The NASDAQ, S&P 500, and Dow Jones have all achieved new record highs, signaling a complete reversal of the recent stock market dip from December to early January.

In Japan, the Nikkei 225 has hit a fresh 34-year high, while China’s Hang Seng is experiencing ongoing weakness, attributed to a battle between the Federal Reserve (Fed) and the financial markets.

The Fed is attempting to talk down interest rates, but market expectations for rate cuts persist, leading to a positive overall sentiment despite some success in lowering rate cut expectations.

A “Fed blackout period” is currently in effect, with no speeches or comments from Fed members expected ahead of the FOMC meeting on January 31st, creating a quieter news period related to the Fed.

Turning to the US dollar, it is trading around a 50% retracement level, with the 200-day and 50-day moving averages serving as significant support and resistance levels.

The US Core PCE, the Fed’s preferred measure of inflation, is anticipated to be a major event for the dollar during the week, potentially influencing its performance.

In the Eurodollar market, trading within small ranges is supported by the 200-day simple moving average, and upcoming factors such as the German and Eurozone PMIs, along with the ECB monetary policy meeting, could play a crucial role in shaping Eurodollar performance in the coming week.

STOCK MARKET:

The ongoing equity rout in China has led to an unprecedented $38 trillion gap between the market capitalization of the US stock market and that of Hong Kong and China combined, setting a new record.

Michael Liang, Chief Investment Officer at Foundation Asset Management HK Ltd., notes that while China presents value, the lack of catalysts is hindering its performance, while the US market benefits from momentum and a favorable economy.

Global investor sentiment toward China is painted negatively as steep losses continue, contrasting with US stocks that have reached record highs, fueled by a technology rally and optimism about potential Federal Reserve interest rate cuts.

Since February 2021, Chinese stocks have witnessed a loss of over $6.3 trillion in market value, while US equities have gained $5.3 trillion over the same period.

Doubts over Beijing’s long-term economic agenda and strategic competition with the US are contributing to what started as a performance-driven exodus potentially becoming a structural shift.

Bloomberg strategists, including Kumar Gautam, suggest that China’s correction might continue, estimating a 51% probability of the MSCI China Index trading below its peak for an average of 35 months.

Despite the prolonged rout, some investors see potential for a technical rebound due to attractive valuations. The MSCI China Index is now 60% cheaper than the US equity benchmark based on earnings-based valuations.

The MSCI Inc.’s key gauge for Chinese equities trades at about eight times 12-month forward estimated earnings, significantly lower than the S&P 500 Index’s 20 times.

Currently, there is little indication of an end to the challenging start of 2024 for Chinese equities, with a gauge of Chinese stocks listed in Hong Kong already losing 13%, making it the worst-performing major global benchmark index in less than a month.

Chinese stocks listed in Hong Kong already losing 13%, making it the worst-performing major global benchmark index in less than a month.

Ready to take your trading to the next level amidst these market dynamics? Explore the cutting-edge capabilities of VT Markets’ MetaTrader 5 platform – your gateway to informed and strategic trading in today’s volatile markets. Start now and experience the difference in your trading journey.

Written on January 23, 2024 at 10:02 am, by anakin

On Monday, the Dow Jones Industrial Average achieved a historic high above 38,000, accompanied by a surge in United Airlines’ stock following strong fourth-quarter results. However, concerns about the grounding of Boeing 737 Max 9 planes led to an anticipated first-quarter loss for the airline. The broader market witnessed milestones, with the S&P 500 and Nasdaq Composite reaching all-time highs. Despite the bullish trend, investors remain cautious, especially amid a tech-focused rally. Currency markets showed calm consolidation, and Treasury yields led to a bull yield curve steepening. Market attention turned to the BoJ’s policy meeting, upcoming economic events, and central bank decisions impacting major currencies. The week’s developments include expectations for the Fed’s role in USD/JPY dynamics and varying rate cut predictions for the BoE and ECB, influencing currency performance.

Stock Market Updates

U.S. stock futures showed minimal movement on Monday night, with the Dow Jones Industrial Average reaching a historic high above 38,000. Notably, United Airlines experienced a more than 6% surge in extended trading following robust fourth-quarter results but anticipated a first-quarter loss due to the grounding of Boeing 737 Max 9 airplanes involved in a recent emergency. Other airline stocks, including American Airlines and Southwest Airlines, rose around 3%, while Alaska Air Group and Delta Air Lines climbed approximately 2%.

Monday’s trading session marked significant milestones as the Dow advanced over 100 points, closing above 38,000 for the first time, and both the S&P 500 and Nasdaq Composite reached new all-time highs. Despite the bullish trend, investors are cautious about the sustainability of gains, particularly as the tech-focused rally contrasts with lackluster broader market participation. The ongoing corporate earnings season adds to market scrutiny, with notable reports expected from Johnson & Johnson, Procter & Gamble, Lockheed Martin before the open, and Netflix after the close on Tuesday.

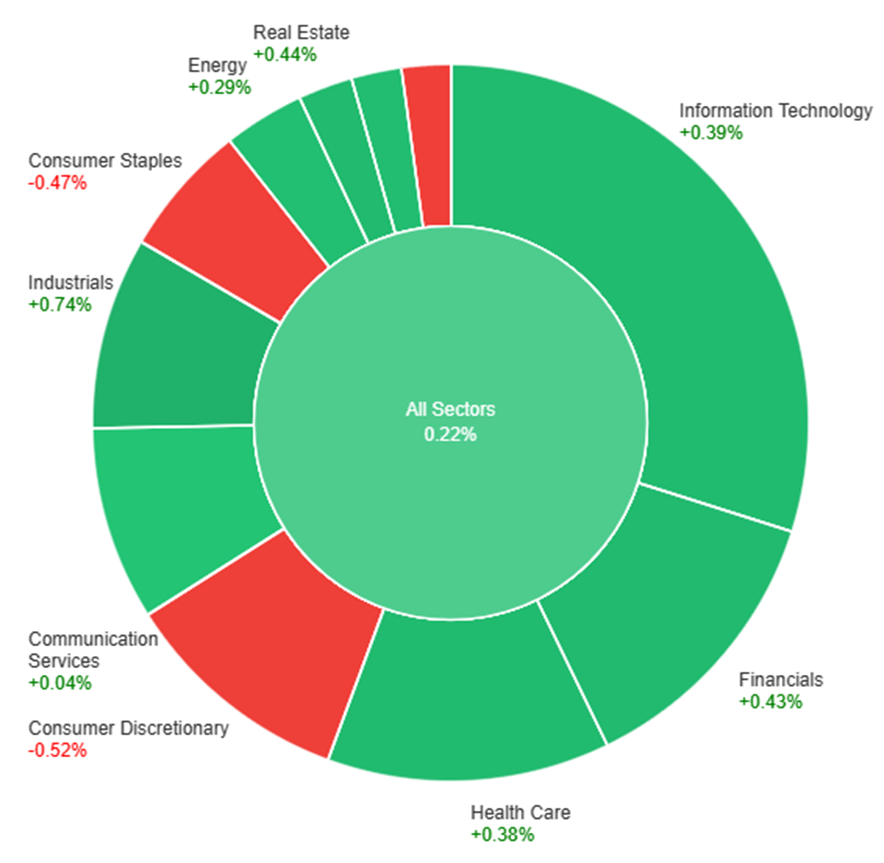

On Monday, the overall market saw a modest gain of 0.22%. Several sectors contributed positively, with Industrials leading the way with a notable increase of 0.74%, followed by Real Estate (+0.44%), Financials (+0.43%), Information Technology (+0.39%), and Health Care (+0.38%). Materials and Energy also experienced slight upticks of 0.30% and 0.29%, respectively. However, not all sectors fared well, as Consumer Staples (-0.47%), Utilities (-0.52%), and Consumer Discretionary (-0.52%) witnessed declines, dragging down the overall market performance. Communication Services showed a marginal decrease of 0.04%.

