· The U.S. dollar saw a modest increase, with its strength limited by low U.S. Treasury yields, indicating market caution.

· Traders are eagerly awaiting the core PCE deflator data, a key inflation metric preferred by the Federal Reserve, which could significantly impact the central bank’s policy direction and market volatility.

· Predictions for January’s core CPI suggest a 0.4% month-over-month increase and a slight annual deceleration from 2.9% to 2.8%, indicating a minimal shift towards lower inflation.

· Recent CPI and PPI reports for the same period have been significantly higher than expected, suggesting that investors might be underestimating inflation risks, which could lead to surprises in the upcoming data.

· A higher-than-expected PCE report may lead to Wall Street adjusting its expectations for Federal Reserve rate cuts in 2024 and could delay the anticipated easing cycle, potentially increasing U.S. Treasury yields and the U.S. dollar value while negatively affecting gold prices.

· Analysis of FOMC meeting probabilities as of February 28 reflects market anticipation and interest rate expectations.

· The article will also cover technical analyses for currency pairs EUR/USD, USD/JPY, GBP/USD, and gold, focusing on recent price trends and identifying key levels for potential buying or selling pressure, useful for risk management in trading strategies.

STOCK MARKET:

· US stock futures dropped slightly as investors awaited the Federal Reserve’s important inflation metric to discern future interest rate directions. Bitcoin continued its ascent, surpassing $63,000.

· S&P 500 and Nasdaq 100 futures both saw a decrease of around 0.3%, while European stocks experienced slight gains amidst a busy earnings announcement day. Notable movements included Moncler SpA’s rise after exceeding profit expectations, Air France-KLM’s drop due to a fourth-quarter loss, and Anheuser-Busch InBev’s decline after failing to meet profit forecasts.

· The market is preparing for the release of the US core personal consumption expenditure (PCE) data, expected to highlight the Federal Reserve’s challenge in reaching its 2% inflation target. This data could indicate the Fed’s continued cautious approach towards easing monetary policy.

· Asian stock markets improved, led by a rebound in Chinese shares. The yen experienced a notable increase against the dollar following indications from the Bank of Japan that it might end its negative interest rate policy.

· Bitcoin’s value neared $64,000, continuing its growth spurred by new demand from exchange-traded funds, approaching its record high of just below $69,000 set in 2021.

· Treasury yields rose slightly after a bond rally, with the 10-year yield decreasing by four basis points and the two-year yield by six points, as per the previous day’s trading.

· Comments from New York Fed President John Williams and Atlanta Fed chief Raphael Bostic emphasized the ongoing battle against inflation and urged patience with policy adjustments, respectively.

· Market predictions align with Federal Reserve officials’ December projections, anticipating roughly 80 basis points of easing by year’s end, equivalent to three rate cuts.

· The dollar weakened against other currencies, particularly the yen, as traders expect a narrowing interest rate gap between Japan and the US.

· Upcoming key events include economic data releases from Germany and the US, statements from Federal Reserve officials, and PMI reports from China and the Eurozone.

On Wednesday, stocks saw a decline as investors awaited an important inflation report due later in the week, with the S&P 500, Nasdaq Composite, and Dow Jones Industrial Average all experiencing losses. Notable decliners included UnitedHealth, Intel, Alphabet, and Urban Outfitters, the latter due to disappointing quarterly results. The market’s attention is now on January’s forthcoming personal consumption expenditure (PCE) data, a crucial inflation indicator for the Federal Reserve. This anticipation comes amid mixed movements in the currency market, where the dollar index made slight gains while investors closely monitor upcoming inflation reports from the U.S. and the eurozone. These reports are pivotal for future monetary policy and interest rate expectations, especially with predictions leaning towards rate cuts by the Federal Reserve and the European Central Bank (ECB) within the year, amidst contrasting inflationary trends in the U.S. and eurozone.

Stock Market Updates

Stocks experienced a decline on Wednesday as the market anticipated an important inflation report set to be released later in the week. The S&P 500 dropped slightly by 0.17%, closing at 5,069.76, while the Nasdaq Composite experienced a more significant fall of 0.55%, ending at 15,947.74. The Dow Jones Industrial Average also saw a minor decrease, losing 23.39 points, or 0.06%, to close at 38,949.02, marking its third consecutive day of losses. Among the notable decliners were UnitedHealth, which fell nearly 3%, and tech giants Intel and Alphabet, which dropped 1.7% and 1.8%, respectively. Additionally, Urban Outfitters saw a significant decrease of 12.8% following its announcement of weaker-than-expected fourth-quarter results.

