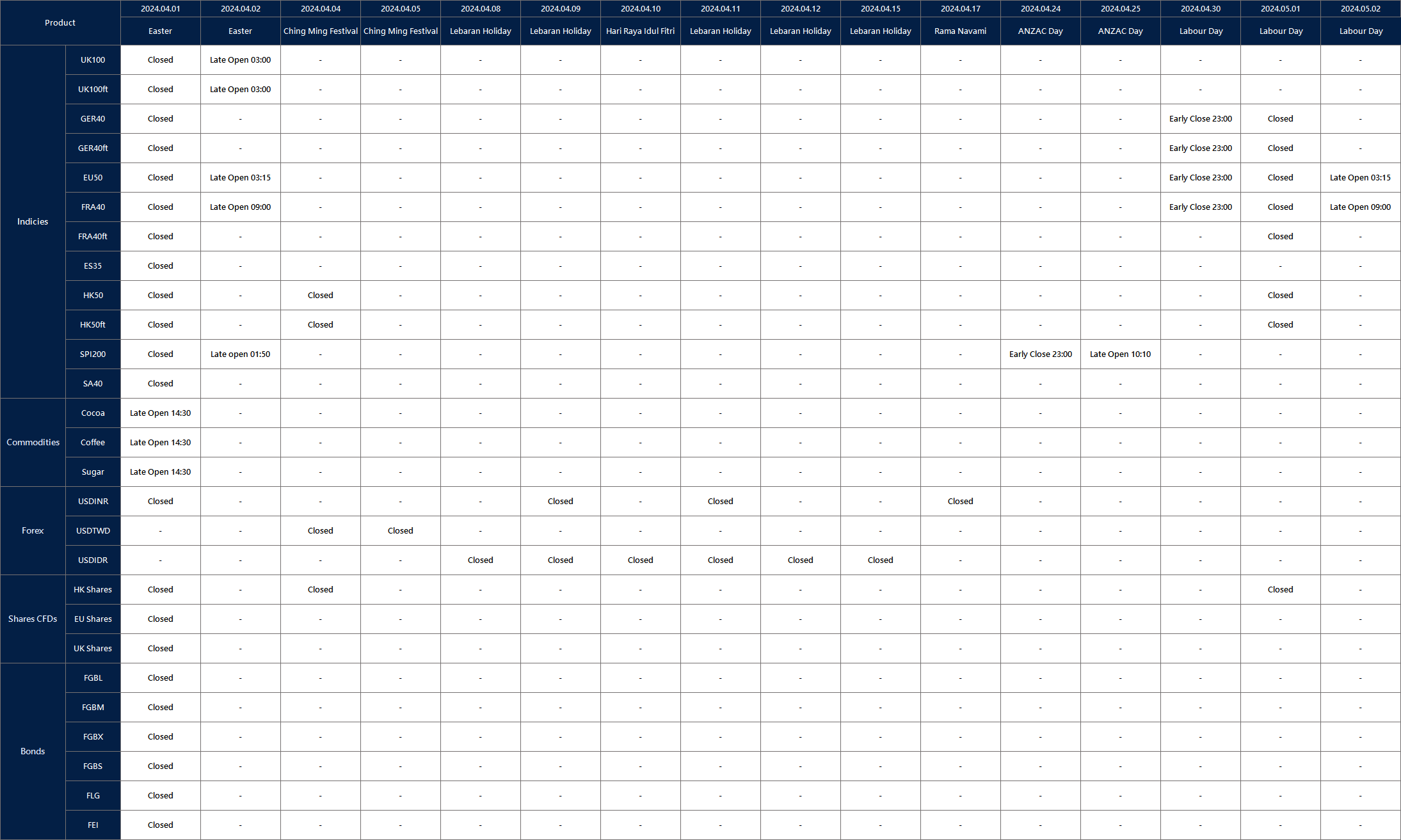

Affected by international holidays, the trading hours of some VT Markets products will be adjusted. Please check the following link for the remaining affected products:

