Gold prices have been fluctuating, stuck in a consolidation phase as they await new catalysts.

Upcoming U.S. inflation data could significantly influence gold’s price direction in the near term.

Impact of Federal Reserve’s Monetary Policy

The Federal Reserve’s stance on interest rates is a crucial factor for gold’s future movements. Current signals suggest no immediate rate cuts, which may dampen gold’s appeal.

Inflation Data and Gold’s Reaction

Expected U.S. inflation rates and their potential impact on gold are discussed, with specific projections for January’s CPI.

An unexpected high inflation report could negatively affect gold prices by adjusting interest rate expectations.

Outlook Based on Inflation Outcomes

Lower-than-expected inflation could boost gold prices, possibly affecting market expectations for future rate cuts.

STOCK MARKET:

Stock Market Highlights

The S&P 500 reached a new record high, closing at 4,995, with the 5,000 mark in sight.

U.S. stocks rose, influenced by quarterly earnings reports and ongoing discussions about interest rate cuts.

Despite mixed earnings, notable movements included Alibaba’s shares dropping after a revenue miss and Snap’s significant decline following a disappointing profit forecast.

Disney announced a 50% increase in its cash dividend after reporting strong earnings, leading to a post-market share price surge.

Federal Reserve officials suggest no immediate rate cuts, with a focus on inflation trends before any policy adjustments.

Concerns around regional banks and the real estate sector were sparked by troubles at New York Community Bancorp, despite a slight recovery in its share price.

On Wednesday, the stock market experienced notable gains, propelling the S&P 500 tantalizingly close to the 5,000 mark, thanks to strong quarterly results underscoring a robust economy. The index rose by 0.82%, setting a new closing high of 4,995.06, while the Nasdaq Composite and Dow Jones also posted gains, driven by upbeat corporate earnings and the growth of tech giants like Nvidia and Microsoft. Despite the Federal Reserve’s cautious stance on interest rate cuts, investor optimism remained buoyed by signs of resilient consumer spending and positive corporate guidance. Additionally, the currency market saw adjustments ahead of key U.S. economic data, with the dollar index slightly retreating as markets await the upcoming CPI report, potentially influencing future Fed policy decisions.

Stock Market Updates

On Wednesday, the stock market witnessed significant gains, with the S&P 500 inching closer to the coveted 5,000 mark, achieving a new closing high as a result of strong quarterly results that suggest a thriving economy. The index saw a 0.82% rise, closing at 4,995.06, and even touched 4,999.89 at its peak during the session. Similarly, the Nasdaq Composite and the Dow Jones Industrial Average experienced increases, with the Nasdaq up by 0.95% to 15,756.64 and the Dow Jones rallying 156 points or 0.4%, to close at an all-time high of 38,677.36. These gains were propelled by optimistic corporate earnings and significant growth in major technology companies like Nvidia, Microsoft, Meta Platforms, Alphabet, and Amazon.

The market’s robust performance is attributed to a better-than-expected earnings season, strong corporate guidance, and signs of resilient consumer spending despite high-interest rates. This optimism persisted even as the Federal Reserve and its officials, including Chair Jerome Powell and Minneapolis Fed President Neel Kashkari, suggested a more cautious approach towards rate cuts, potentially delaying them longer than investors had anticipated. In addition, the stock market’s advance reflects a growing comfort among investors with the prospect of delayed rate cuts. Meanwhile, other notable movements included a significant rise in Enphase Energy’s stock following positive comments on its inventory situation, Ford’s surge after surpassing fourth-quarter expectations, and New York Community Bancorp’s volatile performance after Moody’s downgrade. The market is also anticipating earnings reports from major companies like Walt Disney, PayPal, and Arm Holdings.

