DXY index reflects the US dollar’s rebound on Wednesday.

Day concludes with the dollar retracing from session highs due to Fed minutes causing a pullback in yields.

Focus on Major Currency Pairs and Gold:

Near-term outlook analyzed for major pairs like EUR/USD and USD/JPY.

Fed’s Influence on Dollar Movement:

Last FOMC meeting minutes impact the dollar’s trajectory.

Indicates the potential for sustained high-interest rates and a cautious approach toward easing.

Macro Data Importance:

Fed’s policy outlook in a state of flux.

Macro data becomes crucial in guiding the central bank’s next moves and timing of the first rate cut.

Upcoming Jobs Report:

All eyes on the December nonfarm payrolls survey (NFP) releasing on Friday.

Consensus estimates project 150,000 new jobs, with a potential uptick in the unemployment rate to 3.8%.

Labor Market’s Role in Dollar’s Recovery:

Dollar’s continued recovery hinges on robust and dynamic hiring.

Strong job growth signaling economic resilience could drive yields higher and support the greenback.

Scenario Analysis for Dollar’s Future:

NFP figure above 200,000 considered bullish for the US dollar.

Below-expectation job growth (e.g., under 100,000) could weaken the dollar, confirming expectations for significant rate cuts and indicating economic downshifting.

STOCK MARKET:

Stock Market News Today:

Stocks extend losses at the beginning of the new year.

Nasdaq slides over 1%.

Market Indices Performance:

Dow Jones Industrial Average (^DJI) drops over 0.7% (285 points decline).

S&P 500 (^GSPC) slips approximately 0.8%.

Nasdaq Composite (^IXIC) experiences a nearly 1.2% decline.

Reasons for Stock Decline:

Optimism for swift interest-rate cuts diminishes.

Fresh jobs data and Federal Reserve meeting minutes highlight uncertainty in the timing of rate cuts.

Labor Market Data:

New data from the Bureau of Labor Statistics reveals 8.79 million job openings at the end of November.

Lowest level since March 2021, missing economists’ expectations of 8.82 million openings.

Market Conditions and Expectations:

Year-end market rally expectations take a hit.

Stock indexes and bond prices experience their worst start to a year in decades.

Bonds decline for the fourth consecutive day, pushing the 10-year Treasury yield (^TNX) initially near 4% before reversing to close at roughly 3.91%.

Fed Meeting Minutes Impact:

Stocks show little change after the release of minutes from the recent Federal Reserve meeting.

Minutes indicate Fed officials believe “upside risks” to inflation have diminished.

Majority of participants express the view that a lower target range for the federal funds rate would be appropriate by the end of 2024.

The stock market closed with mixed results as the Nasdaq Composite sustained its longest losing streak since October 2022, dropping by 0.56% while the S&P 500 experienced its fourth consecutive decline. Mega-cap tech stocks, especially Apple, faced significant underperformance due to valuation concerns and Federal Reserve uncertainties. Despite this downturn, some analysts remain optimistic about long-term prospects, expecting the S&P 500 to potentially reach 5,000 by year’s end. Meanwhile, in the currency market, the US Dollar Index showed fluctuations, influenced by investor caution ahead of crucial NFP figures and positive ADP readings. Major currency pairs reacted differently to economic data and risk sentiment, shaping their dynamics against the US dollar, while gold and silver regained momentum amidst the shifting landscape.

Stock Market Updates

The stock market closed with mixed results as the Nasdaq Composite sustained its longest losing streak since October 2022, sliding by 0.56% to 14,510.30. This decline reflects a broader trend, with the index losing nearly 4% since its closing on December 27. Conversely, the S&P 500 experienced a fourth consecutive day of declines, dropping by 0.34% to 4,688.68, while the Dow Jones Industrial Average managed a slight gain of 0.03% to close at 37,440.34. Mega-cap tech stocks like Apple faced substantial underperformance due to concerns over inflated valuations and uncertainty about the Federal Reserve’s potential rate cuts. Apple specifically saw a more than 5% decrease in stock value this week, further exacerbated by recent downgrades from Piper Sandler and Barclays.

Despite the recent market downturn, some analysts remain optimistic about the market’s long-term prospects. He downplays the significance of the recent pullback, considering it more of a statistical fluctuation rather than a substantial indicator of market direction. Suggesting the potential for the S&P 500 to reach around 5,000 by the year’s end, indicating a more than 6% upside from the current levels, highlighting his positive outlook amid the present market fluctuations.