Currency Market Updates

In the currency markets, the dollar, euro, and sterling showed a calm consolidation at the beginning of the week, with profit-taking observed on stretched short yen trades ahead of the BoJ meeting on Tuesday. The dollar index remained flat, EUR/USD held steady, USD/JPY experienced a slight dip of 0.1%, and sterling saw a 0.14% increase. Treasury yields led a broader bull yield curve steepening and a risk-on trend in major government bond and equity markets, except for China. The market’s expectations for a March Fed cut decreased to a 42% probability, down from being fully discounted at the turn of the year, and the expected 150bp of Fed cuts in 2024 was adjusted to 135bp.

The focus turned to the BoJ’s two-day policy meeting concluding on Tuesday, where no significant rate hike expectations were priced in. Modest policy normalization expectations for the yen may be revised lower, leaving Fed policy as the primary driver for USD/JPY. Additionally, upcoming events such as U.S. Q4 GDP, jobless claims, and the Fed’s favored PCE on Friday, as well as the ECB meeting on Thursday, added to the week’s potential market impact. EUR/USD continued to consolidate below key levels, while USD/JPY followed Treasury yields lower but held above crucial support. Sterling outperformed the euro, influenced by the expectation that the BoE would cut rates less than the ECB in the coming year. The yuan remained supported amid a 2.7% dive in the Shanghai Composite, affecting AUD/USD negatively.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Navigates Indecision Amidst Diverging Central Bank Sentiments

The new trading week for EUR/USD opened with uncertainty and fluctuating price action tied to the U.S. dollar, accompanied by low volatility on Monday. As market participants anticipate around 120 basis points in rate cuts for the year, a debate ensues between them and the ECB’s rate-setters regarding the timing of the central bank’s decision to reduce the region’s policy rate. Despite inflation surpassing the bank’s target, European policymakers appear inclined to maintain a restrictive stance, hindered by weak fundamentals in the bloc, limiting the upside potential for the European currency. Meanwhile, across the Atlantic, investors are assigning just over a 40% probability to a Federal Reserve rate cut at the March 20 meeting, according to the FedWatch Tool tracked by CME Group.

On Monday, the EUR/USD moved in consolidation, able to reach the middle band of the Bollinger Bands. Currently, the price moving just above the middle band, suggesting a potential upward movement to reach the upper band. Notably, the Relative Strength Index (RSI) maintains its position at 48, signaling a neutral outlook for this currency pair.

Resistance: 1.0954, 1.1000

Support: 1.0863, 1.0814

XAU/USD (4 Hours)

XAU/USD Retreats Amidst Dollar Weakness and Cautious Market Sentiment

Spot Gold experienced a shift in trajectory, rebounding from an early dip to $2,016.42 to trade around $2,024 during the American session, showcasing modest intraday losses. The weakened demand for the US Dollar, influenced by the strength in global indexes and Wall Street’s positive momentum fueled by robust earnings reports, played a pivotal role. However, market participants remain cautious as the upcoming week brings critical economic data releases, including the preliminary estimate of the Q4 Gross Domestic Product (GDP) in the United States. With various central banks revealing their monetary policy decisions, Gold faces a dynamic landscape, navigating uncertainties surrounding economic indicators and inflationary pressures.

On Monday, XAU/USD moved lower and was able to reach the middle band of the Bollinger Bands. Currently, the price moving just above the middle band suggesting a potential upward movement to reach the upper band. The Relative Strength Index (RSI) stands at 46, signaling a neutral outlook for this pair.

US equities, including the S&P 500 and Dow Jones, reach fresh all-time highs, propelled by a robust performance in big tech stocks.

The ongoing Q4 earnings season, especially results from the ‘Magnificent Seven’ companies, is anticipated to further boost US indices.

Notably, Microsoft alone holds a significant 7.29% weighting in the S&P 500 index.

US Dollar Performance:

The US dollar initiates the year with strength, attributed to Federal Reserve Members countering overly optimistic interest rate cut expectations.

US Treasury yields support the USD against various currencies.

Precious metals, particularly gold, face pressure as they test the $2,000/oz. level.

Upcoming Events and Releases:

A multitude of Q4 US earnings releases is scheduled for the upcoming week.

Key economic events include the closely monitored Bank of Japan Quarterly Outlook Report, significant given elevated USD/JPY levels.

Thursday brings the European Central Bank (ECB) policy decision, while Friday features the US core PCE release, positioning them as the week’s main attractions.

Monday

Economic data: Leading Index, December (-0.3%, expected, -0.5% prior)

Earnings: United Airlines, Logitech, Zions Bancorporation Top of Form

STOCK MARKET:

Market Highlights:

US equities achieve new record highs with S&P 500, Dow Jones, and Nasdaq Composite in positive territory for January.

Consumer sentiment data from the University of Michigan boosts positive vibes as consumers express confidence in the economy.

Corporate Earnings:

Tech results take center stage with Netflix (NFLX) earnings on Tuesday and Tesla (TSLA) on Wednesday.

Other notable reports include Johnson and Johnson (JNJ), United Airlines (UAL), Verizon (VZ), and AT&T (ATT).

Overall, one of the busiest weeks for quarterly reports on Wall Street.

Economic Data:

First reading of Q4 economic growth expected on Thursday.

Release of the Personal Consumer Expenditures (PCE) Index, the Fed’s preferred inflation gauge, scheduled for Friday.

Economic Growth Outlook:

Resilient data indicates a potential 2% annualized growth in the US economy for Q4.

Oxford Economics expresses confidence in the ongoing economic expansion, citing a strong labor market, deceleration in inflation, and looser financial conditions.

Inflation and Rate Cut Speculations:

Key debate centers on when the Federal Reserve will cut interest rates.

Investors shift from an 81% chance of a March rate cut to 49%.

Goldman Sachs chief economist anticipates a March rate cut, driven by a decline in inflation to the target of 2%.

Upcoming Events:

Federal Reserve in blackout period, focusing attention on earnings as a key driver of stock market sentiment.

Technology earnings, particularly from large-cap companies, may influence short-term market direction.

Focus on Netflix demand for new advertising tier and Tesla’s margins, with CEO Elon Musk’s comments under scrutiny.

Fourth quarter earnings show a weak start, but the narrative is expected to shift to Technology and Communication Services, where growth is anticipated.