The market’s focus is now on the upcoming personal consumption expenditure reading for January, a critical inflation measure closely watched by the Federal Reserve. This report is highly anticipated as investors and analysts gauge the potential for continued economic growth and the impact of inflation on monetary policy. The market’s recent performance has been less robust, with the major indexes on track for their second negative week in the last three, despite having reached record highs recently. The downturn, especially in the tech sector, has sparked debates about the durability of the market rally, which has been partly driven by enthusiasm over advancements in artificial intelligence.

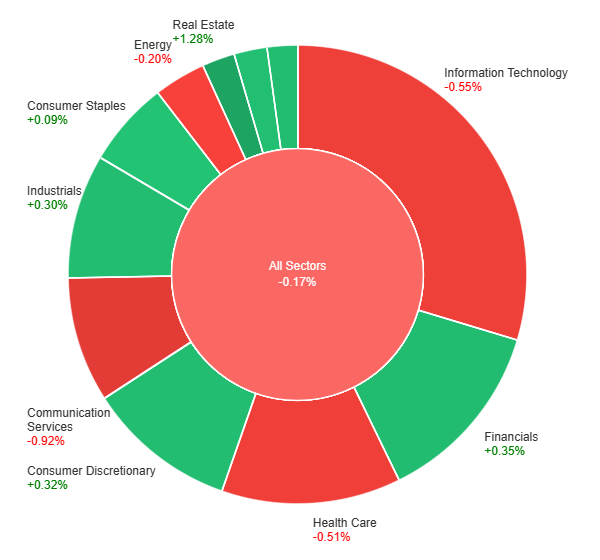

On Wednesday, the overall market experienced a slight downturn, with all sectors combined seeing a decrease of 0.17%. Despite this general downtrend, several sectors managed to post gains, led by Real Estate, which saw a notable increase of 1.28%. Other sectors that experienced growth included Financials, Consumer Discretionary, Utilities, Industrials, Materials, and Consumer Staples, with increases ranging from 0.09% to 0.35%. On the flip side, some sectors faced declines, with Energy, Health Care, Information Technology, and Communication Services witnessing drops between -0.20% and -0.92%, indicating a mixed performance across different areas of the market.

Currency Market Updates

The currency market is currently experiencing nuanced movements as investors anxiously await inflation reports from the U.S. and eurozone, which could significantly influence the trajectory of risk-sensitive currencies. The dollar index saw a slight increase of 0.1%, though it retreated from its early Wednesday highs, indicating a cautious stance among traders. The EUR/USD pair dipped marginally by 0.05%, recovering after testing key support levels amid a broad-based rise in the dollar earlier in the day. The focus now shifts to Thursday’s release of the U.S. core PCE and eurozone CPI reports, which are expected to play a critical role in determining whether the recent reduction in anticipated Fed rate cuts for 2024—and the consequent support this has lent to the dollar—will continue or come to a halt.

Market expectations are leaning towards the Federal Reserve beginning to cut rates by June, with a total of 81 basis points of easing anticipated by the end of the year. Similarly, a June rate cut by the ECB is fully priced in, with expectations of 90 basis points of cuts throughout the year. These developments come as core PCE in the U.S. is forecasted to rise, contrasting with December’s figures, and with the euro zone’s overall and core CPI also set for release, offering further insights into inflationary trends. Amidst this backdrop, the USD/JPY pair has seen a slight increase, attempting to continue its upward trend as markets digest varying signals from Fed speakers and global economic indicators, highlighting the interconnectedness of global financial markets and the significant impact of central bank policies and economic data on currency valuations.

The EUR/USD pair experienced a decline early Friday, pressured by disappointing sentiment indicators from Europe and a significant disparity in US GDP figures that maintained the currency pair’s position within a familiar range midweek. With a packed schedule, Thursday’s focus shifts to German Retail Sales and CPI data, alongside the US Personal Consumption Expenditure (PCE) Price Index inflation figures. The week will conclude with Friday’s release of the pan-European Harmonized Index of Consumer Prices (HICP) inflation data and the US ISM Manufacturing PMI for February, providing critical insights into economic health and potential currency movement directions.

On Wednesday, the EUR/USD moved slightly lower and was able to reach the lower band of the Bollinger Bands. Currently, the price is moving just below the middle band, suggesting a potential upward movement to reach above the middle band. Notably, the Relative Strength Index (RSI) maintains its position at 51, signaling a neutral outlook for this currency pair.

Resistance: 1.0858, 1.0896

Support: 1.0823, 1.0783

XAU/USD (4 Hours)

XAU/USD Steady Amid Economic Expansion and Fed Remarks

Gold prices remained stable near $2,030 on Wednesday, achieving a modest increase of 0.17% as the US economy showed signs of expansion according to the latest BEA report. Despite the US GDP for the last quarter of 2023 slightly missing expectations and mixed retail and wholesale inventory data, a fall in US Treasury bond yields has supported gold prices, keeping them near monthly and weekly highs, just below the 50-day SMA. Meanwhile, comments from Federal Reserve Regional Presidents, Susan Collins and John Williams, about potentially easing policy later in the year while still not meeting the core inflation goal of 2%, have influenced market sentiment, alongside a cautious Wall Street trading mostly in the red.