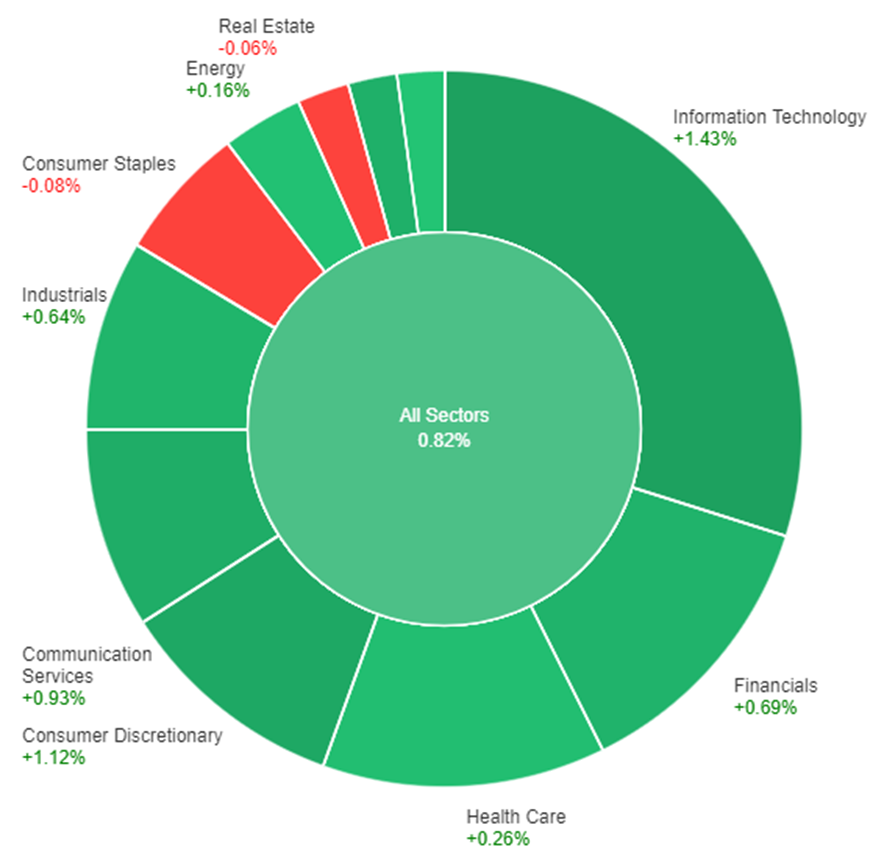

On Wednesday, the stock market showed a positive trend across most sectors, with the overall sectors seeing an increase of 0.82%. Information Technology led the gains with a 1.43% rise, followed closely by Consumer Discretionary and Communication Services, which went up by 1.12% and 0.93%, respectively. Other sectors such as Materials, Financials, Industrials, and Health Care also saw increases, albeit at a slower pace, with gains ranging from 0.26% to 0.81%. The Energy and Utilities sectors experienced minimal growth, with increases of 0.16% and 0.05%, respectively. However, not all sectors fared well; Real Estate and Consumer Staples saw declines of 0.06% and 0.08%, marking them as the only sectors to experience a downturn on Wednesday.

Currency Market Updates

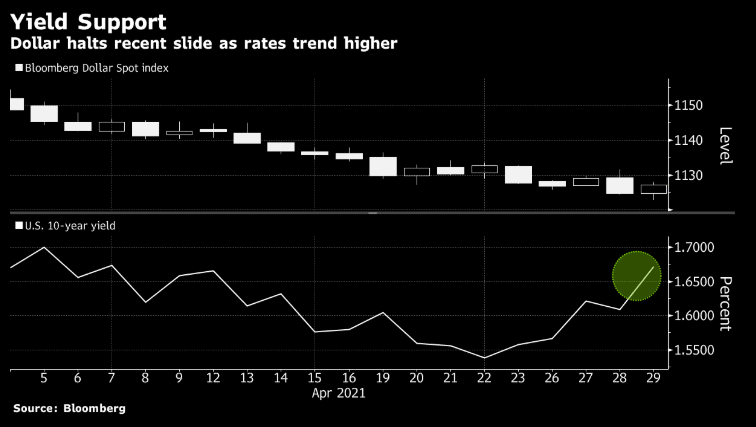

In the currency market, the dollar index saw a minor decline on Wednesday, entering a period of consolidation after experiencing significant gains fueled by robust U.S. employment figures and ISM data. This pause in momentum comes as the market anticipates further disinflationary data before the Federal Reserve considers any rate cuts. The focus now shifts to the upcoming U.S. CPI data scheduled for February 13, which could play a crucial role in shaping future Fed policy decisions. Despite a decrease in the likelihood of a March Fed rate cut, from previously higher probabilities, the market still anticipates substantial easing throughout the year, a scenario that remains more aggressive than the Fed’s own projections.