Recent decisions by central banks have significantly influenced global markets. In December 2023, the Bank of Japan (BoJ) and the Bank of Canada maintained key interest rates, while the European Central Bank (ECB) sustained multi-year high rates to combat inflation. Analysts expect these measures to continue. Key economic indicators, including manufacturing and services sector data, GDP, and inflation figures, will provide insights into the near-term market outlook.

Bank of Japan Rate Statement (23 January 2024)

In the final meeting of the year, the Bank of Japan (BoJ) unanimously decided to maintain its key short-term interest rate at -0.1% and 10-year bond yields at around 0%. Analysts are anticipating that the central bank will continue with the current interest rate levels in its upcoming meeting on January 23, 2024.

Bank of Canada Rate Statement (24 January 2024)

In December 2023, the Bank of Canada kept the overnight rate at 5%, marking the third consecutive meeting with unchanged rates. Analysts project a continuation of the current levels.

European Central Bank Rate Statement (25 January 2024)

In the European Union, the European Central Bank (ECB) sustained interest rates at multi-year highs for the second consecutive meeting in December 2023. This included signaling an early conclusion to its remaining bond purchase scheme as part of efforts to combat high inflation. Analysts are expecting a continuation of these interest rate levels at the ECB’s upcoming meeting on January 25, 2024.

Flash Manufacturing PMI (24 January 2024)

Turning to economic indicators, Germany’s manufacturing Purchasing Managers’ Index (PMI) increased from 42.6 to 43.3 between November and December 2023. In contrast, the UK and the US saw decreases in manufacturing PMIs, from 47.2 to 46.2 and 49.40 to 47.90, respectively. Forecasts for January 24, 2024, indicate anticipated manufacturing PMIs of 43.7 for Germany, 46.7 for the UK, and 47.6 for the US.

Flash Services PMI (24 January 2024)

Shifting to the services sector, Germany experienced a decline in its PMI from 49.6 to 49.3 between November and December 2023. In the same period, the UK’s services PMI increased from 50.9 to 53.4, and the US witnessed a rise in its services PMI from 50.8 to 51.4. Forecasts for January 24, 2024, suggest expected services PMIs of 49.1 for Germany, 53.0 for the UK, and 51.0 for the US.

US Advance GDP (25 January 2024)

In the United States, the American economy expanded at an annualised rate of 4.9% in the third quarter of 2023, slightly below the 5.2% second estimate but matching the initially reported 4.9% in the advance estimate. Looking ahead to the advance GDP release for the fourth quarter on January 25, 2024, analysts expect a slower growth rate of 2%.

US Core PCE Price Index (26 January 2024)

Finally, in the realm of inflation, Core PCE prices in the U.S., excluding food and energy, recorded a 0.1% increase from the previous month in November 2023. With data for December 2023 set to be released on January 26, 2024, analysts are forecasting a growth of 0.2%.

On Thursday, a positive turnaround in the stock market was driven by strong performances from tech companies, notably Apple, following a buy rating upgrade from Bank of America. The Dow Jones Industrial Average gained 201.94 points, the Nasdaq surged by 1.35%, and the S&P 500 climbed 0.88%. The 10-year Treasury yield rose to 4.14% amid tight labor market conditions, leading to concerns about fewer expected rate cuts by the Federal Reserve. In currency markets, the USD index rebounded, affecting pairs like EUR/USD and USD/JPY. GBP/USD held gains, supported by robust UK data. Commodity-centric currencies rose, while Bitcoin declined 2.75% due to higher global yields, contrasting its recent high on January 11.

Stock Market Updates

On Thursday, the stock market experienced a positive turnaround, with tech companies, particularly Apple, leading the way. The Dow Jones Industrial Average rebounded from an earlier loss, gaining 201.94 points or 0.54%, closing at 37,468.61. The Nasdaq Composite surged by 1.35%, reaching 15,055.65, while the S&P 500 climbed 0.88% to end at 4,780.94, just 0.33% away from its closing record. Apple’s shares saw a significant increase of around 3.3% after Bank of America upgraded the stock to a buy rating, predicting over 20% upside over the next 12 months. Other tech-related stocks, such as Taiwan Semiconductor Manufacturing Co., also contributed to the positive momentum, with the VanEck Semiconductor ETF reaching an all-time high, boosted by strong earnings and revenue results.

Additionally, the 10-year Treasury yield rose to 4.14% as fresh jobs data indicated tightness in the labor market, with first-time unemployment insurance filings coming in at 187,000 for the week ended Jan. 13. This stronger-than-expected labor market, combined with robust consumer spending, has raised concerns among investors about potential fewer rate cuts from the Federal Reserve than anticipated. The market is currently pricing in a roughly 56% chance of a quarter percentage point rate cut in March, according to the CME FedWatch Tool. Atlanta Fed President Raphael Bostic’s statement that he expects the central bank to start reducing rates in the third quarter contributed to the market’s uncertainty, as it deviates from the market’s expectations for a faster rate cut.

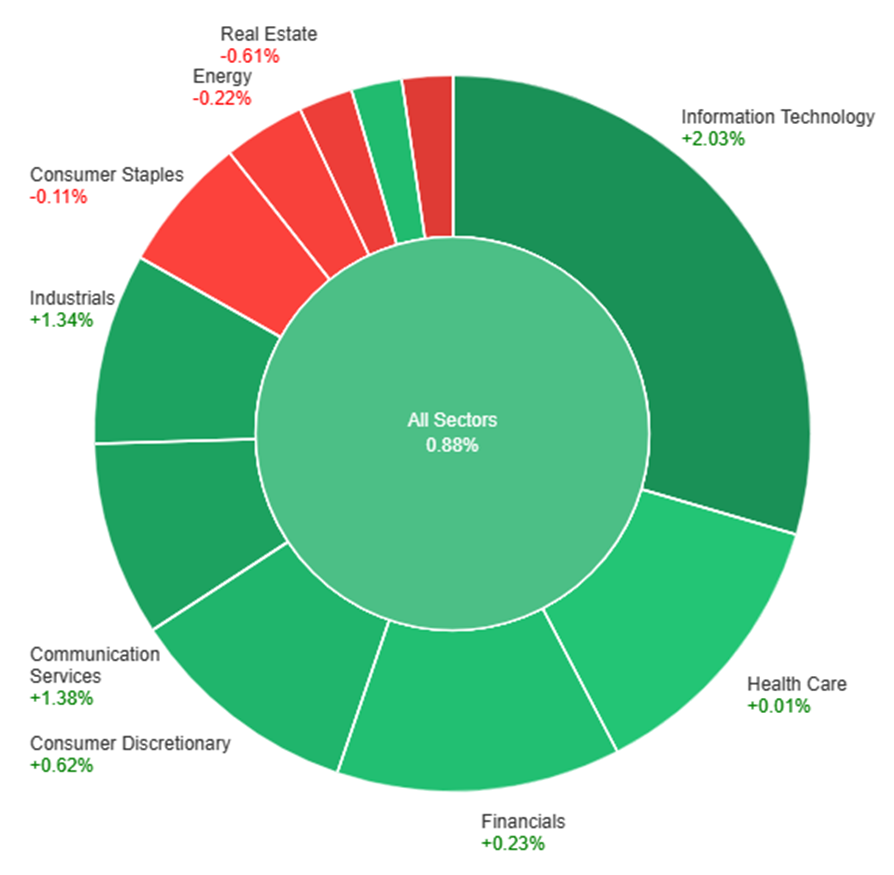

On Thursday, the overall market showed positive performance with a gain of 0.88%. The Information Technology sector led the way with a notable increase of 2.03%, followed by Communication Services and Industrials, which rose by 1.38% and 1.34%, respectively. Consumer Discretionary and Materials also saw modest gains at 0.62% and 0.39%. However, some sectors experienced declines, including Consumer Staples (-0.11%), Energy (-0.22%), Real Estate (-0.61%), and Utilities (-1.05%). Health Care showed minimal movement with a marginal increase of 0.01%. Overall, the day reflected a mixed performance across various sectors in the market.