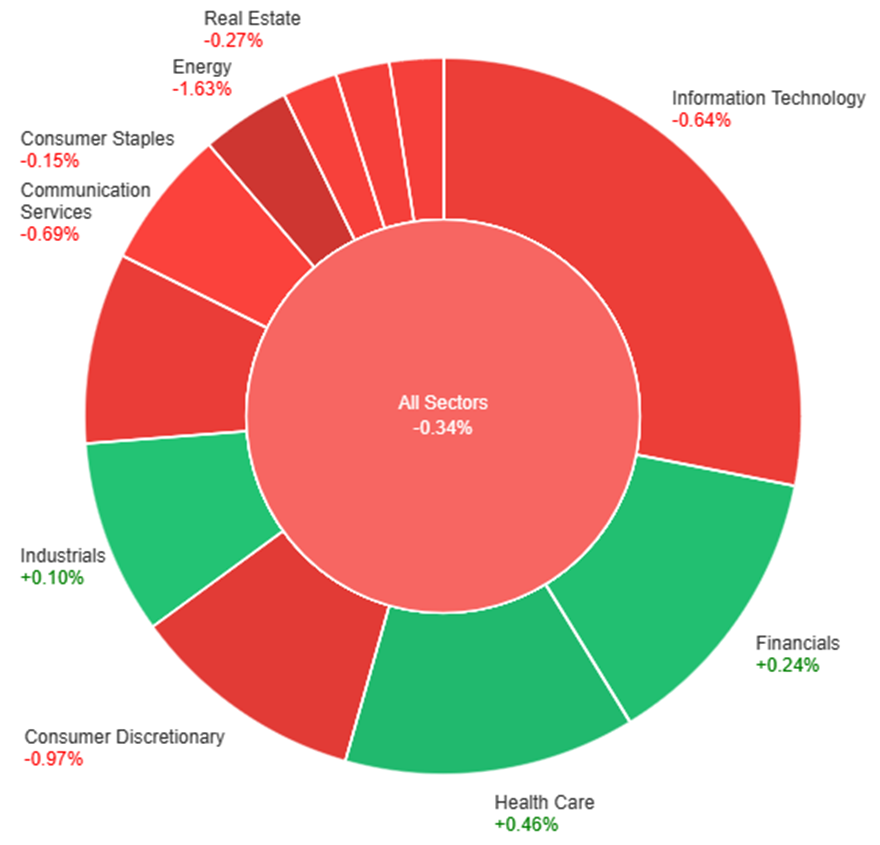

On Thursday, the overall market experienced a slight dip of 0.34%. Among the sectors, Health Care saw a positive uptick of 0.46%, followed by Financials at 0.24% and Industrials at 0.10%. On the downside, Energy suffered the most with a significant decrease of 1.63%, while Consumer Discretionary, Communication Services, and Information Technology also faced notable declines of 0.97%, 0.69%, and 0.64%, respectively. Additionally, Consumer Staples, Real Estate, Utilities, and Materials all experienced minor decreases ranging from -0.15% to -0.33%.

Currency Market Updates

In the latest currency market updates, the US Dollar Index (DXY) showcased a fluctuating performance, hovering around 102.40 following a brief dip to 102.00. Investor caution before the release of crucial NFP figures boosted the dollar amidst mixed risk appetite trends. The positive ADP readings reinforced optimism for December Payrolls, aligning with a rebound in US stocks that revisited the 37700 zone according to the Dow Jones index. The dollar found support from market digestion of the somewhat hawkish tone in the FOMC Minutes and a robust ADP report, while weekly Initial Claims rose by 202K in the week to December 30.

Meanwhile, the EUR/USD pair recovered some ground, touching the 1.0970 zone, and encountering initial resistance despite German flash inflation figures revealing a 3.7% CPI rise in December. GBP/USD initially surged past 1.2700 on upbeat final Services PMI data for December but later retreated to around 1.2660. In contrast, the Japanese yen faced sustained selling pressure, propelling USD/JPY toward the 145.00 barrier amid increased risk appetite and rising US yields. AUD/USD experienced its fifth consecutive drop despite the absence of clear direction in the US dollar and positive readings from China’s Caixin Services PMI. The Canadian dollar, despite weakening, aimed for a retest of two-week highs against the USD ahead of the Canadian labor market report.

Amidst this dynamic landscape, Gold regained momentum, testing the $2040 region per troy ounce, while Silver bounced back from three-week lows, reclaiming the $23.00 per ounce mark despite recent downward trends. The currency market showcased a mix of trends, influenced by economic data, risk sentiment, and fluctuations in key commodities, defining the movement of major currency pairs and their relationship with the US dollar.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Rebounds as Bulls Test Resistance Amidst USD Indecision and Hawkish FOMC Minutes

EUR/USD showed signs of recovery, touching the 1.0970/75 level after a bearish streak. The US dollar lacked clear direction around 102.40 amidst three-week high US yields triggered by a hawkish FOMC tilt, hinting at potential rate reductions by 2024. German inflation figures bolstered the euro, suggesting the ECB might maintain interest rates longer. Meanwhile, a robust ADP report in December hinted at strong Nonfarm Payroll readings, further shaping market sentiments. Bullish momentum faced resistance, indicating a potential standoff in the ongoing currency tussle.

On Thursday, the EUR/USD moved slightly higher and reached the middle band of the Bollinger Bands. Currently, the price moving around the middle band, suggesting a potential downward movement. Notably, the Relative Strength Index (RSI) maintains its position at 44, signaling a neutral but bearish outlook for this currency pair.

Resistance: 1.0980, 1.1068

Support: 1.0892, 1.0814

XAU/USD (4 Hours)

XAU/USD Holds Steady Around $2,040 Amidst Mixed US Data and Fed Meeting Minutes

XAU/USD maintained its position near $2,040 on Thursday after initial gains eased during the American session. The US Dollar faced slight pressure following a mix of US data and insights from the FOMC Meeting Minutes. Despite Fed Chair Jerome Powell’s mention of potential rate cuts, the Minutes didn’t unveil a clear timeline, hinting at a probable move in 2024. Concurrently, the ADP survey indicated robust job growth, surpassing expectations with 164K new positions and signaling alignment with pre-pandemic employment levels. With anticipation for Friday’s Nonfarm Payrolls (NFP) report projecting 170K new jobs, gold remains anchored amidst a landscape of nuanced economic signals.

