On Wednesday, both the S&P 500 and Nasdaq Composite closed lower, hovering near their highest closing levels since August 2022. The S&P 500 slipped by 0.38%, settling at 4,267.52, while the Nasdaq Composite declined by 1.29%, ending at 13,104.89. However, the Dow Jones Industrial Average stood out among the major averages, adding 91.74 points or 0.27% and closing at 33,665.02.

Energy emerged as the best-performing sector in the S&P 500, experiencing a rise of approximately 2.6%. Notably, the SPDR S&P Oil & Gas Exploration & Production ETF (XOP) and First Trust Natural Gas ETF (FCG) both gained over 3%. Regional banks also saw continued growth, with the SPDR S&P Regional Banking ETF (KRE) rising more than 3%. PacWest Bancorp’s shares surged by 14.4%, while Zions Bancorporation added 4.5%.

Despite the recent market rally driven by the promise of artificial intelligence and a 7% increase in the S&P 500 over the past three months, Bob Doll, Chief Investment Officer at Crossmark Global Investments, cautioned about the future impact of the Federal Reserve’s interest rate hikes. Doll pointed to ongoing concerns such as leading economic indicators declining for 13 consecutive months, an inverted yield curve, and liquidity issues. He advised caution and urged investors not to get carried away by the current rally.

Meanwhile, the U.S. trade deficit continued to rise in April, although it came in slightly below economists’ expectations. This deficit could potentially lead to lower GDP growth in the second quarter.

Data by Bloomberg

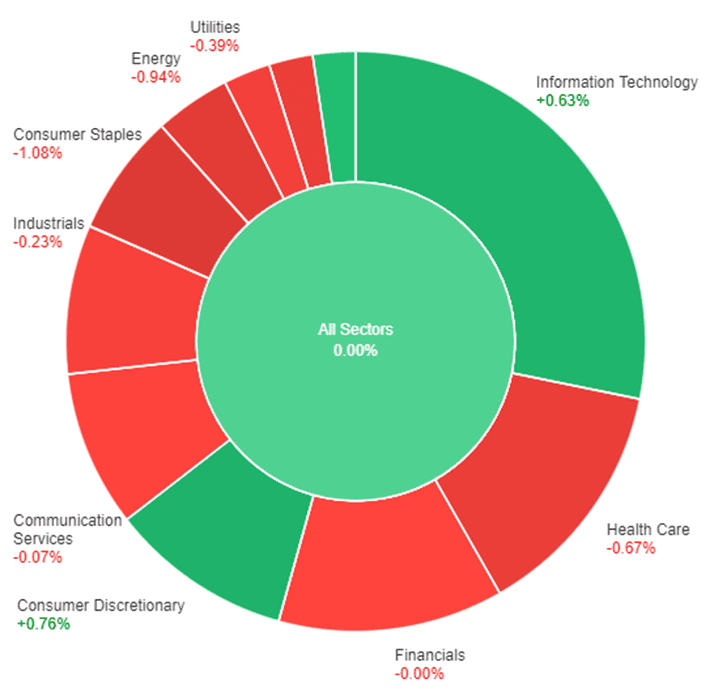

On Wednesday, the overall performance of sectors in the market showed a slight decline, with all sectors experiencing a decrease of 0.38%. However, some sectors managed to outperform the market. Energy was the best-performing sector, with a positive price change of 2.65%. Real estate and utilities also had a good day, with gains of 1.75% and 1.70% respectively. Industrials and materials followed suit with increases of 1.59% and 1.18%.

Financials had a modest gain of 0.33%. On the other hand, several sectors faced declines. Consumer staples and healthcare experienced small decreases of 0.33% and 0.41% respectively. Consumer discretionary had a larger decline of 0.91%. The worst performers were information technology and communication services, both with significant decreases of 1.62% and 1.87% respectively.

Major Pair Movement

The US Dollar Index (DXY) is facing downward pressure around 104.00 as the market balances hawkish Federal Reserve expectations with concerns about US economic growth. Despite the strong performance of US Treasury bond yields and the dollar’s safe-haven status, the index fails to reflect these positive factors.

At the same time, the EUR/USD pair is trading within a week-long Pennant formation near 1.0700, with bullish and bearish forces in contention due to fears of an economic slowdown, higher interest rates, and weaker Eurozone data.

In other currency developments, the GBP/USD pair experiences a slight upward movement but remains significantly below the previous day’s weekly peak around the key level of 1.2500. The pair finds support from the subdued performance of the US Dollar.

Similarly, AUD/USD remains low at approximately 0.6650 after retreating from a one-month high, as concerns about the Reserve Bank of Australia’s hawkish stance and worries about economic growth weigh on the Australian dollar.