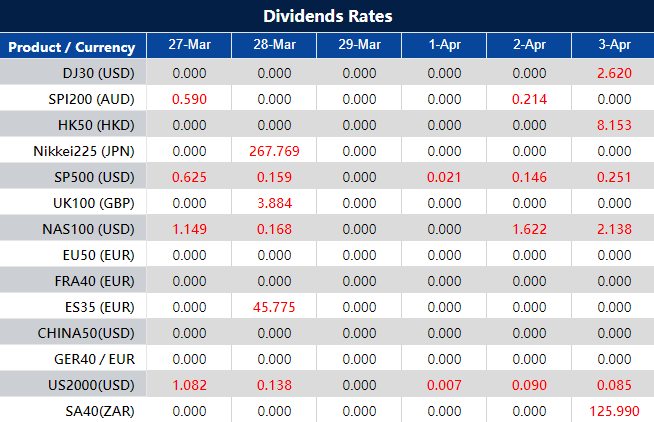

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

Wednesday witnessed a significant uptick in the S&P 500 and Dow Jones, marking a promising close to the first quarter with the best performance since 2019. All sectors of the S&P 500 saw gains, led by utilities, real estate, and industrials, amidst broad market optimism and strategic quarter-end rebalancing. The stock market’s positive trajectory is buoyed by expectations of a soft landing for the U.S. economy and adjusted interest rate cut forecasts. Meanwhile, in the currency market, the dollar index edged up slightly, with USD/JPY experiencing a minor dip amid speculation of Japanese intervention to support the yen. The currency landscape remains cautious, with upcoming U.S. economic data and central bank policy adjustments in focus, especially regarding rate cuts by the Fed and the ECB. Investors and traders are keenly awaiting further indicators, including jobless claims, GDP, and consumer sentiment, to gauge the economic outlook as the second quarter approaches.

Stock market updates

The S&P 500 saw a significant rise on Wednesday, marking a new record high as it continues its journey toward the best first quarter since 2019. The index rose by 0.86%, closing at 5,248.49, while the Dow Jones Industrial Average saw a substantial gain, advancing 477.75 points or 1.22% to close at 39,760.08. The Nasdaq Composite also enjoyed gains, rising by 0.51% to close at 16,399.52. This uplift in the stock market ended a three-day losing streak for both the S&P 500 and the Dow Jones, highlighting a robust broad rally across the market.

In terms of sector performance, all 11 sectors of the S&P 500 experienced gains, with utilities leading the charge with an impressive jump of nearly 2.8%. This was closely followed by real estate and industrials, which advanced 2.4% and 1.6% respectively. This widespread rally underscores the market’s positive sentiment, driven by a strategic rebalance toward the end of the quarter. According to Art Hogan, chief market strategist with B. Riley Wealth, this shift indicates a growing enthusiasm for equities, spurred by quarter-end rebalancing and an overall positive outlook for the stock market as we approach the end of the first quarter.

Looking ahead, the major stock indexes are set to conclude the first quarter on a strong note, with the S&P 500 aiming for a 10% gain, which would be its best first-quarter performance since 2019. The Dow and Nasdaq are also on track for substantial quarterly gains. Additionally, the anticipation of a soft landing for the US economy and adjusted expectations for interest rate cuts contribute to a positive market outlook. Investors are now looking forward to upcoming data on jobless claims, GDP, and consumer sentiment, which will provide further insight into the economic landscape as we move into the second quarter.

Currency market updates

The dollar index experienced a slight increase as the market consolidated gains from the previous week, with traders awaiting further U.S. economic data and navigating quarter-end rebalancing. This period of anticipation comes ahead of the upcoming holiday market closures. Despite a broader increase, the USD/JPY pair saw a minor decline, reflecting market reactions to potential Japanese intervention to support the yen and prevent further decline, contrasting with the aggressive yen support seen in October 2022 following the Fed’s rate hiking cycle commencement.

In currency movements, the USD/JPY dynamics were influenced by speculation around the Federal Reserve’s future rate cuts, with traders eyeing crucial economic data releases for further direction. Meanwhile, the EUR/USD pair dropped slightly amid fluctuations in yield spreads between bunds and Treasuries, indicating a cautious market sentiment towards rate cuts by major central banks. Market pricing shows a significant anticipation of rate adjustments by the ECB and the Fed within the year, highlighting the nuanced interplay between monetary policy expectations and currency valuations.