On Thursday, XAU/USD moved in consolidation and tried to reach the middle band of the Bollinger Bands. Currently, the price moving just below the middle band, suggesting a potential upward movement. The Relative Strength Index (RSI) stands at 44, signaling a neutral but bearish outlook for this pair.

The stock market opened the year with the Nasdaq Composite facing significant losses, marking a 1.18% decrease following the tech giants’ downturn, influenced by Apple’s nearly 4% drop. This decline, paired with the S&P 500 and Dow Jones slipping, reflected a broader tech sell-off. The uncertainty surrounding the Federal Reserve’s rate cut plans triggered this market sentiment, driving the US Dollar Index to a three-week high of around 102.70. While analysts suggest a long-term bullish outlook despite the correction, the Fed’s cautious approach and speculation of rate cuts in 2023 continued to unsettle investors, impacting currency and precious metal markets as the dollar surged further.

Stock Market Updates

The stock market kicked off the year on a rough note, with the Nasdaq Composite leading the downturn. It faced a second consecutive session of losses, closing at 14,592.21, marking a 1.18% decrease. This decline followed the index’s worst day since October, influenced by major tech stocks like Apple, which experienced a nearly 4% drop after a downgrade from Barclays. The S&P 500 slipped by 0.80%, while the Dow Jones Industrial Average slid 0.76%, closing at 4,704.81 and 37,430.19 points, respectively. This downward trend was mirrored by tech giants like Nvidia, Tesla, and Meta, further affected by the U.S. 10-year Treasury yield briefly surpassing the 4% mark, settling around 3.91%. The market sentiment appeared to shift due to uncertainties surrounding the Federal Reserve’s rate cut plans resulting in a sell-off of last year’s high-flying tech winners.

Despite the short-term pessimism, some analysts maintain a long-term bullish outlook, highlighting the current market correction as part of the natural cycle, especially after the remarkable highs of the previous year. However, the release of the Fed’s meeting minutes reinforced the uncertainty, indicating the central bank’s cautious approach to policy changes and the expectation of three-quarter-percentage point cuts sometime during the year. Last year’s market performance, with the S&P 500 surging over 24% and the Nasdaq climbing 43%, marked a substantial rebound from the challenges of 2022 but set the stage for a more cautious and uncertain beginning to the new year.

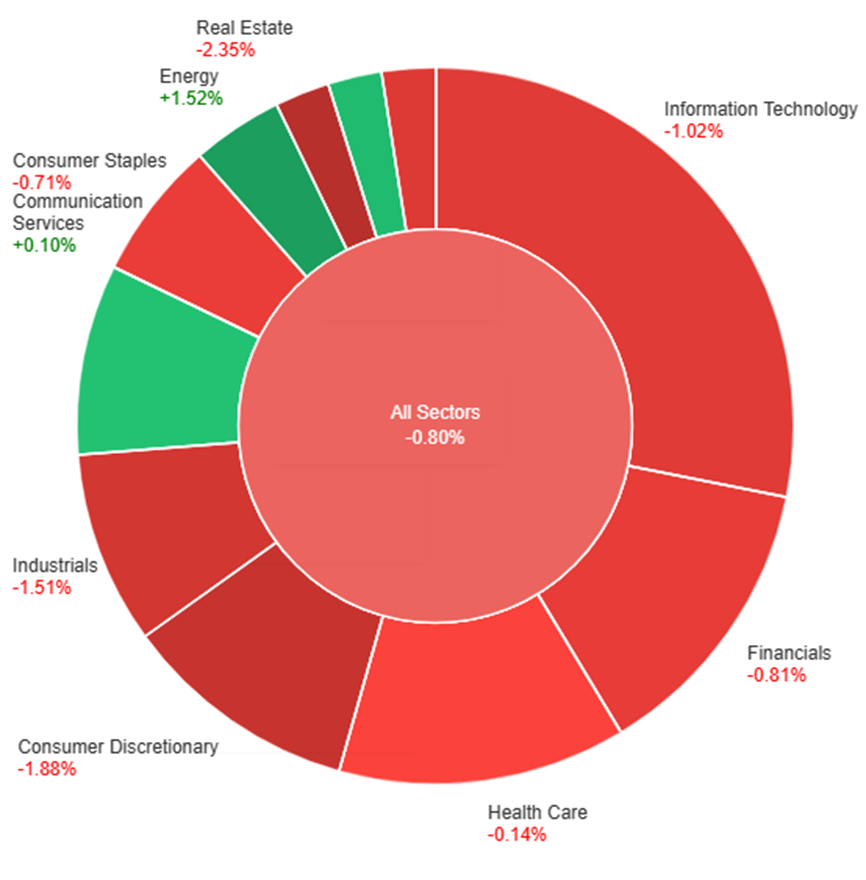

On Wednesday, across all sectors, the market experienced a general decline of 0.80%. Energy and utilities saw modest gains, with energy rising by 1.52% and utilities by 0.39%. Communication services and health care showed slight positive movements of 0.10% and -0.14%, respectively. However, the majority of sectors faced losses: consumer staples (-0.71%), financials (-0.81%), information technology (-1.02%), materials (-1.11%), industrials (-1.51%), consumer discretionary (-1.88%), and real estate (-2.35%). The day marked a mixed performance with select sectors in the positive but a notable downturn in most others.