On Wednesday, XAU/USD moved slightly higher to reach the upper band of the Bollinger Bands. Currently, the price is moving just below the upper band, suggesting a potential higher movement to reach above the upper band and reach the resistance level. The Relative Strength Index (RSI) stands at 57, signaling a neutral but bullish outlook for this pair.

Resistance: $2,042, $2,056

Support: $2,030, $2,017

Economic Data

Currency

Data

Time (GMT+8)

Forecast

EUR

German Prelim CPI m/m

All day

0.5%

CAD

GDP m/m

09:30

0.2%

USD

Core PCE Price Index m/m

09:30

0.4%

USD

Unemployment Claims

09:30

209K

Written on February 29, 2024 at 4:12 am, by anakin

On Tuesday, the stock market displayed mixed outcomes with the S&P 500 and Nasdaq Composite experiencing slight gains, while the Dow Jones Industrial Average faced a minor decline amidst anticipation for upcoming inflation data. Corporate earnings, particularly from Macy’s and Lowe’s, alongside economic indicators, played significant roles in market dynamics. Meanwhile, the currency market witnessed subtle shifts, with the Japanese yen strengthening against the dollar following Japan’s higher-than-expected core CPI report. Investor focus remains on key economic releases, including the personal consumption expenditure price index, with global monetary policy expectations influencing market sentiment.

Stock Market Updates

On Tuesday, the stock market saw mixed results as investors awaited crucial inflation data expected later in the week. The S&P 500 edged up by 0.17% to 5,078.18, while the Nasdaq Composite saw a modest increase of 0.37%, closing at 16,035.30. Contrarily, the Dow Jones Industrial Average experienced a slight downturn, dropping by 96.82 points, or 0.25%, to end at 38,972.41. Notable movements included Macy’s, which surged 3.4% after announcing plans to close approximately 150 underperforming stores due to a previous revenue shortfall. Additionally, Lowe’s shares increased by 1.7% following an earnings beat, with Zoom Video and Hims & Hers Health also making significant gains after surpassing Wall Street’s earnings expectations.

A mix of corporate earnings reports and economic indicators influenced the market’s dynamics. The utilities sector led the market with a 1.9% increase, while the communications services and technology sectors also saw gains. This activity followed a decline from record highs the previous week, spurred by Nvidia’s impressive earnings. Moreover, investor sentiment was affected by a drop in consumer confidence amid concerns over a potential labor market slowdown and a divisive political climate, as reported by the Conference Board. Additionally, a decrease in orders for long-lasting goods in January, particularly in transportation, underscored these economic uncertainties. As investors look ahead, the forthcoming release of the personal consumption expenditure price index and personal income data will be closely scrutinized for insights into economic health and monetary policy direction.