Currency Market Updates

In the currency markets, the USD index rebounded from early lows during the North American trading session, gaining 0.23% in the U.S. afternoon. The surge came after jobless claims data came in below expectations, reducing the likelihood of a March rate cut by the Federal Reserve to 60%. This development suggested that the U.S. economy might not be slowing as initially thought. Meanwhile, the EUR/USD pair fell by 0.22% to 1.0858, with traders closely monitoring declining eurozone growth. USD/JPY reversed its overnight low-yield-related weakness, rising to 148.30 after the positive claims data, although it fell short of breaking Wednesday’s high of 148.53. Traders adopted a defensive stance ahead of Japan’s CPI release on Friday, lightening recent long positions in anticipation, even though expectations for the data prompting a shift to higher rates by the Bank of Japan remained low.

In contrast, GBP/USD held a slight gain, increasing by 0.14% to 1.2692 during New York afternoon trading. Despite facing resistance around the 1.27 level, the inability of bears to build on gains above this threshold hinted at an underlying bid near 1.26. The diminished expectations of a Fed rate cut were underscored by UK data, including Wednesday’s CPI, which exceeded forecasts, indicating that the Bank of England was unlikely to pivot to rate cuts in the near term. Other currency pairs, such as AUD/USD, rose by 0.15% to 0.6561, while USD/CAD remained flat at 1.3504. The latter was supported by rising oil and copper prices, benefiting commodity-centric currencies. In the cryptocurrency space, Bitcoin experienced a 2.75% decline, reaching a new one-month low at $41.3k, following its 21-month high at $49k on January 11. The dip in Bitcoin’s value was attributed to higher global yields, which did not bode well for crypto holders despite the coin being only down 1% year-to-date.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Holds Near Year-to-Date Lows as Greenback Gains Momentum Amidst Robust US Economic Indicators and Fed Uncertainty

On Thursday, the EUR/USD pair maintained a selling bias, settling around year-to-date lows near 1.0840 before experiencing a slight recovery. The uptrend in the US dollar was fueled by strong labor market results and a rebound in the Philly Fed Manufacturing Index. The USD Index (DXY) retained its bullish stance, supported by comments from Atlanta Fed President R. Bostic, hinting at potential rate cuts before July if inflation slows more rapidly than anticipated. Despite a baseline plan for rate reductions in the third quarter, caution is emphasized to avoid premature cuts. The market currently places a 55% probability of a Fed rate cut in March.

Meanwhile, ECB President C. Lagarde hinted at possible rate reductions in the summer. As US yields retreated slightly on the short end, German 10-year bund yields rose beyond 2.30%.

On Thursday, the EUR/USD moved slightly higher, able to reach the middle band of the Bollinger Bands. Currently, the price moving just above the middle band, suggesting a potential upward movement to reach the upper band. Notably, the Relative Strength Index (RSI) maintains its position at 46, signaling a neutral outlook for this currency pair.

Resistance: 1.0954, 1.1000

Support: 1.0863, 1.0814

XAU/USD (4 Hours)

XAU/USD Stabilizes Above $2,000 Amid Economic Uncertainties and Mixed Data

Gold (XAU/USD) has found a foothold around $2,015 per troy ounce after hitting a multi-week low of $2,001.68 earlier in the week. The precious metal rebounded as market sentiment improved slightly, countering the impact of a positive US Dollar driven by concerns over the housing sector and lackluster growth-related data. Despite initial pessimism from Asian shares, optimism grew on Wall Street with better-than-expected US data, including housing starts, building permits, and lower-than-anticipated jobless claims. Federal Reserve officials provided no fresh insights into future monetary policy, leaving investors navigating a landscape of economic uncertainties.

On Thursday, XAU/USD moved higher and reached the middle band of the Bollinger Bands. Currently, the price moving just below the middle band suggesting a potential upward movement to reach above the middle band. The Relative Strength Index (RSI) stands at 48, signaling a neutral outlook for this pair.

On Wednesday, the stock market saw a downturn driven by increasing Treasury yields influenced by robust U.S. economic data. The Dow Jones Industrial Average posted its third consecutive day of losses, dropping by 0.25%, while the S&P 500 and Nasdaq Composite slid 0.56% and 0.59%, respectively. Notable stock movements included a 1.3% drop for Charles Schwab and a 1.3% gain for Boeing. The market reaction was shaped by stronger-than-expected December retail sales data, casting doubt on the need for aggressive rate cuts by the Federal Reserve. The 10-year Treasury yield rose to 4.102%, and traders are estimating a 57% chance of rate cuts in March. In the currency market, the Greenback showed strength, impacting currency pairs like EUR/USD, GBP/USD, and USD/JPY. Gold and Silver prices declined due to the intense dollar rally, while WTI prices rose above $72.00 per barrel amid OPEC’s optimistic report. Traders are eagerly anticipating the EIA’s weekly report on U.S. crude oil inventories for further market cues.

Stock Market Updates

Stocks experienced a decline on Wednesday, influenced by rising Treasury yields following robust U.S. economic data. The Dow Jones Industrial Average marked its third consecutive day of losses, falling by 0.25%, while the S&P 500 and Nasdaq Composite slid 0.56% and 0.59%, respectively. Notable stock movements included a 1.3% drop for Charles Schwab due to mixed quarterly results, while Boeing saw a 1.3% gain, countering recent losses and positioning itself as one of the Dow’s leading gainers.

The market reaction was partly shaped by stronger-than-expected December retail sales data, suggesting a resilient consumer and casting doubt on the need for aggressive rate cuts by the Federal Reserve. Retail sales increased by 0.6% from November, exceeding economist estimates, potentially influencing the Fed’s monetary policy decisions. The 10-year Treasury yield rose to 4.102%, driven by Federal Reserve Governor Christopher Waller’s caution about a slower-than-anticipated easing of monetary policy. Traders, as reflected in CME Group’s FedWatch tool, are currently estimating a 57% chance of the Federal Reserve initiating rate cuts in March.

