Stocks faced a downturn for the second consecutive session, driven by declines in major technology firms like Apple, which saw nearly a 3% drop following a report of decreased iPhone sales in China, leading the Nasdaq Composite down by 1.65%. The Dow Jones and S&P 500 also experienced significant losses. Despite the broader tech sector’s struggles, companies such as Target and AeroVironment outperformed expectations, showcasing resilience amidst market reassessment of recent highs driven by AI optimism. Bitcoin’s volatility highlighted the fluctuating nature of digital currencies. Meanwhile, the currency market reacted to weaker-than-expected US economic data, influencing expectations of the Federal Reserve’s monetary policy, with the dollar showing mixed responses against major currencies as the market anticipates key economic updates and Federal Reserve Chair Jerome Powell’s testimony.

Stock Market Updates

Stocks experienced a downturn for the second consecutive session on Tuesday, led by significant declines in major technology companies like Apple, which contributed to pulling the broader market away from its recent record highs. The Nasdaq Composite saw a notable decrease of 1.65%, closing at 15,939.59, primarily due to the downturn in technology stocks. Similarly, the Dow Jones Industrial Average fell by 404.64 points, or 1.04%, ending the day at 38,585.19, while the S&P 500 dropped by 1.02%, to close at 5,078.65. The decline in Apple’s stock, nearly 3%, was sparked by a report from Counterpoint Research indicating a significant drop in iPhone sales in China during the first six weeks of 2024. Other major tech companies, including Netflix, Microsoft, and Tesla, also faced declines around 3% to nearly 4%, with the S&P 500’s information technology sector leading the downturn with a loss of more than 2%.

Despite the broader tech sell-off, some companies managed to buck the negative trend. Target saw its shares jump 12% following a report of strong holiday-quarter earnings that surpassed Wall Street expectations. Similarly, AeroVironment experienced an almost 28% surge after delivering a positive quarterly report and outlook, which exceeded analyst forecasts. These movements occurred as investors are reassessing the market’s recent surge to all-time highs, fueled by optimism surrounding artificial intelligence. Even with the downturn over the past two sessions, the three major stock averages remain significantly higher for the year. Additionally, Bitcoin reached a new record high on Tuesday, though it quickly retreated into the red after surpassing its peak for the first time in two years, highlighting the volatile nature of digital currencies amidst broader market fluctuations.

Data by Bloomberg

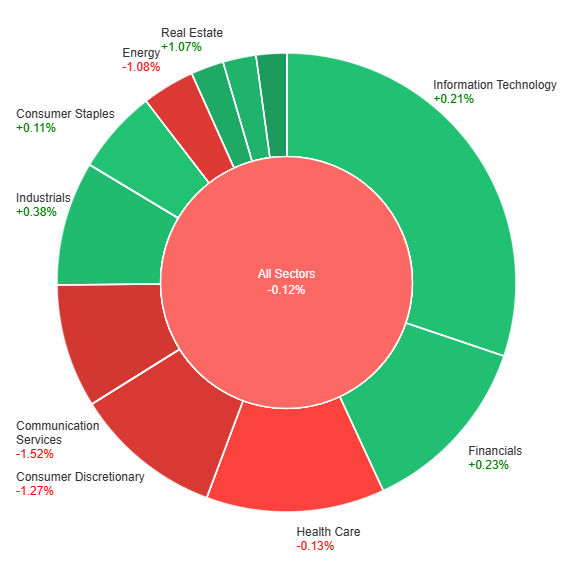

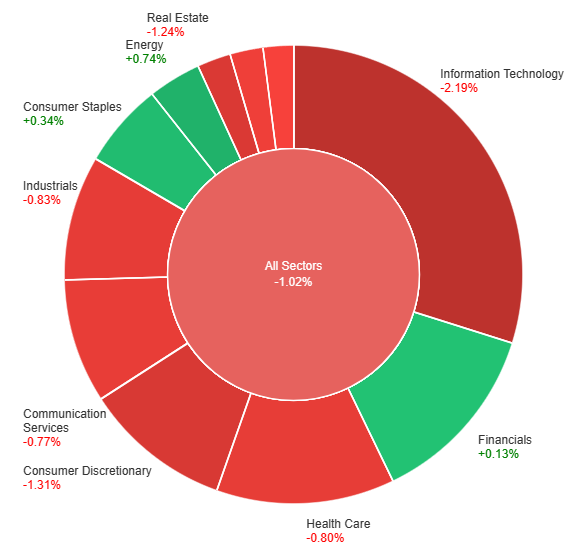

On Tuesday, the market saw an overall downturn, with all sectors combined dropping by 1.02%. Despite this general decline, some sectors managed to post gains; Energy led with a 0.74% increase, followed by Consumer Staples and Financials, which rose by 0.34% and 0.13% respectively. However, the majority of sectors experienced losses, with Utilities, Materials, and Communication Services seeing declines of less than 1%. More significant losses were recorded in Health Care, Industrials, and Real Estate, with Consumer Discretionary and Information Technology facing the steepest drops at -1.31% and -2.19%, respectively, indicating a challenging day for these sectors.