Currency Market Updates

The currency market experienced notable movements amid a strengthening US Dollar Index (DXY), which surged to a three-week high of around 102.70. This uptrend was propelled by persistent risk aversion in the market and a concurrent increase in US yields across various maturities, reinforcing a bullish sentiment around the dollar. The EUR/USD pair dipped below the 1.0900 mark for the first time since mid-December, reflecting the greenback’s strength and broader weakness in risky assets. Meanwhile, GBP/USD bucked the trend, reclaiming ground above 1.2600 after enduring three consecutive sessions of losses. The USD/JPY pair climbed to approximately 143.70 due to the ongoing uptrend in US yields and a lack of direction in Japan’s JGB 10-year yields. Additionally, AUD/USD faced continued pressure, sliding for the fourth consecutive session amid overall bearish sentiment in high-beta currencies and the commodity complex.

Amidst these fluctuations, the Canadian dollar weakened for the fifth consecutive session, propelling USD/CAD to a two-week high near the 1.3370 zone. The surge in the greenback and US yields impacted precious metals negatively, driving gold prices to multi-day lows around $2030 per ounce and causing silver to breach the $23.00 mark per ounce, reaching a new two-week low. The absence of impactful revelations in the FOMC Minutes sustained the positive momentum for the US Dollar, despite the committee’s indication that rates might reach their peak cycle soon and projections hinting at a potential rate reduction by 2024, a move already anticipated by the market. Some members expressed the possibility of maintaining the policy rate at its current level for an extended period beyond initial expectations, contributing to the ongoing dollar strength.

Throughout the week, the EUR/USD maintained a bearish trajectory, extending its decline below the 1.0900 mark due to a robust US dollar surge, driven by a resurgence in the USD Index to three-week highs around 102.70/75. Despite a positive German job report, the euro struggled against the dollar’s dominance, remaining susceptible to US economic dynamics. Factors contributing to the dollar’s strength included a recovering US yield curve, lower-than-expected JOLTs Job Openings, and surprising upward movement in the ISM Manufacturing PMI. The absence of new information from the FOMC Minutes, which hinted at a potential slowing of interest rate hikes, coupled with remarks from Richmond Fed’s T. Barkin supporting a soft landing for the US economy, further bolstered the greenback’s position midweek.

On Wednesday, the EUR/USD moved lower creating a lower push to the lower band of the Bollinger Bands. Currently, the price moving slightly above the lower band, suggesting a potential upward movement. Notably, the Relative Strength Index (RSI) maintains its position at 30, signaling a bearish outlook for this currency pair.

XAU/USD experienced a continued decline, hovering near $2,031.20 during the mid-US afternoon as the US Dollar maintained its upward momentum against major currencies. The boost in the USD stemmed from positive US news, including a better-than-expected ISM Manufacturing PMI and steady job openings reported by the BLS. These indicators hint at a stabilizing labor market, influencing the Federal Reserve’s stance. As the market anticipates the FOMC Minutes, expected to offer insights into rate cut discussions and potential timing, traders await cues on the Fed’s trajectory, currently pricing in a potential rate cut by May.

On Wednesday, XAU/USD moved lower and reached the lower band of the Bollinger Bands. Currently, the price moving just above the lower band, suggesting a potential upward movement. The Relative Strength Index (RSI) stands at 37, signaling a bearish outlook for this pair.

The new year began with a mild downturn in the stock market, seeing the S&P 500 drop by 0.57% after an impressive 2023. Tech giants like Apple faced setbacks, while defensive stocks supported the Dow Jones. Despite this, the market enjoyed a bullish run in 2023 due to a strong economy and Fed signals. Analysts maintain optimism, anticipating a potential rebound during the earnings season. In currency markets, the dollar rebounded by 0.8% after a dovish Fed stance, influencing various pairs like EUR/USD and USD/JPY. The focus shifts to upcoming U.S. economic indicators and FOMC minutes for insights into potential market shifts.

Stock Market Updates

The stock market kicked off the new year on a slightly bearish note, with the S&P 500 falling by 0.57%, marking its first decline after a strong 2023. The Nasdaq Composite experienced its worst day since October, dropping by 1.63%, while the Dow Jones Industrial Average managed a slight gain of 0.07%. Apple faced a significant setback, sliding over 3% due to a downgrade from Barclays, impacting the performance of the Magnificent Seven market leaders basket. However, defensive stocks like Johnson & Johnson and Merck supported the Dow’s positive momentum.