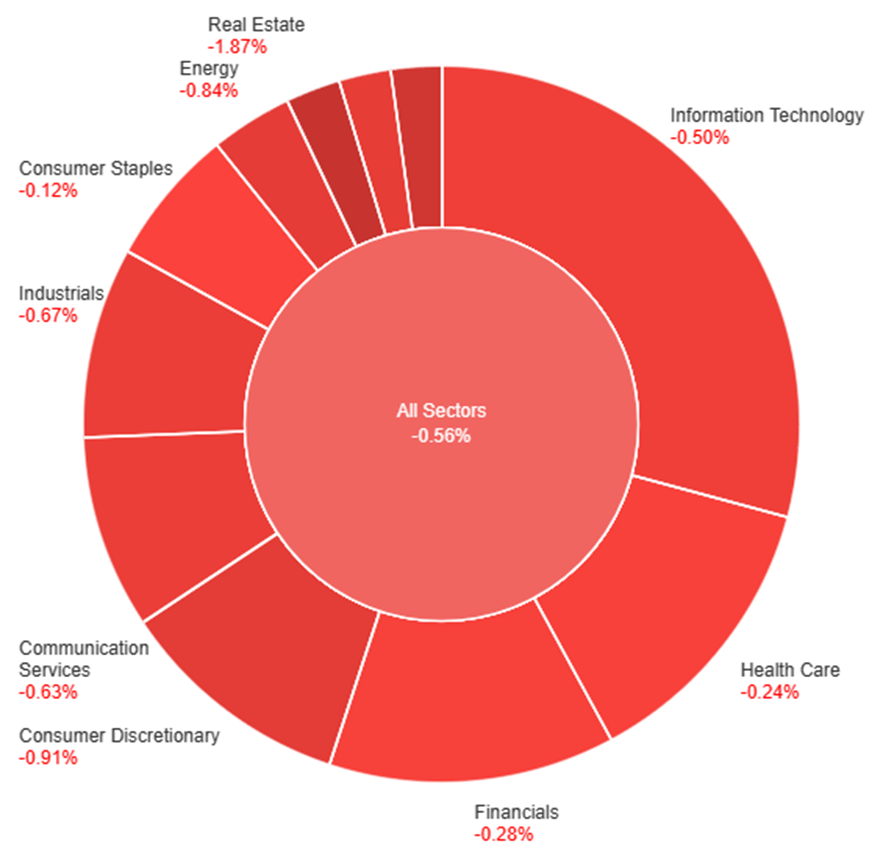

On Wednesday, across various sectors, the market experienced a downward trend, with the overall performance showing a decline of 0.56%. Notably, Utilities and Real Estate were the hardest hit, witnessing substantial decreases of 1.52% and 1.87%, respectively. Other sectors, including Consumer Discretionary, Energy, and Materials, also faced notable declines ranging from 0.80% to 0.91%. The weakest performers among the major sectors were Communication Services (-0.63%), Industrials (-0.67%), and Information Technology (-0.50%). The day saw a broad-based negative impact on the market, reflecting a cautious sentiment across various industries.

Currency Market Updates

In the currency market updates, the Greenback exhibited notable strength, propelling the USD Index to new 2024 peaks around 103.70, fueled by rising US yields across various maturities. The EUR/USD pair faced downward pressure, reaching multi-week lows near 1.0840, influenced by persistent dollar strength and ECB officials downplaying expectations of interest rate cuts in H1 2024. Meanwhile, GBP/USD saw support from higher-than-expected UK inflation figures, leading to decent gains, while USD/JPY surpassed the 148.00 barrier, driven by the dollar’s upward momentum and robust US yields. However, the Australian dollar faced continued selling pressure, with AUD/USD sinking to six-week lows near 0.6520, impacted by general dollar dynamics and discouraging results from the Chinese docket.

In the broader market, the intense dollar rally, coupled with rising US yields, adversely affected both Gold and Silver prices. The negative sentiment around Silver was exacerbated by disappointing Chinese data releases. On the energy front, WTI prices rose above $72.00 per barrel, partially reversing recent weakness following an optimistic report from OPEC. Despite challenges from China and a stronger dollar, traders are attentively awaiting the EIA’s usual weekly report on US crude oil inventories for further market cues.

In Wednesday’s trading session, EUR/USD encountered downward pressure, briefly touching multi-week lows before rebounding. The prevailing uptrend in the US dollar, fueled by robust December Retail Sales, tempered expectations of a Fed rate cut in March. CME Group’s FedWatch Tool indicated a shift, with the probability dropping to just above 50%. Meanwhile, ECB officials, including Knot and Vasle, highlighted market expectations for rate cuts, emphasizing alignment for a 2% inflation target by 2025. Lagarde hinted at a potential rate cut in the summer. Bond yield increases globally, particularly German 10-year bunds and rising US yields, contributed to the euro’s weakness. Poor Chinese fundamentals added to concerns about delayed economic recovery.

On Wednesday, the EUR/USD moved slightly higher, trying to reach the middle band of the Bollinger Bands. Currently, the price moving just below the middle band, suggesting a potential upward movement to reach above the middle band. Notably, the Relative Strength Index (RSI) maintains its position at 46, signaling a neutral outlook for this currency pair.

Resistance: 1.0954, 1.1000

Support: 1.0863, 1.0814

XAU/USD (4 Hours)

XAU/USD Slumps to Mid-December Lows as Dollar Surges Amidst Global Stock Decline

Spot gold, represented by XAU/USD, experiences a downturn, reaching its lowest point since mid-December. The decline is attributed to the strengthening US Dollar, which advances as global stocks continue to fall. Investors are scaling back expectations for a Federal Reserve rate cut in March, evident in the decreasing probability from 70% to 52% according to the CME FedWatch Tool. Mixed US data, including positive Retail Sales and Industrial Production figures, alongside hawkish sentiments from Fed officials, contribute to the diminishing likelihood of a March cut. Rising government bond yields and a continued slump in Wall Street further compound the challenges for gold in this market environment.

On Wednesday, XAU/USD moved lower and was able to create a lower push to the lower band of the Bollinger Bands. Currently, the price moving just above the lower band suggesting a potential downward movement to create another lower push to the lower band. The Relative Strength Index (RSI) stands at 36, signaling a bearish outlook for this pair.

The U.S. dollar regained strength against major counterparts on Tuesday.

Supported by higher U.S. Treasury yields, market expectations for a March interest rate cut fell below 59%, down from 77% just one day prior.

Fed Governor’s Comments:

Fed Governor Christopher Waller’s statement suggested a cautious approach, indicating that the Federal Open Market Committee (FOMC) doesn’t need to ease its stance as rapidly as in the past.

This stance contributed to the strengthening of the U.S. dollar.

Currency Performance:

Euro, British pound, and Australian dollar experienced sharp declines against the U.S. dollar.

Notable thresholds were breached during this pullback.

Fed March Meeting Probabilities:

The probability chart from CME Group highlights the diminishing likelihood of a rate cut in March.

EUR/USD Technical Analysis:

EUR/USD exhibited a decline, breaking the lower boundary of a short-term rising channel at 1.0930.

The pair moved towards the 200-day simple moving average, a crucial support at just above 1.0840.

Maintenance of this support is imperative; failure may lead to a retracement towards 1.0770.

If downward pressure eases and prices rebound, technical resistance is anticipated at 1.0930, followed by 1.1020.

Further strength could shift focus to 1.1075/1.1095 and subsequently 1.1140.

STOCK MARKET ANALYSIS:

Market Overview:

US stocks encountered challenges on Tuesday as investors remained attentive to the trajectory of interest rates.

The lackluster start to the earnings season, particularly with big bank results, influenced market sentiment.