Currency Market Updates

In the latest currency market updates, the USD index experienced a slight decline, down by 0.1% during North American afternoon trading, recovering from more significant losses that ensued after the release of weaker-than-expected factory orders and ISM non-manufacturing data. This weaker data has revived market expectations for a potentially more dovish monetary policy path from the Federal Reserve in 2024. As the market anticipates the forthcoming ADP and JOLTS data, alongside Federal Reserve Chair Jerome Powell’s semi-annual monetary policy testimony before the House Financial Services Committee, current market and Federal Reserve dot plot expectations align closely. However, this equilibrium might shift should forthcoming data indicate a softer economic outlook, or if Powell hints at a decreased hesitancy to lower interest rates, potentially affecting yields and pressuring the dollar downwards.

Amid these developments, major currency pairs have shown varied reactions. The EUR/USD pair saw a modest increase of 0.04% in afternoon trading, staying below its peak following the US data release. The muted response suggests traders are cautious, anticipating that the European Central Bank (ECB) might mirror any significant policy shifts by the Fed. Meanwhile, the USD/JPY pair declined to a low of 149.70 after the release of the soft ISM data, influenced by narrowing U.S.-Japan interest rate differentials, which prompted some dollar selling. The GBP/USD pair notably rallied, breaking significant resistance levels, buoyed by the prospect of diverging monetary policies between the U.S. and the UK, particularly in light of the UK’s high inflation rates. Elsewhere, commodities such as Bitcoin and gold recorded new highs before retracting slightly, benefiting from a dip in global yields and indicating a rising interest in USD alternatives amid the current economic climate.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Navigates Uncertain Waters Amid Mixed Central Bank Signals

Following a disappointing US ISM Services PMI report, EUR/USD momentarily reached a two-week high near 1.0880, only to see those gains diminish. Despite a temporary dip, the USD Index (DXY) found some footing, yet remained subdued amid anticipation of Federal Reserve Chair Powell’s testimonies and the upcoming ECB interest rate decision. The currency pair’s fluctuations reflect broader market speculations on future interest rate adjustments by both the Federal Reserve and the European Central Bank, amidst contrasting economic signals from the US and Eurozone. Federal Reserve officials have voiced varying stances on the timing and conditions for rate cuts, reflecting uncertainty in monetary policy directions. Meanwhile, the ECB hints at a possible easing cycle beginning soon, further complicated by mixed inflation data from Europe. These dynamics suggest a potentially stronger dollar in the short term, with EUR/USD possibly facing a downward correction towards its year-to-date lows, amid the backdrop of concurrent monetary easing by both central banks.

On Tuesday, the EUR/USD moved higher and was able to reach the upper band of the Bollinger Bands. Currently, the price is moving just above the middle band, suggesting a potential upward movement to reach the upper band. Notably, the Relative Strength Index (RSI) maintains its position at 52, signaling a neutral outlook for this currency pair.

Resistance: 1.0858, 1.0888

Support: 1.0838, 1.0812

XAU/USD (4 Hours)

XAU/USD Hits Record High Amid Weak US Economic Data and Stock Market Retreat

On Tuesday, Spot Gold surged to a new all-time peak of $2,141.81, buoyed by a combination of softer-than-expected US economic indicators and a downturn in stock markets. The precious metal’s ascent was particularly sparked by disappointing figures from the Institute for Supply Management (ISM) regarding the services sector and a significant drop in January’s Factory Orders. Moreover, the retreat in US Treasury yields, with the 10-year note dipping to its lowest in a month at 4.14%, alongside declines across major US stock indexes, notably a 1.64% fall in the Nasdaq Composite, further propelled gold’s upward trajectory.

On Tuesday, XAU/USD moved higher to reach the upper band of the Bollinger Bands. Currently, the price is moving just below the upper band, suggesting a potential higher movement to reach above the upper band and reach the resistance level. The Relative Strength Index (RSI) stands at 78, signaling a strong bullish outlook for this pair.

Resistance: $2,147

Support: $2,100, $2,079

Economic Data

| Currency | Data | Time (GMT + 8) | Forecast |

|---|---|---|---|

| AUD | GDP q/q | 08:30 | 0.2% (Actual) |

| USD | ADP Non-Farm Employment Change | 21:15 | 107K |

| GBP | Annual Budget Release | Tentative | |

| CAD | BOC Rate Statement | 22:45 | |

| CAD | Overnight Rate | 22:45 | 5.00% |

| USD | JOLTS Job Openings | 23:00 | 9.03M |

| CAD | BOC Press Conference | 23:30 |