Additionally, USD/CAD initially dropped to a low of 1.3318 following an unexpected interest rate hike by the Bank of Canada, marking the lowest level since May 8. However, the pair later rebounded to around 1.3400, erasing its losses, due to the overall strength of the US dollar supported by higher US yields.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Holds Steady Ahead of ECB Meeting and US Economic Indicators

The EUR/USD pair showed a mixed performance as it initially dipped close to weekly lows near 1.0645, surged to 1.0739 – its highest level since Friday – and then retraced back to the 1.0700 range. The pair remained range-bound, eagerly awaiting new catalysts and events scheduled for the following week.

The upcoming European Central Bank (ECB) meeting, where a rate hike is expected, will be a crucial event with new forecasts, shaping market expectations for July. Germany’s reported industrial production increase of 0.3% MoM in April fell short of expectations. On Thursday, a fresh estimate of Q1 Euro area GDP and employment change data will be released.

Meanwhile, the US dollar gained momentum after the Bank of Canada’s rate hike and was further supported by surging US bond yields, with the 10-year yield reaching the highest level since May 29. The focus shifts to upcoming events, including the Federal Reserve’s decision on the Fed Fund rate, as well as potential actions from the Reserve Bank of Australia and the impact of US employment data, particularly the crucial Consumer Price Index report on Tuesday and the weekly jobless claims report on Thursday.

According to technical analysis, the EUR/USD pair moved in flat on Wednesday as we can see that the upper and lower bands is getting narrower. Currently, the EUR/USD is running just above the middle band, with the potential for it to move higher and try to push the upper band of the Bollinger Bands. The Relative Strength Index (RSI) is currently at 50, indicating that the EUR/USD is in a neutral trend.

Resistance: 1.0724, 1.0766

Support: 1.0671, 1.0634

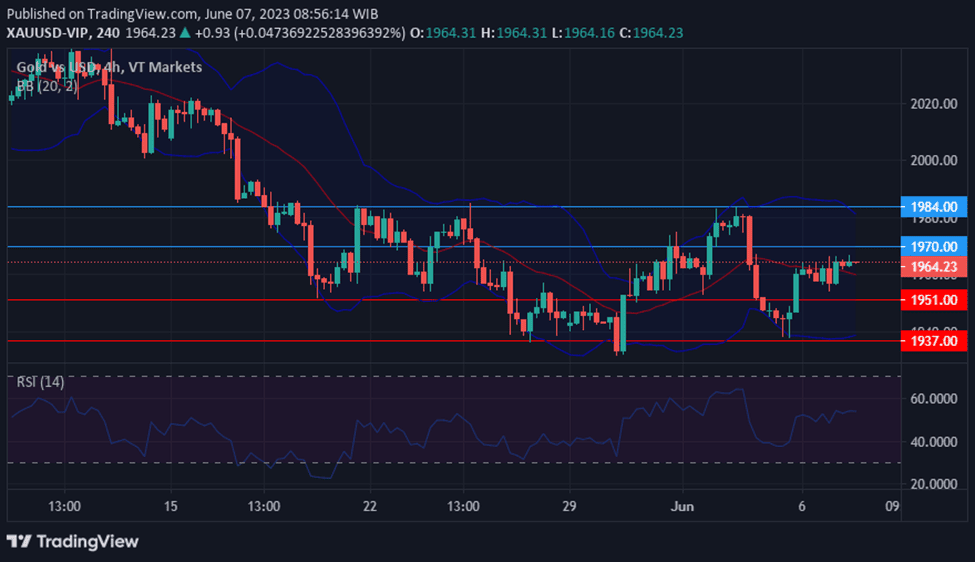

XAU/USD (4 Hours)

Gold (XAU/USD) Retreats as US Dollar Regains Strength Amid Speculation of Fed Rate Hike

Gold (XAU/USD) experienced a decline after reaching a peak of $1,970.15 per troy ounce, nearing the $1,940 level. The initial weakness of the US Dollar was reversed during the US session, as rising US government bond yields provided support. The speculation surrounding the US Federal Reserve’s potential decision to raise interest rates by 25 basis points next week favoured the USD, despite still high odds for no change. The Bank of Canada’s surprise rate hike and the Reserve Bank of Australia’s recent move cast doubt on the expected end of the tightening cycle in the US. The mixed trading of US stock indexes reflected the uncertainty surrounding the Fed’s next steps, while the 10-year Treasury note and 2-year note yields rose by 8 and 6 basis points, respectively.

According to technical analysis, the XAU/USD pair is moving higher in the early session on Wednesday but then drop to break our support level in the US session and reach the lower band of the Bollinger Bands. There is a possibility that the XAU/USD will move back higher for today and try to reach the middle band of the Bollinger Bands. Currently, the Relative Strength Index (RSI) is at 41, suggesting that the XAU/USD is in a slight bearish tone.

Resistance: $1,962, $1,970

Support: $1,937, $1,927

Economic Data

| Currency | Data | Time (GMT + 8) | Forecast |

|---|---|---|---|

| USD | Unemployment Claims | 20:30 | 236K |