Performance Indicators:

Dow Jones Industrial Average (^DJI) concluded the session down 230 points, influenced notably by Boeing’s (BA) negative performance (-7.89%).

S&P 500 (^GSPC) experienced a 0.4% decline.

Nasdaq (^IXIC) closed slightly lower despite intermittent shifts into positive territory, driven by movements in chipmakers Nvidia (NVDA) and Advanced Micro Devices (AMD).

Key Stock Movements:

Goldman Sachs (GS) stock edged slightly higher following a reported fourth-quarter earnings increase of 51% year over year.

Morgan Stanley (MS) shares dipped up to 4% during the session but posted fourth-quarter revenue that exceeded Wall Street expectations.

Upcoming Retail Sales Report:

Investors await Wednesday’s retail sales report, anticipating its impact on the Federal Reserve’s data-driven policy decisions.

Last week’s unexpected cooling in US wholesale inflation increased hopes for a potential interest rate cut in March.

Fed Governor’s Perspective:

Fed Governor Chris Waller expressed belief in the Fed’s ability to lower interest rates in the coming year, contingent on inflation remaining in check.

He emphasized that the timing and extent of rate cuts will hinge on incoming economic data.

Corporate Developments:

A federal judge intervened in the merger deal between Spirit Airlines (SAVE) and JetBlue (JBLU) due to antitrust concerns.

Spirit Airlines faced a significant 47% drop in its stock value following the news of the blocked merger.

Overall Sentiment:

The market remains cautious and attentive to various factors, including corporate earnings, interest rate expectations, and economic data, influencing trading decisions and overall sentiment.

In the shadows of the 17th-century Amsterdam, a groundbreaking financial experiment unfolded, forever altering the course of economic history. The year 1602 saw the birth of the Amsterdam Stock Exchange, a brainchild of the Dutch East India Company, marking the world’s inaugural official stock exchange.

The Amsterdam Stock Exchange source: The Low Countries

Under the canopy of a buttonwood tree on Wall Street, 24 stockbrokers laid the groundwork for organised securities trading, introducing the novel concept of issuing shares to the public.

Fast forward to today, where the once humble origins have burgeoned into a global financial behemoth. With a staggering size surpassing $100 trillion, the modern stock market stands as a testament to the enduring legacy of those early investors and the evolution of financial markets through centuries.

Whether you’re a novice or a seasoned investor, understanding the basics is key to navigating the complexities of the stock market. In this comprehensive guide, we’ll delve into the essentials of stocks and Share CFDs, with a special focus on popular trading strategies.

source: ABC News

Stocks: Unlocking Ownership and Dividend Potential

At its core, a stock symbolises ownership in a company, with popular names like Apple (AAPL), Microsoft (MSFT), Amazon (AMZN), and Google’s Alphabet (GOOGL) exemplifying this ownership’s profound impact. Investors holding these stocks actively participate in globally influential companies.

Beyond theoretical ownership, shareholders hold significant rights. This includes voting on corporate decisions and attending pivotal annual shareholder meetings, allowing active engagement in corporate governance.

Stock ownership’s allure extends to the potential for dividends, a feature prominent in dividend-paying stocks like Johnson & Johnson (JNJ), Coca-Cola (KO), Procter & Gamble (PG), and McDonald’s (MCD). These stocks appeal to investors seeking a steady income stream, enhancing the overall return on investment.

In essence, owning stocks aligns investors with a company’s success and prosperity. It’s not just financial; it’s a connection to brands and businesses shaping our daily lives. Investors in these well-known companies become integral contributors to ongoing success and innovation in the business world.

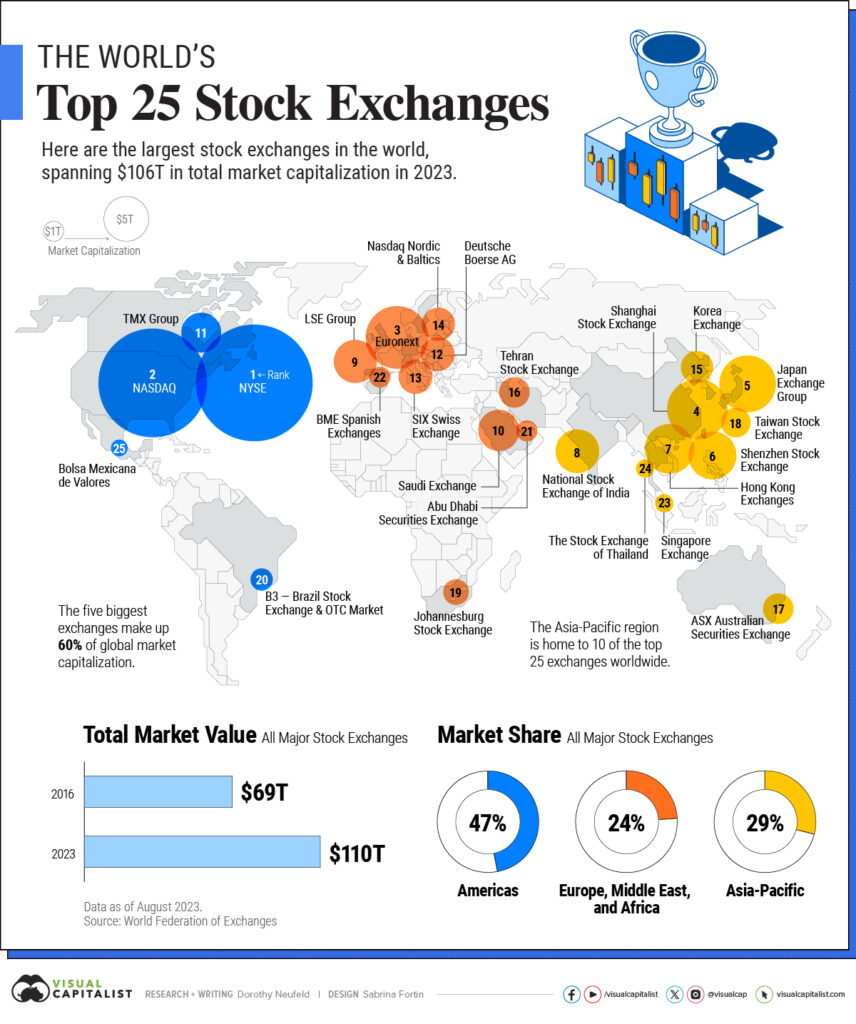

Stock Exchanges: The Pulsating Heart of Global Trading

Major stock exchanges worldwide serve as the epicentres where the world’s most influential stocks are bought and sold, shaping the landscape of global finance. Two giants stand out in this domain – the New York Stock Exchange (NYSE) and NASDAQ.

The Largest Stock Exchanges in the World 2023 source: Visual Capitalist

The New York Stock Exchange (NYSE), located on Wall Street in New York City, is the largest and most prestigious stock exchange globally. It boasts a rich history dating back to 1792, providing a platform for some of the most prominent and established companies.

NASDAQ, on the other hand, is renowned for its technology-focused listings and electronic trading platform. Born in 1971, it has become synonymous with innovation and hosts many of the world’s leading technology companies.