In 2023, the stock market saw a remarkable surge, with the S&P 500 climbing for nine consecutive weeks, ending the year on a high note—its best streak since 2004. The bullish run was fueled by a resilient economy, cooled inflation, the Federal Reserve signaling an end to rate hikes, and an anticipation of future rate cuts. Tech giants like Apple, Microsoft, and Nvidia led the charge, with the Nasdaq Composite registering its best year since 2020. Despite the initial decline in the new year, analysts like Hatfield remain optimistic about equities, foreseeing a potential rebound during the upcoming earnings season.

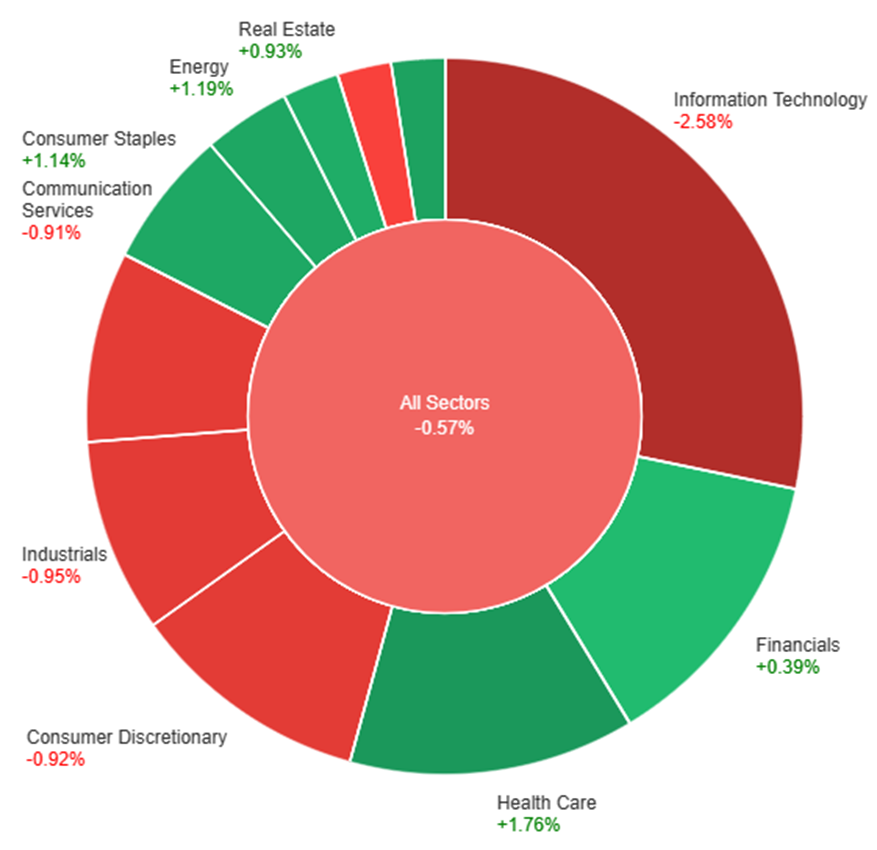

On Tuesday, across all sectors, the market experienced a slight decline of 0.57%. Health Care, Utilities, and Energy sectors showed positive gains, with Health Care leading at +1.76%, followed by Utilities at +1.38% and Energy at +1.19%. Conversely, Information Technology took a significant hit, dropping by -2.58%. Sectors like Consumer Discretionary, Communication Services, and Industrials also experienced declines ranging from -0.91% to -0.95%. Meanwhile, Financials and Real Estate showed modest gains, while Materials faced a small decrease of -0.20%.

Currency Market Updates

The currency markets witnessed a resurgence of the dollar index by 0.8% following profit-taking on short trades that ensued after a more dovish stance from the Fed in mid-December. This unexpected turn led to a tumble in Treasury yields and rate expectations, prompting a surge in risk-taking behavior. The focus now hovers around the upcoming key U.S. labor market data, ISM releases, and the scrutiny of FOMC meeting minutes as market participants gauge the impact of these factors on the dollar’s recent slide and the potential for a reversal.

EUR/USD experienced an 0.82% decline, approaching the 50% retracement level of December’s surge, while USD/JPY rose 0.8%, seeking to breach resistance around 142 to push towards 143. Sterling mirrored the pressures faced by EUR/USD, dropping by 0.77%, largely influenced by lagging gilt treasury yield spreads. Concurrently, USD/CAD ascended by 0.63%, propelled by Canada’s PMI hitting a 3-1/2-year low at 45.4. Market sentiment hinges on upcoming crucial U.S. economic indicators that are expected to confirm a cooling labor market with receding inflationary pressures, yet still shy of the Fed’s 2% target. The interplay of these data releases will likely shape the trajectory of major currency pairs in the coming days.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Declines as Dollar Gains Ground Amidst Economic Contractions

The EUR/USD pair experienced a significant downturn, touching lows of 1.0940 amidst a stronger US Dollar driven by a gloomy market sentiment due to persistent economic contraction signals at the close of 2023. S&P Global’s released PMI data for both the Eurozone and the US showcased a slight improvement in the EU’s manufacturing index while the US saw a contraction, aligning with a risk-averse atmosphere that pushed stocks downward and lifted Treasury yields. Eyes are now on upcoming data, particularly the December US ISM Manufacturing PMI and FOMC Meeting Minutes, as Chairman Jerome Powell hinted at potential rate cuts, prompting curiosity about policymakers’ official discussions.