Currency pairs reacted to these developments, with the EUR/USD pair showing some resilience by posting a modest gain of 0.14%, despite facing resistance at key technical levels. This movement reflects ongoing market adjustments ahead of significant Treasury auctions and amidst mixed signals from Fed officials regarding the pace of future rate cuts. Meanwhile, the USD/JPY pair edged higher, influenced by the dynamics of Treasury yields in comparison to Japan’s relatively stable and low yields. Other currencies, such as the British pound and the Swiss franc, also experienced movements influenced by speculation around monetary policy adjustments and interventions, respectively. As markets brace for the U.S. annual CPI revisions and January’s CPI report, currency traders remain vigilant, gauging the potential impact of these releases on Fed policy and consequently on currency valuations.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Rises Amid USD Weakness and Central Bank Signals

As the US Dollar experiences a corrective decline, dipping back to the 104.00 area due to lower US yields and speculations around the Federal Reserve’s potential easing in its May or June meetings, the EUR/USD pair found the opportunity to climb back to the 1.0780 level. This move is further supported by Fed Chair Jerome Powell’s remarks on a cautious approach to interest rate adjustments and Minneapolis Fed Neel Kashkari’s openness to evaluating data before rate cuts, hinting at 2-3 adjustments this year. Meanwhile, the European Central Bank (ECB) Board member Isabel Schnabel highlights the critical phase of monetary policy adjustment in the EU, advocating for prudence amidst challenging economic signals. This juxtaposition of the Fed’s easing potential and the ECB’s cautious stance contributes to the current dynamics of the EUR/USD exchange rate.

On Wednesday, the EUR/USD moved higher and able to reach above the middle band of the Bollinger Bands. Currently, the price is moving just above the middle band with narrower bands, suggesting a potential slightly upward movement to reach the upper band. Notably, the Relative Strength Index (RSI) maintains its position at 49, signaling a neutral outlook for this currency pair.

Resistance: 1.0817, 1.0880

Support: 1.0724, 1.0662

XAU/USD (4 Hours)

XAU/USD Rise Amid Weakening US Dollar and Static Treasury Yields

Gold (XAU/USD) experienced a notable increase, reaching $2,044.64, driven by a combination of Wall Street’s positive momentum and a weakening US Dollar, which struggled throughout the day due to a lack of significant market events. This shift came as investors adjusted their positions following recent announcements from major central banks, which tempered expectations for rate cuts. Despite optimistic remarks from Federal Reserve officials on inflation trends, caution was advised against premature policy adjustments. Concurrently, a decrease in early gains for US Treasury yields, with the 10-year note dropping slightly to 4.09%, contributed to the Dollar’s underperformance, further bolstering gold’s appeal.

On Wednesday, XAU/USD moved higher and was able to reach the upper band of the Bollinger Bands. Currently, the price is moving slightly above the middle band, suggesting a potential upward movement to reach back to the upper band. The Relative Strength Index (RSI) stands at 52, signaling a neutral outlook for this pair.

The US dollar saw a significant boost following strong economic data and is poised for further movement based on upcoming Federal Reserve speakers’ comments.

Despite a slight softening, the dollar had previously surged over two days, fueled by a better-than-expected non-farm payroll report, indicating a robust and strengthening labor market.

The services sector, as shown by the ISM services PMI, has expanded for 13 consecutive months, surpassing expectations and previous readings, hinting at a resilient economy despite tight monetary policies.

Improvements in new orders, prices, and imports within the ISM report suggest strong consumer spending and the impact of increased shipping costs on prices.

The Senior Loan Officer Survey highlighted a growing willingness among credit providers to extend credit and a slight increase in demand for it, contrasting with expectations in a high-interest rate environment.

Economic Indicators and Fed’s Influence

Federal Reserve Speakers and USD Outlook:

The dollar’s trajectory may continue to be influenced by forthcoming comments from Fed speakers on monetary policy and interest rates.

Observations on economic data and cautious approaches to interest rate cuts are anticipated to contribute to the dollar’s recent advances.

This economic resilience and strong data suggest potential delays in starting interest rate cuts, leading to recent gains in US yields and the dollar.

The dollar index (DXY) showcased significant gains, with a focus on whether this momentum can be sustained, especially as it approaches key resistance levels noted in previous months.

Federal Reserve’s Neel Kashkari’s comments on the unexpected strength of the US economy indicate that the current interest rates may not be as impactful due to a higher post-Covid neutral rate.

STOCK MARKET:

Snap Inc.’s Financial Performance and Market Reaction

Snap Inc., the parent company of Snapchat, did not meet Wall Street’s revenue forecasts for the quarter, causing a 30% drop in its stock price.

Despite its innovative features, Snap struggles to secure digital advertising revenue against larger competitors like Facebook’s Meta Platforms and Alphabet.