In Europe, the London Stock Exchange (LSE) stands as a financial powerhouse, hosting a diverse array of companies. Meanwhile, the Euronext group, spanning Amsterdam, Brussels, Dublin, Lisbon, Milan, and Paris, plays a pivotal role in European trading.

Turning our attention to Asia, the Tokyo Stock Exchange (TSE) in Japan and the Hong Kong Stock Exchange (HKEX) command significant influence. These exchanges contribute to the vibrancy and dynamism of the Asian financial markets.

These exchanges are more than mere facilitators; they are the driving forces shaping stock prices globally. The dynamic interplay of supply and demand on these platforms directly influences the valuation of stocks.

Understanding the mechanics of stock exchanges, particularly the NYSE and NASDAQ, is essential for investors seeking to decipher the intricate forces that shape market trends and individual stock prices. As investors, being attuned to the activities on these exchanges equips us to navigate the complexities of the global financial arena.

Stocks and Other Financial Instruments: Navigating the Financial Landscape

In the expansive realm of financial instruments, it’s vital to differentiate between various assets. Beyond stocks, investors encounter bonds and Exchange-Traded Funds (ETFs), each with its unique characteristics.

Bonds, in contrast to stocks, represent debt rather than ownership. When an investor buys a bond, they are essentially lending money to a company or government entity. In return, the bondholder receives periodic interest payments and the eventual return of the principal amount.

Exchange-Traded Funds (ETFs), on the other hand, are investment funds that trade on stock exchanges. ETFs offer a diversified investment approach by bundling together a collection of stocks, bonds, or other assets. They provide investors with a way to gain exposure to a broad market or sector without directly owning individual securities.

Understanding these financial instruments allows investors to tailor their portfolios to match their risk tolerance, investment goals, and preferences.

Stocks vs Share CFDs: Navigating Investment Avenues

Share CFDs, or Contracts for Difference, are financial derivatives that allow traders to speculate on the price movements of underlying stocks without actually owning the shares.

Unlike traditional stock trading, where investors physically buy and own shares in a company, CFDs are contracts between traders and brokers.

The derivative nature of CFDs lies in their ability to derive their value from the underlying asset, in this case, stocks. This derivative structure opens up a world of advantages for traders, enabling them to profit from both rising and falling markets.

Advantage 1: Leverage

One of the key advantages of share CFDs is the ability to trade with leverage. Leverage allows traders to control a larger position size with a smaller amount of capital. While this magnifies potential profits, it’s crucial to note that it also amplifies potential losses. This feature makes CFDs an attractive choice for traders seeking to maximise their market exposure without the need for a substantial upfront investment.

Advantage 2: Short Selling

Share CFDs provide a unique opportunity for traders to profit from falling prices through short selling. In traditional stock trading, short selling is often complex and may involve borrowing shares, but with CFDs, this process is streamlined. Traders can take advantage of market downturns by selling CFDs on stocks they anticipate will decline in value, potentially yielding profits even in bearish market conditions.

Advantage 3: Diversification

Diversification is a cornerstone of sound investment strategy, and share CFDs offer a compelling way to achieve it. With CFDs, traders can access multiple assets with a smaller capital requirement compared to traditional stock trading. This not only enhances risk management but also provides the flexibility to explore diverse markets and sectors.

If you’re an active, short-term trader seeking flexibility and leverage, share CFDs are ideal. Designed for day and swing traders comfortable with increased risk, CFDs allow you to profit in both rising and falling markets. With 24/5 trading, global market exposure, and lower transaction costs, they suit those wanting diverse opportunities.

Share CFDs Trading Tips: A Strategic Approach

Engaging in share CFDs trading demands a strategic mindset. To streamline your approach, focus on these five essential tips:

1. Thorough Research: Prioritise in-depth research on underlying assets, staying informed about market trends, company performance, and global economic factors.

2. Effective Risk Management: Set clear stop-loss and take-profit levels to manage risks diligently. Discipline in risk management is crucial in the unpredictable world of CFD trading.

3. Understand Leverage: Use leverage judiciously, considering its impact on both profits and potential losses. Avoid excessive leverage to mitigate significant financial risks.

4. Stay Informed: Regularly check economic calendars and major market events. Earnings reports, economic indicators, and geopolitical developments can significantly influence asset prices.

5. Continuous Learning: Embrace ongoing education to stay current on market trends, trading strategies, and industry developments. A commitment to learning enhances trading proficiency and adaptability over time.

Incorporating these key tips into your trading strategy will provide a solid foundation for navigating the dynamic landscape of Share CFDs with confidence.

Trading Share CFDs with VT Markets

Discover a wealth of share CFDs trading opportunities with VT Markets, offering access to over 800 leading companies from the US, UK, EU, and Hong Kong.

Leverage up to 20:1 to maximise your trading potential, taking both long and short positions for as low as $0 per trade. This flexibility empowers you to profit from fluctuations in share prices, whether they rise or fall.

Ready to embark on live trading? Open a live trading account with VT Markets for real-time market access. If you’re still refining your strategies, take advantage of the risk-free demo account. Test your approaches and get acquainted with the platform before committing real capital.

VT Markets provides a user-friendly experience for traders of all levels, ensuring you have the tools needed to navigate the dynamic world of share CFDs with confidence.

In conclusion, success in trading stocks and share CFDs demands a strategic approach, disciplined risk management, and continuous learning. Whether you prefer traditional stocks or the flexibility of CFDs, confidence stems from knowledge and a well-crafted strategy. Happy trading!

On Tuesday, the Dow Jones Industrial Average faced a 0.62% dip, closing at 37,361.12, influenced by increased bond yields and mixed fourth-quarter earnings. Boeing shares plummeted 7.9% due to a Wells Fargo downgrade, while AMD soared 8.3% on a positive semiconductor demand outlook. Goldman Sachs outperformed profit expectations, boosting its shares, while Morgan Stanley saw a 4% decline despite revenue beats. The USD index rose by 0.75%, driven by higher U.S. Treasury yields and shifting Fed rate expectations. Currency pairs experienced notable movements, with EUR/USD dropping 0.76%, USD/JPY rising by 1%, and GBP/USD weakening. In the cryptocurrency landscape, BTC rose 1.4%, ETH increased by 2.2%, and gold fell 1% following SEC approval of spot ETFs and market focus on ether spot ETF approvals.

Stock Market Updates

The stock market experienced a decline on Tuesday, with the Dow Jones Industrial Average dropping 0.62%, closing at 37,361.12. Bond yields increased, contributing to the negative sentiment as investors examined fourth-quarter earnings. Boeing shares fell sharply by 7.9% following a downgrade by Wells Fargo, citing ongoing issues with its 737 Max 9 model. On a positive note, AMD shares surged 8.3% due to optimistic analyst commentary on semiconductor demand. The benchmark 10-year Treasury note yield rose over 11 basis points to 4.064% after Federal Reserve Governor Christopher Waller hinted at a slower-than-expected easing of monetary policy.

In the banking sector, Goldman Sachs reported better-than-expected profit and revenue, causing a slight increase in its shares, while Morgan Stanley posted a revenue beat but saw a decline of over 4%. Overall, 78% of the roughly 30 S&P 500 companies reporting fourth-quarter results have exceeded earnings expectations. Investors are now anticipating December retail sales data, set to be released on Wednesday, which could impact market sentiment based on U.S. consumer spending trends and concerns about economic growth.