The British pound found some stability, managing to stay above a recent low, supported by steady yields spreads between Gilts and Treasuries. This steadiness is amidst a broader market focus on upcoming U.S. economic indicators and a keen interest in Federal Reserve Governor Christopher Waller’s speech for insights into the central bank’s rate strategy. As the market approaches the holiday weekend, with key economic data on the horizon, currency traders are closely monitoring shifts in monetary policy outlooks and their potential impact on currency markets.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD outlook influenced by ECB and Fed’s potential easing cycles

The EUR/USD pair witnessed a slight decline as the US Dollar gained modestly, influenced by expectations of divergent monetary policy strategies between the Federal Reserve (Fed) and the European Central Bank (ECB). Both central banks are anticipated to initiate easing cycles possibly in June, albeit at potentially different paces. ECB’s consideration for a rate cut is supported by moderating wage growth in the eurozone, suggesting a cautious approach towards easing. Meanwhile, the probability of a Fed rate cut in June slightly decreased. Despite these developments, the broader economic outlook hints at a stronger Dollar in the medium term, especially as both banks move towards easing, potentially driving EUR/USD towards its year-to-date low and beyond.

On Wednesday, the EUR/USD moved lower, able to reach near the lower band of the Bollinger Bands. Currently, the price is moving slightly above the lower band, suggesting a potential slight downward movement to reach the lower band. Notably, the Relative Strength Index (RSI) maintains its position at 38, signaling a bearish outlook for this currency pair.

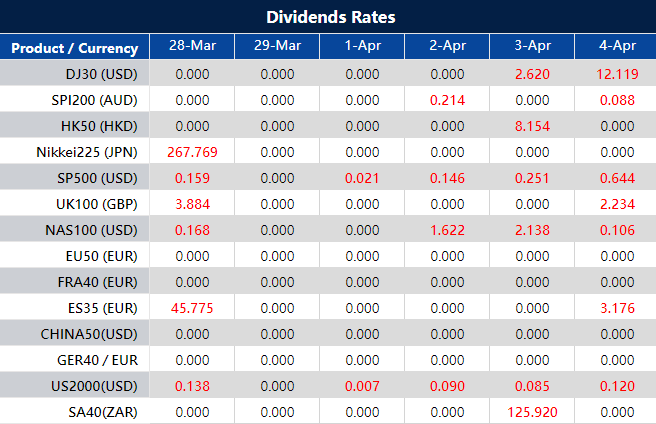

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

This week witnessed a slight retreat in major U.S. stock indexes, with the S&P 500, Nasdaq Composite, and Dow Jones Industrial Average all experiencing downturns, contrasting sharply with their recent record highs. Notably, Tesla, Seagate Technology, and Krispy Kreme outperformed, driven by positive developments. Mixed economic data revealed robust durable goods orders but a drop in consumer confidence, setting a cautious tone for investors as they await key reports on personal consumption and labor market trends. In currency markets, the dollar index recovered, supported by U.S. Treasury yield rebounds and anticipation of upcoming economic data releases. The forex market sees cautious trading, with the USD/JPY pair in focus amid intervention concerns, and the EUR/USD facing downward pressure due to diverging central bank policies and economic forecasts. The market remains watchful, with investors poised for the next set of economic indicators to gauge future directions.

Stock market updates

The S&P 500 experienced a downturn for the third consecutive session, evidencing a modest retreat in the broader market. This downtrend saw the S&P 500 decline by 0.28%, closing at 5,203.58, while the Nasdaq Composite dropped by 0.42%, ending the day at 16,315.70. The Dow Jones Industrial Average slightly decreased by 31.31 points, or 0.08%, to settle at 39,282.33. This cooling period contrasts sharply with the performance seen last week when all three indexes reached record highs on Thursday, and the Dow neared the 40,000 milestone. Notably, Tesla, Seagate Technology, and Krispy Kreme were among the stocks that bucked the day’s downward trend, posting significant gains due to various positive developments.