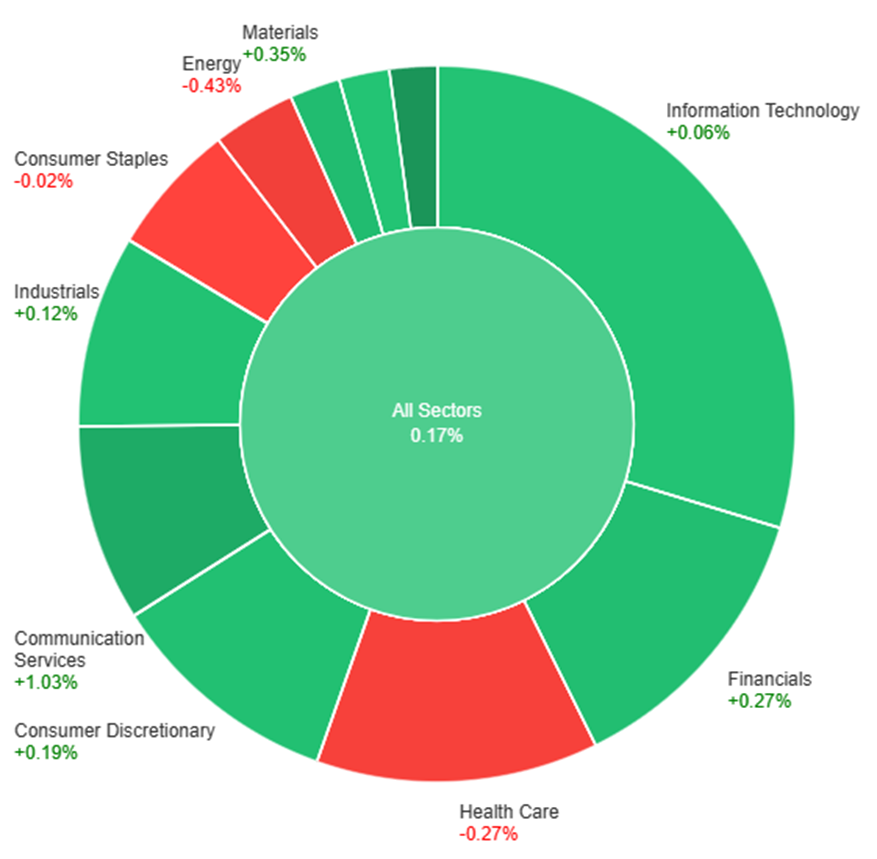

On Tuesdayday, the overall market saw modest gains, with all sectors collectively up by 0.17%. Utilities led the performance with a significant increase of 1.89%, followed by Communication Services and Materials, which rose by 1.03% and 0.35%, respectively. Financials, Consumer Discretionary, and Industrials also experienced gains, though more modest, ranging from 0.12% to 0.27%. Information Technology and Real Estate sectors saw minimal increases, whereas Consumer Staples, Health Care, and Energy sectors faced declines, with Energy recording the largest drop at -0.43%.

Currency Market Updates

The currency market saw nuanced movements with the dollar index slightly declining by 0.09%, influenced by a mix of supportive corporate month-end flows and weaker-than-expected U.S. economic data concerning durable goods and consumer confidence. The Japanese yen emerged as a notable performer, appreciating following a report that showed Japan’s core CPI rising above forecasts. This development came amidst static policy pricing from major central banks such as the Federal Reserve, European Central Bank, and the Bank of Japan, with the market participants keenly awaiting further key data releases scheduled for later in the week and the next.

The FX landscape was further characterized by the lingering weakness of the USD against the JPY, spurred by Japan’s inflation data, while the EUR/USD, GBP/USD, and other major currency pairs saw marginal gains. Despite some reasons to overlook the disappointing U.S. durable goods data, attributed partly to Boeing’s challenges, the misses in economic reports have heightened the anticipation for upcoming releases on core PCE, income, spending, and employment data. Market speculation regarding the Federal Reserve’s interest rate path remains a focal point, especially after Kansas City Fed President Jeffrey Schmid’s hawkish remarks, contrasting with the market’s reduced expectations for Fed rate cuts. The evolving monetary policy expectations for the ECB, BoE, and BoJ also play a critical role in shaping the currency market dynamics, with all eyes on the upcoming eurozone CPI and U.S. core PCE data to gauge potential shifts in monetary policy and currency valuations.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Stabilizes Amid Anticipation of Key Economic Data

The EUR/USD pair has been hovering around the 1.0850 mark, showing little movement as traders await impactful economic releases. Following a more significant than expected decline in US Durable Goods Orders for January, market focus now shifts to upcoming US GDP figures, German Retail Sales, CPI data, and the US PCE inflation report. These forthcoming data points are crucial for gauging the economic health of both regions and could potentially influence the currency pair’s direction.

On Tuesday, the EUR/USD moved slightly lower and was able to reach the middle band of the Bollinger Bands. Currently, the price is moving around the middle band, suggesting a potential downward movement to reach below the middle band. Notably, the Relative Strength Index (RSI) maintains its position at 53, signaling a neutral outlook for this currency pair.

Resistance: 1.0858, 1.0896

Support: 1.0823, 1.0783

XAU/USD (4 Hours)

XAU/USD See Modest Gains Amid Weakening Dollar and Anticipation for Key Economic Reports

Gold (XAU/USD) experienced a slight increase in its price during Tuesday’s mid-North American session, trading at $2,034.88, a 0.18% gain, amid a backdrop of falling US Treasury bond yields and a weakening US Dollar, as indicated by a 0.05% drop in the US Dollar Index (DXY). This modest uptick occurs as the precious metal hovers around the 50-day Simple Moving Average, with investors keenly awaiting the Personal Consumption Expenditures (PCE) report and latest Gross Domestic Product (GDP) data, which are anticipated to be significant factors that could drive Gold out of its current $2,020-$2,050 trading range. The outlook is further clouded by the recent report on Durable Goods Orders for January, which fell more sharply than expected, and mixed Home Prices data, suggesting a potentially volatile period ahead for Gold prices.

On Tuesday, XAU/USD moved lower to reach the middle band of the Bollinger Bands. Currently, the price is moving just above the middle band, suggesting a potential consolidation movement. The Relative Strength Index (RSI) stands at 53, signaling a neutral outlook for this pair.