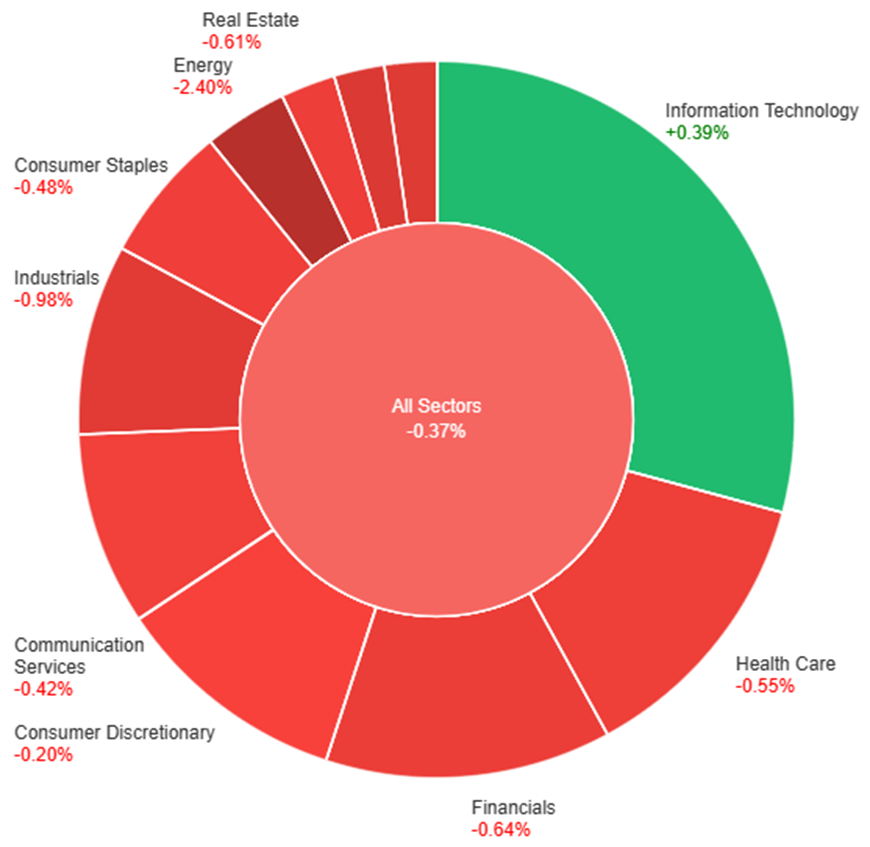

On Tuesday, the overall market experienced a slight decline of 0.37%. The Information Technology sector saw a positive movement with a gain of 0.39%, while Consumer Discretionary showed a modest decrease of 0.20%. Communication Services and Consumer Staples both experienced declines of 0.42% and 0.48%, respectively. Health Care, Real Estate, and Financials also saw negative trends with decreases of 0.55%, 0.61%, and 0.64%, respectively. Industrials faced a more significant downturn with a decline of 0.98%. The Utilities and Materials sectors both exhibited larger decreases of 1.05% and 1.19%, respectively. Energy witnessed the most substantial decline among all sectors, with a notable decrease of 2.40%.

Currency Market Updates

In the latest currency market updates, the USD index surged by 0.75%, driven by rising U.S. Treasury yields and a shift in Fed rate expectations. Governor Christopher Waller’s comments acknowledging the potential for rate cuts tempered extreme dovish sentiments, contributing to the rally. The 5-30-year Treasury yields rose, bolstering the dollar, while less-dovish ECB comments and higher Canada CPI played roles in shaping the session. Despite the increase in long-end Treasury yields, there remains a 68% chance of a 25bp Fed cut in March, indicating a nuanced market sentiment. Notably, the EUR/USD pair declined by 0.76% to 1.0870, reflecting the impact of less-dovish ECB central bank comments on the euro, amidst concerns about euro zone growth.

In parallel, other currency pairs saw notable movements. USD/JPY rose by 1% to 147.25, driven by higher Fed rate expectations and a consistently low BoJ rate outlook. GBP/USD weakened due to the less-dovish Fed rate view, although the impact was relatively muted given higher UK inflation and rate expectations. Focus now shifts to the UK CPI data, with potential implications for the BoE’s rate decisions. USD/CAD rose by 0.43%, reaching 1.3484, but gains were tempered by stronger-than-expected Canada CPI, diminishing expectations for an early BoC rate cut. Additionally, AUD/USD fell by 1.2%, influenced by higher rates and concerns about global growth amid doubts regarding China’s recovery. In the broader financial landscape, BTC rose by 1.4% to $43.3k, ETH increased by 2.2%, and gold fell 1% to $2,035, reflecting market responses to SEC approval of spot ETFs and shifting focus to ether spot ETF approvals.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Suffers Sharp Decline as USD Gains Momentum Amidst Divergent Central Bank Signals and Strong US Yields

EUR/USD extended its bearish trend, breaking below the critical support level at 1.0900 and hitting a new yearly low near 1.0860. The upward momentum of the US Dollar, driven by a surge in the USD Index to 2024 peaks beyond 103.00, was reinforced by robust US yields as traders returned from the MLK holiday. ECB officials’ comments, though leaning towards rate cuts, clashed with market expectations, leading to a subdued EUR. Despite positive Economic Sentiment indicators in Germany and the Eurozone, the Euro failed to find support, and the probability of a Fed rate cut in March, as indicated by CME Group’s FedWatch Tool, decreased slightly. The decline in the Euro was set against the backdrop of rising yields in both German bunds and US Treasuries.

On Tuesday, the EUR/USD moved lower, able to reach the lower band of the Bollinger Bands. Currently, the price is moving just above the lower band, suggesting a potential upward movement to reach the middle band. Notably, the Relative Strength Index (RSI) maintains its position at 30, signaling an oversold outlook for this currency pair.

Resistance: 1.0895, 1.0954

Support: 1.0814, 1.0742

XAU/USD (4 Hours)

XAU/USD Faces Sell-Off Amid Interest Rate Uncertainty and Inflation Dynamics

Gold prices (XAU/USD) experienced a decline as attempts to surpass the weekly high of $2,060 fell short. This setback was triggered by investors reassessing the Federal Reserve’s potential interest rate adjustments. The release of the December Consumer Price Index (CPI) report, coupled with hawkish statements from European Central Bank (ECB) officials, influenced market sentiment. While expectations for a rate cut in March persist, the Federal Reserve remains cautious, considering the robust consumer price inflation in the U.S. economy, steady labor demand, and low recession risks. As markets await cues from upcoming data such as monthly U.S. Retail Sales, Industrial Production, and the Fed’s Beige Book, the trajectory of gold prices hinges on evolving interest rate outlooks.

On Tuesday, XAU/USD moved lower and tried to reach the lower band of the Bollinger Bands. Currently, the price moving just above the lower band suggesting a potential upward movement to reach the middle band. The Relative Strength Index (RSI) stands at 40, signaling a neutral but bearish outlook for this pair.