On Tuesday, the EUR/USD moved lower and reached the lower band of the Bollinger Bands. Currently, the price moving slightly above the lower band, suggesting a potential upward movement. Notably, the Relative Strength Index (RSI) maintains its position at 32, signaling a bearish outlook for this currency pair.

Resistance: 1.0980, 1.1068

Support: 1.0892, 1.0814

XAU/USD (4 Hours)

XAU/USD Holds Steady Amidst Market Caution and Dollar Strength

Spot Gold maintained a steady stance, lingering around its daily opening without a definitive trajectory, recuperating slightly from an intraday dip to $2,055.82. The US Dollar gained traction throughout the European trading session, bolstered by Wall Street’s subdued performance. Investor apprehension loomed after the long weekend, accentuated by the forthcoming pivotal US employment data and a lineup of significant economic indicators. The sentiment downturn followed the disappointing US S&P Global Manufacturing PMI, overshadowing the better-than-expected European Manufacturing PMIs. This cautionary atmosphere was compounded by US stocks dipping and government bond yields edging upwards, indicating renewed market apprehension regarding projected rate cuts across major economies. Eyes remain fixed on the imminent US employment reports and upcoming European inflation updates, shaping the short-term technical outlook for XAU/USD.

On Tuesday, XAU/USD moved lower and reached the lower band of the Bollinger Bands. Currently, the price moving just above the lower band, suggesting a potential upward movement. The Relative Strength Index (RSI) stands at 46, signaling a neutral outlook for this pair.

Economic data: S&P Global US Services PMI, December, final (48.4 expected, 48.2previously); MBA Mortgage Applications, week ending December 29

CURRENCIES:

U.S. Dollar’s Downward Correction

Witnessed a significant downward correction in the U.S. dollar due to expectations of the Federal Reserve reducing borrowing costs.

US Treasury yields plunged in the last quarter of 2023, contributing to the dollar’s lowest level in five months.

Currency and Precious Metal Performance

EUR/USD and GBP/USD experienced a notable surge, reaching multi-month highs in late December.

Gold prices showed strength, concluding 2023 above $2,000, though slightly below its all-time high.

The bullish trend in gold is expected to continue, benefiting from the Federal Reserve’s policy shift.

Equity Market Rally

The pullback in U.S. bond yields triggered a substantial rally in the equity market.

Major stock market indexes reached new records, reflecting the prevailing risk-on sentiment.

Outlook for Q1 2024

U.S. dollar may continue to face losses in the coming months due to downward-sloping yields.

Anticipated upward momentum for gold, EUR/USD, GBP/USD, and stocks in Q1.

Caution advised as some markets approach potential overbought conditions.

Increased Volatility and Trading Setups

Expect different market dynamics leading to heightened volatility.

Opportunities for enticing trading setups in major assets, including currencies, commodities (gold, silver, oil), and cryptocurrencies.

STOCK MARKET:

Fed Rate Cut Speculation:

Morgan Stanley’s Ellen Zentner suggests a possible Fed rate cut may come later than market expectations.

Zentner emphasizes that monthly payroll additions below 50,000, coupled with consistent low inflation, could trigger a March rate cut.

Caution is advised, highlighting that a single weak jobs report might not be sufficient for a rate cut decision.

Morgan Stanley’s Base Case:

The base case for Morgan Stanley remains a Fed cut in May, contrary to earlier market expectations.

Late 2023 Market Rally Impact:

Investors face the question of whether the late 2023 market rally accelerated the gains expected in 2024 or if there is room for further upward movement.

Ryan Detrick, Chief Markets Strategist at Carson Group, cites historical data indicating that after a late-year S&P 500 rally exceeding 10%, the benchmark average historically rose by an average of 19.5% in the following year.

Contrasting Views on Market Continuation:

Tom Lee, Fundstrat’s Head of Research, acknowledges the likelihood of new all-time highs for the S&P 500 but anticipates a subsequent consolidation.

Lee points out key concerns, including investor uncertainty about the Fed’s rate-cut timing and a potential downturn around February or March in an election year.

Tom Lee’s Market Outlook:

Lee predicts a brief pullback after new all-time highs, suggesting a range of S&P 500 at 4,400-4,500.

Consistent with the 2024 Year Ahead Outlook, Lee’s base case envisions most gains for the S&P 500 in the second half of 2024.

The inaugural week of 2024 is poised to be a dynamic period for traders and investors, with a spotlight on critical economic indicators that are expected to shape market sentiments. Among the pivotal data releases are the ISM Manufacturing and Services PMI from the US, the German Preliminary CPI from the EU, and the highly anticipated US and Canada Employment Change figures. This overview aims to guide you through the key developments and predictions, with a specific emphasis on the potential impact on major currencies, particularly the US Dollar.

It’s crucial for traders to be cautious and stay on top of the latest developments for a successful week of trading.

ISM Manufacturing PMI (3 January 2024)

The ISM Manufacturing PMI, holding steady at 46.7 in November 2023, is expected to modestly increase to 47.1 in the upcoming release on 3 January 2024.