Comparison with Industry Giants

Internal Challenges Over Macro-Economic Issues

Analysts suggest Snap’s revenue shortfall is due to internal issues rather than broader economic challenges, indicating a failure to leverage a resilient advertising market.

Strategic Focus and Management’s Response

CEO Evan Spiegel emphasized the potential for growth, planning to target advertisers aiming for direct sales or website traffic, moving away from mere brand awareness campaigns.

Snap reported Q4 revenue of $1.36 billion, below the expected $1.38 billion, with its annual revenue for 2023 remaining steady at $4.6 billion.

Operational Adjustments and Future Outlook

Snap announced a 10% workforce reduction, equivalent to 528 employees, as part of its strategy to invest in long-term growth.

The company aims to expand Snapchat’s user base, especially in its most profitable markets like North America and Europe, despite stagnation and modest growth in these regions, respectively.

With 414 million daily active users in Q4, surpassing the anticipated 411.6 million, Snap foresees growth to 420 million users in the next quarter, projecting revenue between $1.1 billion and $1.14 billion against analysts’ expectations of $1.1 billion.

Following these announcements and the earnings call, Snap’s shares significantly declined in after-market trading.

In contrast to Snap’s performance, Meta’s advertising sales increased by 25% in the last quarter, while Google saw an 11% growth in its ad business, including a 16% rise in YouTube ad sales.

Affiliate World Dubai, the ultimate event for top affiliate marketers and ecommerce entrepreneurs, brings together 5,500+ industry players for three days of networking, learning, and expert sessions. Discover cutting-edge strategies and real-life case studies from leaders in affiliate and e-commerce marketing, making it a must-attend for insights and connections.

Smart Vision Summit Oman 2024, the largest conference on investment in the Middle East, unites leaders in finance, investment, and fintech. With keynotes, panels, workshops, and networking, it’s a platform for sharing insights, exploring trends, and exchanging ideas. Open to investors, professionals, entrepreneurs, and enthusiasts, the event covers topics like investment strategies, market trends, technology, risk management, and regulatory updates. Attendees gain insights, discover opportunities, and stay ahead in this dynamic industry.

An elite assembly bringing together Traders, Introducing Brokers, Investors, Financial Institutions, and Brokers in the dynamic Trading and Investing Community. This pivotal platform fosters connections, cultivates relationships, and keeps participants updated on market trends and financial insights. Beyond networking, it offers interactions with industry-leading service providers, enriching skills, knowledge, and investment strategies.

On Tuesday, the stock market witnessed modest gains, driven by positive corporate earnings and the investors’ assessment of future Federal Reserve rate cuts. The S&P 500, Nasdaq Composite, and Dow Jones Industrial Average all saw increases, with standout performances from Palantir Technologies and Spotify Technology after reporting strong quarterly revenues. Despite the optimism from earnings, Federal Reserve Chair Jerome Powell’s remarks have cooled expectations for an immediate rate cut, hinting at a possible delay. This cautious optimism was mirrored in the currency market, where the dollar dipped slightly amidst varying signals from Fed officials and global economic updates. Notably, Treasury yields corrected after a recent surge, influencing currency movements and reflecting the market’s nuanced reaction to inflation concerns, Fed policy expectations, and international economic indicators.

Stock Market Updates

On Tuesday, the stock market experienced gains as investors weighed the latest corporate earnings against expectations for future interest rate cuts by the Federal Reserve. The S&P 500 saw a slight increase of 0.23%, closing at 4,954.23, while the Nasdaq Composite edged up 0.07% to 15,609.00. The Dow Jones Industrial Average experienced a more notable rise, adding 141.24 points or 0.37% to finish at 38,521.36. Significant movements were observed in individual stocks, with Palantir Technologies soaring nearly 31% after reporting a revenue beat for the fourth quarter. Similarly, Spotify Technology’s shares climbed almost 4% following its earnings report, which exceeded expectations and showed an increase in Premium subscribers.

Despite the positive momentum from robust earnings among technology giants, recent comments from Federal Reserve Chair Jerome Powell have tempered expectations for an imminent rate cut. Powell suggested that any potential rate reductions might occur later than the market had hoped, pushing back against the anticipation of a March rate cut. This adjustment in expectations comes as the market sees narrow leadership, raising concerns about the sustainability of the current rally without broader market participation. As the earnings season reaches its midpoint, notable companies such as Amgen, Chipotle Mexican Grill, and Ford are poised to release their financial results after the market closes, potentially influencing future market movements.