Market dynamics on Tuesday were influenced by a mix of economic indicators and corporate news. Tesla’s shares surged nearly 3%, marking a notable rebound for the electric vehicle giant amidst a challenging year. Seagate Technology enjoyed a 7.4% uplift after an optimistic rating upgrade by Morgan Stanley, fueled by artificial intelligence prospects. Krispy Kreme’s shares skyrocketed by 39% following the announcement of an expanded partnership with McDonald’s, signaling positive investor sentiment towards these corporate strategies. According to Tom Hainlin, a senior investment strategist, the market’s expansion to include more cyclical sectors is a reflection of enduring economic health and persistently high inflation, despite mixed signals from Tuesday’s economic data, including robust durable goods orders but declining consumer confidence.

As the month draws to a close in a relatively quiet trading environment, expectations are set for the market’s performance in light of upcoming economic reports. Ross Mayfield, an investment strategy analyst, suggests that investors are adopting a wait-and-see approach ahead of crucial updates on personal consumption expenditure and labor market openings. The major stock indexes are poised for their fifth consecutive month of gains, with the S&P 500, Nasdaq Composite, and Dow Jones Industrial Average showing increases of over 2%, 1.4%, and 0.7%, respectively, for March. This resilience underscores the market’s capacity to sustain growth momentum amidst varying economic signals.

Currency market updates

The dollar index witnessed a revival, climbing back to positive territory amidst cautious trading ahead of the quarter-end and upcoming holidays, bolstered by mildly supportive U.S. economic data and anticipation of Friday’s core PCE update. The uplift in Treasury yields and the dollar was partly fueled by a rebound in U.S. durable goods orders, although mixed signals came from regional Fed manufacturing indexes and a dip in consumer confidence below expectations. The two-year Treasury yields saw a brief recovery, influenced by a solid five-year auction, setting the stage for potential shifts in yield and dollar movements post the critical core PCE, income, and consumption data release, with the forex market open for trading despite the closure of bond and stock markets on Friday.

In the currency pairs, USD/JPY modestly increased after overcoming concerns of potential Japanese intervention, which had been a hot topic following the Bank of Japan’s rate hike. Despite speculation and previous interventions aimed at curbing the yen’s decline, the upcoming U.S. economic data could solidify the dollar’s uptrend, making it difficult to justify intervention based on fundamental analysis. Meanwhile, EUR/USD experienced a slight decline, with market sentiment influenced by expectations of policy divergence between the ECB and the Fed, further compounded by pessimistic GDP forecasts for Germany contrasted with an upgraded U.S. GDP outlook by the FOMC.

The Swiss franc emerged as the weakest among major currencies, influenced by expectations of further rate cuts by the Swiss National Bank. Sterling remained stable, facing resistance ahead of recent highs, while the yuan found some footing after a previous setback, hinting at state-supported stabilization efforts. The currency market’s dynamics continue to be shaped by a complex interplay of economic indicators, central bank policies, and geopolitical factors, awaiting more definitive direction from upcoming high-tier U.S. data and its implications for global financial markets.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD holds steady as central banks signal easing cycles amid mixed economic signals

In a day marked by slight movements, the US dollar saw a marginal rise, leading to a modest decline in the EUR/USD pair, which hovered around 1.0830. This minor fluctuation occurred amidst a backdrop of falling US and German yields, reflecting broader uncertainties and a cautious outlook from investors. Central banks on both sides of the Atlantic are gearing up for anticipated easing cycles starting possibly in June, with the pace of interest rate cuts expected to vary between the Federal Reserve (Fed) and the European Central Bank (ECB). Despite differing strategies, the ECB is poised not to fall significantly behind the Fed in its monetary easing efforts.

The week also highlighted contrasting perspectives within the Fed regarding the timing and necessity of rate cuts, underpinning a broader debate on how to navigate current economic challenges while aiming for a “soft landing.” With the FedWatch Tool indicating a rising probability for a rate cut in June, and ECB officials signaling readiness for easing, the stage is set for potential shifts in monetary policy that could impact currency dynamics.