Resistance: $2,042, $2,056

Support: $2,030, $2,017

Economic Data

Currency

Data

Time (GMT + 8)

Forecast

AUD

CPI y/y

08:30

3.4% (Actual)

NZD

Official Cash Rate

09:00

5.50% (Actual)

NZD

RBNZ Monetary Policy Statement

09:00

NZD

RBNZ Rate Statement

09:00

USD

Prelim GDP q/q

21:30

3.3%

Written on February 28, 2024 at 2:48 am, by anakin

The DXY index, which measures the US dollar’s performance, showed limited movement on Monday despite a slight increase in US Treasury yields.

Investors are adopting a cautious approach in anticipation of Thursday’s core personal consumption expenditures (PCE) deflator release, a critical inflation measure favored by the Federal Reserve.

January’s core PCE is anticipated to rise by 0.4% from December, potentially reducing the annual rate from 2.9% to 2.8%, indicating a modest yet positive development.

There’s a possibility that the actual figures could exceed expectations, mirroring recent trends seen in CPI and PPI reports, which could impact traders’ outlooks.

Upcoming US PCE Report Analysis:

An unexpected increase in the PCE data might lead to higher interest rate expectations, suggesting a delayed start or smaller reductions in the easing cycle by policymakers.

Such a scenario would likely result in higher US Treasury yields, benefiting the US dollar.

Technical Analysis of USD Currency Pairs:

The latter part of the article shifts focus to the technical analysis of EUR/USD, USD/CAD, and USD/JPY currency pairs.

It will explore market sentiment and pinpoint crucial support and resistance levels that may influence the pairs’ movements in the near future.

STOCK MARKET:

Market Performance:

The Dow Jones Industrial Average (^DJI) decreased by 0.2%.

The S&P 500 (^GSPC) dropped by 0.4% after reaching new highs last week.

The Nasdaq Composite (^IXIC) experienced a 0.1% decline, following a strong performance in tech stocks.

Inflation Data Anticipation:

Investors are on edge as they await new inflation figures that could challenge the recent stock market rally, particularly after Nvidia’s (NVDA) impressive results.

Concerns are mounting over a potential surprise in the upcoming Thursday PCE index report, the Federal Reserve’s favored inflation measure, especially after a higher-than-expected CPI report earlier in February led to market volatility.

Economic Indicators and Corporate Results:

This week’s inflation report is a key focus, alongside updates on consumer and manufacturing sectors, which will provide insights into the US economy’s condition.

Berkshire Hathaway (BRK-B) is nearing a $1 trillion market valuation following a record annual profit, with Warren Buffett highlighting the company’s durability and acknowledging Charlie Munger’s contributions.

Domino’s Pizza (DPZ) shares surged 6% after announcing a dividend increase and surpassing fourth-quarter sales forecasts.

Coinbase (COIN) shares rose 16% as Bitcoin (BTC-USD) remained above $54,000, reflecting positive sentiment in the cryptocurrency market.

On Monday, the stock market experienced a downturn, with the S&P 500, Nasdaq Composite, and Dow Jones Industrial Average all closing lower, moving away from recent record highs. This shift comes as investors brace for a slew of economic data, including a crucial inflation measure and updates on consumer spending, which could impact Federal Reserve policy decisions. The market’s focus is particularly on the upcoming personal consumption expenditures price index, a preferred inflation indicator by the Fed. Additionally, Amazon’s inclusion in the Dow signifies a shift toward tech and consumer retail sectors, despite a slight dip in its shares. With Treasury yields rising and various economic indicators on the horizon, investors remain cautious amid an uncertain longer-term outlook, even as currency markets react to potential monetary policy adjustments in the U.S. and Europe.

Stock Market Updates

On Monday, the S&P 500 saw a decline, moving away from the record high it reached the previous Friday, as the market anticipated upcoming inflation data. The index fell by 0.38% to 5,069.53, while the Nasdaq Composite dropped by 0.13%, ending the day at 15,976.25. The Dow Jones Industrial Average also experienced a downturn, losing 62.30 points, or 0.16%, to close at 39,069.23. Notably, Amazon was added to the Dow, replacing Walgreens Boots Alliance, which is expected to heighten the index’s focus on the tech and consumer retail sectors, even as Amazon’s shares dipped slightly by 0.15%. Additionally, Treasury yields rose, exerting further pressure on the stock market.