FOMC Meeting Minutes (4 January 2024)

The Federal Reserve maintained the fed funds rate at 5.25%-5.5% for a third consecutive meeting in December 2023. However, they have hinted at a potential 75 basis points cut in 2024. Therefore the meeting minutes on 4 January 2024 will provide insights into the Fed’s latest monetary policy stance, reflecting the current economic indicators, including slowed growth, moderated job gains, and persistent but slightly eased inflation.

German Prelim CPI (4 January 2024)

After a 0.4% decline in November 2023, Germany’s Preliminary CPI, anticipated on 4 January 2024, is expected to rebound with a projected increase of 0.2%.

Canada Employment Change (5 January 2024)

Following positive employment numbers in October and November of 2023, Canada is poised to release its December 2023 employment data on 5 January 2024. Forecasts suggest an increase of 12K jobs, but with a marginal uptick in the unemployment rate to 5.9%.

US Non-Farm Employment Change (5 January 2024)

November 2023 saw a robust addition of 199k jobs in the US, surpassing October figures. The upcoming release on 5 January 2024 is anticipated to reveal a positive trend with an estimated increase of 163,000 jobs, while the unemployment rate is expected to inch up to 3.8%.

US ISM Services PMI (5 January 2024)

Closing the week, the US ISM Services PMI, reflecting growth in the services sector, is projected to experience a marginal decline from 52.7 to 52.6 in the December figures, set for release on 5 January 2024.

As traders embark on the first week of 2024, vigilance and adaptability will be key. Stay informed, monitor the latest developments, and be prepared for potential market shifts in response to these critical economic indicators.

In the penultimate trading session of the year, the S&P 500 approached an all-time high, indicating a robust finish to an exceptionally bullish year for stocks. The Dow Jones Industrial Average secured a new record, while the Nasdaq Composite saw a slight dip. With major indices poised to end 2023 on gains, projected around 13.8% for the Dow and 24.6% for the S&P, the Nasdaq’s remarkable 44.2% rise stands out, buoyed by tech giants and fervor over AI. As the market anticipates the traditional “Santa Claus rally,” the late 2023 surge sets an optimistic tone for 2024, backed by positive technical indicators and expectations of rate cuts and reduced inflation. In the currency market, the US Dollar Index fluctuated significantly, buoyed by rising Treasury yields, impacting major pairs like EUR/USD and GBP/USD. Additionally, USD/JPY and AUD/USD experienced noteworthy volatility, while gold faced a pullback amidst the USD resurgence and climbing yields, reflecting the complex interplay of economic factors and geopolitical events shaping currency movements.

Stock Market Updates

In the penultimate trading day of the year, the S&P 500 edged slightly higher, nearing an all-time high at 4,783.35, signaling a robust end to a bullish year for stocks. The Dow Jones Industrial Average also achieved a new record, closing at 37,710.10, while the Nasdaq Composite experienced a minor dip to 15,095.14. Notably, all major indices are set to conclude 2023 with gains, with the Dow and S&P projected to finish up nearly 13.8% and 24.6%, respectively. The Nasdaq stands out with a remarkable 44.2% climb, its most substantial increase since 2003, primarily fueled by the resurgence of mega-cap tech companies and the fervor surrounding artificial intelligence.

Amidst this year-end rally, the market looks forward to the “Santa Claus rally,” historically observed in the final days of a year and the early days of the subsequent one. The market’s impressive late-2023 surge, rebounding from a sluggish third quarter, positions the S&P with an 11.6% quarterly increase, marking its strongest quarterly performance in three years. As 2023 concludes, the optimistic sentiment continues, with a positive technical outlook and expanding market breadth anticipated to set the stage for a promising 2024. Forecasts pivot on expectations of forthcoming rate cuts and sustained alleviation in inflation, creating what’s termed a “perfect storm” for stocks in the coming year.