Amid these developments, the enduring resilience of the US economy, juxtaposed with the euro area’s more tepid fundamentals, suggests a medium-term outlook favoring a stronger dollar. This scenario sets the stage for a potential deeper correction in the EUR/USD pair, with targets looming at the year-to-date low around 1.0700 and possibly extending towards the 1.0500 level observed in late 2023. The interplay of central bank policies, economic indicators, and market sentiment will be critical in shaping the currency pair’s trajectory in the coming months.

On Tuesday, the EUR/USD moved higher, able to reach near the upper band but then moved back lower to reach the middle band of the Bollinger Bands. Currently, the price is moving slightly below the middle band, suggesting a potential slight downward movement to reach the lower band. Notably, the Relative Strength Index (RSI) maintains its position at 42, signaling a neutral but bearish outlook for this currency pair.

Sydney, Australia, 27 March 2024 – Global multi-asset broker VT Markets recently successfully participated in the World Affiliate Dubai conference, a prestigious event brought together global top affiliate marketers and ecommerce entrepreneurs to network and exchange professional insights among peers.

The abovementioned event, along with the Smart Vision Summit Oman 2024 in mid-February, where VT Markets picked up the Best Forex Introducing Broker Provider award, are key events in the region that serve the fintech community by facilitating the exchange of information, while providing a platform for key industry players to showcase their innovations and solutions to the public. These engagements signify an integral part of VT Markets’ strategic growth plans in the MENA region.

In addition to active participation in industry events, VT Markets recently achieved notable recognition at the International Business Magazine Awards 2024, securing three prestigious accolades: Best Multi-Asset Broker MENA 2024, Most Reliable Trading Platform MENA 2024, and Most Transparent Forex Broker MENA 2024. A spokesperson for VT Markets commented, “Winning these awards underscores our unwavering commitment to delivering trading excellence to our clients, with reliability and transparency as our guiding principles.”

VT Markets is committed to providing comprehensive and unparalleled client experiences, including personalized account management and priority customer support. Further elevating the experience, private luxury car commutes are made available for client consultations, ensuring clients enjoy seamless financial journeys in every way.

Looking ahead, VT Markets remains proactive in its engagement with the MENA region, with plans to participate in the upcoming Brokersview Expo on April 16th, 2024. This global event, which integrates resources from the financial sector, further solidifies VT Markets’ ongoing commitment to the MENA region as it continues its momentum into the second quarter of 2024.

About VT Markets:

VT Markets is a regulated multi-asset broker with a presence in over 160 countries. To date, it has won numerous international accolades including Best Customer Service and Fastest Growing Broker.

In line with its mission to make trading accessible to all, VT Markets currently offers unfettered access to over 1,000 financial instruments and a seamless trading experience via its award-winning mobile app.

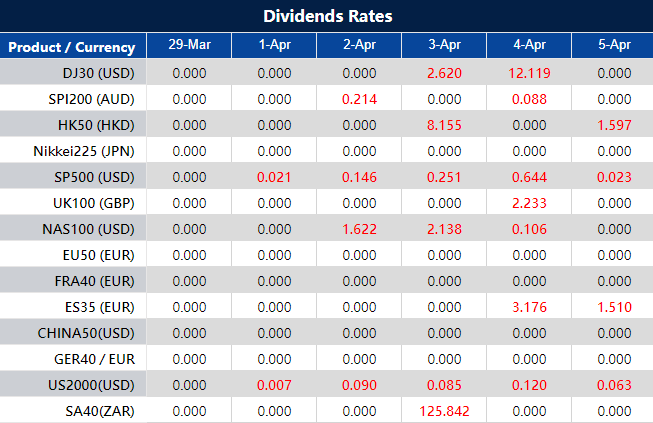

Please note that the dividends of the following products will be adjusted accordingly. Index dividends will be executed separately through a balance statement directly to your trading account, and the comment will be in the following format “Div & Product Name & Net Volume ”.

Please refer to the table below for more details:

The above data is for reference only, please refer to the MT4/MT5 software for specific data.

If you’d like more information, please don’t hesitate to contact [email protected].

{kind=link}