The market’s recent performance has been bolstered by strong earnings from companies like Nvidia, propelling the S&P 500 and the Dow to record highs at the end of the previous week. However, investors remain cautious, looking ahead to several economic indicators due to be released, including the personal consumption expenditures price index, a key measure of inflation favored by the Federal Reserve. Meanwhile, new home sales for January fell short of expectations amid high mortgage rates, underscoring the ongoing economic challenges. This week will also see the release of data on durable orders, wholesale inventories, consumer spending, and PCE numbers, all of which could significantly influence market sentiment.

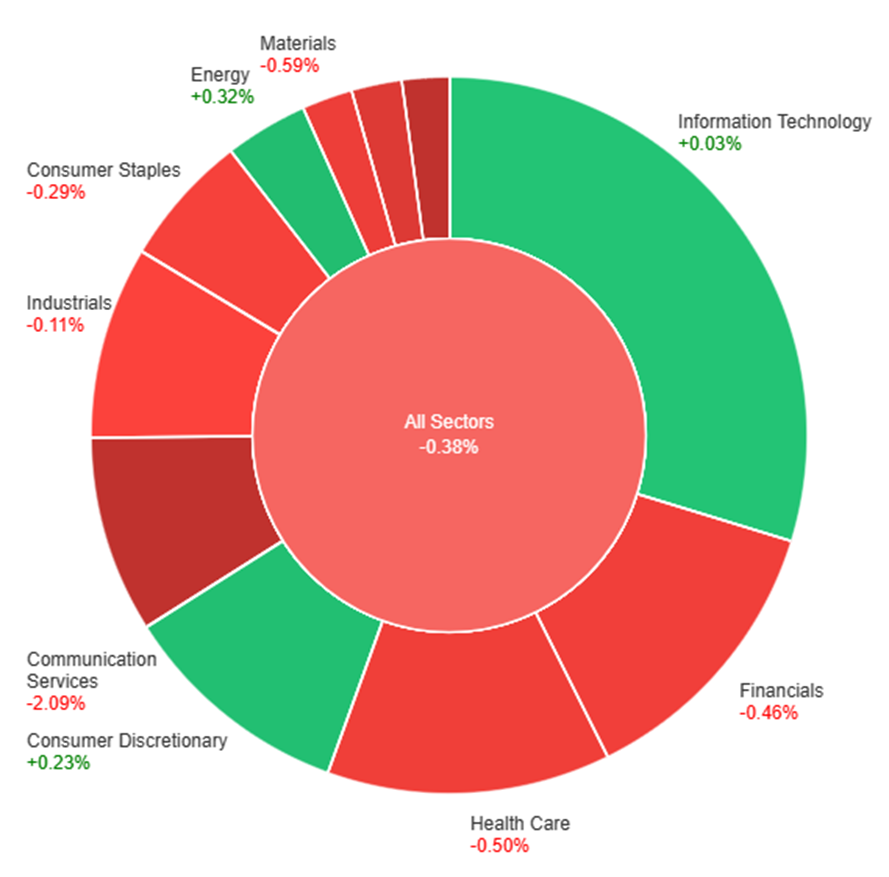

On Monday, the market showed a mixed performance across various sectors. While the overall sectors declined by 0.38%, Energy (+0.32%), Consumer Discretionary (+0.23%), and Information Technology (+0.03%) sectors experienced gains, indicating some areas of strength in the market. However, most sectors saw declines, with Utilities (-2.10%) and Communication Services (-2.09%) facing the steepest drops, followed by significant downturns in Real Estate (-1.14%), Materials (-0.59%), Health Care (-0.50%), and Financials (-0.46%). Industrials and Consumer Staples also saw modest declines, underscoring a generally bearish sentiment across the broader market.

Currency Market Updates

In recent currency market updates, the dollar index experienced a slight decline of 0.1%, influenced primarily by gains in the EUR/USD pair, as investors awaited crucial inflation data from both the U.S. and the eurozone. This upcoming data is expected to provide insights into the future of the narrowing gap between bund and Treasury yields observed since mid-February. The anticipation around this data release stems from its potential to either confirm or alter the current expectations regarding monetary policy adjustments by the Federal Reserve and the European Central Bank (ECB), especially in light of recent economic indicators. The dollar, meanwhile, saw an uptick against traditionally lower-yielding currencies like the yen, as well as risk-sensitive currencies such as the Australian dollar and the yuan, amidst speculations on the Federal Reserve’s interest rate decisions following a strong U.S. jobs report and inflation figures that surpassed forecasts.