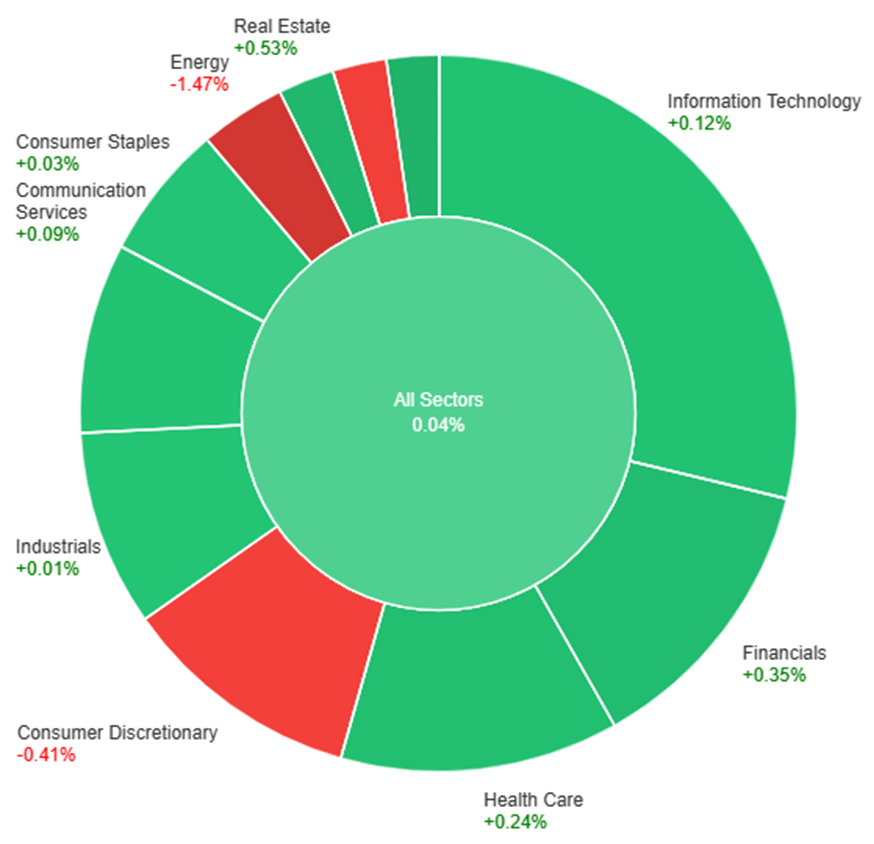

On Thursday, most sectors experienced modest gains, with Utilities leading at +0.70%, followed closely by Real Estate at +0.53% and Financials at +0.35%. Health Care, Information Technology, and Communication Services saw smaller increases ranging from +0.12% to +0.24%. However, Consumer Discretionary and Materials faced declines of -0.41% and -0.46% respectively. Energy witnessed a significant drop of -1.47%, marking the most substantial decrease among all sectors for the day.

Currency Market Updates

In the currency market update, the US Dollar Index (DXY) demonstrated significant volatility, bottoming out at 100.86 before sharply rebounding to 101.25. The Greenback’s resurgence was propelled by a surge in US Treasury yields, reaching 3.85% following a successful auction of the 7-year note. Despite the correction, with higher yields contributing to its recovery, the overall trend for the USD remains downward, albeit with potential for further correction.

EUR/USD faced its steepest decline in two weeks, sliding from a monthly high of 1.1139 to the 1.1055 area. The pair’s movement was influenced by Spain’s impending inflation figures and Eurostat’s scheduled release of Eurozone figures, both expected to provide significant insights into the euro’s trajectory. Similarly, GBP/USD retreated from above 1.2800 to around 1.2700, with the UK’s final economic report for 2023 focusing on Nationwide Housing Prices for December.

USD/JPY experienced notable volatility, plunging to 140.23—the lowest level since July—before recovering to 141.40, supported by rising yields. AUD/USD reached a peak at 0.6871 but failed to maintain momentum, slipping to 0.6835. The Australian Dollar faces immediate support at 0.6825, while a potential upswing could occur if it surpasses 0.6850.

Gold faced a pullback from $2,088 to $2,065 due to the rebounding US Dollar and rising yields. Despite the overarching upward trend, current conditions hint at a potential downside bias ahead of the Asian session for the precious metal. These fluctuations across currency pairs and gold prices reflect the intricate interplay between economic indicators, market sentiments, and geopolitical events driving currency market movements.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Falters Despite US Economic Data; Eyes on Eurozone Inflation

The EUR/USD faced setbacks as it slipped below 1.1100, driven by a surge in US Treasury yields despite mixed American economic reports. The US Dollar remained resilient, largely unaffected by the jobless claims uptick and stagnant pending home sales. Amidst Wall Street’s festive rally, the greenback found strength with a rebound in yields post a 7-year note auction, sidelining the impact of economic data. Attention turns to Spain’s preliminary CPI figures for December, crucial for insight into Eurozone inflation, likely to shape the pair’s trajectory.

On Thursday, the EUR/USD moved lower and reached the middle band of the Bollinger Bands. Currently, the price moving slightly above the middle band, suggesting a potential upward movement. Notably, the Relative Strength Index (RSI) maintains its position at 55, signaling a neutral outlook for this currency pair.

Resistance: 1.1138, 1.1222

Support: 1.1043, 1.0946

XAU/USD (4 Hours)

XAU/USD Continues Surge Amid Dollar Weakness and Investor Optimism

Gold prices are on the rise as the US Dollar faces pressure amidst a buoyant Asian stock market. Investor enthusiasm for anticipated aggressive interest rate cuts by the Fed, coupled with China’s commitment to bolster domestic demand and liquidity injections by the PBOC, fuels risk appetite, edging the Dollar lower. Despite a slight rebound in US Treasury bond yields, Gold maintains its upward momentum, nearing the $2,100 mark in Asian trade. The Dollar Index hovers near five-month lows, while US Treasury bond yields, after bouncing off multi-month lows, stand at 3.81%, up 0.50% on the day. Wednesday’s market return saw Gold hit a record close above $2,070, propelled by a Dollar sell-off post-positive US auctions. Anticipation of Fed rate cuts continues to drive demand for stocks and bonds, influencing Treasury yields. With the focus shifting to mid-tier US Jobless Claims and a seven-year bond auction, Gold traders remain vigilant amid pre-New Year thin liquidity conditions, expecting potential upside boosts.

On Thursday, XAU/USD moved lower and reached the middle band of the Bollinger Bands. Currently, the price moving at the upper band, suggesting a potential upward movement. The Relative Strength Index (RSI) stands at 53, signaling a neutral outlook for this pair.

Resistance: $2,088, $2,103

Support: $2,065, $2,048

Written on December 29, 2023 at 3:10 am, by anakin