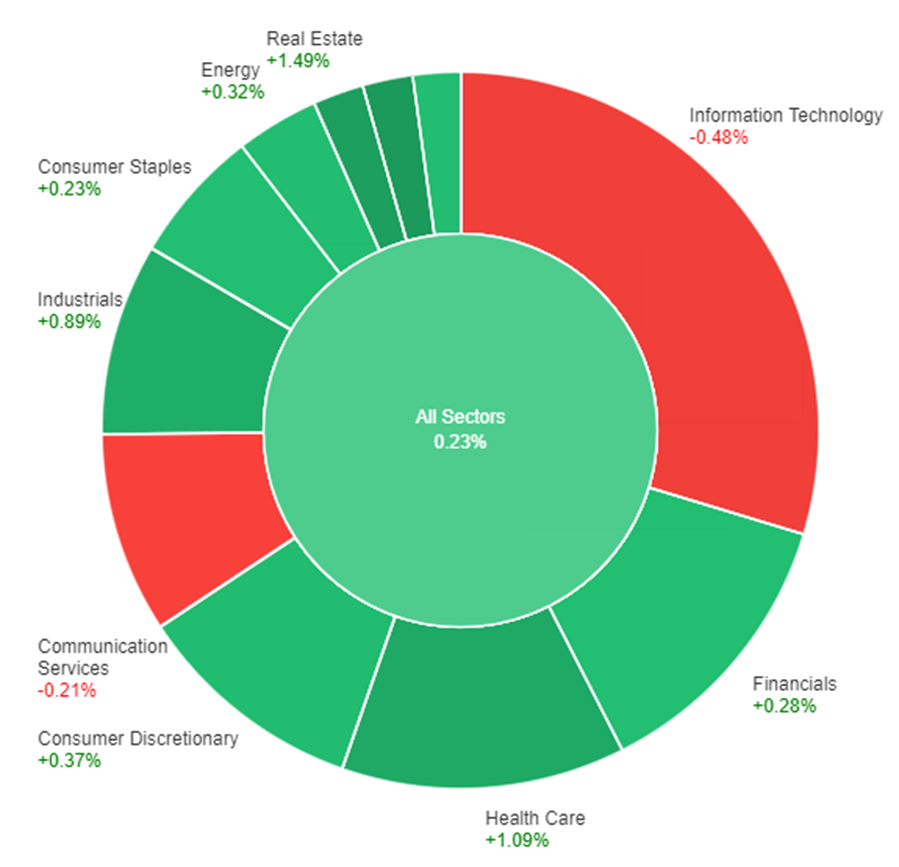

On Tuesday, the overall market saw a modest increase, with all sectors combined going up by 0.23%. The Materials sector led the gains with a notable rise of 1.71%, closely followed by Real Estate and Health Care, which went up by 1.49% and 1.09%, respectively. Industrials also saw a healthy increase, up by 0.89%. Other sectors such as Consumer Discretionary, Energy, Utilities, Financials, and Consumer Staples saw more modest increases, ranging from 0.37% to 0.23%. In contrast, Communication Services and Information Technology experienced declines, down by 0.21% and 0.48% respectively, indicating a mixed performance across different market areas.

Currency Market Updates

In the recent currency market updates, the dollar experienced a slight decline, losing 0.25% against a basket of currencies. It marked a correction following its sharp gains fueled by inflationary pressures evident in U.S. jobs and ISM services reports. This movement in the dollar index was accompanied by a retreat in Treasury yields, which had previously surged but encountered resistance, leading to a correction. The EUR/USD pair managed to recover from early losses, finding support at December’s lows, as the correction in Treasury yields eased the upward pressure on the dollar. This shift comes amid a backdrop of no significant U.S. economic releases, except for the New York Fed’s report on Q4 Household Debt and Credit, which highlighted increasing credit stress among the less creditworthy, even as overall delinquency rates remained lower than pre-pandemic levels.