Investor focus is particularly honed in on the upcoming core PCE reading, February ISMs, and the March 8 employment report, with the outcomes likely to influence Federal Reserve policy discussions significantly. Despite the current market pricing, which reflects a cautious stance on the pace and extent of Fed rate cuts, the longer-term economic outlook remains uncertain. This uncertainty is exacerbated by persistent high-interest rates and a stock market buoyed by a limited number of companies, raising concerns over potential underperformance in U.S. economic data relative to expectations. Meanwhile, in Europe, inflation data releases are poised to further clarify the ECB’s stance on interest rates, amidst statements from President Christine Lagarde indicating sustained wage growth. Additionally, Japan’s inflation figures and the potential implications for the Bank of Japan’s policy direction add another layer to the global currency market dynamics, with significant attention also being paid to the British pound’s movements against the backdrop of the Bank of England’s anticipated policy decisions.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Gains Amid Speculation of US Interest Rate Cuts and ECB’s Prudent Stance

The EUR/USD pair experienced a rebound, touching the 1.0860 mark as the new trading week began, fueled by a weakening US dollar and speculation about potential Federal Reserve interest rate cuts, possibly starting in June. This speculation has been supported by recent US inflation data and a tight labor market, increasing the odds of monetary easing. Meanwhile, European Central Bank (ECB) official Yannis Stournaras emphasized the need for cautious monetary policy adjustments, aiming for a gradual approach to rate cuts to ensure inflation targets are met. The interplay between anticipated US monetary policy adjustments and the ECB’s prudent stance is likely to continue driving EUR/USD price actions in the near term.

On Monday, the EUR/USD moved higher and was able to reach the upper band of the Bollinger Bands. Currently, the price is moving just below the upper band, suggesting a potential downward movement to reach the middle band. Notably, the Relative Strength Index (RSI) maintains its position at 60, signaling a slightly bullish outlook for this currency pair.

Resistance: 1.0858, 1.0896

Support: 1.0823, 1.0783

XAU/USD (4 Hours)

XAU/USD Retreats Below $2,030 Amid Rising US Treasury Yields and Technical Pressure

Gold experienced a slight downturn, falling below the $2,030 mark during the American trading session on Monday, as it faced technical and fundamental pressures. The recovery of the 10-year US Treasury bond yields toward 4.3% contributed to the decline in the XAU/USD pair, reflecting a dampened appeal for the non-yielding asset. Technical analysis reveals a decrease in buying interest, with a potential for a bearish extension highlighted by the metal’s performance around critical simple moving averages (SMAs) and technical indicators. Meanwhile, the broader market’s cautious stance ahead of significant US economic data releases, including the closely watched US Core Personal Consumption Expenditures (PCE) Price Index, adds to the bearish sentiment surrounding gold.

On Monday, XAU/USD moved lower to reach the middle band of the Bollinger Bands. Currently, the price is moving just above the middle band, suggesting a potential consolidation movement. The Relative Strength Index (RSI) stands at 55, signaling a neutral outlook for this pair.

Resistance: $2,042, $2,056

Support: $2,030, $2,017

Economic Data

Currency

Data

Time (GMT + 8)

Forecast

USD

Durable Goods Orders m/m

21:30

-4.9%

USD

CB Consumer Confidence

23:00

114.8

Written on February 27, 2024 at 12:47 am, by anakin

Market confidence surged, led by Nvidia’s strong Q1 2024 forecast.

Nvidia’s success propelled the S&P 500 to record highs; Japanese index topped after 34 years.

Gold prices climbed, and the USD sought equilibrium amidst positive market sentiments.

Anticipated January PCE inflation results could prompt continued USD decline and boost gold.

Sterling remained strong with minimal impactful data expected to affect its position.

The Euro’s rally against major G7 currencies may be losing momentum as the week ended.

STOCK MARKET:

Economic data: Dallas Fed Manufacturing Activity, February (-27.4 previously); New home sales, January (684,000 annualized rate expected, 664,000 previously); New home sales, month-over-month, January (+3% expected, +8% previously)

As we approach the end of February 2024, the financial world turns its focus towards a series of crucial economic updates slated for release. These reports, spanning from Japan’s inflation rates to the ISM Manufacturing PMI in the United States, are poised to provide fresh insights into the global economic landscape. Among these, the Reserve Bank of New Zealand’s rate statement stands out as a particularly significant event. Here’s what to expect in the week ahead:

February 27, 2024: Japan’s inflation rate

The annual inflation rate in Japan has seen a decrease, landing at 2.6% in December 2023, down from 2.8% the previous month. This marks the lowest inflation rate since July 2022. Analysts are now eyeing a further drop to 2.1% for January 2024, with the data expected to be unveiled on 27 February. This anticipated decrease could signal easing inflationary pressures within the Japanese economy, offering a glimpse into the country’s current economic health.

February 27, 2024: US durable goods orders

In the United States, new orders for manufactured durable goods showed no significant change in December 2023, a stark contrast to the 5.5% rise observed in November. The forecast for January 2024 is less optimistic, with analysts predicting a 4.5% decline. Set to be released on 27 February, this data could reflect the changing dynamics in U.S. manufacturing and consumer confidence.