Further influencing the currency markets, Treasury Secretary Janet Yellen expressed manageable concerns over commercial real estate, while Federal Reserve Bank of Cleveland President Loretta Mester indicated a possibility of gradual rate cuts if inflation continues to decline. The EUR/USD pair also received a boost from a significant rise in German industrial orders, notably influenced by a surge in aircraft orders, despite the broader data suggesting a more nuanced picture. Other currencies like the Sterling saw gains against the dollar, buoyed by improved UK PMI figures and a more risk-friendly market atmosphere, partly due to positive movements in Chinese equities. Meanwhile, the USD/JPY pair corrected after a rapid rise, influenced by Treasury yield adjustments and shifting expectations regarding Fed rate cuts and potential monetary policy adjustments by the Bank of Japan, highlighting the global interconnectedness of currency movements and monetary policies.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Outlook Amidst US Dollar Fluctuations and Central Bank Decisions

As the US Dollar’s demand declines, the EUR/USD pair may see fluctuations influenced by recent central bank decisions and US economic data. With the Reserve Bank of Australia maintaining a cautious stance and the possibility of delayed rate cuts by the Federal Reserve, investor sentiment shifts, impacting bond yields and the USD’s appeal. Additionally, remarks from Federal Reserve officials, including Loretta Mester, could further influence market dynamics and the EUR/USD trajectory, amidst a lack of significant macroeconomic releases.

On Tuesday, the EUR/USD moved flat between the lower and middle bands of the Bollinger Bands. Currently, the price is moving just below the middle band with wider bands, suggesting a potential upward movement to reach the middle band. Notably, the Relative Strength Index (RSI) maintains its position at 42, signaling a neutral but bearish outlook for this currency pair.

Resistance: 1.0817, 1.0880

Support: 1.0724, 1.0662

XAU/USD (4 Hours)

XAU/USD Recovers as US Dollar Demand Weakens Amid Central Bank Caution

Spot Gold (XAU/USD) experienced a recovery on Monday, trading near an intraday high of $2,038.17, as demand for the US Dollar waned following global central bankers’ hints at maintaining current monetary policies, contrary to earlier investor expectations for tighter monetary conditions. This shift came after the Reserve Bank of Australia signaled a possible continuation of rate hikes if necessary, aligning with cautious sentiments from other central banks. Despite strong US macroeconomic data supporting the Dollar and boosting government bond yields, a subsequent rally in bonds and a retreat in yields by Tuesday signaled a market repositioning that favored Gold. This adjustment occurs in a week’s light on macroeconomic announcements but with anticipated comments from Federal Reserve officials, including Loretta Mester.

On Tuesday, XAU/USD moved higher and was able to reach the middle band of the Bollinger Bands. Currently, the price is moving slightly below the middle band, suggesting a potential upward movement to reach the upper band. The Relative Strength Index (RSI) stands at 51, signaling a neutral outlook for this pair.

Has experienced four consecutive weeks of decline.

Dollar strength projected to influence trading dynamics persistently.

Factors Influencing the Euro

New yearly low against the US Dollar due to adjustments in early rate-cut expectations.

US job market’s robust performance last week impacts global financial markets, diminishing prospects of a Federal Reserve rate cut in March.

Market Reaction and Outlook

Euro and Sterling reach multi-week lows against the Dollar.

With a light data week ahead, Dollar’s dominance expected to continue.

Germany’s Economic Data

Disappointing trade figures released, exacerbating the Euro’s challenges.

December’s trade balance improved, but imports and exports dropped more than forecasted.

Exports decreased by 4.6%, and imports by nearly 7%, signaling a tough start to 2024 for Germany’s economy.

Eurozone Economic Concerns

Germany’s economic struggles highlighted by farmers’ protests and train drivers’ strikes

Trade data fuels recession fears, potentially pressing the European Central Bank towards an interest rate cut, with market eyes on April, pending inflation trends

STOCK MARKET:

US Stock Market Performance

Experiences a downturn with Federal Reserve’s cautious stance on rate cuts.

S&P 500 down by 0.3%, indicating a minor pullback from recent highs.

Dow Jones drops by 0.7%, and Nasdaq decreases by 0.2%.

Impact of Federal Reserve’s Position

Jerome Powell’s comments dampen hopes for an imminent interest rate reduction.

Powell emphasizes the risk of acting prematurely before inflation is adequately controlled.

Market Sentiment Shift

Traders adjust expectations, reducing bets on rate cuts for March and May.

Increase in 10-year Treasury yield to 4.17% reflects changing investor outlook.

Corporate Earnings Focus

Market participants turn to corporate earnings for market direction.

Recent positive earnings from Meta and Amazon had fueled a market rally.

McDonald’s Earnings Disappointment

Shares drop over 3% following sales figures not meeting expectations.

Highlights investor reliance on corporate performance in the absence of significant economic news.

{kind=link}