February 28, 2024: Australia’s CPI

Australia’s Consumer Price Index (CPI), a key indicator of inflation, increased by 3.4% in the year to December 2023, a slowdown from the 4.3% climb seen in November. Projections suggest a slight easing to 3.2% for January 2024, with the figures due on 28 February. A moderation in CPI growth may indicate that inflationary pressures are beginning to stabilise in Australia.

February 28, 2024: Reserve Bank of New Zealand’s rate decision

The Reserve Bank of New Zealand (RBNZ) previously held its official cash rate (OCR) steady at 5.5% during its November meeting. This pause, consistent for the fourth consecutive time, met market expectations. Analysts widely anticipate that the RBNZ will maintain the OCR at 5.5% in its upcoming 28 February meeting. The decision is keenly awaited, as it could signal the central bank’s outlook on New Zealand’s economic conditions and inflationary trends.

February 29, 2024: Canada’s GDP

Canada’s GDP growth for November exceeded expectations, registering a 0.2% increase. This improvement followed three months of stagnant growth. The forecast for December 2023 points to a further rise of 0.3%, with the announcement scheduled for 29 February. A consecutive growth increment would signify a strengthening in the Canadian economy’s recovery momentum.

February 29, 2024: US core PCE price index

The core PCE price index in the US, an important measure of inflation that excludes food and energy costs, experienced a slight uptick of 0.2% in December 2023. Analysts are now expecting a more pronounced increase of 0.4% for January 2024, with data due on 29 February. This anticipated growth could reflect persisting inflationary pressures within the core sectors of the U.S. economy.

March 1, 2024: US ISM manufacturing PMI

The ISM Manufacturing PMI in the United States showed signs of improvement in January 2024, reaching 49.1 from 47.1 in December, marking the highest level since October 2022. The forecast for February remains optimistic, with analysts predicting the index to hold at 49.1. The upcoming release on 1 March will be closely watched as an indicator of the health and direction of the U.S. manufacturing sector.

Written on February 26, 2024 at 3:43 am, by anakin

U.S. Dollar Maintains Strong Position: The USD continues to show a strong upward trend; focus is on EUR/USD, GBP/USD, and gold prices.

Date and Analyst: Article written by Diego Colman, Contributing Strategist, on February 23, 2024.

Anticipation for Core PCE Data: Markets are on alert for the upcoming U.S. core PCE data release, a key inflation indicator favored by the Fed.

Potential Market Volatility: The upcoming economic event may cause significant fluctuations in the FX market, requiring traders to stay alert.

Core PCE Projections: Expectations suggest a 0.4% rise in core PCE for January, potentially lowering the annual rate to 2.7% from 2.9%.

Inflation and Economy Dynamics: Recent CPI and PPI reports indicate potential for higher than expected inflation rates.

Fed’s Response to Inflation: Persistent inflation and strong labor market data might postpone the Fed’s easing cycle, possibly tilting rate expectations higher.

Interest Rates and U.S. Dollar: Prolonged higher interest rates could increase U.S. Treasury yields, potentially boosting the dollar’s upward momentum.

Impact on Currency Pairs and Gold: A strong dollar could hinder gains in EUR/USD and GBP/USD pairs, as well as pressure gold prices.

Technical Analysis Ahead: The article will next delve into the technical analysis for EUR/USD, GBP/USD, and gold prices, highlighting important price levels for traders.

STOCK MARKET:

Nvidia’s Earnings Drive Markets: Nvidia’s significant earnings report spurred markets to all-time highs across the US, Europe, and Japan.

Record Market Capitalization: Nvidia’s market cap surged by $277 billion in a single session, marking the largest increase ever.

Sustainability of the Tech Rally: Questions arise about the tech rally’s longevity and its potential spread to other sectors.

AI’s Role in Growth: UBS Global Wealth Management highlights generative AI as a key growth theme, driving Nvidia’s success and potential market broadening.

European Market Movements: The Stoxx Europe 600 index hits a record, driven by gains in the mining sector and positive corporate earnings.

Megacap Influence in Europe: A few large companies significantly contribute to the Stoxx 600’s performance, mirroring US market concentration risks.

Global Equity Outlook: Citigroup strategists predict a broadening of global equity returns beyond a narrow first quarter.

Asian Market Trends: Continued gains in China’s CSI 300 and steady performance in other Asian markets, despite Japan’s holiday closure.

Fed’s Interest Rate Strategy: Hawkish comments from Fed officials suggest rate cuts are on the horizon, but not imminent.

Commodity Market Updates: Mixed movements in oil, gold, and metals, with iron ore experiencing a notable weekly drop.

{kind=link}